AWL was listed on a few days back with slight discount to the IPO price and has recovered to a fair value now after a steep ~69% runup. I generally steer clear of Adani group companies however when I came across the info that this is a JV with Wilmar with 50% stake the CG risk was somewhat mitigated.

Also, I realize the IPO pricing was not at very high valuations and was worth a second look.

Introduction:

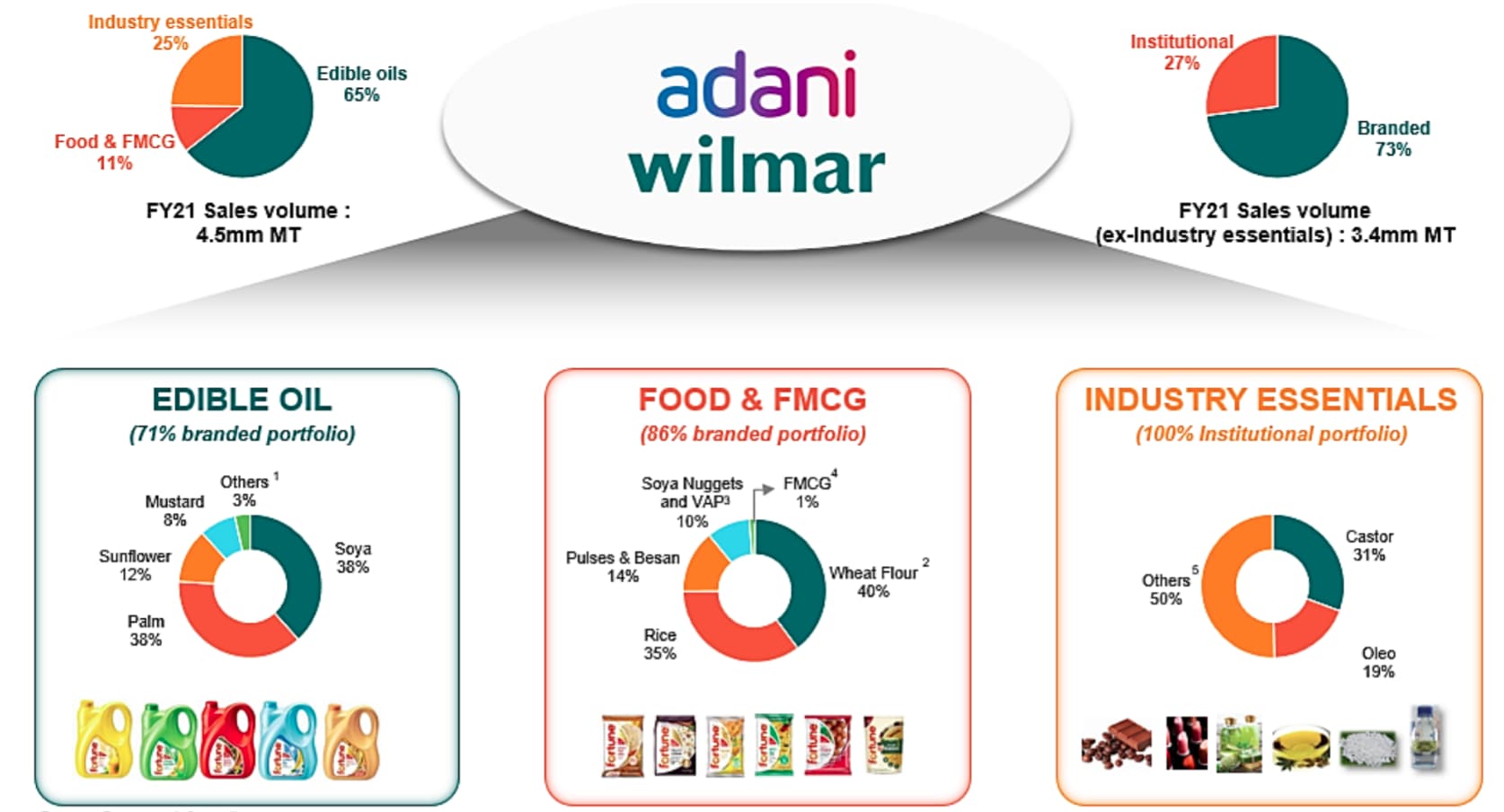

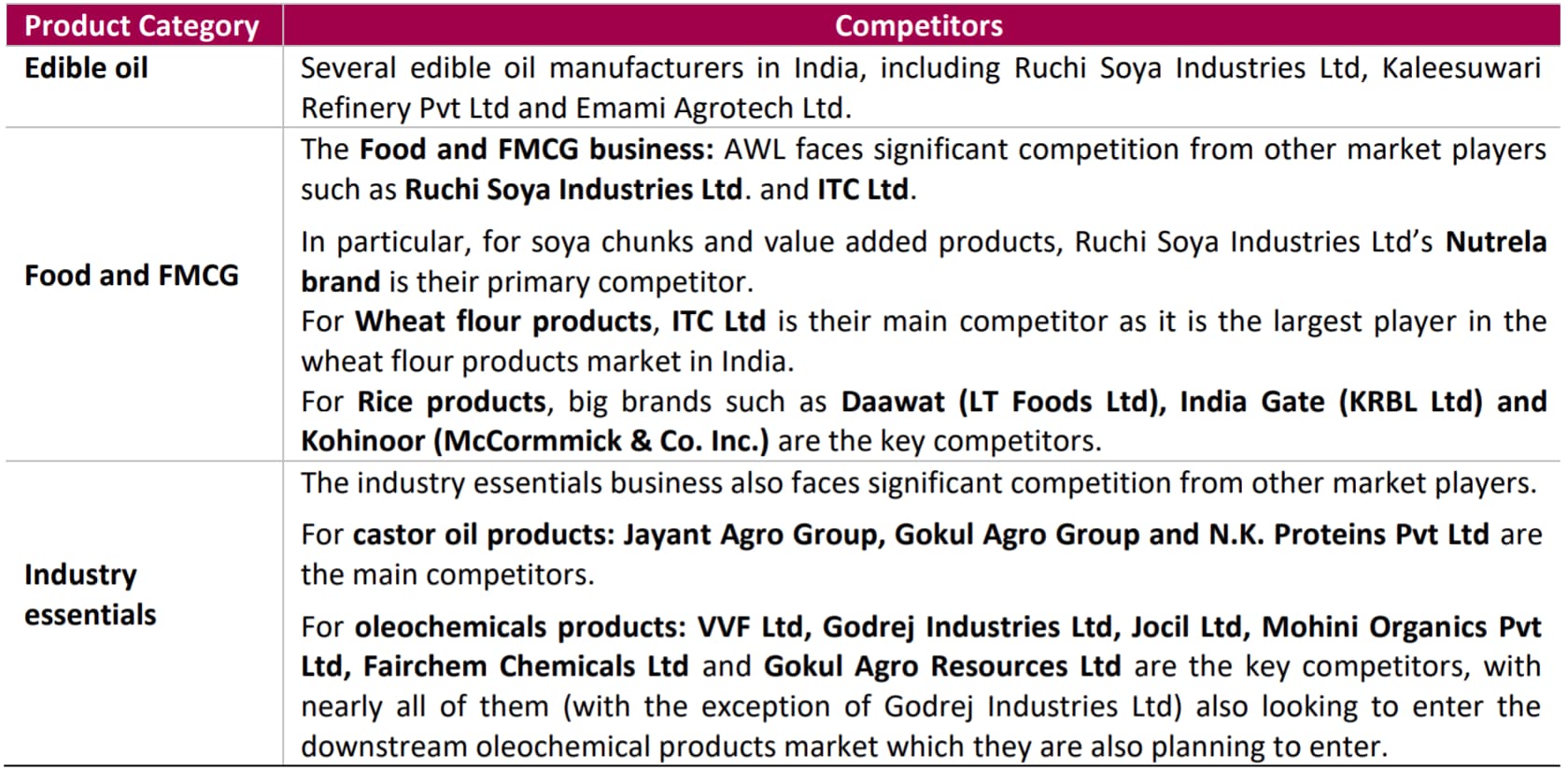

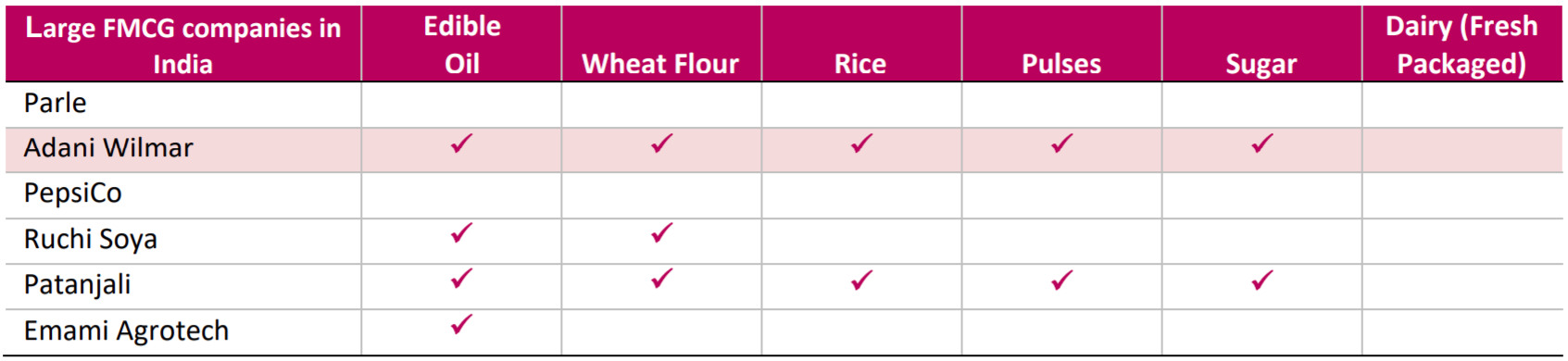

AWL a joint venture between the Adani Group and the Wilmar Group. AWL is one of the large FMCG food companies with essential kitchen commodities like edible oil, wheat

flour, rice, pulses and sugar. Products are mainly in 3 categories:

edible oil - Fortune Brand oils

packaged food and FMCG - Packaged wheat flour, rice, pulses, besan, sugar, soya

chunks and ready-to-cook khichdi etc

Industry essentials - including oleochemicals, castor oil and its derivatives and de-oiled

cakes.

Strong raw material sourcing capabilities Via Wilmar ofcourse. (India’s largest importer of crude edible oil as of March 31, 2021)

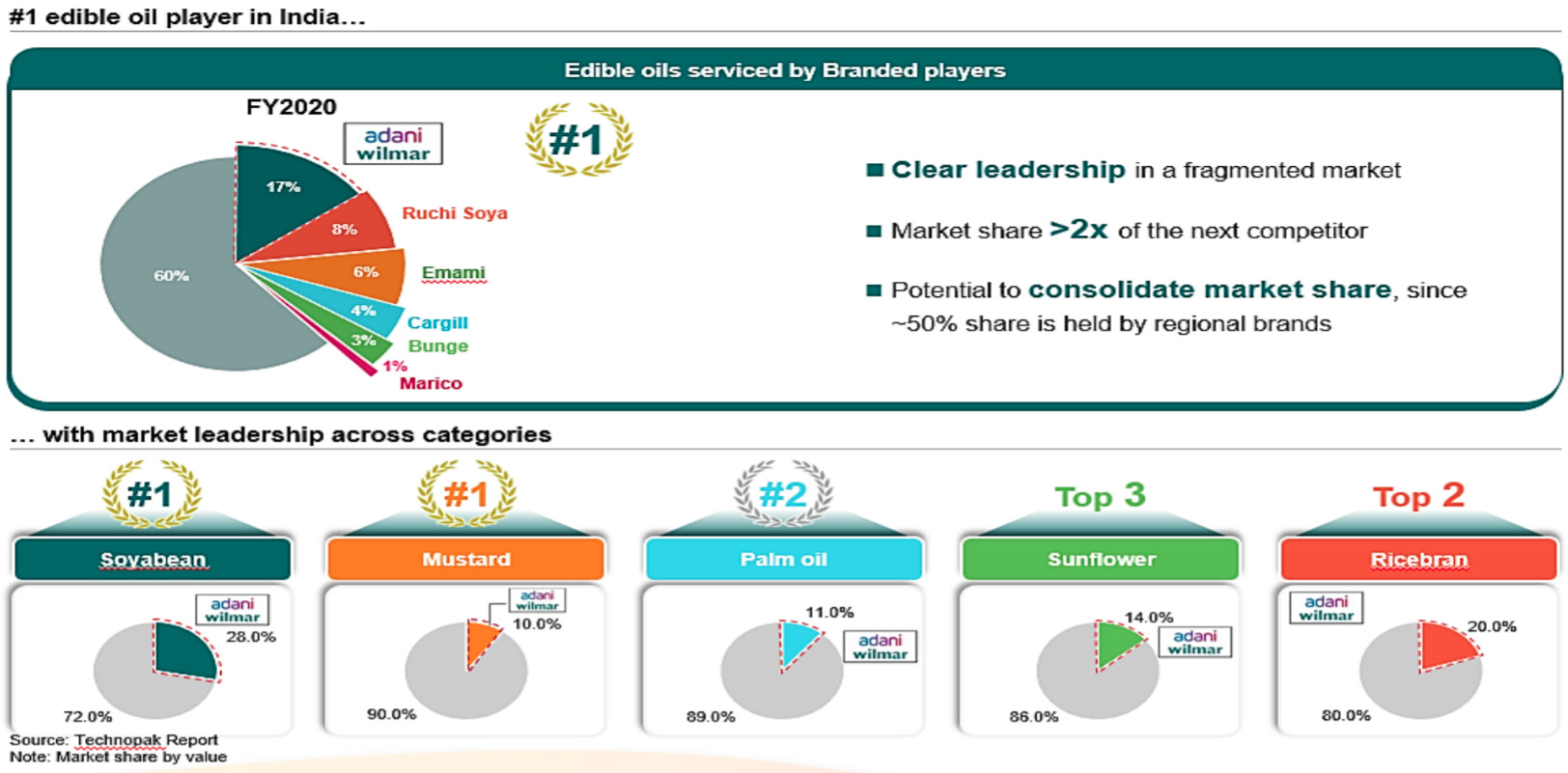

Strong Production & pan-India Distribuion - 22 plants located across 10 states, comprising 10 crushing units & 19 refineries. Refinery in Mundra is the one of the largest single location refineries in India - capacity 5,000 MTPD. They used 36 additional leased tolling units which gives them with additional manufacturing capacities. 5,590 distributors in 28 states, serving over 1.6 million retail outlets, ~35 % of the retail outlets in India.

Kuok Khoon Hong is the Non-Executive Chairman, co-founder of Wilmar International Ltd (current Chairman and CEO of Wilmar International Ltd)

Most of their crushing units are integrated with refineries to refine crude oil. They further derive de-oiled cakes from crushing and use palm stearin derived from palm oil refining to manufacture oleochemical products, such as soap noodles, stearic acid and glycerin

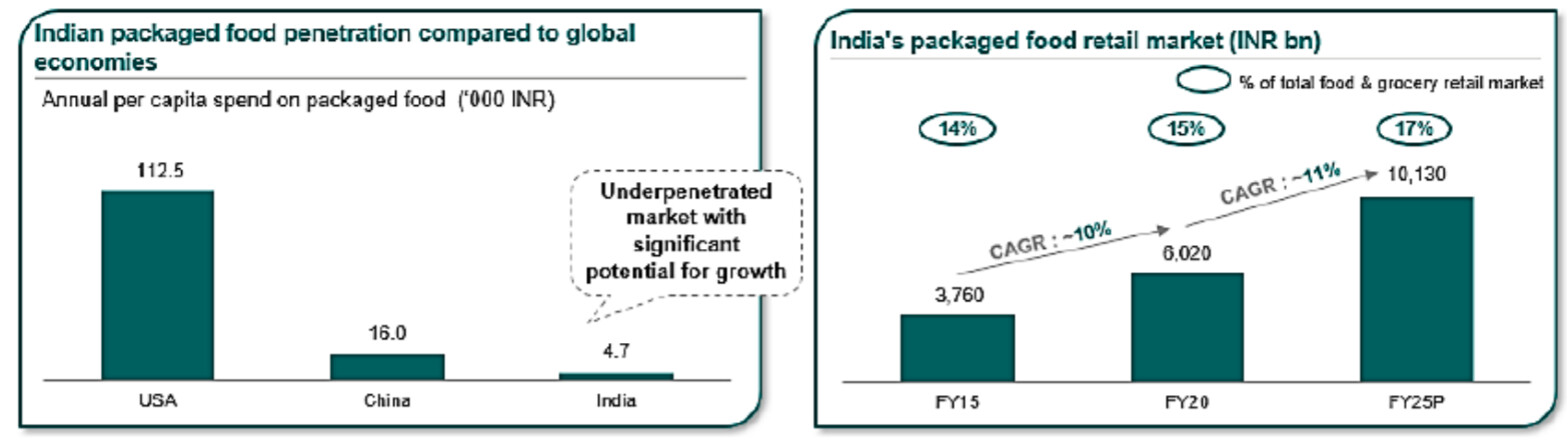

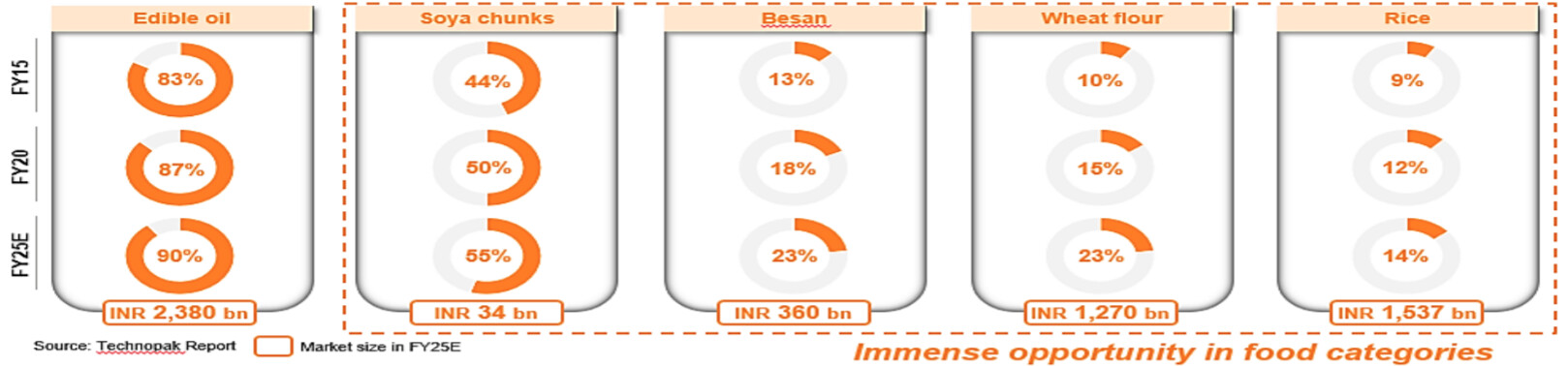

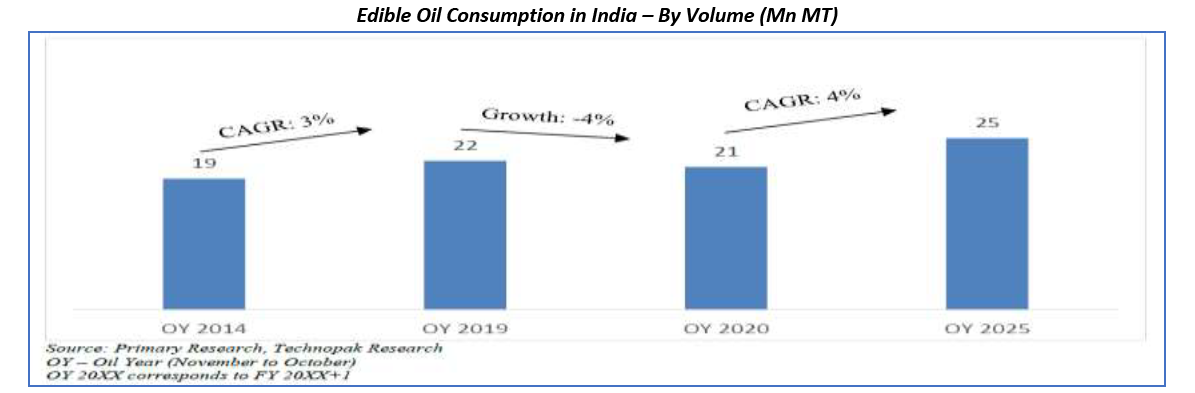

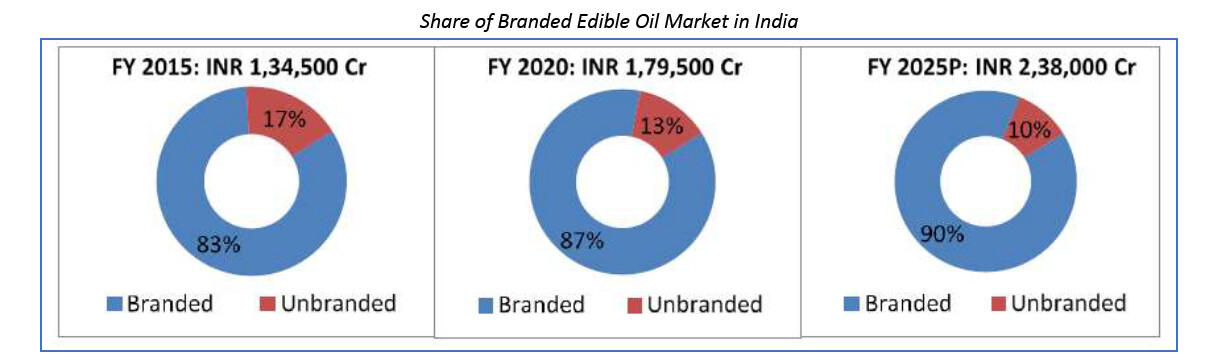

TAM - Essential commodities like edible oils, wheat flour, rice, pulses and sugar, account for ~66% of the spend on essential kitchen commodities in India. Penetration rate of packaged foods in India remains low, which provides significant potential for growth for packaged edible oil and food products.

The packaged food under-penetration in India compared to the United States and China

Castor Oil - Global export of Castor Oils has grown with a CAGR of 4% in value terms during the period CY 2015-19. India is one the biggest exporter of Castor oil with a share of 88% in global castor oil market. Industrial application, extracted majorly in India.

Adani group is involved in quite a few legal & regulatory proceedings. Huge debt in other group companies which may be an overhang if the regime changes.

Inhouse R&D team is just 12 people. With the company of this size, this seems meagre, maybe they don’t need R&D & are more or less dependent on parent wilmar.

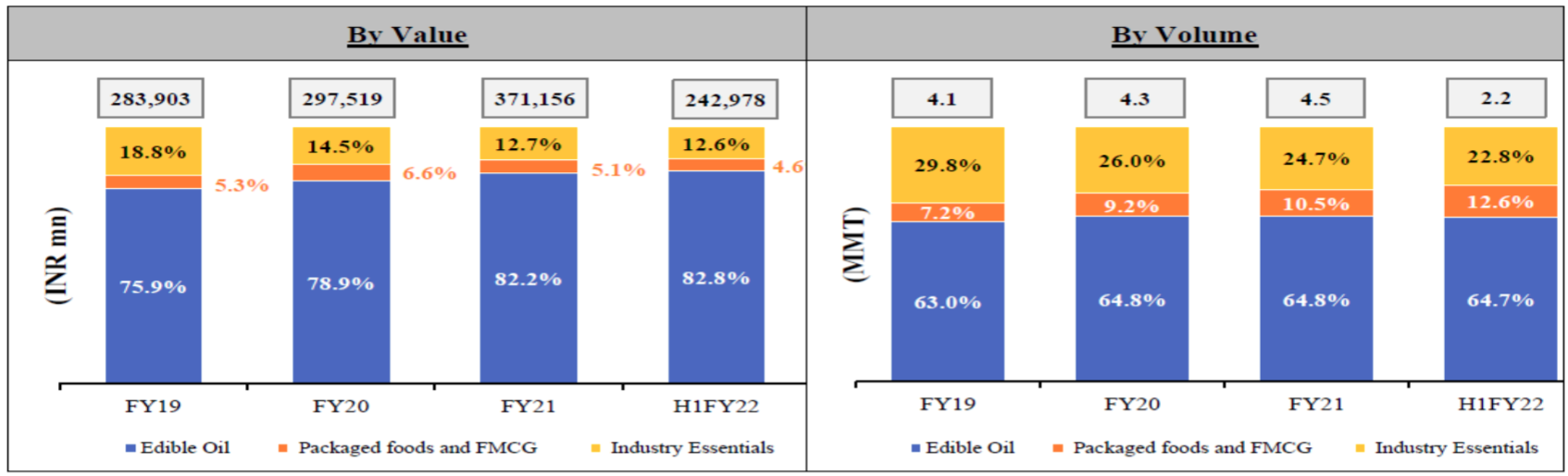

Their bread & butter is Edible oil which they seem to have perfected and due to this they operate at very low EBIDTA & PAT margins. Edible oil a very competitive product to be in & needs certain scale to remain viable.

After setting & beefing up of Fortune brand over the years they have launched many more products capitalizing the brand but havn’t created any other new brand which is as big.

Patanjali seems to b ethe closed peers in most product categories but the valuations are not available and they also are a market favorite in terms of quality & are equally price competitive.

Summary:

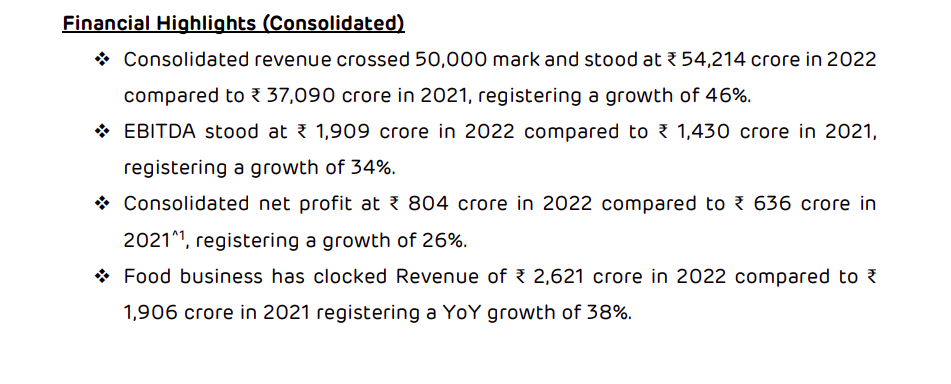

With the kind of growth & urbanization we can see decent growth in market and AWL is well placed to keep capturing market from regional & unorganized players. The IPO was priced decently at ~30 K cr Mcap comparing to H1 revenue of ~24.8 K crs it had a enough MOS for me to buy into. I think it has run up quite from the listing price & seems costly from my value perspective.

Disclosure: Holding from IPO & bought additionally on listing & will hold on for the foreseeable future…

Not sure how the target of 640/650 is being arrived here in this article. The current price run up has already made this overvalued as per me.

It’s tough to gauge the valuations basis peers as we don’t have any with similar scale. Wilmar Int. trades at 1.5X sales with similar margin profile. Not much coverage from institutions not unusual with Adani group company, Some research reports I came across recently have valued AWL less than current valuation,

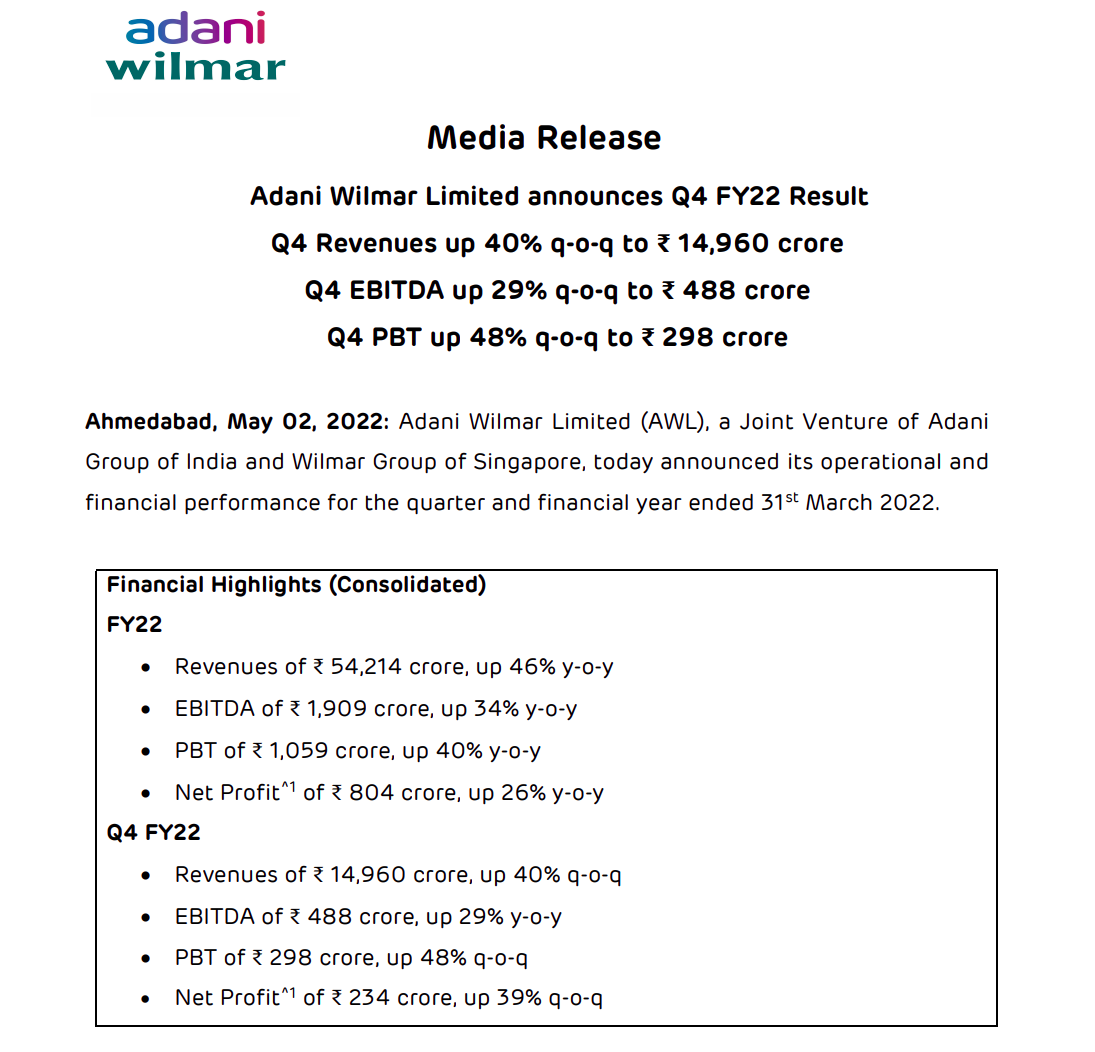

Q4 Results are expected on May 2nd '22. I do not know frankly what to expect from the results. It was an eventful qtr. and a positive surprise will be well received.

This was my first investment ever in an Adani company and I have to agree that it has been an excellent one till now. I have booked out my entire capital @ 750 and have left my profits to grow for some more time. The stock price is in definite euphoria and no estimate of the target can be provided by anyone like in all other Adani companies.

Disc:- Invested & biased, Not an investment advise. Please do your own due diligence.

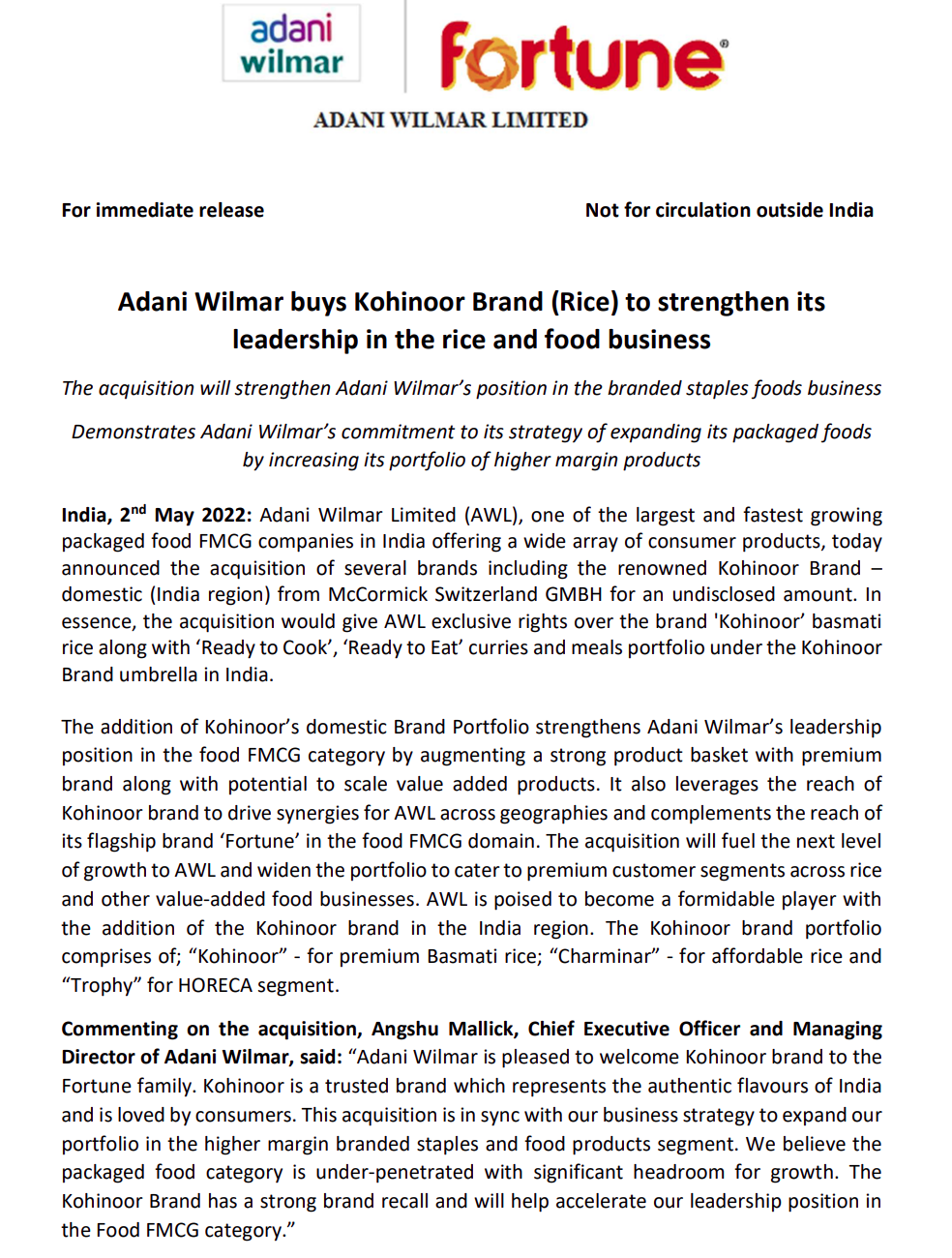

Acquistion started as indicated by the CEO in last interview with CNBC. The ongoing tailwind in the Rice Export business can be cashed in well with the help of AWL’s Distribution and Export infra.

It’s not Kohinoor Foods ltd… The company acquired by AWL is Kohinoor Specialty Foods India Pvt. Ltd… whose 100% holding is with McCormick & Company. Further the operating income of FY 21 of KSF India Pvt.Ltd is 376 cr. Out of which 75% revenue comes from Basmati Rice and rest is from other food products. It will strengthen AWL in the Domestic Rice Market.

Thanks for highlighting @shubham55 , You are right. I have corrected my post accordingly.

Can you please expand further on the Financials of KSF India Pvt ltd if you have.

Are such low margins common in this industry. Groceries might have low margins but 1.5% looks v less. A small change in expenses can bring the company in losses. How big risk it can be considering stock is trading at 120-125 PE valuation. can any one please advise.

Moderators may delete the post if it doesn’t add value in discussion. I am in learning phase.

Disc : Invested in IPO , booked profits at 718. No holdings now.

Admire that being in learning phase you held on to the IPO investment till 718 and also prudently booked profits when you saw exuberance.

I think market is factoring huge revenue increase for Adani Wilmar (sector leading) for multi years along with margin expansion. If the run rate of revenue increase continues and margin expands significantly, market may prove right so far…

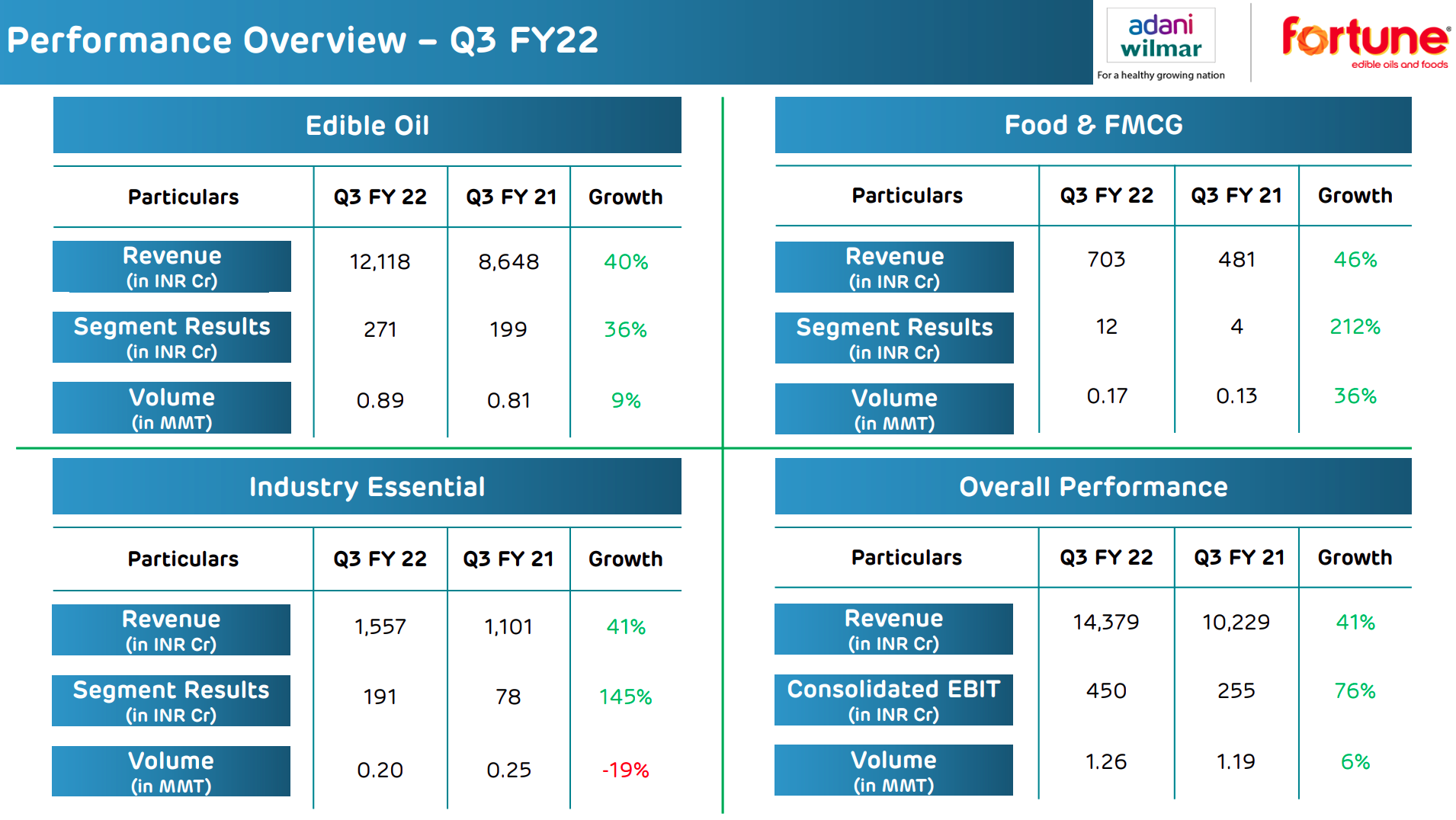

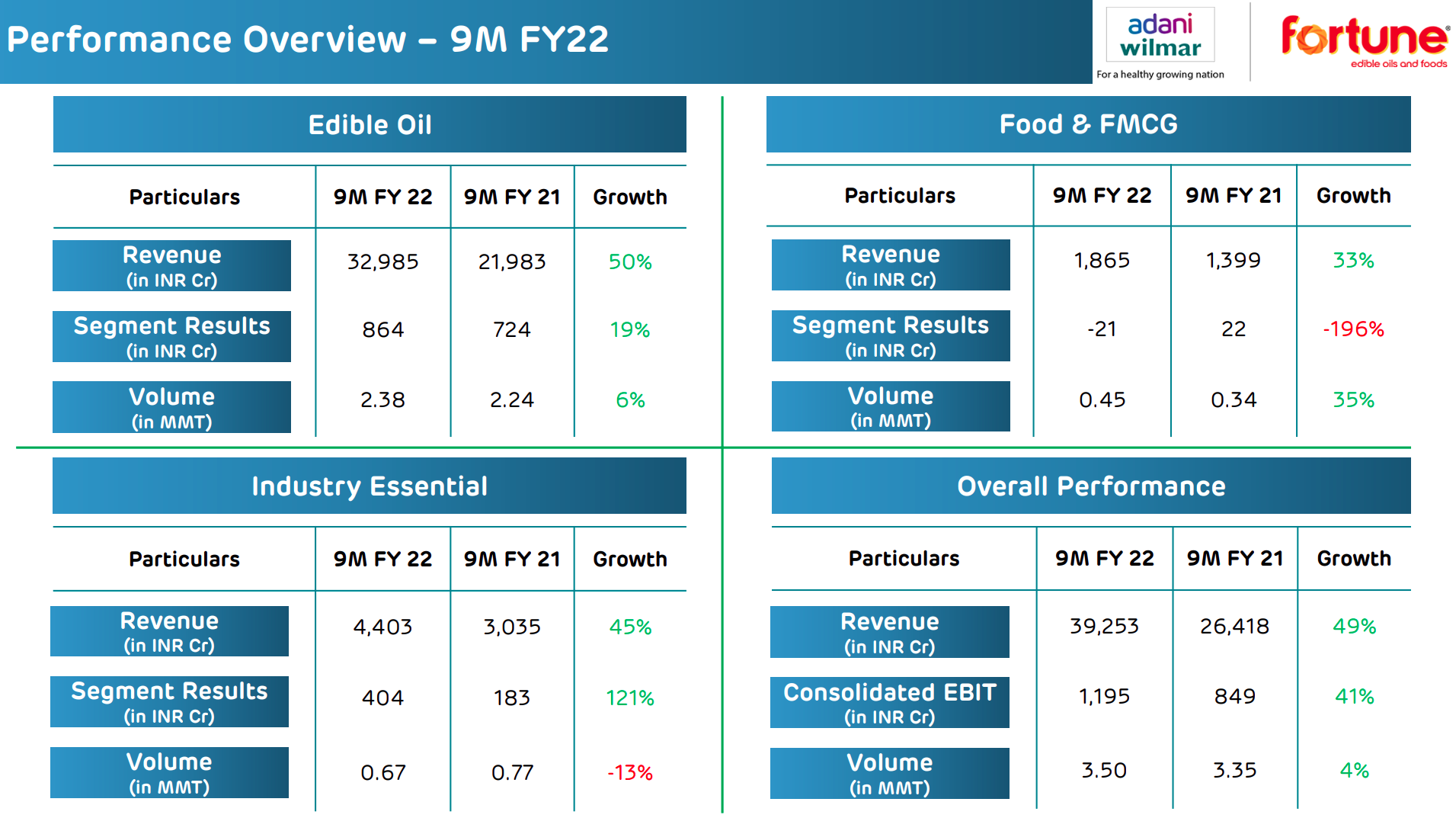

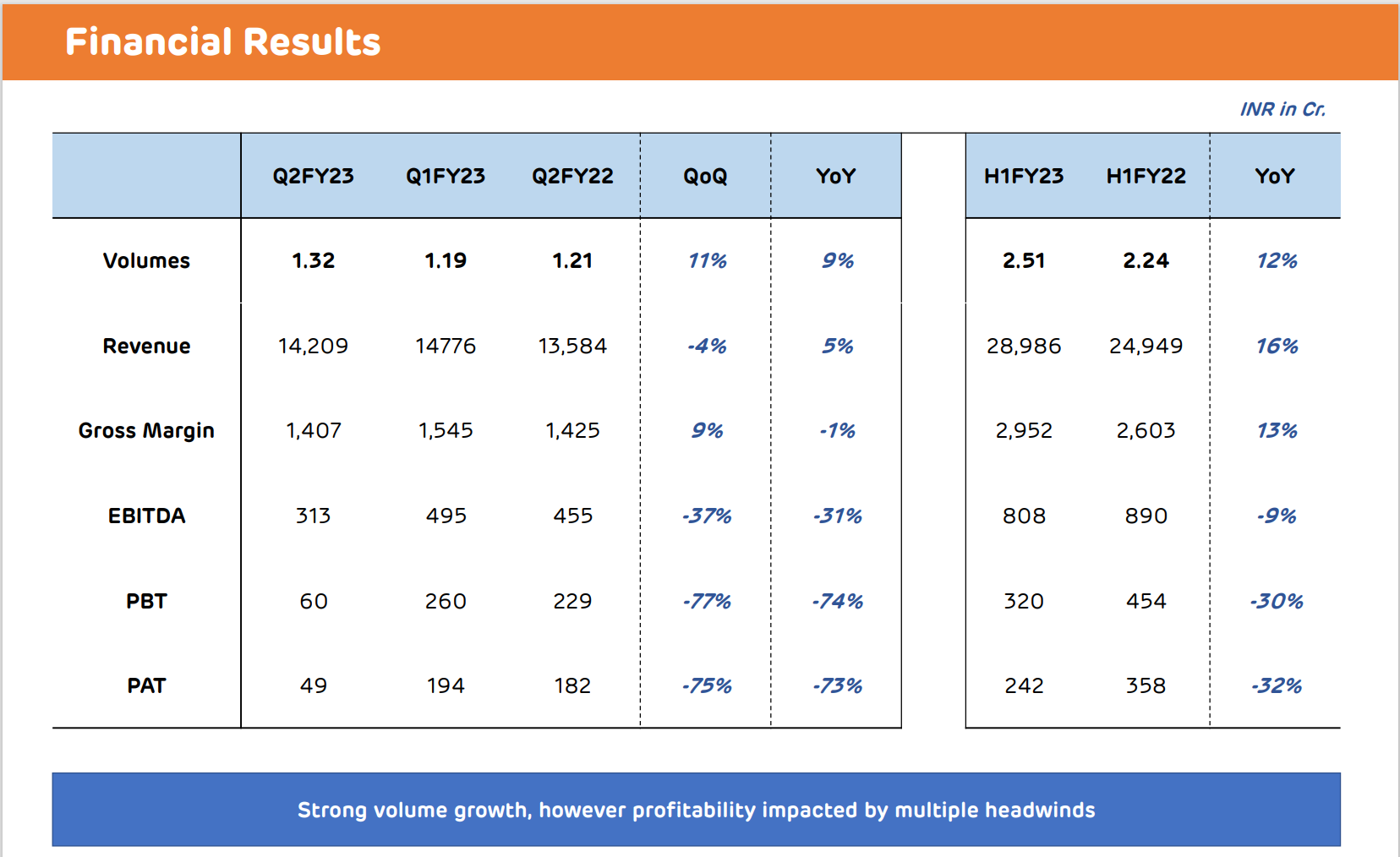

In this result, what was not so positive for me that the overall revenue growth > revenue growth of Fortune (high margin foods) portfolio. Could this be a one off because of global edible oil situation, I dont know…

Yes, It seems so. As seen in Singapore listed Wilmar international as well as its other subsidiaries. The low margin is definitely a permanent risk. Although Ameya (an IT expert and industry insider) talked about the tech stack, AWL is effectively using to optimize their operations and pricing, They will most likely be operating with a very low margin for a major part of their business. Here is the link to Ameya’s tweet.

Also, Using the well-established Fortune brand, they are expanding into other profitable products/SKUs which compliments an existing infra and supply chain, so it will gradually grow in profitability but a HUL like profitability is not expected, ever from AWL.

Along with the market expectation of expanding market share and topline expansion for AWL as indicated by @Investor_No_1 , This is also to do with being an Adani group company, as most of their free float is blocked somehow by FIIs, Atleast till they reduce the promoter holding further down as per SEBI listing rules. Low float is kind of a tricky situation and can backfire and wise investors should be able to exit the party before the music stops else can be trapped at high valuations.

This is commendable. While investing on listing day I knew it was listing cheap and bought 6% of PF, booked out my invested capital in a record 2 months’ time around 750 and left 2X Profits invested. Since this is my first Adani stock and now only a profit play for me, I am trying to maximize the returns as I expect this to show a good run like other Adani stocks as well as it has entered euphoria. This may turn out to be a decent upside for my FY23 returns or can be a bust, which we will see in time to come but I am in no hurry and willing to give it a longer rope.

Disc:- This is not an investment advice and I would myself never buy this above 1 - 1.25X topline.

Company has already informed that revenue my be in mid single digit so on revenue front it is better than expected. On profit front fall is more than expected. May be RM issue will be sorted out from Q3 onwards as hinted by the company.

Disc- personal view, invested and biased.