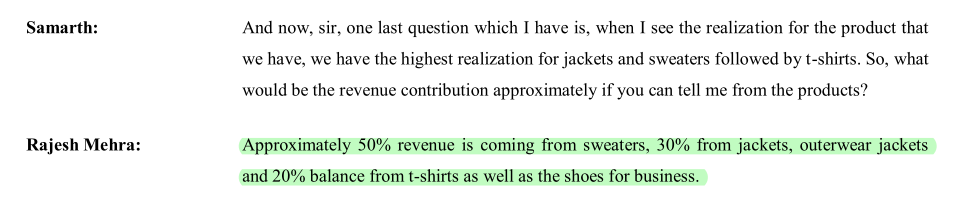

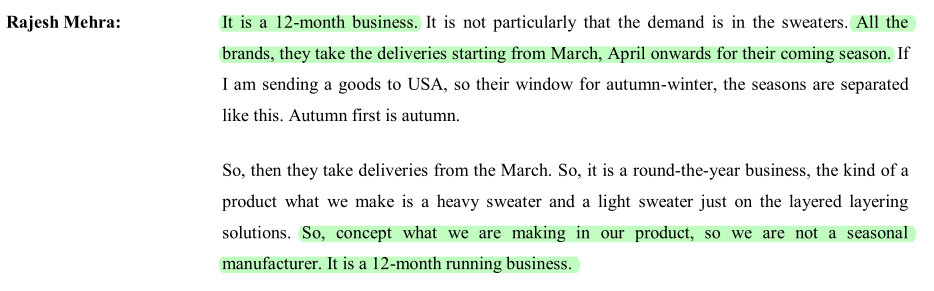

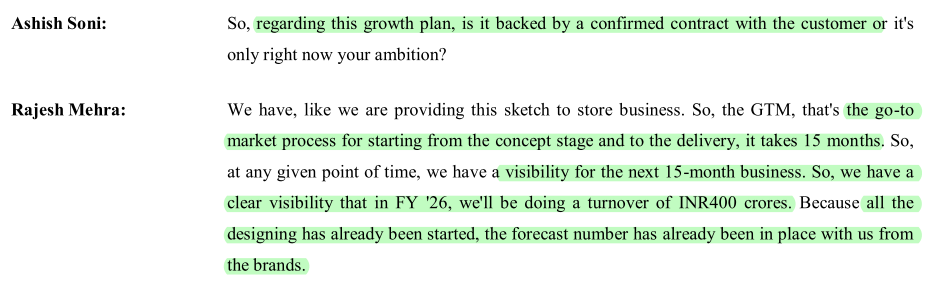

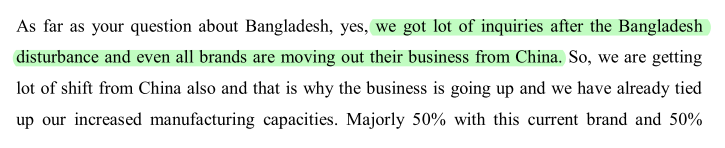

My first post on VP on this Co that conducted its 1st conf call in Feb. I had posted that here.

Co just did their 2nd conf call and transcript is now available

.

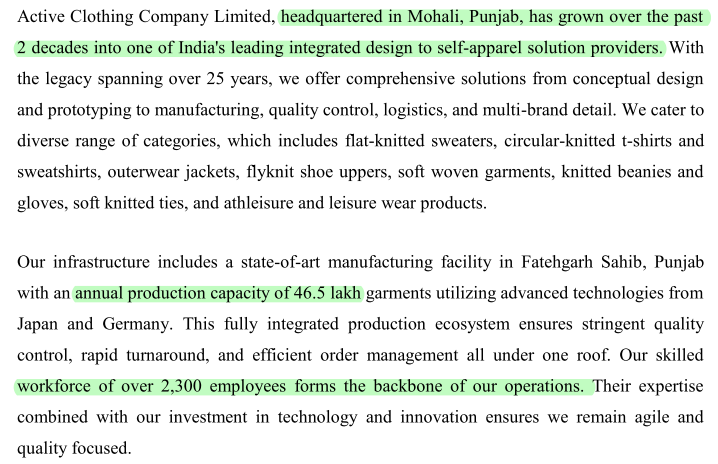

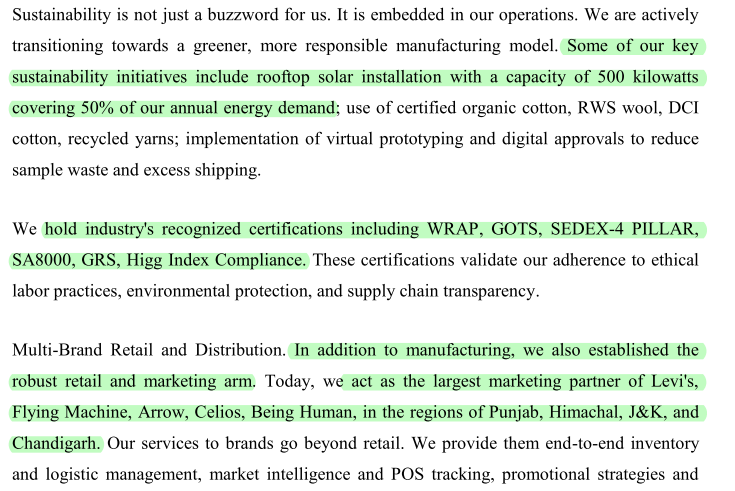

I am going to try to summarize about the Co from the conf call introduction below and follow up with important highlights from conf calls.

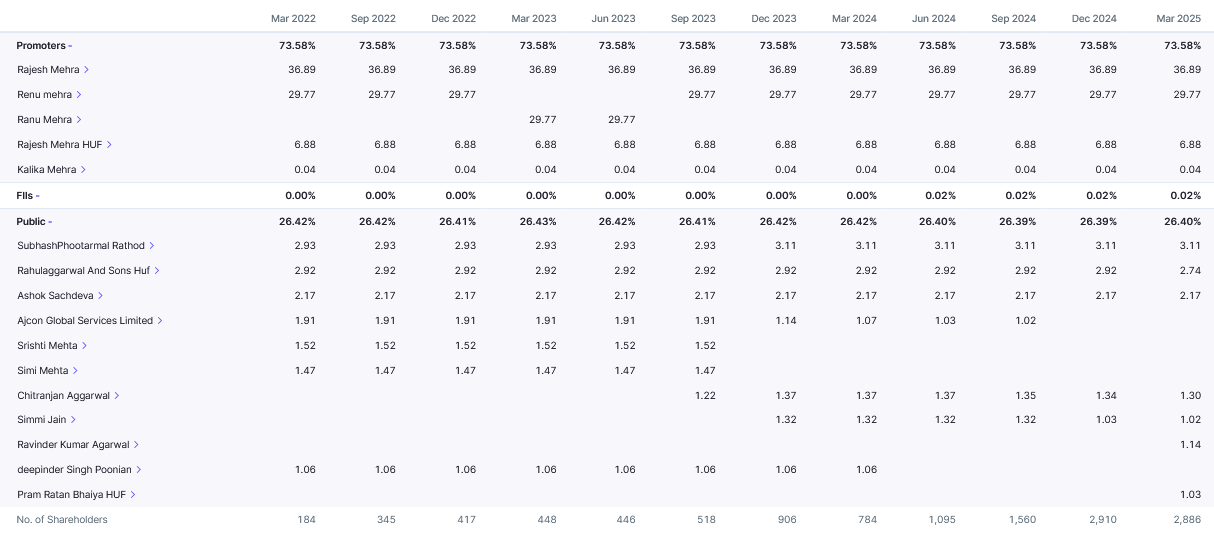

Here’s the shareholding from screener

Co is run by Mr. Rajesh Mehra. My interest in the Co is because of 3 factors

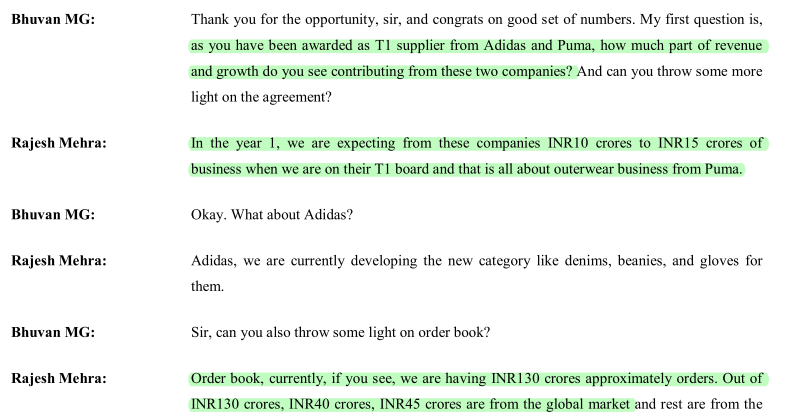

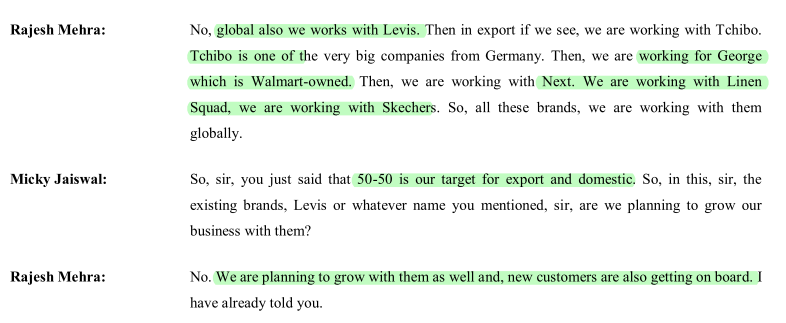

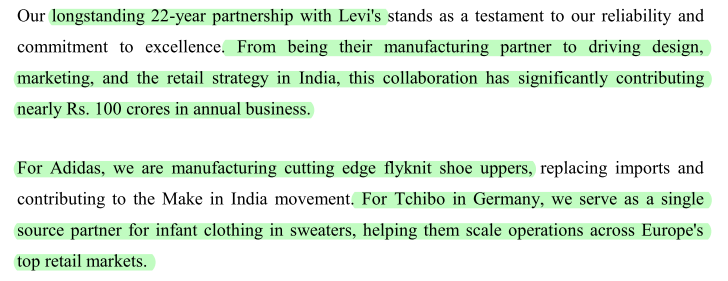

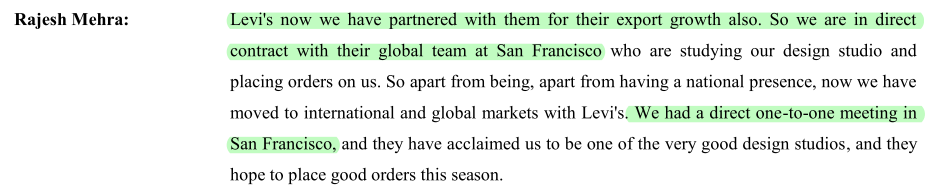

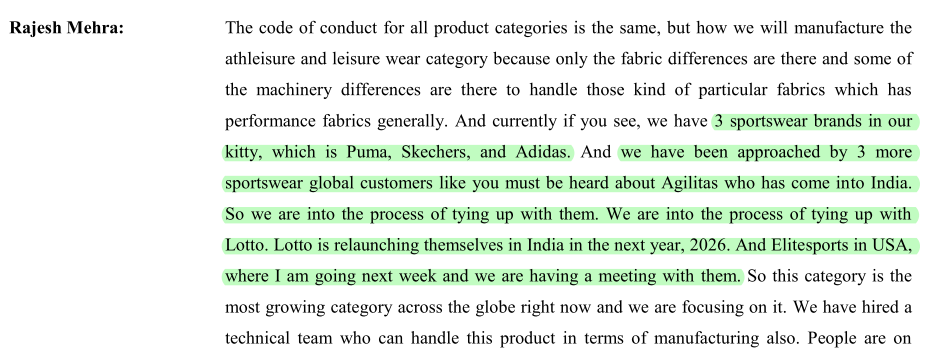

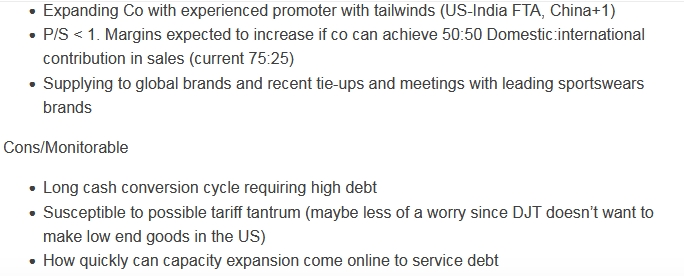

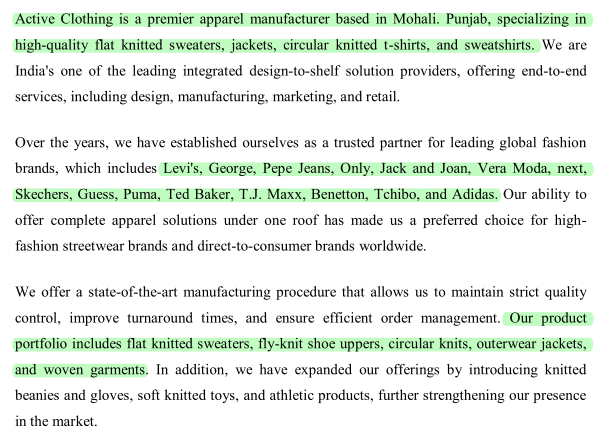

1 Co has had major wins with US cos like Adidas, Puma last FY and is already a supplier to Levis

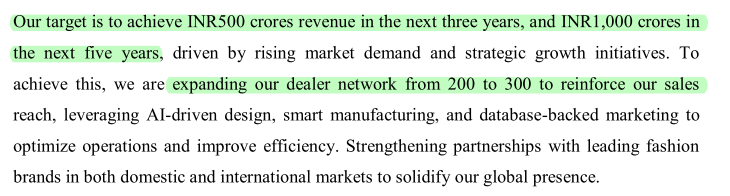

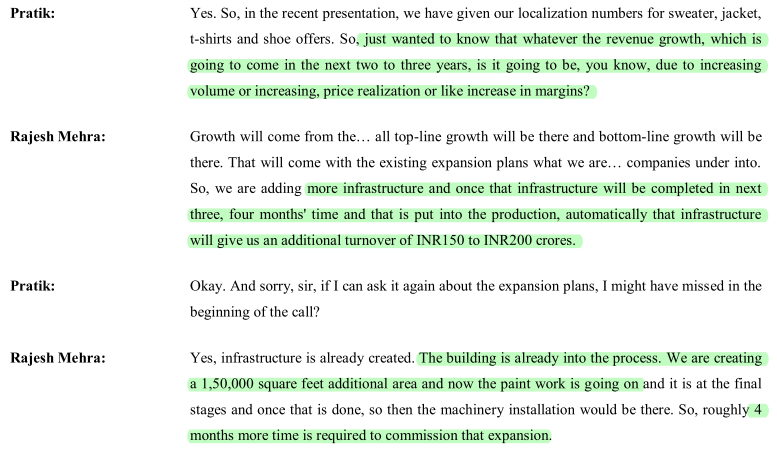

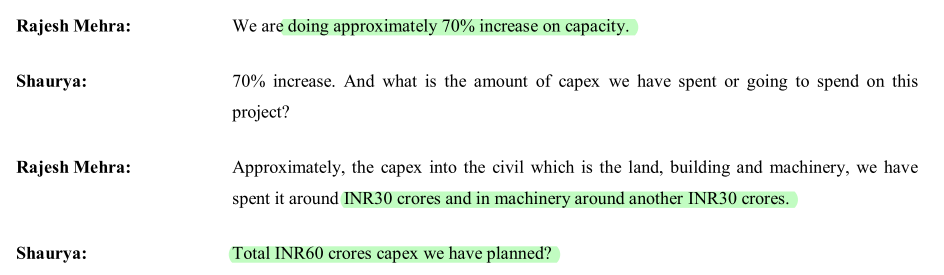

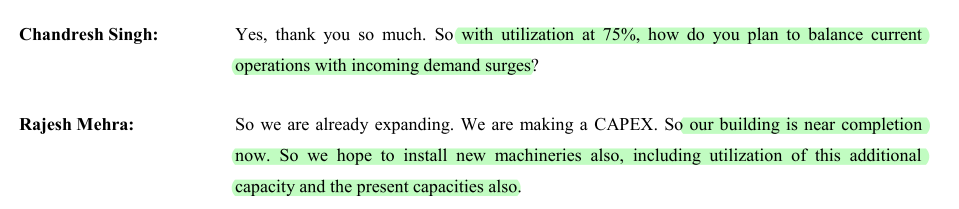

2 Co is expanding capacity by ~70% in the upcoming quarters and targeting consistent revenue growth as mentioned by promoter in conf call

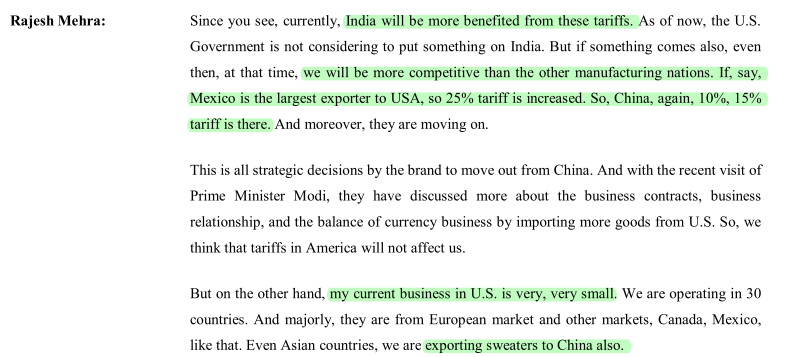

3 Possibility of India US trade deal giving more traction to the co

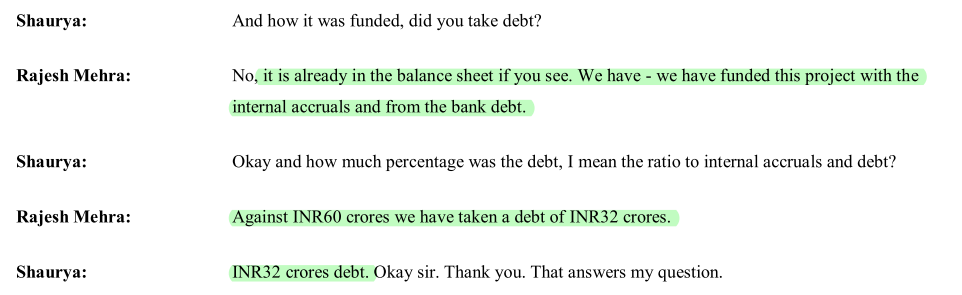

Co is using internal accruals and has taken on debt to fund expansion - so that’s something to track about the Co. @vatsal10 has been discussing about the co with me over DM; so will ask him to post more discussion points here.

I have been investing in the co since the first conf call and have transactions in the past 3 months. I will provide snippets from the conf call in a follow up post.