new promoters are coming and valuations are cheap already after a 60% correction from ATH

1 Like

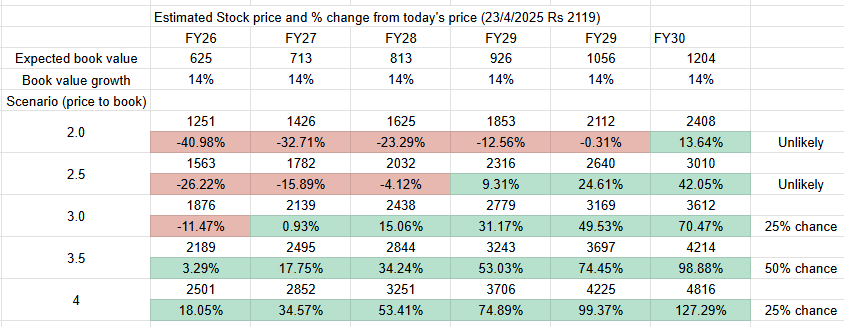

Aavas has run up close to 4.0 P/B - seems richly valued.

I estimated price based on some forward looking P/B scenarios.

Historically - book value growth has been 14-16% - I do not see that changing. Hence, it is hard to believe that market will give a P/B multiple higher than 3.5-4.0.

2 Likes

Promoter has changed, so old calculations will not matter. How things will pan out, no one knows

CVC is the new promoter. The previous PE investor/promoter did not change the strategy much. Growth has been relatively slow under the previous promoter.

You are right it has to be seen what stand CVC takes. Management commentary during Q4FY25 earnings call might provide some early signals.

1 Like

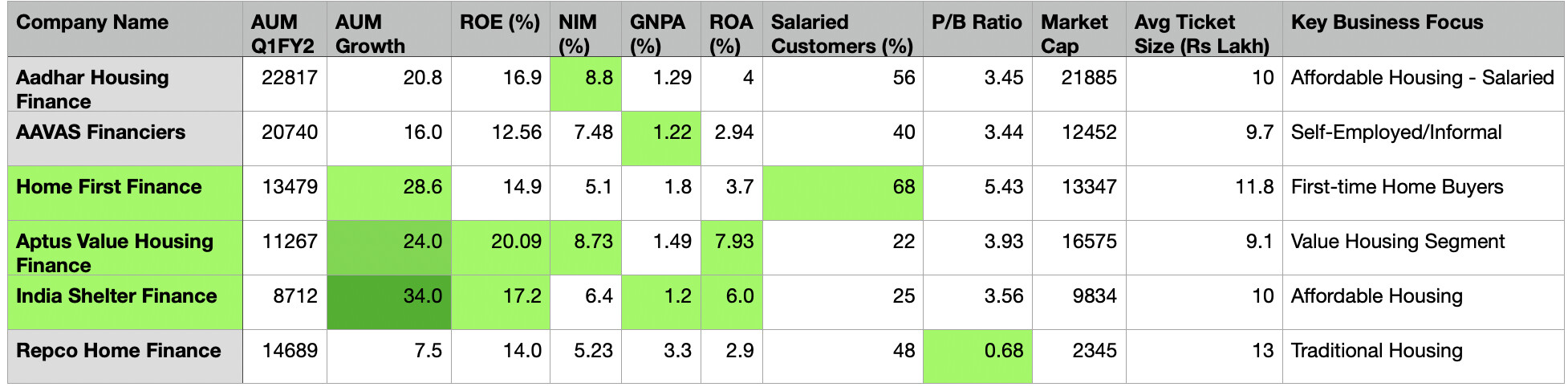

As far as the housing finance market goes, the valuations are generally by the price to book value and AAVAS is at the high end with Bajaj housing and Home First.

Others like LIC, Hudco, Canfin, Repco, Samman etc are valued much more lower. Does AAVAS offer a better offering, definitely as compared to LIC and Hudco. As compared to Bajaj / Home First, I think the offerings are similar. Repco is the most cheapest available

2 Likes

My read on Q4FY25 results and future outlook

Delivered a steady Q4FY25 with 18% AUM annual growth to ₹20,400 Cr and disbursements crossing ₹2,000 Cr for the first time this Q. However, loan asset growth lagged at 16% due to higher securitisation, which boosted ROE (14.1%) but raises concern on sustainability of earnings. Asset quality remains strong (GNPA 1.08%), and spreads, though compressed to 4.89%, may have bottomed out. Management expects spreads to improve with BPLR hikes and cooling cost of funds. With expansion into Tamil Nadu, focus on <₹10L loans (less bank competition), and front-loaded investments in branches and tech, Aavas continues to balance quality growth and profitability. Expected growth next year also around 20%.

At 3.8x P/BV, I will continue to be invested. Need to track trends in AUM growth, securitisation volume, borrowing cost, spread pick-up, and MSME asset quality closely.

7 Likes

Any idea on today’s crackdown? I wasn’t expecting this, it’s back to 1 Year back. I hold over 5% of my NW in this stock and been holding this for past 3 years. Any recent news which could have triggered today’s sell off or is it inline with market today?

Price hit 52W low.

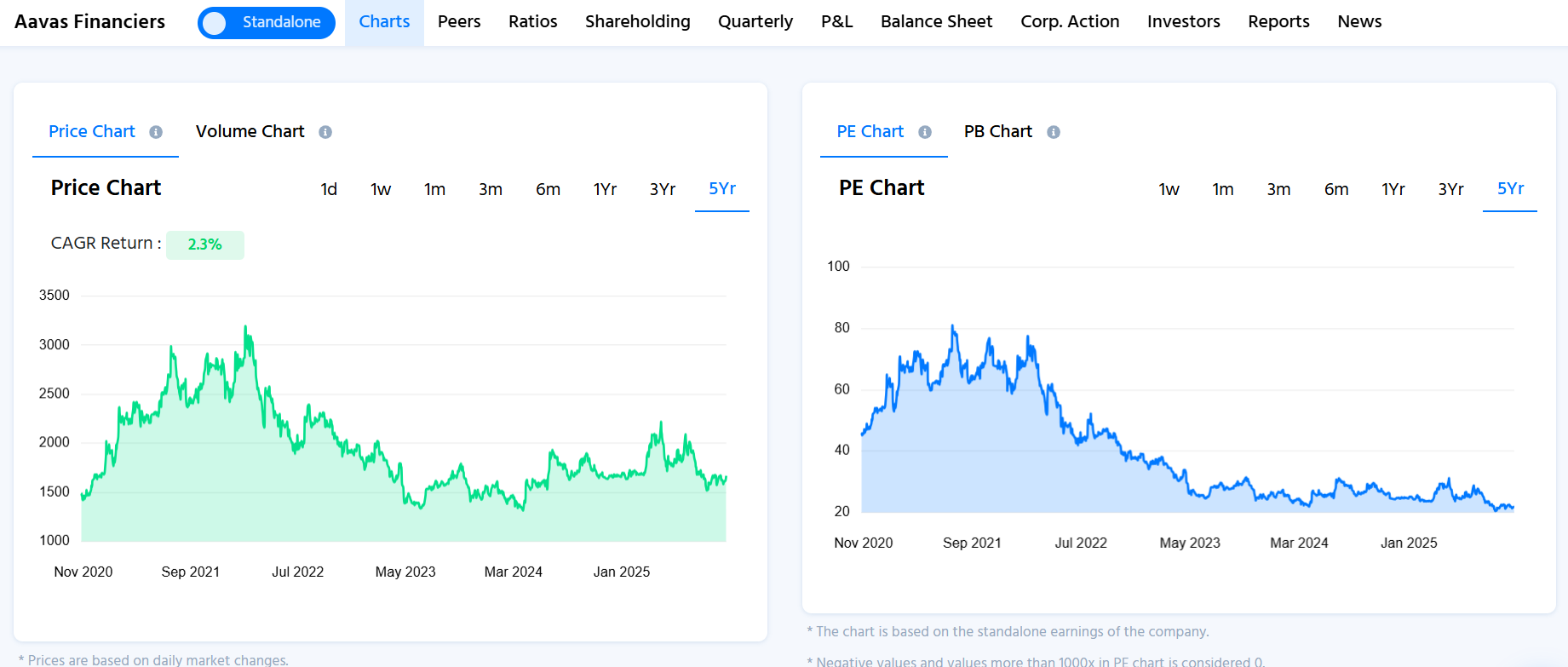

Price to book is 2.8 - lowest ever. Other companies have not dropped. Not sure why there is relentless selling.

1 Like

P/B might be bit outdated as taken from screener. Just curious to know why someone will stay invested when we have companies like India Shelter, Home first and Aptus are growing much faster with better ROE. Looks like 20k Cr AUM bug has caught up with Aavas. AUM growth has been coming down and they are not able to keep up even with their guidance.

1 Like

I had hopes from this stock when it crossed 1900/- with good volumes. But since then price action has turned unfavourable for positional traders like me. Booking some losses and moving on without trying to find the “why”! ![]()

2 Likes

Sorry, bit off topic but, where is this screen shot from?

Hi Anuj,

I had prepared a table based on the last quarters numbers.

This is entirely my own research and personal view meant to spark discussion and get more inputs from the ValuePickr community. It isn’t investment advice.

Aavas Financiers Ltd is a National Housing Bank-registered housing finance company that mainly focuses on low- and middle-income groups in semi-urban and rural India that are frequently underserved by mainstream lenders. The organisation offers home loans for purchase, construction, and renovation, as well as loans against property and mortgage-backed MSME loans. It has its presence in 13 states such as Rajasthan, Maharashtra, Gujarat, Madhya Pradesh, Haryana, Uttar Pradesh, and Odisha through a robust branch network and direct sourcing model.

The firm has recently taken a significant operating change by implementing a realization-based disbursement framework, where disbursements are noted only after the amount is credited to the borrower’s account. The move improves transparency, enhances compliance readiness, and offers a true picture of the business, though it has temporarily resulted in softer disbursement numbers for Q1FY26. The conversion rate of sanctions to disbursements reduced by about 10% below 75%, but normalisation is expected in the next few quarters as the system stabilises.

In the last few years, Aavas Financiers’ stock performance has been inconsistent, with a 1-year CAGR of -5.2%, 3-year CAGR of -8.2%, and 5-year CAGR of +1.9%. This is due to short-term stress on account of the transition to a realisation-based payout model and general valuation readjustments in the HFC space. PE ratio has come down steadily from about 40x in 2022 to almost 22x in 2025, representing a steady de-rating as growth slowed and investors valued the stock more cautiously.

Management has reaffirmed its FY26 AUM growth guidance of 18-20% and anticipates the temporary weakness in disbursements to return in H2 and H3. July disbursement growth has already improved, rising by about 16% year-on-year, and at a current monthly run rate of ₹550-600 crore. By FY27, Aavas hopes to sustain a 20-25% AUM growth cycle once the adjustment to the new disbursement model is complete.

Between June 2024 and June 2025, the promoter holding structure altered significantly with promoter stake increasing to 48.96% from 26.47% following CVC Capital Partners’ entry with its more robust institutional support. FII and DII holdings fell to 29.77% and 11.52%, respectively, as investors rebalanced following the change of ownership. This change indicates infilling of promoter confidence and opens the door for possible long-term stability once growth momentum picks up.

Operationally, the company continues to increase its distribution footprint, with the addition of 10 new branches in September and entry into Tamil Nadu as a fresh geography. Its direct sourcing model is a source of strength, evident in its greater employee-per-branch ratio of approximately 18 versus peers’ 10-12, underpinning customer engagement and asset quality. The low balance transfer-out ratio of 4.9% reflects good customer retention. Recent investments in technology have greatly enhanced efficiency, cutting turnaround time from 13 days to 6 days.

Aavas seems to be moving towards a more transparent, institutionally regulated, and process-oriented organisation. Short-term financial numbers may reflect some softness due to adjustment, but the long-term path seems constructive with persistent emphasis on quality growth, prudent underwriting, and operational efficiency.

Would really appreciate the members’ opinions on the questions below.

- Is the realisation-based model a short-term drag or long-term positive?

- How will CVC Capital’s entry shape Aavas’ strategy and governance?

- At 22x PE, is the stock fairly valued or undervalued?

- Can focus on self-employed borrowers improve asset quality?

- Is 18-20% AUM growth achievable amid transition?

4 Likes

Any updates on what happening in complete housing finance sector?

Everything is down for more than 20-25%.

The housing finance sector is under pressure primarily because affordable housing—the core demand driver for many HFCs—has structurally weakened in 2025. Sales of homes priced below ₹50 lakh fell 17% and new launches dropped 28%, reducing the segment’s share of total housing sales to just 18–19% from 38% in 2019. Developers are steadily exiting this space due to low margins (10–15%) and shifting capital to luxury housing, which offers 30%+ returns, leading to fewer projects and lower loan origination opportunities for lenders. Although government schemes like PMAY and GST cuts exist, outdated pricing thresholds and rising costs have limited their effectiveness, raising concerns that the affordable housing deficit could reach 30 million units by 2030. Markets are therefore pricing in slower growth and lower profitability, which explains why housing finance stocks are down across the board.

company projections shared by TIjori

Aavas Financiers.pdf (1.3 MB)