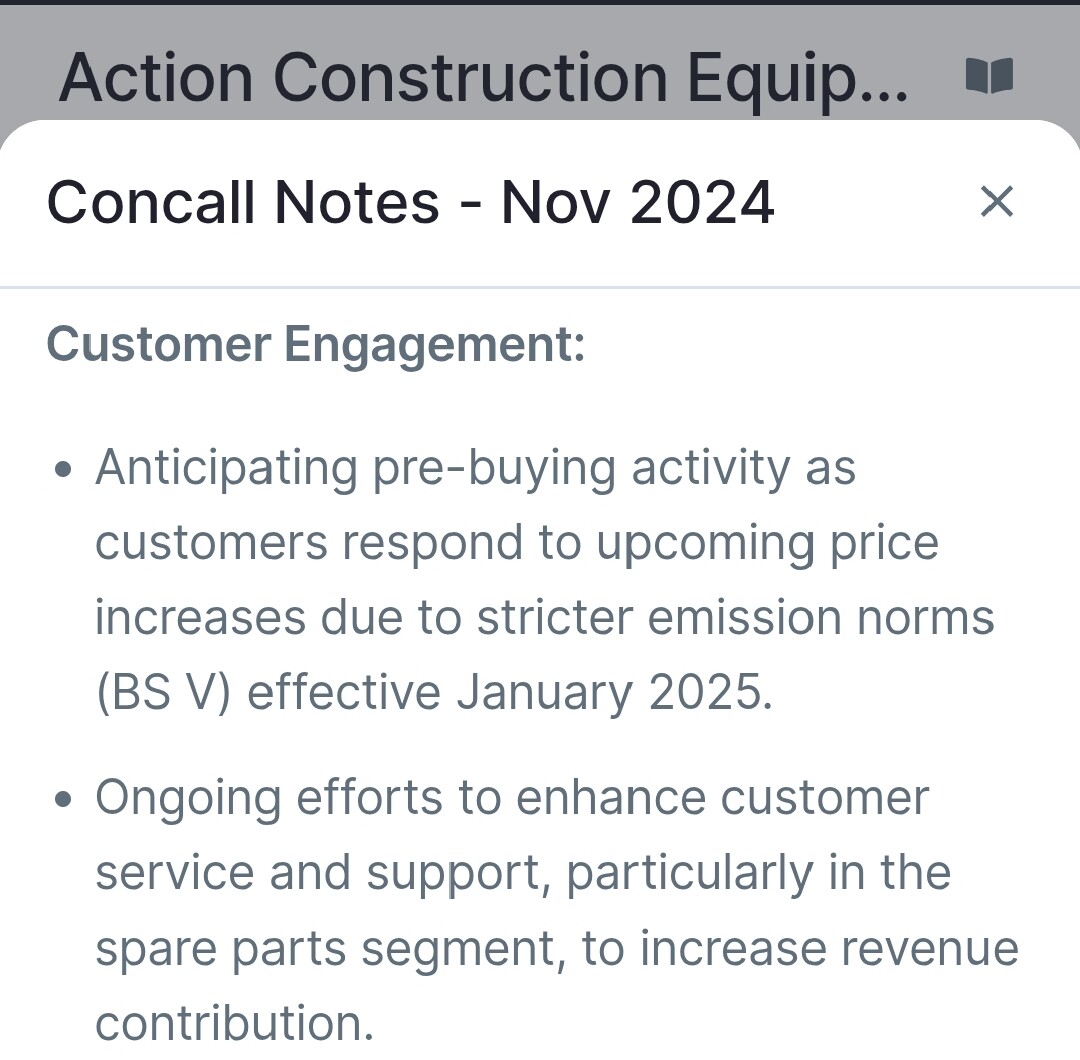

Q4 may have bumper numbers as from 1st April new construction equipment would have to comply to stricter emission norms, leading to higher cost. So purchase decisions may move left by a quarter or so for some buyers.

4 Likes

Hi Aarti, Sales volumes in fact will be the highest in Q4 as you can see from Vahan registrations. Also the valuations have cooled down from 54 PE to 33 PE with fantastic Q3 results. The share price has been in consolidation since last April where it made a high of approx 1700. So in my opinion valuations are not high as compared to other sectors like solar or railways where prices are correcting due to capex or trump issues.

3 Likes

agree also q4 in general is best quater for them

2 Likes

That will also mean, less sales in next few quarters.

May be…May be not.

It’s not gonna be next Quarter sales will increase 50% than normal progression that it will bring down sales in next quarter.

What may happen as per me:

- In terms of volume’s the pace of sales increase may reduce for 1 or 2 quarters.

- With new emission norms, the price of equipments will increase, so this increase in price may make up for slowness of pace of volumne growth. So Top line & Bottom line growth may not be impacted.

2 Likes

As per their last concall, stricter emission norms have already been implemented from Jan 2025 along with price increase.

3 Likes

Nice find. Thanks for sharing

1 Like

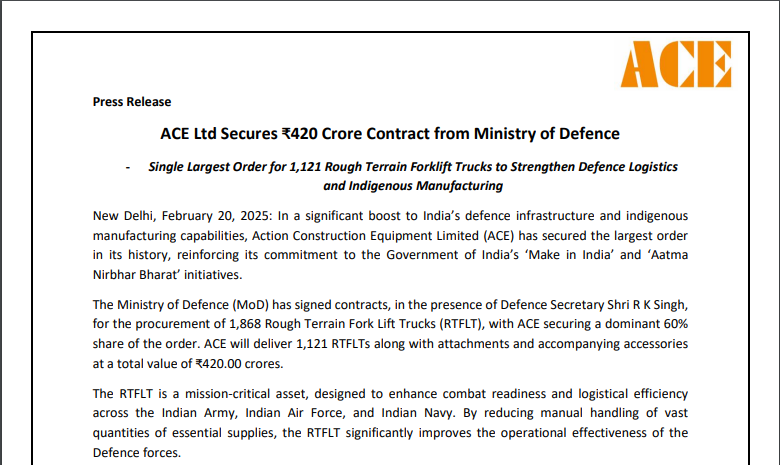

ACE was awarded this breakthrough contract after successfully demonstrating the superior capability of its equipment through rigorous performance testing.

This is a milestone order for them

15 Likes

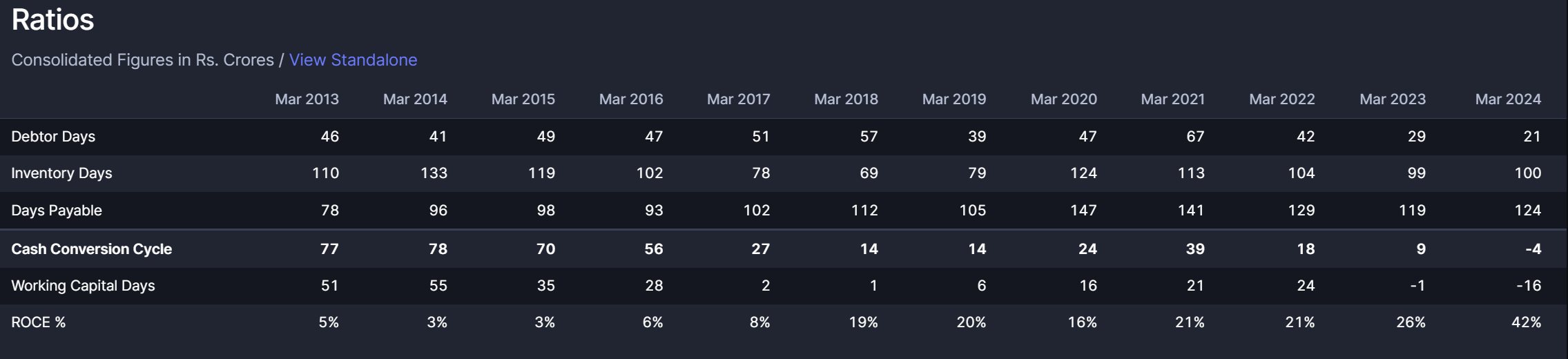

why the ROCE jumped suddenly from single digits for 5 years to double digits since 2018 till now? what changed fundamentally ?

i mean yes because of ebitda margins jump , it happened but why the margins jumped quickly and stayed stable till now?

ROCE is expressed as a percentage and calculated with the formula:

ROCE = (EBIT / Capital Employed ) × 100

A higher ROCE signals that a company is squeezing more profit out of every rupee of capital it employs—either by earning more, using less capital, or both.

If you look at the yearly numbers for EBIT and Capital Employed, you will realise the reason for this. EBIT has gone up substantially, whereas Equity has stayed same, and debt has decreased.

The infra spending push since 2016-17 has increased the need for construction equipment + cranes. ACE has been a direct beneficiary, where the operating leverage has kicked in. Same or slightly high Fixed Costs, but revenue has increased much faster, resulting in quicker EBIT rise. The capital allocated has remianed more or less the same. They will need more capital in FY26 for developing the additional land they acquired, so ROCE might cool off now.

7 Likes

ACE | Know your Company

4 Likes

has the company never made ROCE of double digit before 2018 from 2006 when the company listed ?

what changed suddenly from 2018? can you please summarise how and why their margins increase suddenly from 2018 and is it sustainable and why it was an average business before 2018?

1 Like

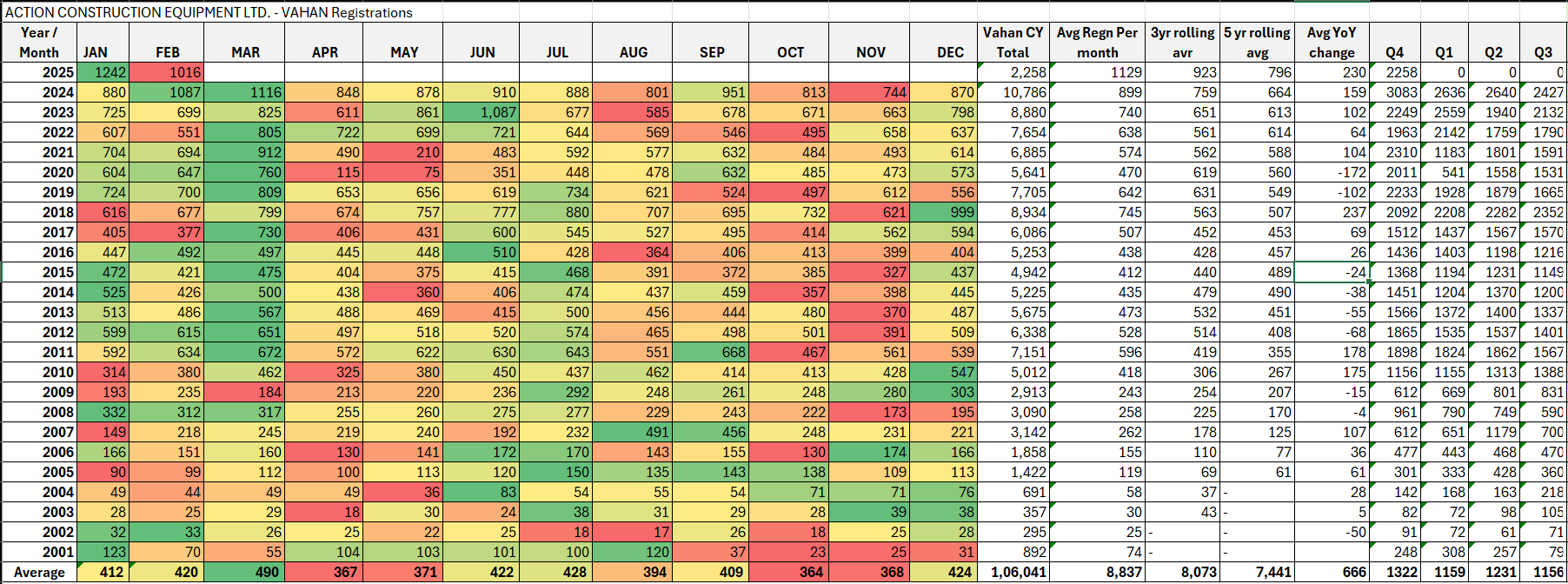

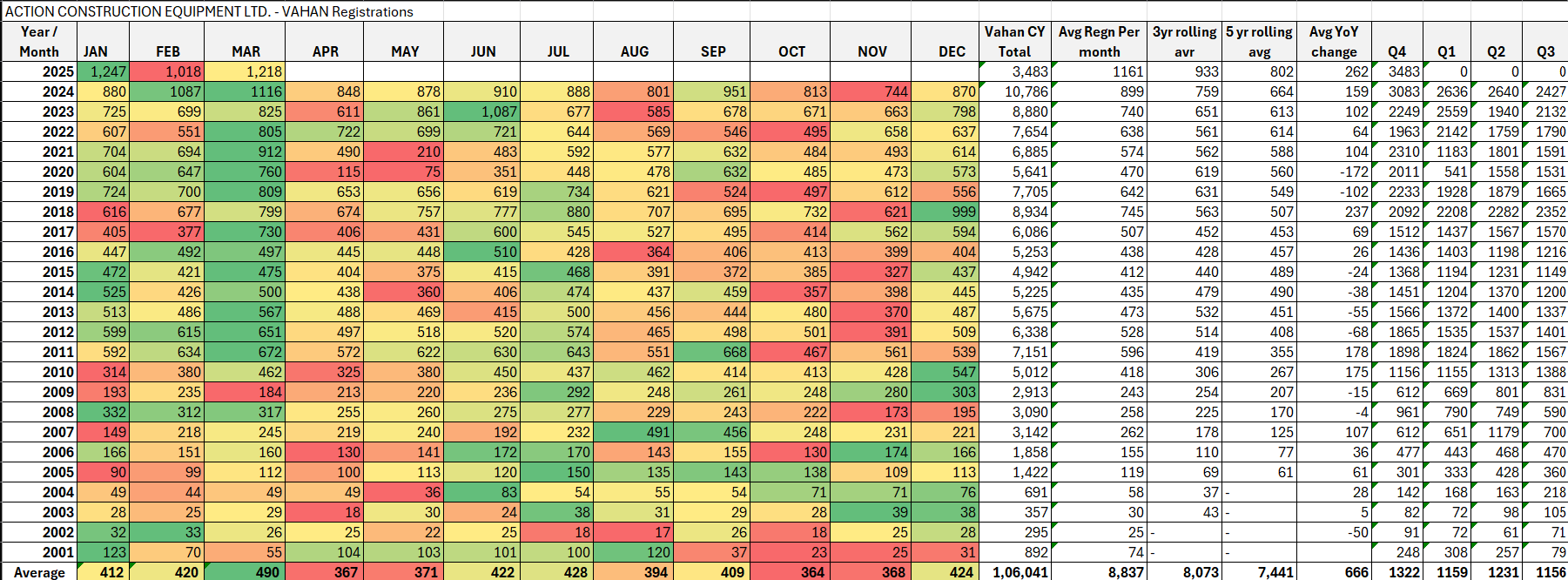

- Feb 2025 sales is 1,016 units as per VAHAN. It was 1087 in Feb-24, so flatish.

- Q4 volumes for Jan+Feb are 2258 vs 1967, a rise of 14.8%

- YoY growth is tempering on VAHAN numbers

8 Likes

thanks for sharing , what is the source for the above table

- Mar 2025 sales is 1,218 units as per VAHAN. It was 1116 in Mar-24, so ~10% growth.

- Q4 volumes are 3483 vs 3083, a rise of ~13%

- Some Estimates based on my internal calculations (could be wrong). Am projecting Q4 sales to be atleast around 940Cr, with NP of Rs.128 Cr. (Edit - For some reasons Q4 realization per unit is 30% lesser last year, maybe product mix. I have taken the lower end of realization, so sales can exceed 1000Cr for Q4, but may not be 30% higher)

- Edit - I have positions, these are older 1 year, no new positions.

Source: VAHAN SEWA| DASHBOARD

16 Likes

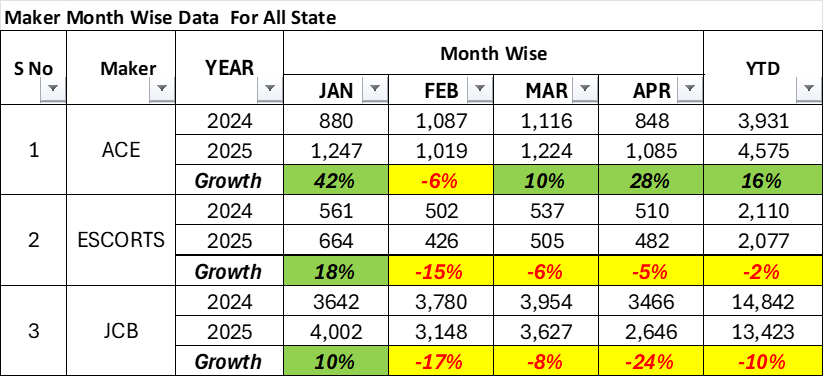

Data for April 2025

| Month | Vehicle Registration | YoY Change (Apr 2025 vs Apr 2024) |

|---|---|---|

| April 2024 | 848 | |

| April 2025 | 1,087 | +28.20% |

Source: Vahan

7 Likes

Nice. Can you please let me know the source?

Though when I navigate through south india while driving, I see majority as JCB’s!! ![]()

Both ACE and JCB are market leader in different segments. ACE key product is Cranes whereas JCB is dominant leader in Backhoe (JCB do not make Cranes). Though ACE also manufacturers backhoe but market share is quite low w.r.t JCB.

The data source -

2 Likes