source of this result ?

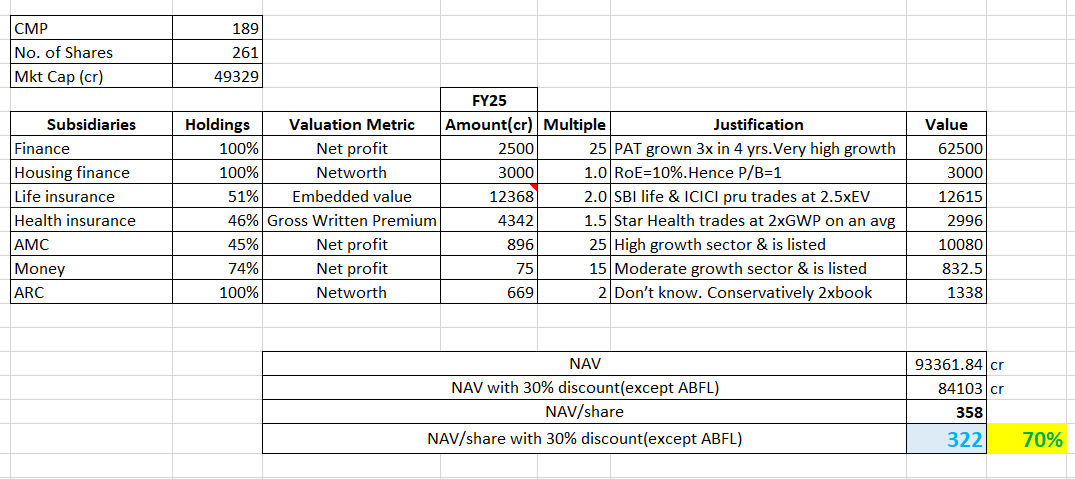

I did a Sum Of The Parts valuation with an assumption that ABFL will get merged with ABCL in next 2 yrs and hence no discount for ABFL’s value but only for other companies.

Please let me know the feedback.

3 Likes

Wondering what would be the thoughts of assigning P/E Multiple of 25 Times to ABFL other than PAT growth. How about considering P/B multiple and compare it with peers operating in same segment.

2 Likes

Even on P/B this stock should trade between 2.5 to 3. Its a long hold in my portfolio and increased stake by 70% after latest results. Vishaka Muley playing her cards she is known for. She developed ICICI Bank Credit operations. Especially for NBFC its important to bet on Jocky than horse. Fair targets post NBFC tag should be 350 approx.

3 Likes

ABFL’s revenue and profit were 1780 cr and 270 cr respectively in FY15. Now in FY25, they are expected to be 14500 cr and 2500 cr resp. These are 23% and 25% of revenue & profit growth CAGR. So it deserves 25 P/E (assuming conservatively a 12-15% CAGR in next 10 yrs).

I think its a mistake not to assign PE for financial stocks. I did not buy HDFC bank for a decade because it was trading at 4 PB but if i had considered PE, it was cheap (23 PE mostly for 20% CAGR).

@Gaurav_Catalyst What else could be the criteria to assign P/E other than PAT growth and NPA? If NPA is stable, P/E is the right way to value and not P/B.

2 Likes

In NBFC space, considering the recent actions of RBI (on Banks, NBFC, MFI etc.) - expecting a stock to trade at good P/E (without looking at P/B, ROE, NPA, Growth rate, etc.) would be asking too much. On stable NPA, for sure level of NPA’s are not that much what we have seen in past at industry level.

1 Like

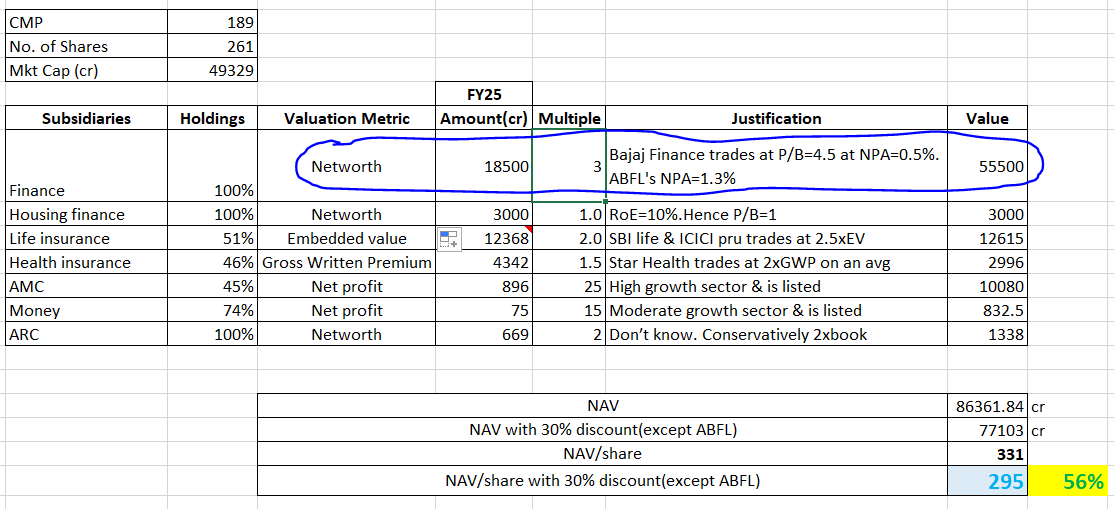

Considering P/B valuation for ABFL, i arrive at following valuation

Right now, based on ABCL mkt cap, i think market has assigned P/B=1.5 to ABFL which is too low for company that grows at 25% consistently. Unless market knows something terrible that is going to be realized in the next 2 years, this valuation is not justifiable or it can continue to trade at P/B=1.5 without any rerating but still can deliver a return equal to the NBFC’s networth growth (25% now) to the investors.

9 Likes

AB Capital is always linked to Vodafone Idea, markets have fear that Birla group may involve AB Capital for corporate guarantees of Idea which was a sinking ship but chances of revival are bright now. KM already clarified multiple times that No Birla group companies will be involved for Idea resolution also Birla has a minor holding of less than 8% now. Logically that factor is also discounted. Its rerating pending now which can’t be avoided for long. Lets wait and watch

4 Likes

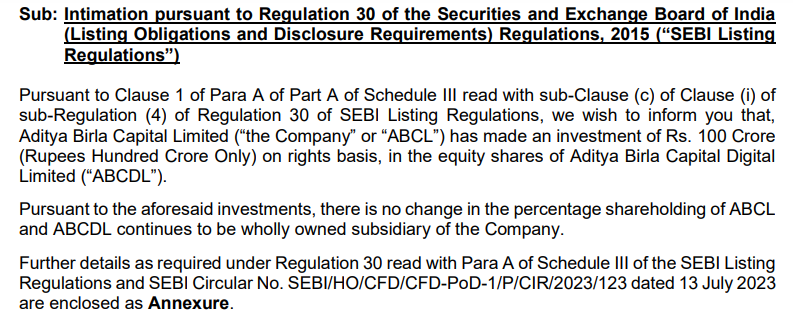

AB CAPITAL :Co. has made an investment of ₹ 100 Crore on rights basis, in the equity shares of Aditya Birla Capital Digital Limited (“ABCDL”).

1 Like

Your conviction in this seems to be a solid one.

Since last week, I am going through their some of recent concall transcript & investor presentations.

Some of the key points observed:

- Catalyst for Growth coming from two verticals mainly i.e. NBFC & HFC

- AMC stake, seems more of a liquid cash position - which can be used to encash when cash is needed to support growth of NBFC & HFC (to augment capital base)

- Insurance business can be listed in few years down the line (like edelweiss has communicated recently)

- ARC & Money (broking biz) does not seems to be focus area.

With above in mind; Growth, profitability, NPA levels, credit cost, regulatory environment, underlying economic conditions and investor sentiments around NBFC & HFC will ultimately determine the price movement in ABC share price.

Would be glad to learn & understand more details about your (or other fellow VP members) solid conviction either in favor (or against) ABC.

Disc: Not yet invested in ABC, but holding 7% of PF in Edelweiss.

6 Likes

AB Capital is a holding company rightnow, AB finance has NBFC tag, ABC has planned for amalgamation with ABF which will convert deposit taking NBFC. That will act a real trigger for P/B rerating. Expecting somewhere between 300-350 right valuation.

9 Likes

Hi,

Thank you for the information, is there any time line provided by ABCL management regarding amalgamation of ABF(Aditya Birla finance) with itself?

And as per below article ABF has to be listed in bourses by Sep 2025.

I am confused, if ABF will be amalgamated with ABCL than how it will be listed? Or by this amalgamation ABCL avoided listing of ABF? Please enlighten…

Thanks,

Deb

6 Likes

By this amalgation ABCL avoided listing of ABF.

3 Likes

ABF will cease to exist, ABCL will get NBFC tag.

3 Likes

Besides the re-rating, the holding company discount will no longer exist that can give further boost to the share price, imo.

5 Likes

Hi,

Aditya Birla Capital becomes first BFSI firm to offer full suite of financial services on ONDC platform

Will this result in new leg of growth?

ABC also continuing increase stake in its subsidiaries rapidly:

Thanks,

Deb

4 Likes

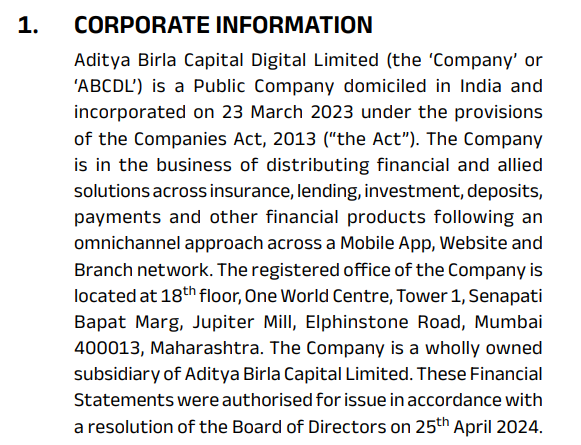

Was going through published annual account for FY2024 of this subsidiary (ABCD).

Few observations:

-

Incorporated in last week of FY2023, main business is - to be a Distributor (via app, website, branch network).

-

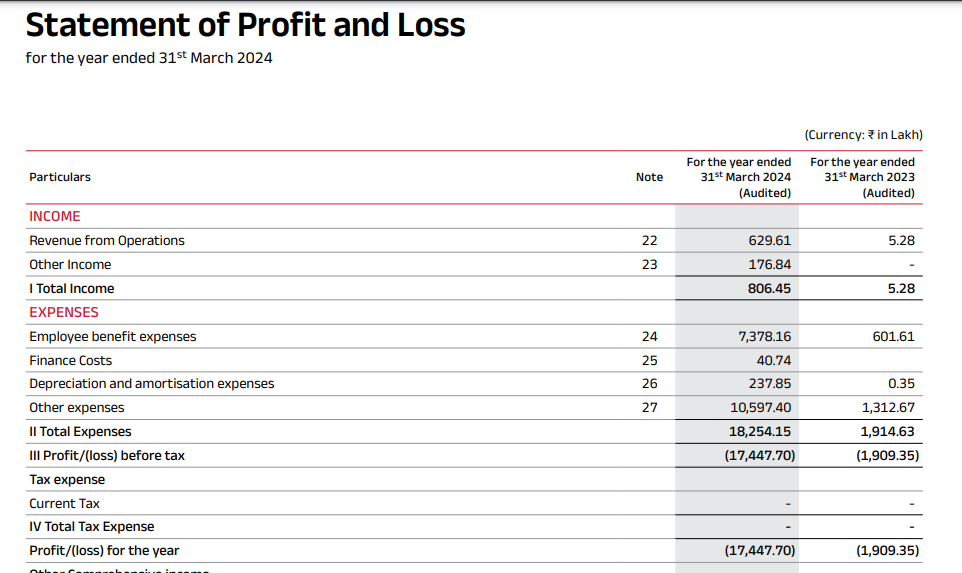

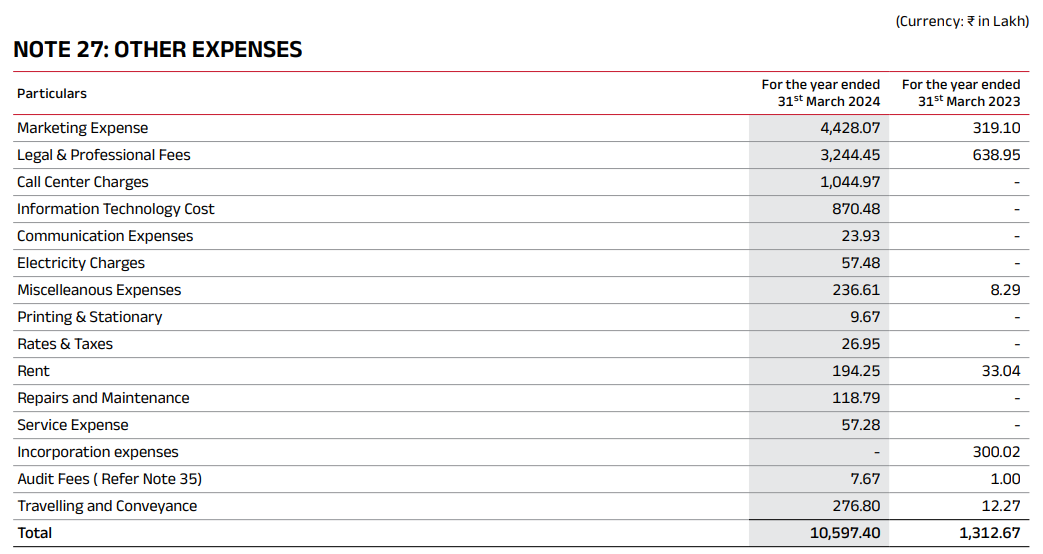

In full operational FY2024, revenue from ops (distribution) of only 6 Crores vs expenses of almost 73 Cr. on employees, 44 Crores on Marketing, 32 Crores On Legal & Professional Fees, 10 Crores on Call center etc.

- All income is from fellow subsidiaries (hence a conclusion that ABCD has been incorporated to sell ABC ecosystem products only), mainly from Aditya Birla Finance, Aditya Birla Housing Finance, and Aditya Birla Health Insurance etc.

{kind=link}

Few doubts:

-

When ABC subsidiaries have thousands of sales employees (for direct sales), 2lakh+ channel partners (like DSAs, MFDs, Insurance agents etc.), a subsidiary which is also into insurance broking (AB Insurance brokers) - Why another separate subsidiary for distribution of products.

-

Is it possible that operational costs related to Employees, Marketing, legal etc. has been booked in ABCD rather than AB Finance, AB Housing Finance etc … to showcase better operating margins in those subsidiaries ?

-

Though at consolidated profitability level it is immaterial (i.e. improved profits in 100% owned AB Finance and AB Housing Finance, and Losses in 100% owned ABCD) - but any scope of financial engineering which has been done in this whole system - Or I am reading too much into it.

-

What could be potential revenue in ABCD vs expenses … couple of year down the line … looking at their FY2024 operating expenses, it seems to me that 150-200 Crores would be bare minimum opex run rate for each subsequent years

-

Is it a remote possibility, that ABCD could also sell products of other financial products manufacturers (like banks, AMCs, Insurance Cos, NBFCs etc.) - and hence, a much larger scope for revenue & profitability.

Look forward to valuable inputs from VP forum members.

Disc: Not yet invested in ABC or any of it’s listed subsidiary, but reading in details each of them before committing any capital in CY2025.

5 Likes

Good inputs…But i think instead of delving into this digital business which is miniscule, the need of the hour is to assess the risk associated with the ongoing MFI stress.

Between FY20 and FY24, the company has grown its AUM at 22%, RoE and RoA improved from 10 to 17 and 1.7 to 2.5% respectively. On the otherhand, NNPA has decreased from 2.7 to 1.3%. So it appears we are in the best phase of the cycle.

Can this NPA be stable even at the cost of growth, RoA, etc., for the next 5 yrs? If yes, its a no brainer.

9 Likes

Hi,

Company has filled petition in NCLT for the merger of the wholly owned subsidiary Aditya Birla finance with itself on 9th January. PFA for the same.

bab3ebf4-4753-4c1c-b23a-5ce023963bcc.pdf (2.4 MB)

Surprised to see even after this potential event of rerating announcement to bourses, market is not kind enough to the stock , and it has kind of become a falling knife in recent times,almost one third of the market cap is wiped out in just a span of 3 months . Wondering what Market knows which I don’t.

Senior borders please guide!

Disclaimer: Invested in recent times,so views may be biased.Not a buy,sell recommendation.

Thanks,

Deb

7 Likes