In my opinion such small quantities do not mean anything except for signalling. Unless its more than 1% of their own holding I would not give it too much weight

10 Likes

Any thoughts on the narrative that the infra/capex theme has sizzled out?

https://www.ambit.co/newsletter/221/Asset%20Management_August2024

(year old article but seems to have been proven right)

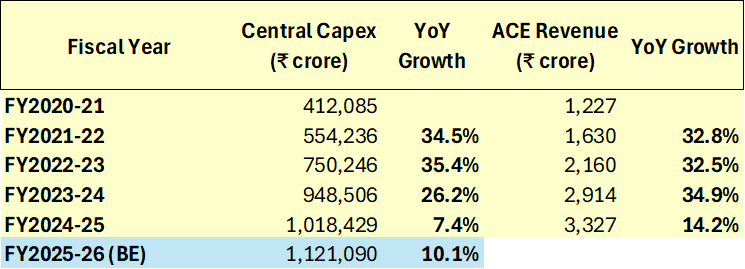

This is also reflected in the slowing down of govt infra spending. A plausible story is that after the 2024 election, the govt. realized that spending on infra, while good for the country, won’t get them votes from the masses, so they’re now focusing on giving freebies.

Private capex is actually facing degrowth this year as companies are cautious given tarrifs etc.-

Press Release:Press Information Bureau

This is probably why ACE stock has derated. On one hand, this can be an opportunity to buy a fundamentally excellent company and a play on the long term India growth story at a decent valuation (which is why I entered at Rs. 932/share at 26 P/E) , but if they aren’t able to outgrow the govt. spending by penetrating new markets significantly, they might not meet their aggressive guidance (which they already lowered) and the stock might trade sideways for quite a while. Would appreciate any counterarguments.

15 Likes

@ashwind Sir, can you post vahan registration table pls

ACE management has clarified that vahan data is not very helpful as there is a lag of 1-2 months against what they have sold out. But still if you want to track it.. here is the link

4 Likes

Few points from concall [07-11-25]

- Management expects flattish to single digit growth for the full year FY 26.

- The proposed anti-dumbing duty (ADD) is 26% for one chinese player and 52% for all others, the final notification from finance ministry is expected by mid to end dec.

- The Kato JV will be effective once the govt. notification on ADD on chinese cranes is officially implemented.

- Management stated that their medium term guidance is intact, projected revenue for FY 27 is ₹4,000 to ₹4,400 crores

3 Likes

can anyone post full content of this article?

https://www.business-standard.com/industry/news/need-anti-dumping-duties-on-chinese-excavators-cranes-ace-s-sorab-agarwal-125113000417_1.html

1 Like

ACE & Sanghvi Movers Limited Sign Strategic MOU of Indigenously

Manufactured Heavy Cranes - This seems like a very good development.

Questions I have:

- Is this related to the Anti Dumping Duty that was supposed to come into effect from mid-Dec?

- Will this help ACE to break into the heavy tonnage cranes (crawler/truck) (KATO tieup) where it does not have much heft?

- Mostly this might be at lesser EBITDA, but will help in market share. Need to get more details like actual machine numbers, probable revenue, etc.

ACE & Sanghvi Movers Limited Sign Strategic MOU of Indigenously

Manufactured Heavy Cranes

6 Likes

The ADD notification on cranes was expected around mid to end of Dec,

Under Rule 18 of Anti Dumping Duty, the central govt. has three months to issue notification, now that deadline is passed, does it means that DGTR recommendation is lapsed?

1 Like

Notice from KATO WORKS for the JV

20260213_news02.pdf (148.7 KB)

6 Likes

There are many positive triggers that are being awaited for this Company in the last 5-6 quarters.

hope that Kato’s JV is a start in that direction.

Financially it’s a solid Company.

4 Likes