Starting a thread for ACME Solar Holding

Overview

It’s a pure power generation company bidding on renewable power projects (solar, wind, hybrid, FDRE) under build-operate-own model where they agree 25-year Power Purchase Agreements with “offtakers” which can be utility companies themselves (e.g. BESCOM), special purpose intermediaries set up by central and state governments (e.g. SECI) or power generation companies themselves (e.g. NTPC, NHPC etc).

The Opportunity

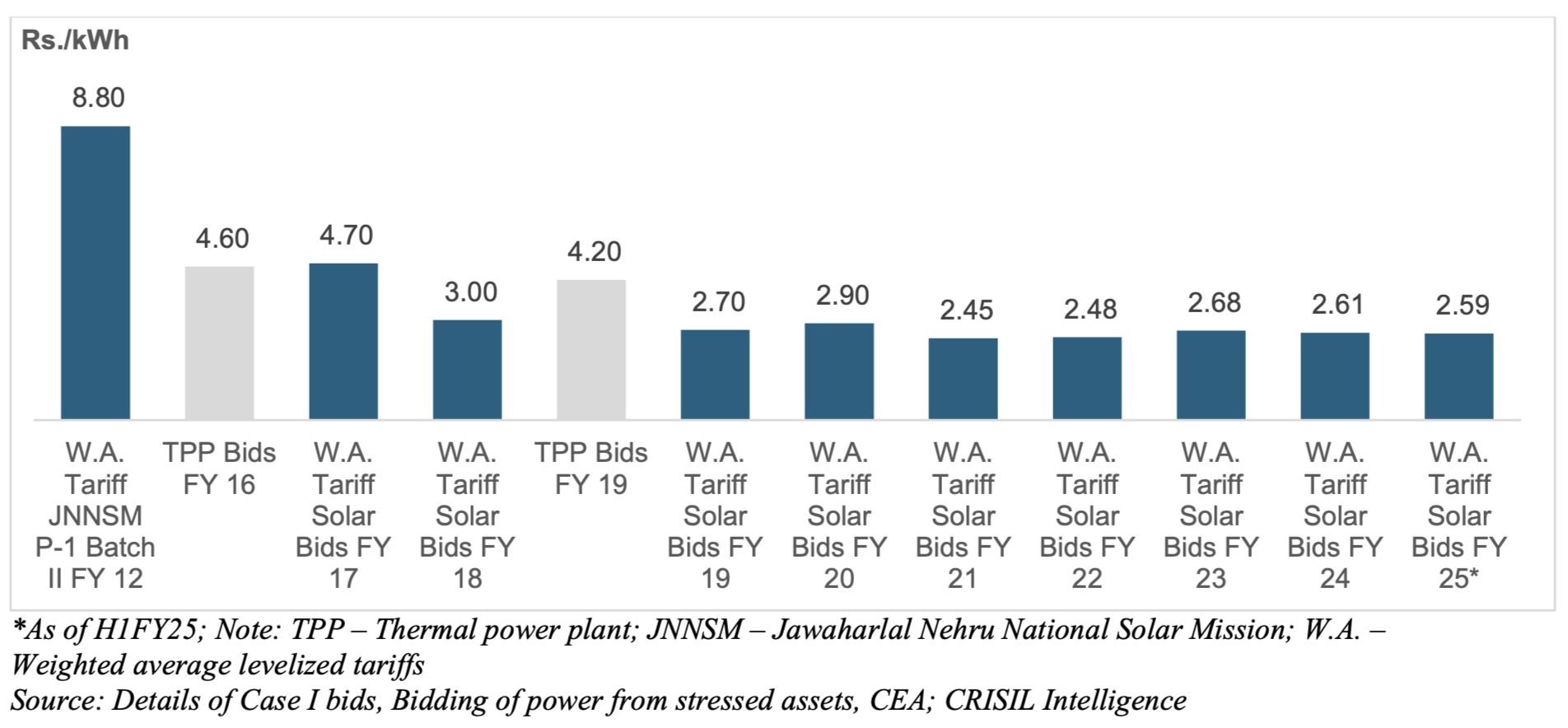

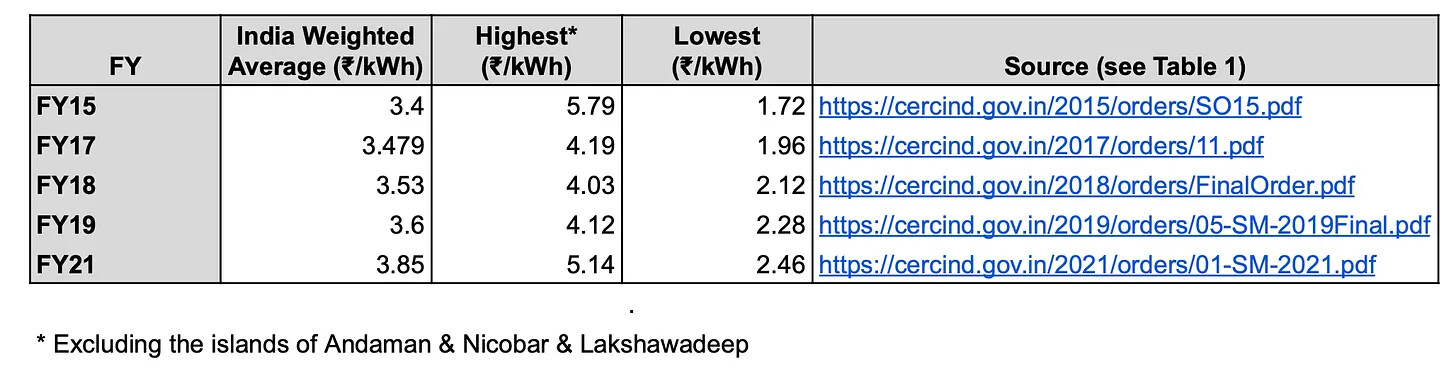

Currently, solar & wind power is the cheapest form of energy in India (and the world). I compiled average power purchase costs (APPC) for non-renewable sources of power from CERC reports, see below

As of FY21 (sorry, could not find any data for FY22-FY24) APPC is ₹3.85/kWh while PPAs for solar power are being agreed to ~ ₹2.45/kWh, wind power at ~₹2.7/kWh and hybrid power at ~₹3/kWh - significantly less than the APPC of non-renewables.

However, solar, wind and hybrid (solar+wind for better availability) suffer from intermittent supply e.g. high loads at low demand times and low loads at high demand times. The solution is FDRE using batteries for storage.

Currently FDRE tariffs are at ~₹4.4/kWh and if we take the CAGR of 2.21% increase in non-renewable APPC, non-renewables are at ~₹4.2/kWh. So we are very close to renewable power with battery storage becoming cheaper than non-renewables in India.

To not belabour this point too much, it’s pretty much inevitable that the unit economics of renewables with battery storage will be better than non-renewable power plants.

Unit Economics

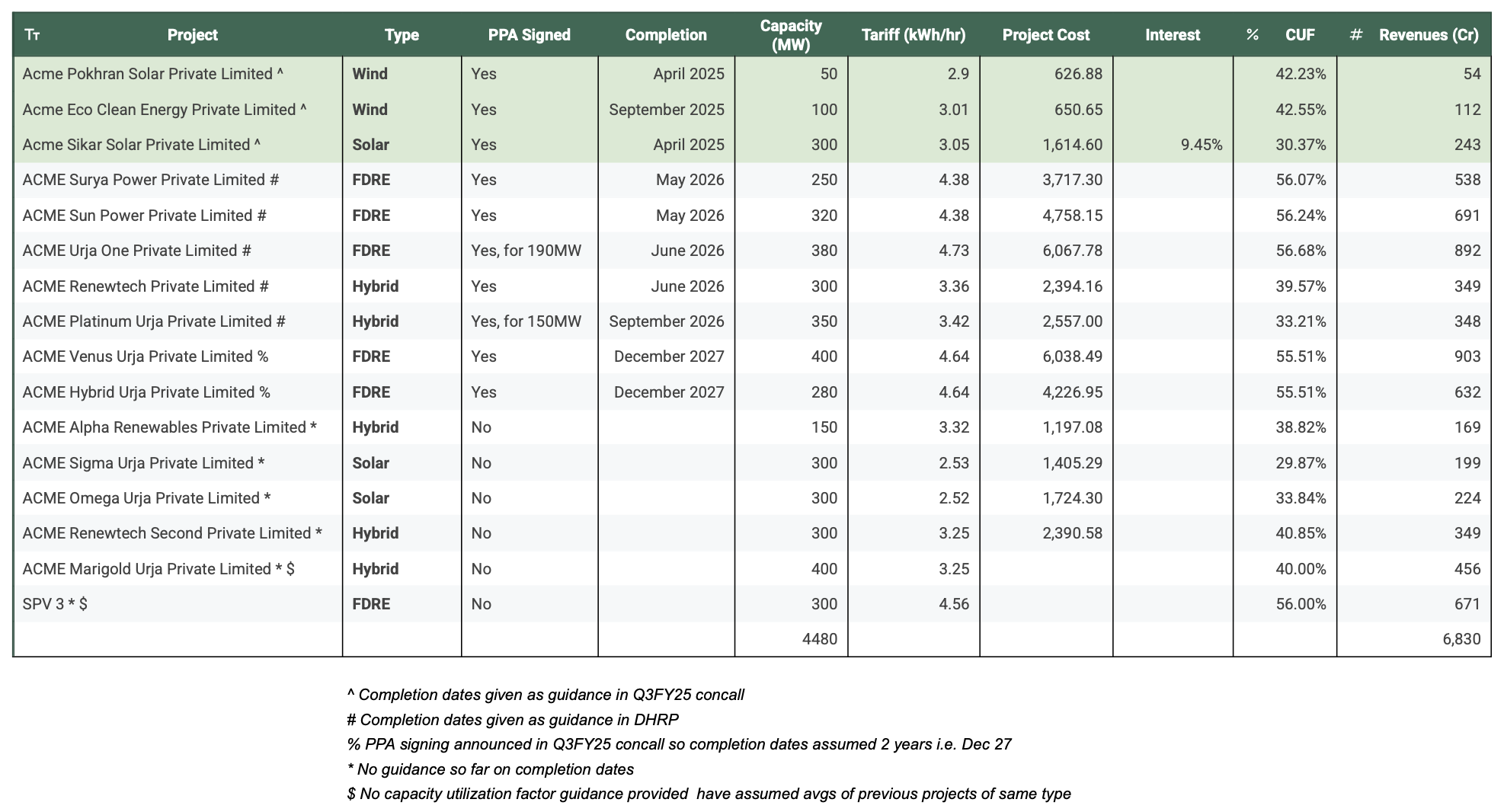

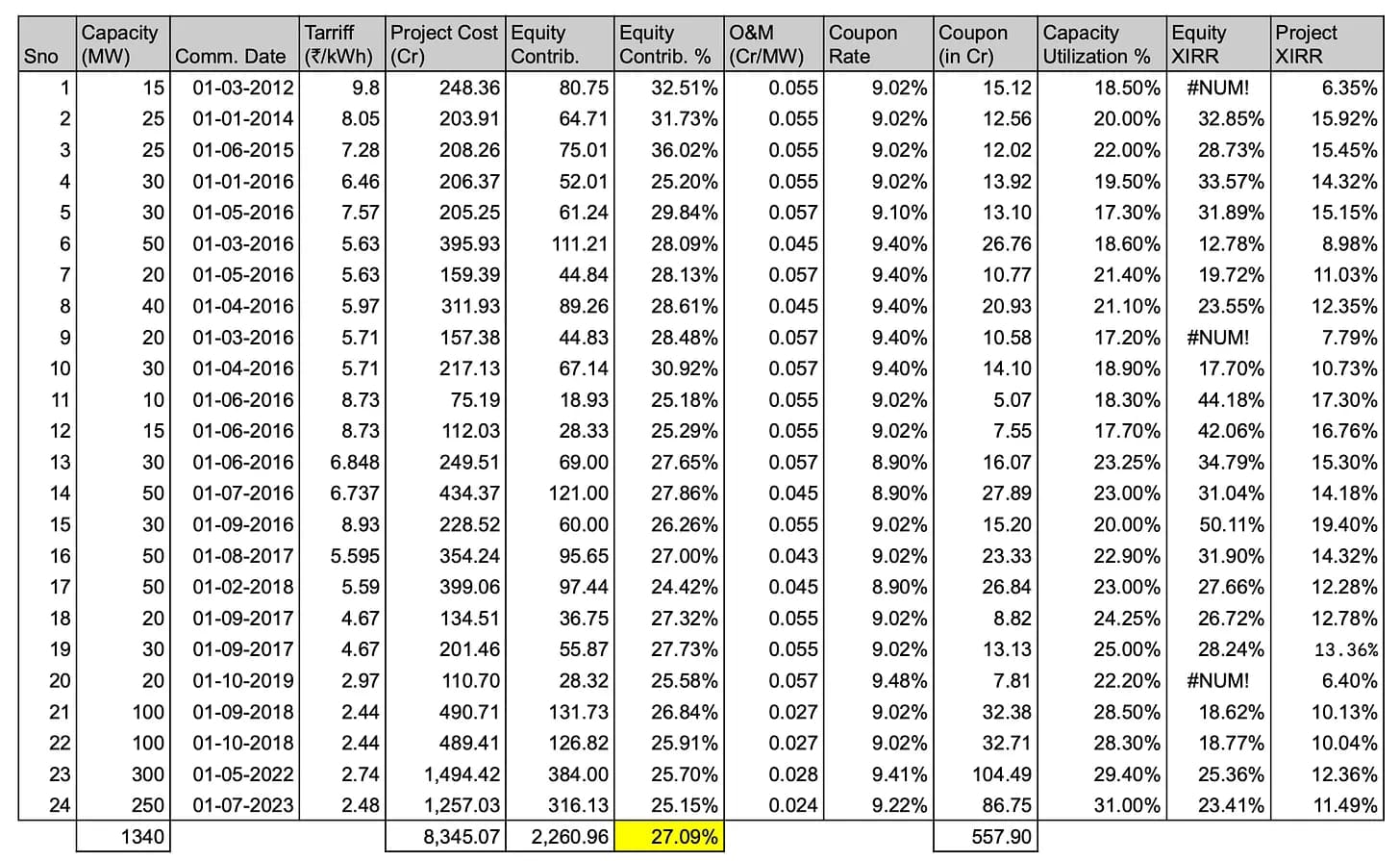

ACME’s RHP is unique among renewable power generation companies as it provides details of every project - its development costs, outstanding loans against the project and their interest/coupon rates, split between equity and debt, capacity utilization factors, PPA tariffs etc.

Using this info, I could calculate the project and equity XIRRs of each project under the portfolio

(The #NUM! ones are the ones with negative equity XIRR but for some reason, Google spreadsheet gives an error).

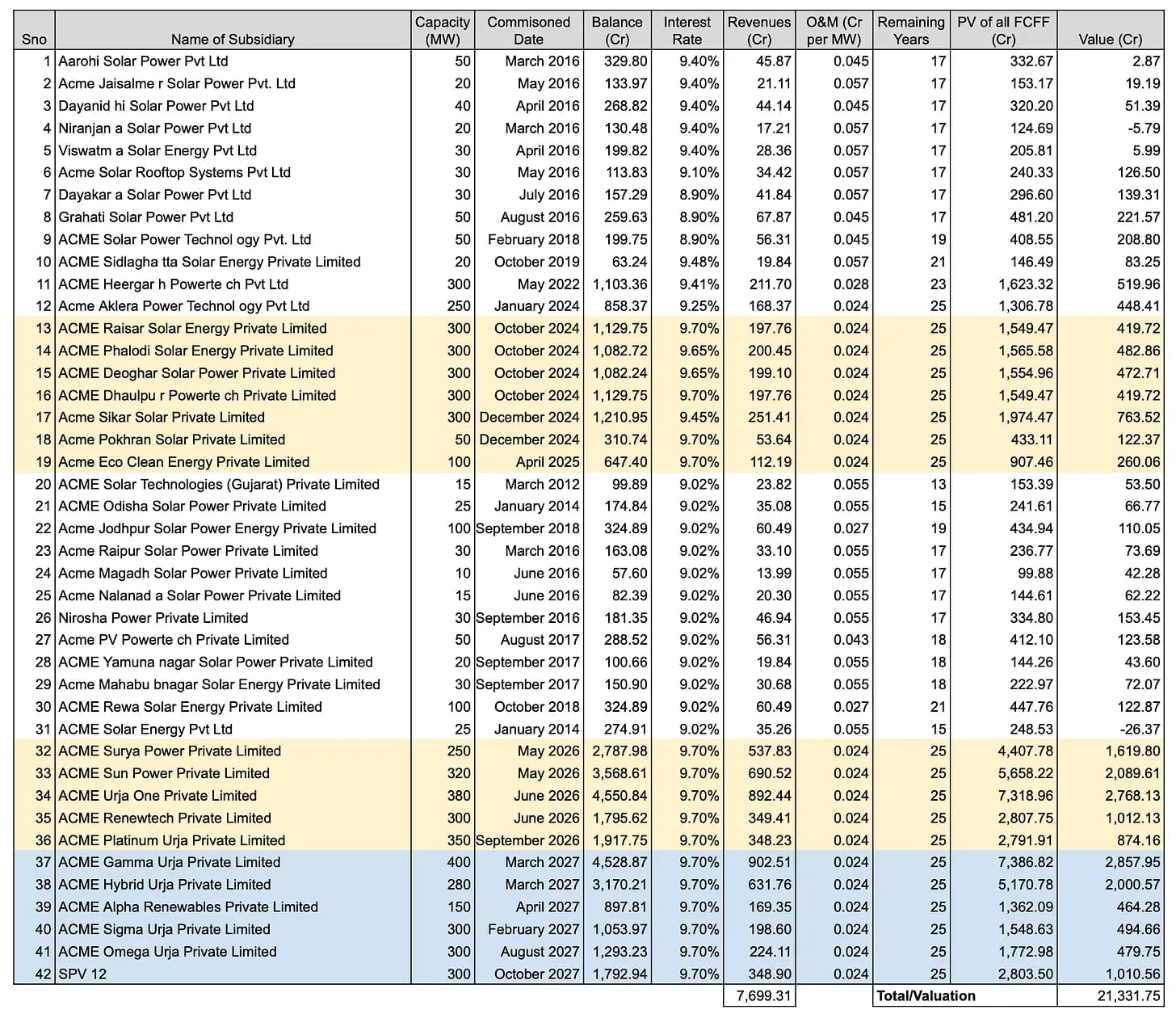

Valuation

To calculate the value of ACME, I discount the cash flows of each of their existing and future power plants (these are in various stages from already under construction to only PPA signed to only LOA signed).

I assume that no sales after the 25 year PPA expires so no terminal value calculated, just 25 years (or less for existing power plants) of cash flows discounted.

I use cost of equity as 14.2% (based on this EY survery -https://nsearchives.nseindia.com/web/sites/default/files/inline-files/TheCostofCapitalSurvey_IndiaInsights2024_EY_NSE.pdf) and cost of debt of 9.4% (from their RHP).

The value of the FCFF I arrive at is 21,331 cr. Subtracting net debt of 6,882 cr (as per todays Q3 presentation), I get a valuation of 14,449 cr. The market cap is currently 11,545 Cr as of close today (29 Jan) so about 25% upside.

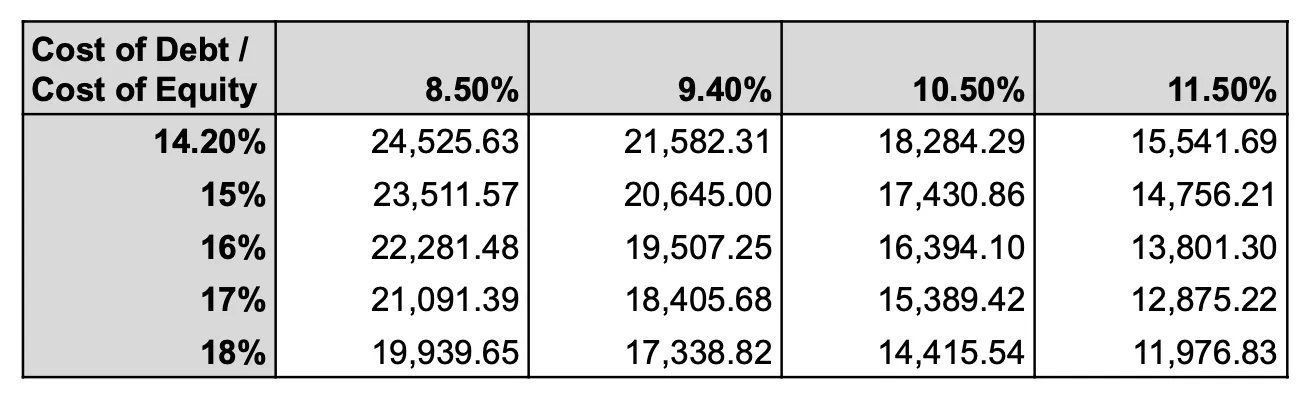

Sensitivity Analysis

For convenience, I ran a sensitivity analysis with different cost of debt and cost of equity

Right now, it looks like the market is valuing ACME at a cost of equity of around 17% which might be justified given that they (and all renewable power generation companies) have very high operational leverage.

Risks

Marco Risk

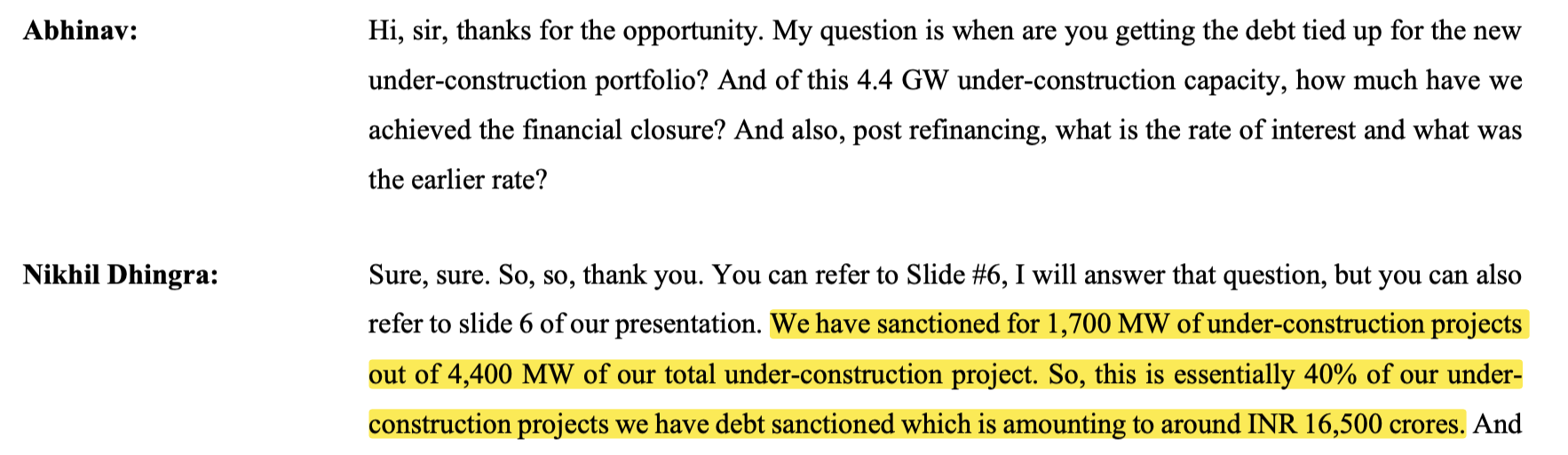

Equity XIRR is very sensitive to interest/coupon rate of debt. PPAs are 25 years long but in India, you don’t get such long duration debt. In ACME’s RHP, you can see all are around 5 years long so you have to refinance 5 times during the project lifetime.

Higher interest rates at time of refinancing can push a project’s XIRR to negative as PPAs do not have any renegotiation component as far as I know (I’m sure they would have mentioned it in the RHP if it did ![]() )

)

Project Delays

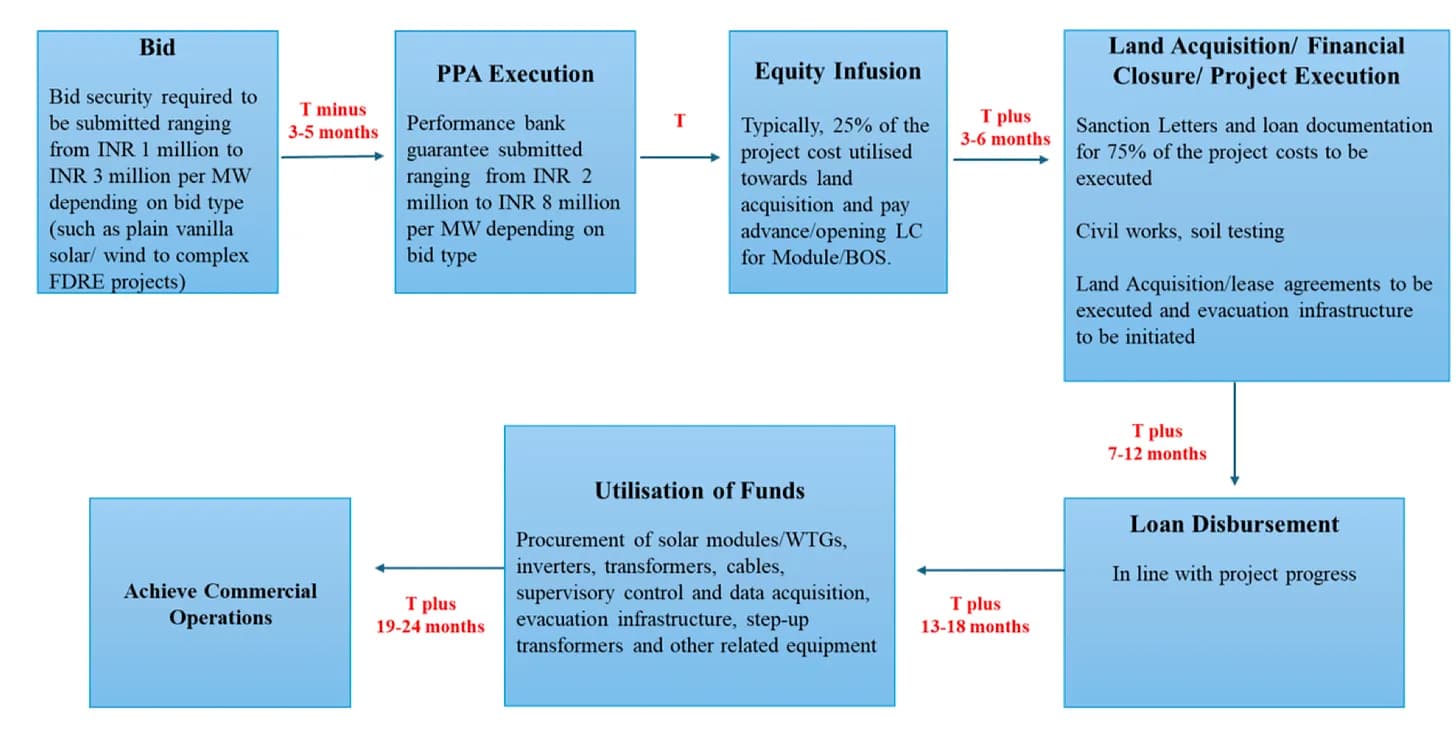

There is a construction period between loan disbursement and commission of project, that ACME estimates in their RHP, of 7-17 months.

In this period, you have debt servicing costs but no sales from the project. If there are delays, then this drags down PAT for the quarter.

For example - guidance for Raiser, Phalodi, Dheoghar and Dhaulpur projects was Oct 24 but they were commissioned only in Dec 2024 and guidance for Pohkran, Ecoclean and Sikar projects was Dec 2024 but they are still under construction as per Q3 presentation.

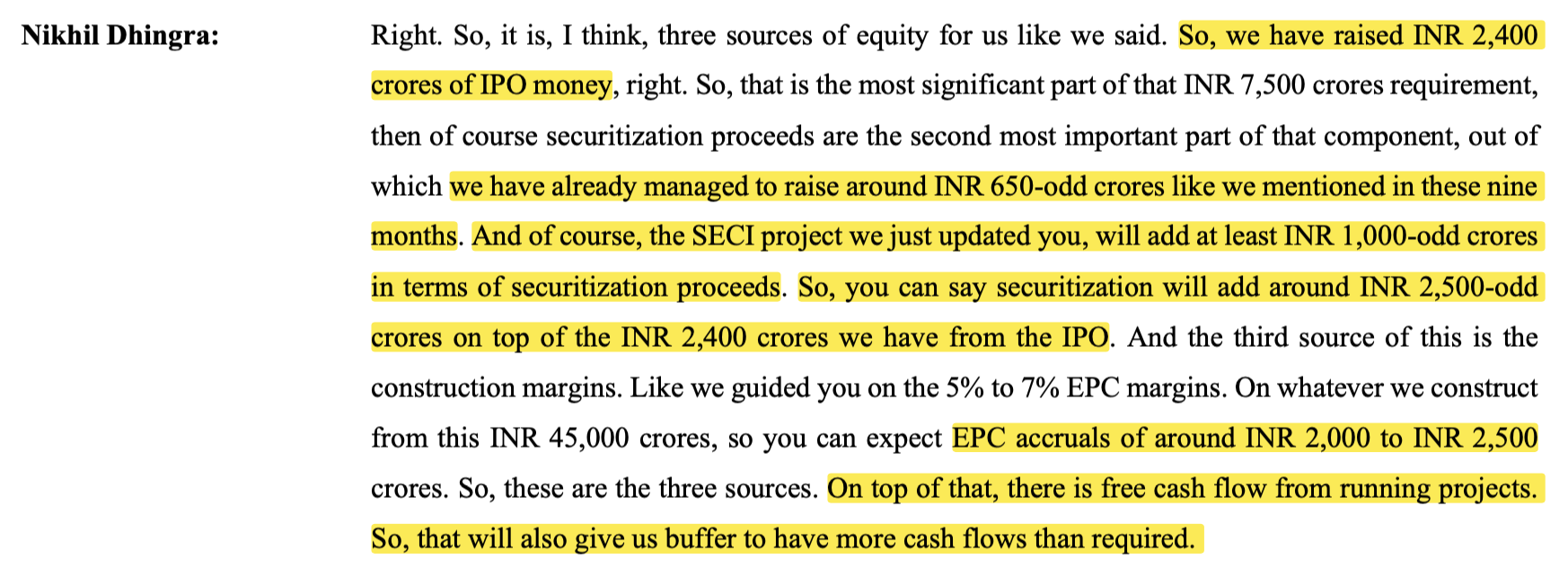

Dilution Risk

I did some preliminary analysis so not sharing the figures yet but it looks like they currently don’t have enough to make the equity contributions of all their future projects. So they could dilute shareholders by raising this amount from the market.

Disc: Invested at ₹179, plan to add on around this level and below whenever the opportunity arises