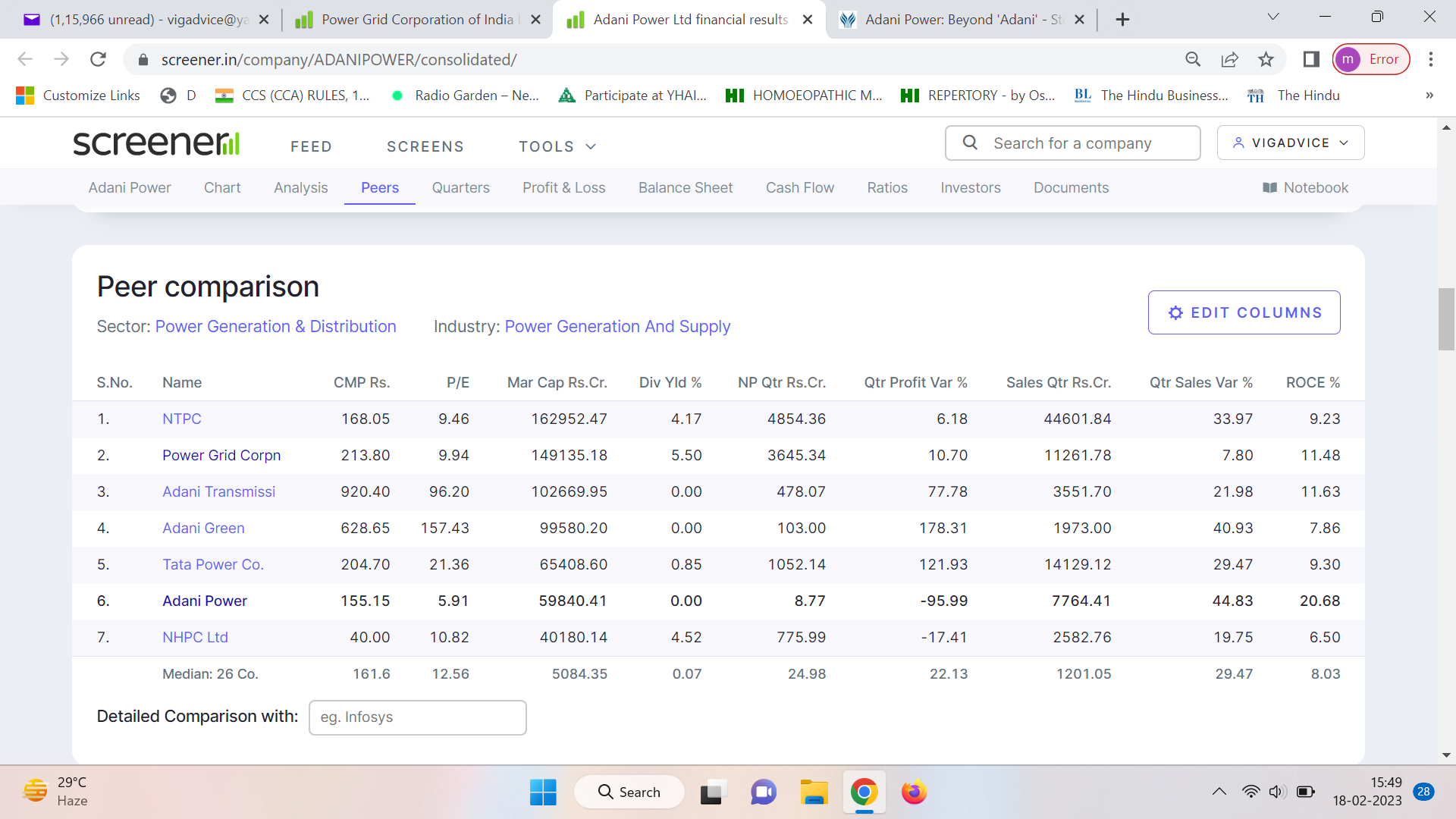

Adani Power(AP): My reasons to get in at CMP (ie. <350 levels).

Tata Power* put all it’s might to raise money for it’s Renewable Energy Projects, however the acute supply disruptions Covid brought in the World(particularly India) gave a reality check that it cannot do away with Coal, just yet. At least for this decade, the Coal is here to stay. This “fundamental-assumption” helped put the entire Coal Sector back on Investor’s agenda.

Since 2016, no New Thermal Power plant has been sanctioned due to India’s commitments to Paris Agreement. However, AP quite smartly, has been vying for distressed Thermal Power Plants, thereby gaining a disproportionate market share in Power Generating Companies(GenCos), eg. it bought GMR, DB Power, Udupi PC, Lanco etc. Its’ Jharkhand, Godda Districts’ under-construction plant(set to begin operations within 6-months), was carefully crafted as a SEZ(to supply power exclusively to Bangladesh), ie. the tax benefits will be accrued. Till recently, securing Coal for this plant was a major roadblock, but the opening up of Carmichael Coal Mines’(Australia), has ensured a steady & disproportionate supply for the fuel needs of AP, vis a vis its’ Thermal Peers. This is a major “backward-integration”, which will increase the earnings visibility for AP in an ever increasing power demand in a country like India.

GenCos in India usually stay under severe Financial Stress(in part due to legacy issues of Over Capacities built during UPA-II) and majorly due to inability of Discoms(Distribution Companies) to collect bill amounts and payback the GenCos in time. The inability of Discoms to collect money from the general populace is left unabated by the Political Executive of the states, for whom collection becomes an election issue. However, the Central Govt’ usually incentivizes the GenCos by bailing out the distressed DisComs, eg. UDAY Program, which was launched in 2015. Another such program is in making, ie. 2022 and may see light soon as a budget-announcement.

AP’s debt is majorly the deliverables from the Discoms, however, the company is not only looking up for Central Govt’s package but actually fighting tough legal battles to recover them back. eg. It did major recoveries by winning legally over Rajasthan, Haryana, Jharkhand, Maharasthra in 2021 and now UP, TN, MP are next. This is also favourable to Central Govt(which may help create conditions for such recoveries), as those recoveries will form part of State’s Budget. One may say that this is Adani’s clout which is helping it recover the dues, but this is a fair-pratice & favours the overall business atmosphere in the country. Recoveries must be promoted and timely collection should be ensured by State Govts.

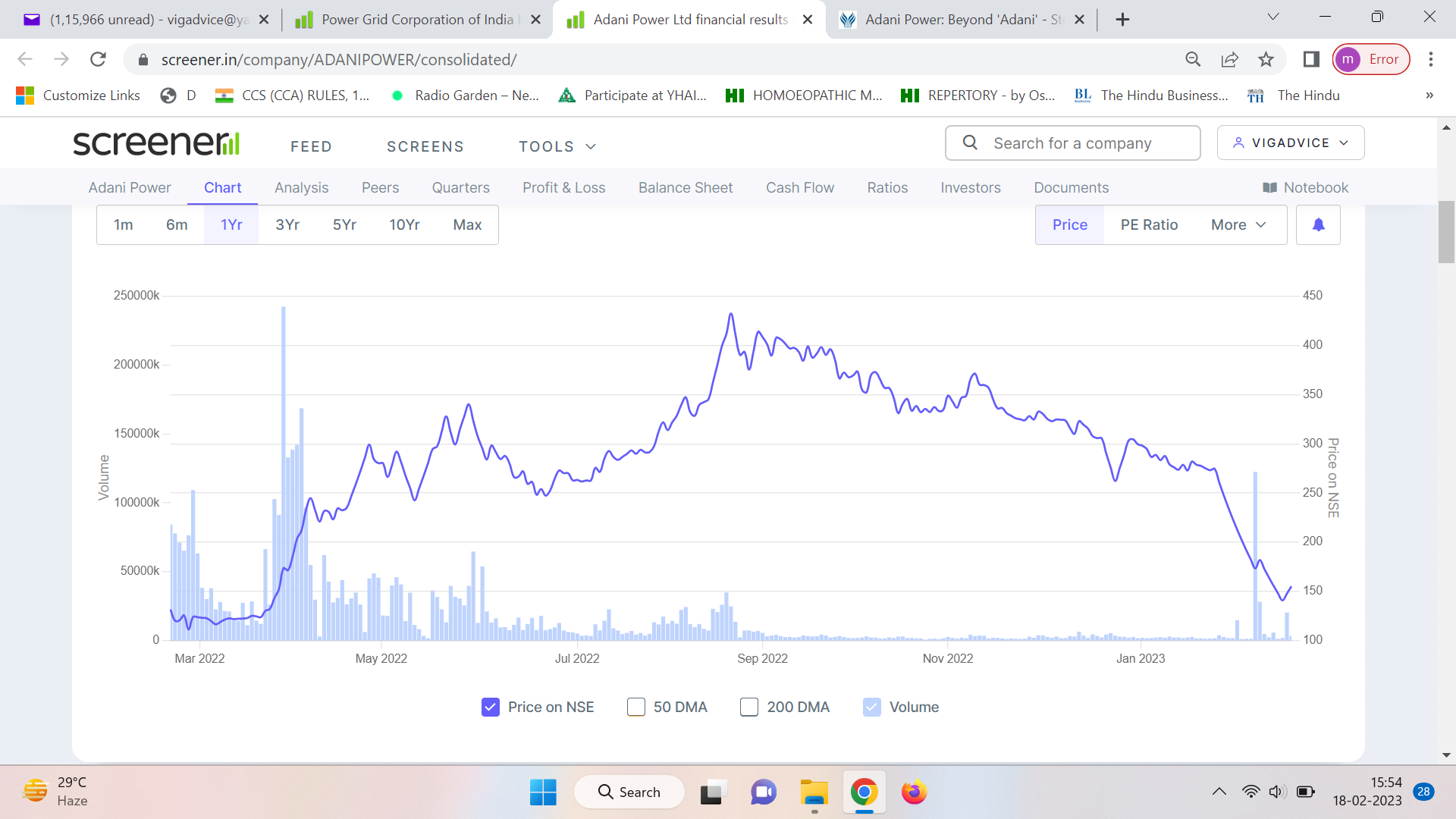

It is presently(shifted up from ASM-IV today) in ASM-III( ie. negativity is priced in), which should give investors time to to study & get in. Upon a reasonable sideways performance(3 months now), it should start to show an upmove soon, ie. when it(tends to) get out of the ASM Framework. Additionally, it’s inclusion in MSCI Index in May, brought in funds from BlackRock and Fidelity, which will actually pave way for sustained FII(and Institutional) interest in Short to Medium Term. The Power Demand picks up in Summers, consequently, the Demand for Power Sector Stocks, plummets in Winters. Personally I see a cyclical+value opportunity in AP.

Did I tell you something?

*****(a peer which common investors so fondly claim as a great firm, having Thermal + Wind + Solar + New Projects eg. Hybrid, all built in).

Disclaimer: Not a buy/sell reco, only an analysis. This will help provide people some perspectives on how they should value this firm, beyond the obvious high-debt/‘adani’/coal narrative.

Can someone help me understand what can be possible range of regular other income of Adani Power.

It is fluctuating a lot. Also why there is negative taxes?

Adani Power Limited has delivered a strong performance in Q1 FY25, with significant year-on-year growth in PLF to 78% and increased power dispatch across all plants. The company is benefiting from growing power demand, lower imported coal prices, and a competitive position in merit order dispatch. APL’s strategically located open capacity has also capitalized on high merchant demand and tariffs. The management is optimistic about the future, citing favorable outlook for India’s thermal power capacity growth.

Strategic Initiatives:

Capacity Expansion: APL is aggressively pursuing capacity expansion through both organic and inorganic routes. The company aims to increase its capacity from the current 15 GW to 30.67 GW by FY29-30.

Mahan Energen Phase II: The 1600 MW Ultra-supercritical expansion project is on track for completion by June 2027.

New Projects: APL has initiated preparations for three new 1600 MW projects each at Raipur, Raigarh, and Mirzapur.

Acquisitions: The company is awaiting NCLT approval for resolution plans of Lanco Amarkantak and Coastal Energen, which will add 1800 MW of operating capacity and 1320 MW of under-construction capacity.

Fuel Security: APL is focusing on enhancing fuel security through commercial mining licenses under an asset-light model.

Trends and Themes:

Rising Power Demand: India’s power demand is projected to grow significantly, with peak demand estimated to reach 400 GW by 2031-32.

Thermal Power Necessity: Despite renewable energy growth, thermal power remains crucial for meeting base load and peak demand.

Long-term PPAs: State governments are inviting bids for long-term power purchase agreements (PPAs) to meet future demand.

Merchant Power Opportunities: High merchant demand and tariffs are providing additional revenue streams for power producers.

Industry Tailwinds:

Government’s Revised Projections: The government has increased its power demand projections, indicating a need for 80-90 GW of additional thermal power capacity by 2031-32.

Resource Adequacy Requirements: States are mandated to ensure 24x7 power supply, driving demand for firm power contracts.

Favorable Regulatory Environment: Improved resolution of regulatory petitions and recovery of past dues from DISCOMs.

Industry Headwinds:

Competition from Renewable Energy: Increasing renewable capacity and battery storage solutions may impact thermal power demand in the long term.

Potential Carbon Taxes: Future implementation of carbon taxes could impact profitability if not adequately passed through to consumers.

Analyst Concerns and Management Response:

Concern: Exposure to merchant power market risks.

Response: Management aims to maintain an 80:20 ratio of long-term PPA to merchant capacity to balance stability and upside potential.

Concern: Acquisition strategy and integration risks.

Response: APL is selectively evaluating acquisitions based on criteria such as equipment quality, location advantages, and expansion potential.

Concern: Future carbon taxes impact.

Response: Management expects carbon taxes to be treated as change in law events, allowing pass-through under PPAs.

Competitive Landscape:

The thermal power generation sector in India is consolidating, with fewer developers available. APL’s aggressive expansion plans and strategic acquisitions position it favorably to capture a significant market share in the growing power demand scenario.

Guidance and Outlook:

The management expressed confidence in doubling capacity to 30 GW by FY29-30 and expects revenue growth to outpace capacity growth due to potentially higher realizations.

Capital Allocation Strategy:

APL is pursuing a balanced approach, utilizing strong cash flows for debt reduction and funding expansion plans. The company is open to both organic growth and strategic acquisitions that align with its objectives.

Opportunities & Risks:

Opportunities:

Significant demand growth in the Indian power sector.

Potential for higher realizations in the merchant power market.

Acquisition of stressed assets at attractive valuations.

Risks:

Regulatory changes affecting PPA terms or tariff structures.

Volatility in fuel costs, particularly for imported coal.

Potential disruption from renewable energy and storage technologies.

Regulatory Environment:

The regulatory environment appears supportive, with improved resolution of past regulatory issues and recovery of dues. The management expects future regulatory changes, such as carbon taxes, to be passed through under PPA provisions.

Customer Sentiment:

Customer sentiment appears positive, with growing power demand from both industrial and residential sectors. State utilities are proactively seeking long-term power supply arrangements to meet future demand.

Top 3 Takeaways:

APL is targeting aggressive capacity expansion from 15 GW to 30.67 GW by FY29-30 through a mix of organic growth and strategic acquisitions.

The company is maintaining a balanced approach with 80% capacity under long-term PPAs and 20% for merchant sales to optimize returns while managing risks.

Strong industry tailwinds, including government projections of significantly higher power demand, position APL favorably for sustained growth in the coming years.

come across one youtube video about business model of Adani power and future prospects, very interesting points highlighted about company

Adani Power – ₹1.12 Lakh Crore Cash Flow Story (FY25–FY31)

Adani Power is expected to generate ~₹1.23 lakh crore in Fund Flow from Operations (FFO) over the next 6 years, driven by strong operational efficiency and locked-in capacity. After accounting for ₹11,000 crore in debt repayments (amortized), the company is left with ~₹1.12 lakh crore available for growth CapEx.

This positions Adani Power to self-fund its entire 13.1 GW capacity expansion pipeline, which is already in advanced development stages (100% land and BTG orders in place).

what your opinion about how adani will utilize the cash flow and will a dividend policy will come in future, I had doubt it will be liberal with dividend like NTPC, is thermal power has so much scope to invest for Adani power for huge capex, divided will help promoters to fund capex in other companies, i had made a small tracking position and i will be interesting to see how this goes

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

ValuePickr Forum is visited today both by novices and wannabe stock pickers, as well as very sophisticated investors. Some of us have made the transition from novices, to learners, to stock pickers to now being reasonable capital allocators. To know the difference visit [Capital Allocation thread] (https://forum.valuepickr.com/t/initiating-a-new-stock-idea-discussion-thread). Its our dream to create a natural vibrant eco-system of learners, individual investors, industry professionals and Institutional investors in a…

Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/colleague and look to edit the post in order to meet prescribed guidelines. We have the responsibility - especially the thread initiator (assumption is he/she is a savvy investor) - to cater to bringing everyone on same page - quickly - if you know what we mean.