Explanation of decline in profits in Q4 given my management.

Abneesh Roy:

I have two questions. First, regarding the recent demand from the edible oil industry to increase import duties on refined palm oil — what’s your view on the likelihood of this happening? And how would it impact your overall margins, especially since margins this quarter were disappointing? Could this potentially affect margins going forward?

Angshu Mallick:

Regarding the duty differential between crude palm oil (CPO) and refined palmolein — currently, it’s only 7.5%. At this level, it’s actually cheaper to import refined olein and sell it, rather than importing CPO, processing it, and then selling. The industry has invested significantly in capacity, but most players are operating at only 40–45% utilization.

We’ve been urging the government to consider the “Make in India” initiative seriously, which requires at least a 15% duty differential. If that’s implemented, we can import more CPO and process it domestically. The government seems receptive — there are positive signals, and we believe action will follow. They’ve realized that benefiting the Indonesian industry isn’t useful for us, so we hope to see changes soon.

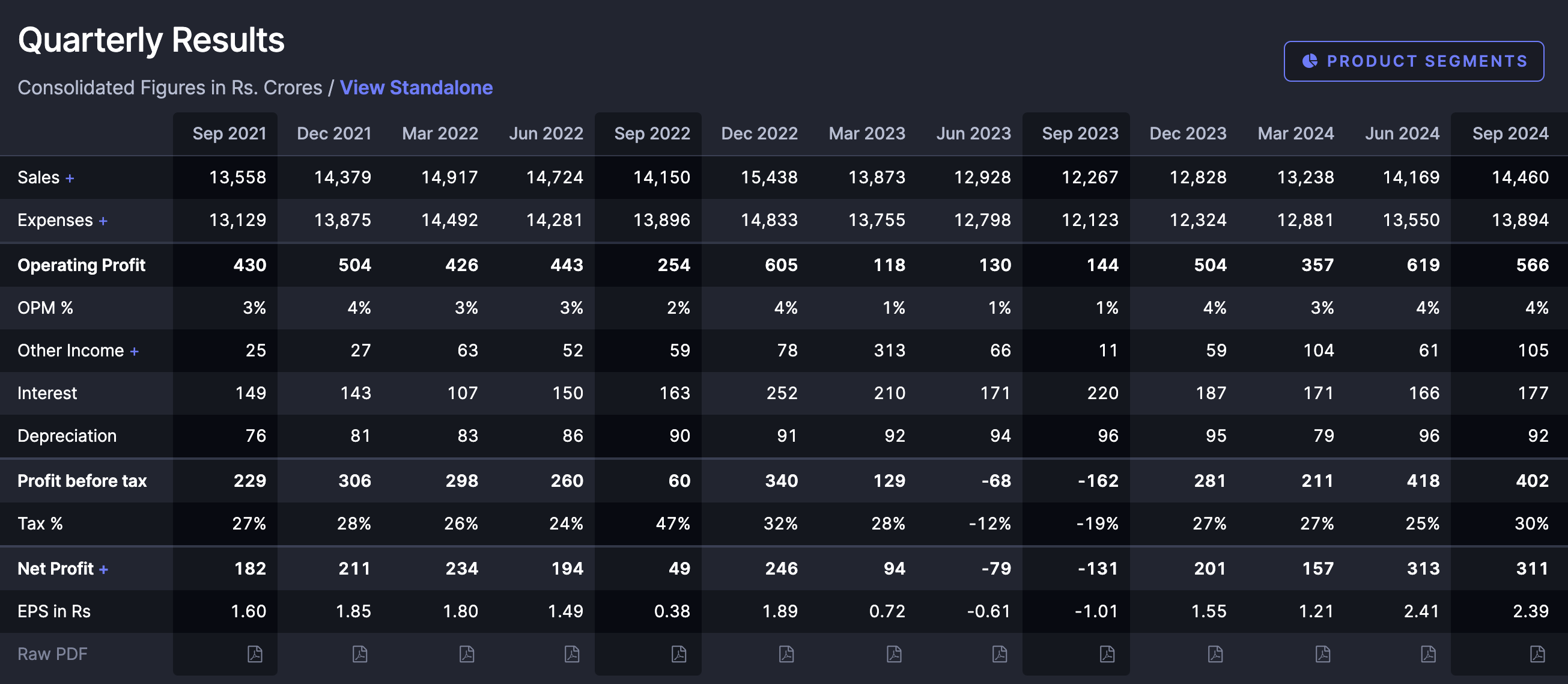

On the margin side — despite a soft quarter, we had one of the best years in the last 25 in terms of EBITDA. Margins in edible oil have generally been good and steady. We’ve delivered consistent performance over the last 12 quarters, barring a one-off issue last year. The outlook remains stable, and we expect edible oils to continue performing as promised.

Abneesh Roy:

Just a follow-up on margins. The full year was strong — the first 9 months showed around 4%+ margins. But this quarter saw a sharp decline in EBITDA margins. Was there an inventory loss? And what’s your view on margins for Q1 and Q2? Do you expect to return to the 4% range?

Shrikant Kanhere:

Let me take that. Whether we like it or not, we need to acknowledge that we’re operating in a commodity business. Commodity cycles don’t align neatly with calendar quarters. Sometimes parts of the cycle wrap up in one quarter, and others spill into the next. That’s why looking only at quarterly numbers can be misleading.

It’s more meaningful to assess performance over a half year, or ideally, a full year — that’s when the commodity cycle tends to play out completely. Since we work with hedging mechanisms, one leg of the hedge might conclude in one quarter and the other in the next, creating timing differences.

Also, don’t just look at margins in percentage terms. Focus on the absolute margin per ton. This year, we benefited from a favorable cycle and some inventory gains, which may not repeat next year. That said, we expect to maintain our margin structure in per-ton terms.

To be specific, our EBITDA per ton for edible oil should be in the range of INR 3,500–3,600, assuming no exceptional events like last year.

Abneesh Roy:

One last quick question — your pricing shows around a 37% hike, yet Q4 edible oil volumes are higher than Q3, but profits are lower. Did you push for market share growth by sacrificing margins?

Shrikant Kanhere:

Yes, we did take a slightly aggressive approach. As Mr. Mallick mentioned, palm oil prices stayed high, and it’s a key segment for us. We chose to defend market share and volume, which did result in some margin compromise. Additionally, as I said earlier, the timing of the commodity cycle could also explain the lower margins this quarter.

While both executives do provide useful context, their responses seem somewhat strategic — offering explanations around the factors influencing margins rather than directly addressing the specific concerns raised. Angshu Mallick’s response, in particular, could be interpreted as trying to avoid giving a firm answer on the likelihood of duty changes and how that might impact margins in the short term. Similarly, Shrikant Kanhere’s explanation on commodity cycles feels like an effort to avoid a direct answer to the immediate margin drop in the latest quarter.