Abbott has seen OPM expansion every few years. Sudden spurt in profitability is due to increase in margins. Is this margins sustainable and they can further expand? Any one closely tracking can provide mgmt commentary or insights. Else stock may see time correction in a band with 10-15% return for next couple of years till any new trigger for margin expansion.Similar pattern is seen from 2014-2017 when 10-12% of growth in Net profits ,followed by sudden spurt in 2018 due to margin expansion. Also significant increase is seen in “Other income” in 2018 and current fiscal.Any one aware from where it has come and will remain sustainable in future.

On your query on other income jump:

Mgmt. Plans to launch a large number of new products going forward. This can be found in their commentary/interviews.

I think 15% OPM is a fair assumption on average.

The business has a very high ROCE and pays out around 30% as a dividends on average so the company should be able to reinvest bulk of its earnings at a high return.

I dont know about any triggers on the margin expansion, however the company has grown its sales by atleast 10% each and every year for the last 10 years. (not cagr but every single year). That is definately something quite impressive.

Thematically Indians will consume more quality or “branded medication” as income rises and consumption increases. They dont have any overseas exposure, it is more of a branded consumer kind of a business, difference being that they sell pharma/healthcare products. So broadly in the long run they should grow well and throw out quite a bit of free-cash.

I think they should continue to grow in a stable manner. They are market leaders in quite a few of their segments and the business has great metrics, akin to an FMCG business. I do not know about the next 2 years share price but if you have a 3-4 year plus view I think you could see 15%+cagr incl. dividends.

Median PE for the last 8 years has been around 35x. Companies with an “FMCG” nature and strong brands with such return metrics coupled with a MNC parentage might never trade cheap per se. That is something only each individual can take a call on.

Risks are that the govt can put price caps etc: but that is very hard to do in India. There is no quality control over generics. A doctor cannot prescribe a generic drug to a patient because the doctor will be unsure about the quality checks that the govt has put into place, if any at all. Atleast reputed pharma companies have some quality regulation as they are indeed worried about their brands. This is because they can command a premium due to their brand and are hence incentivised to invest in quality control. If the industry is commoditised there is no incentive to invest in quality and everyone will look to drive down costs. In India this proposal may not be feasible from an employment point of view and a health point of view. So that risk will be an overhang but I think that is all it will be.

Another concern is the parent has an unlisted entity but this has not hampered the performance of the listed entity or its shareholder wealth creation.

They also have a cash balance that has been increasing quite rapidly over the years. The promoter owns close to 75% as it is. This build up of cash and high promoter holding could make them a delisting candidate.

11 Likes

Hi

I have been trying to figure out some stuff related to Abbott India’s global contribution to Abbott Laboratories listed in the US. Some of my observations. Also within India the non listed entity what does it exactly generate.

So Abbott in India is listed as Abbott India Ltd. As per SEC filings (form 10K) there are a total of 5 subsidiaries in India

- Abbott Healthcare Private Limited

- Abbott India Limited (listed)

- Alere Medical Private Limited

- Inverness Medical Shimla Private Limited

- St. Jude Medical India Private Limited

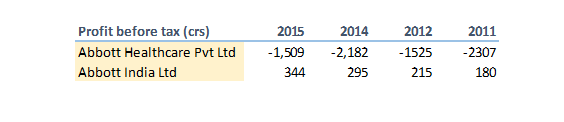

I tried to look around for revenues for all the 4 non listed companies but I didnt find any details on St. Jude, Alere & Inverness seem to be medical devices companies (not sure). Abbott Healthcare is the primary unlisted entity. Now I tried to get all financials for Abbott Healthcare but from 2016 onwards till last AGM which happened in November 2018 no financials are available with ministry of corporate affairs (if I have committed an error please help here).

I was a tad surprised with these numbers. For 2012 & 2011 I couldn’t figure out the sales for Abbott Healthcare. For 2015 & 2014 it was 3,813 crs & 4,197 crs respectively (Abbott India Ltd had 2,289 crs & 2,276 crs respectively). The depreciation expense in 2015 & 14 seem very high at 1,851 crs & 2,275 crs respectively, wonder whether this is to do with some Piramal related stuff. I don’t know.).

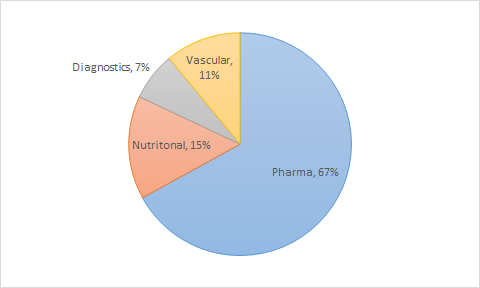

I am interested to know more about Abbott Healthcare Pvt. Ltd. because it holds certain products which are quite good. Overall Abbott globally is structured into

- Pharma

- Diagnostics

- Nutritional

- Cardiovascular & Neuromodulation

I think nutritional division in India is via the private entity.

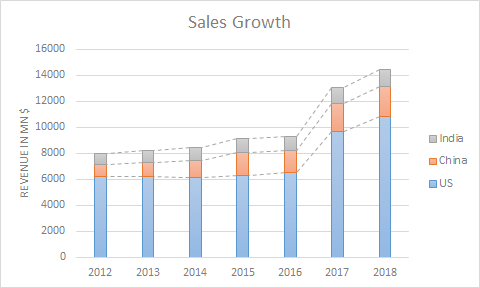

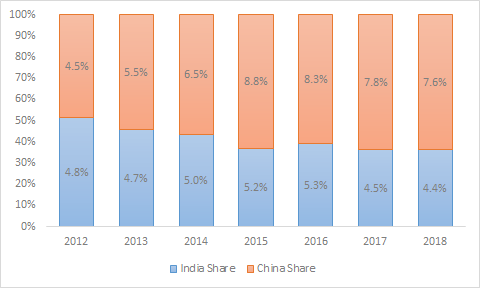

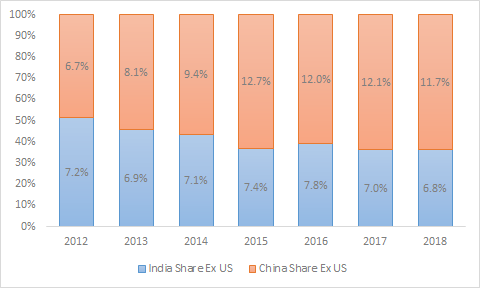

Coming to overall conribution of India to Abbott globally. After US the largest market is China followed by India, these 3 made up 47% of global sales for Abbott in 2018.

Will keep sharing as I dig around more.

Regards

Deepak

disc: not invested. just studying.

15 Likes

Very good detail and inputs. Pls share further details.

Hi

Now looking at the product portfolios.

For Abbott Healthcare Pvt Ltd. as per their 2015 filings (like I said I have not been able to procure latest report of AGM of Nov 2018) following is the breakup of revenue streams.

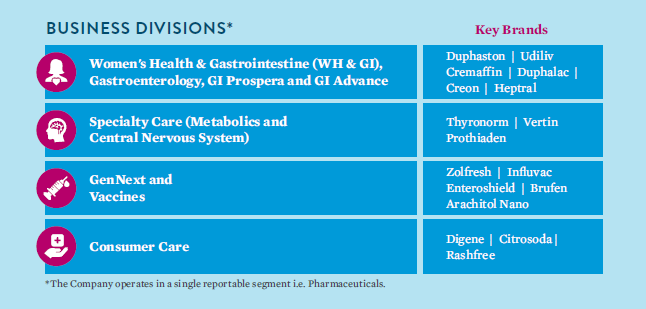

For the listed entity Abbott India Ltd. their business segments are divided into

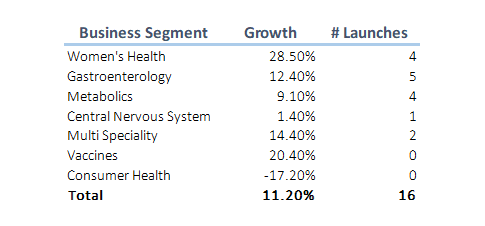

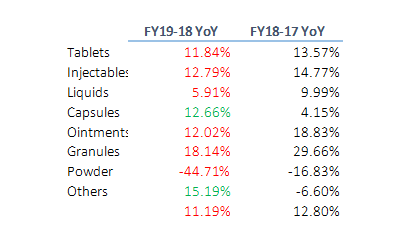

In 2018 the Women’s segment grew 19.1%, vaccines by 59.7%, metabolics by 15.3%

Their website gives a merged product portfolio of 600+ products across

- Pharma

- Nutrition

- Diabetes Care

- Diagnostics

- Vascular

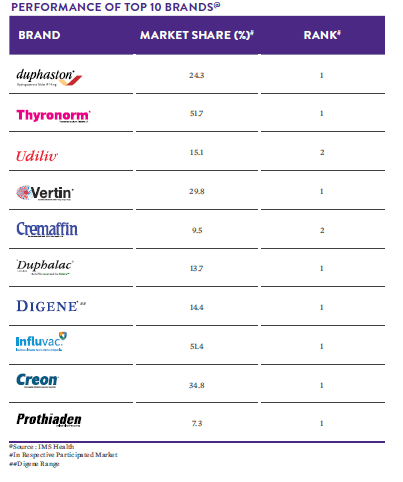

The listed entity’s top 10 brands in 2018 AR

My father is a surgeon and I know for sure Influvac and Thyronorm are heavily prescribed in their respective use cases. Have a family member whom Udiliv helped.

Nutrition which I feel could gain a lot of traction with rising income doesn’t find place in the listed entity.

Globally Abbott Laboratories is structured around the areas I mentioned in my last post but many brands are not under the listed entity in India. I am not sure even if those are sold in India.

So now I wonder how do we see the current portfolio of products evolving and what new gets added to it. As they have mentioned in the 2018 AR that they operate only in Pharma.

Also I forgot to mention the unlisted Abbott Healthcare Pvt Ltd parent is Abbott Asia Holdings Ltd (100%) based out of UK. This finds mention in the list of subsidiaries in the 10K filings to SEC.

Regards

Deepak

10 Likes

Hi

The FY19 AR is up now. I was quickly going through it to see the product suite changes and developments. Some notes below.

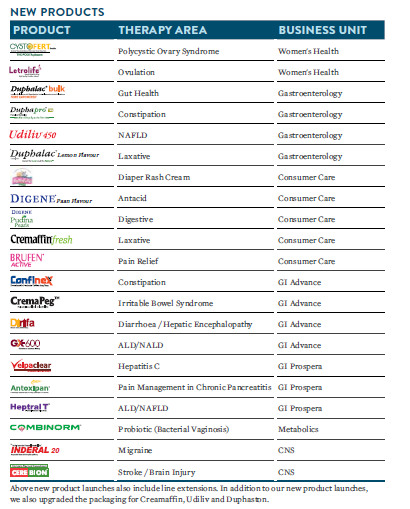

- 16 new products launched in the year

- Sales grew by 11.2%

- PAT grew by 12.2%

- As per some market research they grew 1.8x times the market

- Profit for the year grew by 12.2%.

- Claim to have outperformed consistently in Women’s Health, Gastroenterology, Metabolics, Pain Management, Central Nervous System and Vaccines

- The Consumer Health portfolio, led by Digene, is going through a tremendous turnaround. Intend to launch more products in this space.

- 6 brands appear in the list of top 100 brands of Indian Pharmaceutical Market

- 9 of top 10 brands are leaders in their respective participated market

- EBIDTA margins grew from 15.2 in 2017 to 18.7 in 2018 to 18.9 in 2019

- Claims to have leadership position in most of therapeutic areas it operates in

- One of the lowest attrition rates

- Launched “a:care” a digital healthcare initiatives. I personally dont like these forays honestly

Performance of the various business segments:

-

Women’s Health

Strong growth of 28.5% in this therapeutic area during the year, mainly led by Duphaston

which grew by 29.1%.

Launched 4 new products i.e. Estrabet Gel (Menopause), Fertifoid (Male Infertility), Doxstem (Nausea and Vomiting in Pregnancy) and Combinorm Wash (Vaginal Hygiene) were launched in this therapeutic area. -

Gastroenterology

The Company grew by 12.4 % in this area during the year, mainly driven by Udiliv and Duphalac.

Launched 5 new products i.e. Cremagel H (Anal Fissures), Dezoflav (Hemorrhoids), PepIBS (Irritable Bowel Syndrome), Lolept Injection (Hepatic encephalopathy) and Lolept Sachet (Hepatic encephalopathy) were launched. -

Metabolics

The growth of this therapeutic area during the year is 9.1% mainly driven by Thyronorm which retains flagship position in its segment.

Launched 4 new products Methimercazole (Hyperthyroidism), Thyronorm 37.5 (Hypothyroidism) Tenefron (Type 2 Diabetes) and Tenefron M/M Forte (Type 2 Diabetes) were launched. -

Central Nervous System

This therapeutic area showed a negative growth of 1.4%. Vertin (Vertigo) and Prothiaden (Depression) continue as the market leaders in their participated market.

During the year, Inderal F (Migraine Prophylaxis) was launched. -

Multi-Specialty

This therapatic area has shown a growth of 14.4% during the year. The double-digit growth was mainly driven by Zolfresh, Arachitol Nano and Brufen. Zolfresh retains number 1 position in its participated market.

Launched 2 new products Nefosar tablets (Analgesic) and Nefosar Injection (Analgesic) were launched. -

Vaccines

The Vaccines showed strong double-digit growth of 20.4% and contributed 3.6% of Sales for the year. The growth was mainly driven by Influvac, a number 1 product in its participated market. -

Consumer Health

During the year, this business showed degrowth of 17.2%.

However, the Company focuses on connecting with patients through positioning of its products mainly through mass media, social media and point of sale promotion including new advertisement and marketing strategies to achieve the growth of this portfolio.

Summary of Business Segments

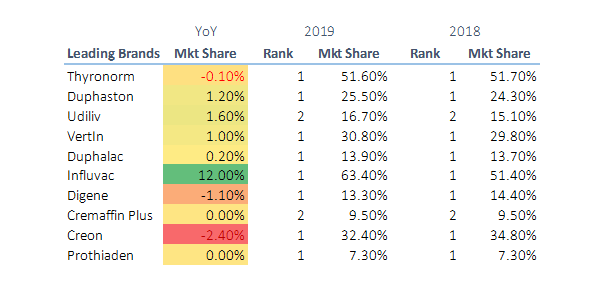

Summary of changes in market share of leading brands

Changes in Sale of Products

Regards

Deepak

disc: just studying. not invested only tracking.

14 Likes

Thanks for the color. Abbott Labs of US is a dominant player in the medical diagnostic equipment. Is there any news or info that in future those products may be rolled out in India through the listed entity. I know they sell Abbott US stents in India. Not sure which entity sells them

1 Like

Thank you so much for the information. Do you have any breakdown of percentage of revenue in the seven business divisions mentioned and margin in each of the division… Please let us know whether any conference call is available in public media .

Thank you

Hi @goutam

Revenue break up in the segments is not mentioned in the annual report only growth in segments. I can write to them but I doubt they would give us this.

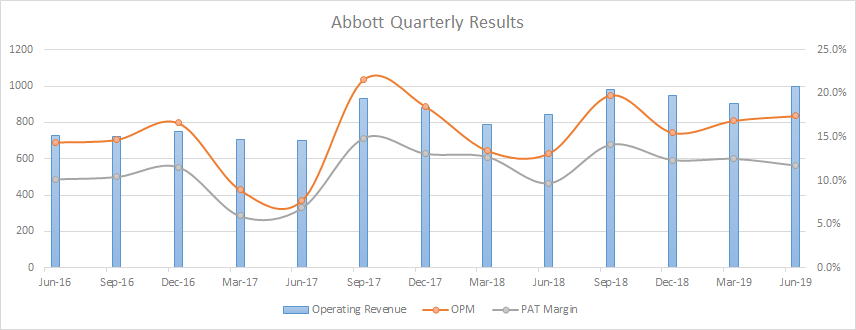

Also quarterly results came out. Decent.

- 18% increase in operating revenues from June last year

- 10% increase in opertaing revenues since Mar 19

- 400bps increase in OPM since Jun 18

- 200bps increase in PAT margin since Jun 18

- 500bps increase in OPM since Mar 19

- 110 bps decrease in PAT margin since Mar 19

Abbott Q1FY20.pdf (1.3 MB)

Rgds

Deepak

disc: not invested. studying. tracking the company.

I am still invested but have cut my exposure (since the story is getting too well known and I found better opportunities)

One of the key risks everyone is ignoring in my opinion is branded generics getting banned in India

1 Like

Can you pl share the other better opportunities you mentioned over Abbott India

My 2 cents: I work for Abbott US and I know that they are hiring for Abbott India IT and looking for expansion which is a positive sign always.

44% price increase YTD vs 11% increase in earnings. PE is expanding. Even in days when index are sliding Abbott is able to make up moves. Pharma Fmcg hybrid with MNC parent seems to be preferred by market.

This business is distinctly different from other Pharma companies that manufacture APIs or do contract manufacturing, or are Biotech firms that need to link up with a go-to-market provider. With a strong brand and medicines for lifestyle diseases which are mostly repeat businesses with a lot of stickiness, Abbott is closer to Johnson & Johnson than it is to say, a Lupin or Biocon.

They are also going beyond pills to provide what they call a pill+service model where instead of selling just the pill, they are selling “Care”. They are doing some interesting stuff with feet-on-the-street building and strengthening their distribution, organising diagnostic outreach to get people diagnosed of ailments they have cures for, to expand their market (like collaboration with Metropolis labs for Vit-D, Gutfit programme, in addition to their Thyroid, diabetes and liver programmes). What I also liked was that the ailments they are focusing on are rampant in India - be it Thyroid (1/3rd of India has some Thyroid related ailment says a recent survey), diabetes (diabetes capital of the world), fatty liver, vitamin-D & calcium deficiency, migraine and heart. The market is fairly large it appears for most of these. They have several other products in the pipeline as well.

Given the size of the opportunity, its not surprising to see them advertising aggressively on all media of late. It looks like they are going to be bringing in a heart-related medical device (Confirm Rx device) which is probably why they are advertising aggressively on TV.

They have also appointed Mr Mark Murphy II as additional director of Abbott India, who appears to have been involved in the development of this device at St. Jude Medical that Abbott seems to have acquired.

The more I dig, the more I seem to like this business but the unlisted entity sticks out like a sore thumb. Pediasure and Glucerna belong to the unlisted entity and I hope it gets merged here soon, if at all. If a listed entity is paying for ads, the unlisted entity gets a free ride with the mindspace captured? Doesn’t appear fair.

Price controls are another risk here but going by the size of the opportunities, I think it would be possible to make a decent buck here even with price controls, as it appears to be happening with Thyronorm. At Rs.170 a bottle for 100 pills, that have to be taken lifelong everyday by a large portion of a large population (they can afford to pay for a Rs.300 Thyroid test upfront for the Patient to get them diagnosed, as they have a 50% market share in the hypothyroid market, to acquire a lifelong customer) and with several other such products in the basket (most of these are already market leaders), it may not be a bad long term bet.

Disc: Invested

AR has more details - https://www.bseindia.com/bseplus/annualreport/500488/5004880319.pdf

13 Likes

Which survey?

Medical journals peg it around 5% at most, both globally and in India too.

I saw that article and its from 2011 so looked for something more recent and came across these.

It looks like numbers are up as diagnosis is now easier and accessible. Anecdotally, I have had 3 in the family and extended family recently diagnosed for hypothyroidism in the last 1 year.

2 Likes

The big question to me is if this device and other b2c machines will be launched via listed or unlisted entity. What is rationale to have an unlisted entity?

1 Like

One of my friend works as tech head for a medical device start up which is specialized in Vertigo treatment. He says Abbott through its Indian arms either from Listed or unlisted entities sponsor many programs to support start ups. There isnt any clear cut differentiation between two entities. In fact in the past we have seen Abbott India top management joining parent company.

In terms of business, Abbott India grew faster than Abbott Healthcare. Despite acquiring Piramal’s healthcare division and holding some niche brands Abbott Healthcare isnt growing very fast.

I have been tracking Abbott India from quite sometime however never got opportunity to enter. @phreakv6 Any views on valuation?

1 Like

Yes Abbott Healthcare is growing sub 2% or so while Abbott India is growing in double digits. I think though the unlisted entity is a worry, the focus appears to be on Abbott India as all the new launches appear to be happening in the listed entity. As for valuation, I go with simple back-of-the-envelope calculations. If the business grows at the same rate it has grown in the last 10 and if we go with the lowest possible multiplier, we should still be able to make a CAGR of 10% while median valuation should fetch a satisfactory 14% CAGR for the next 10 years. I am replacing my FDs which give me abysmal 7%, so I would take that.

Besides, Abbott is paying 36% tax on average for the last 5 years, so the Corp tax cut should bring the current P/E down to 40 levels. With about 70% reinvestment and a 37% return on capital and enough and more opportunity to grow and the management displaying the hunger for it, I would think even current levels are attractive. I started buying around 9200 and have added more in 5 digits as well. It may not be attractive if your return expectations are higher. Being an illiquid stock, sharp downmoves are possible as well if any NLEM revisions or fixed-dose combination restrictions crop up.

17 Likes

Just to add to the discussion, in 2016 AGM, I had asked them about the unlisted entity having products like Pediasure & Ensure. The management had quoted ‘Abbott USA is spending on advertising & marketing more than Abbott India’ so Abbott India is getting more advantage than Abbott USA.

6 Likes