AAVAS FINANCIERS LIMITED was Formerly known as “Au HOUSING FINANCE LIMITED started its journey from Jaipur, Rajasthan, in 2012 and is now present in 11 states namely Rajasthan, Gujarat, Maharashtra, Madhya Pradesh, Delhi, Uttar Pradesh, Chattisgarh, Haryana, Uttarakhand, Himachal Pradesh and Punjab with total branches of 263.

AAVAS Choose to be present in low- and middle-income segment in suburban and rural areas (people how mostly don’t have access to formal banking)…

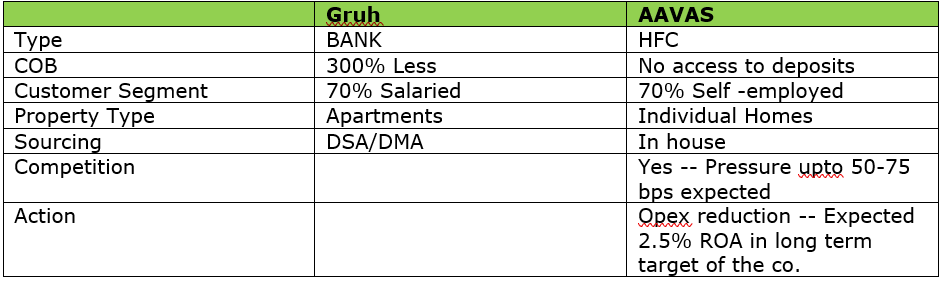

Asset Side:

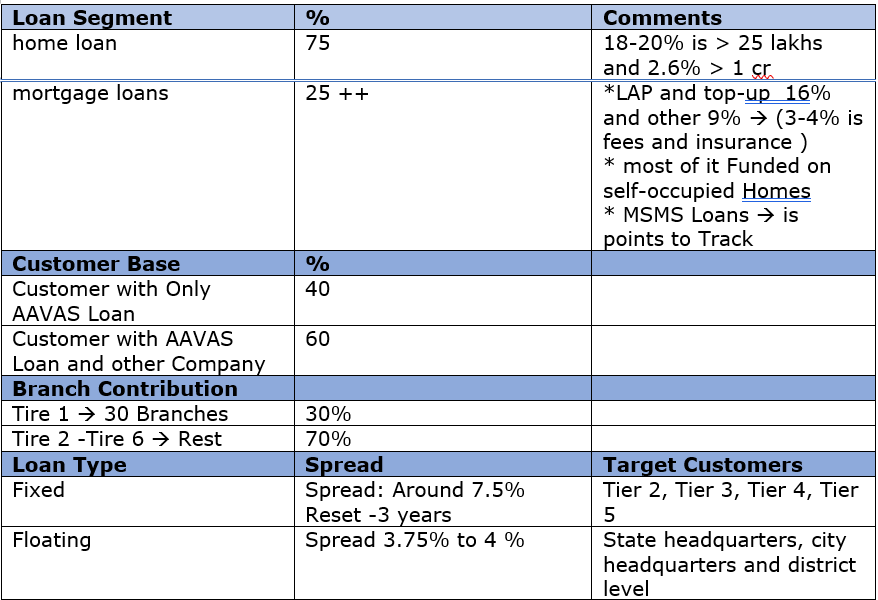

AAVAS provides home Loan (Purchase, Land Purchase + construction) and mortgage loans (LAP , Top-up , Insurance) for salaried and self-employed category.

They have been funding 60%++ to self employed and 40%-- to salaried persons and with a very low average ticket size of 9.1 lakh for Home loans and 6.7 lakh for Mortgage loans.

Company avoids risky assets on book with no developer funding, no corporate loan, no high ticket LAP, no under construction property and finance only Apartments which are 85-90% completed are financed.

Loans are majorly given for homes to be self-occupied purpose (95%+ customers live in this homes) and all the loans are sourced in house with right from lead generation to risk management and collections.

The company Has been very vocal on being non-DSA model (in house sourcing) and would like to continue the same as it would reduce the Asset side risk though it leads to higher operating cost. the company is confident that the higher cost resulted could be mitigated by tighter control over the OPEX.

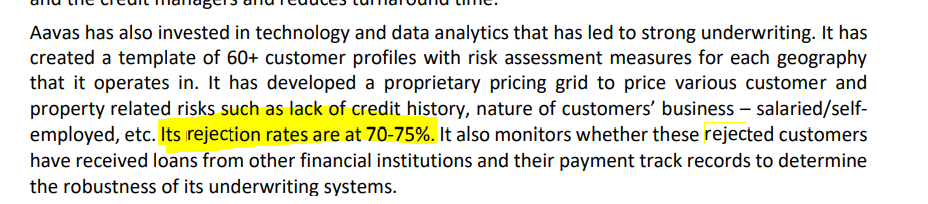

It has 600 credit Managers to assess the risk of the customers and they has apprised over 300 K customers.

The company has brought down turnaround time from 21 days FY14 to 10.6 days in FY 20.

Rejection ratio: 2800 to 3300 approved out of 10,000 applications a month.

Important Statistics on Assets Side ::

Balance Transfer::

BT IN: Company focuses on procuring own customers and is very less reliant on BT IN as source of growth, which is good – 5% of the AUM is in BT

BT Out: BT out is major risk for the company as they cater to informal sector (with high spreads) and put this on Cibil framework. it would be easy for good paying customer to find a better bank/NBFC with cheaper rate.

BT out as per 12-18% of AUM happens as per industry , the company has been trying to counter the same with Analytics and has got down the time to deal/ negotiate with BT Out customer from 5-10 days 1.5 years back to 24 hours

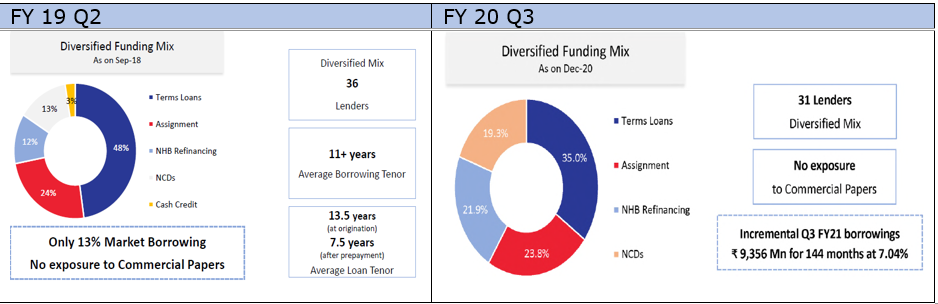

Liability Side:

AAVAS has extraordinary capital adequacy ratio of 53% and with current growth rate would require raising capital in next 2-3 years.

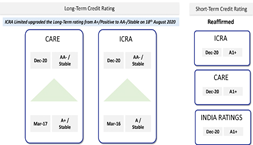

Though the company does not have good parentage, it has been able to raise liability at decent rate and as per the growth needs.

It has been able to get rerated upwards in the past 10 years with a good track record …

Despite have a good credit rating the company never relied on commercial paper or short-term borrowing … and management is very vocal of not having CP on the books…

Asset and liability management:

Company has been following the strategy of long-term liability for long term assets.

Avg tenor of borrowing has been 130+ months for the last 4 years to fund the liabilities.

Disciplined ALM by the company has lead to ALM surplus funds.

The company due to its positive credit rerating has been able to decrease the reliance on bank funding.

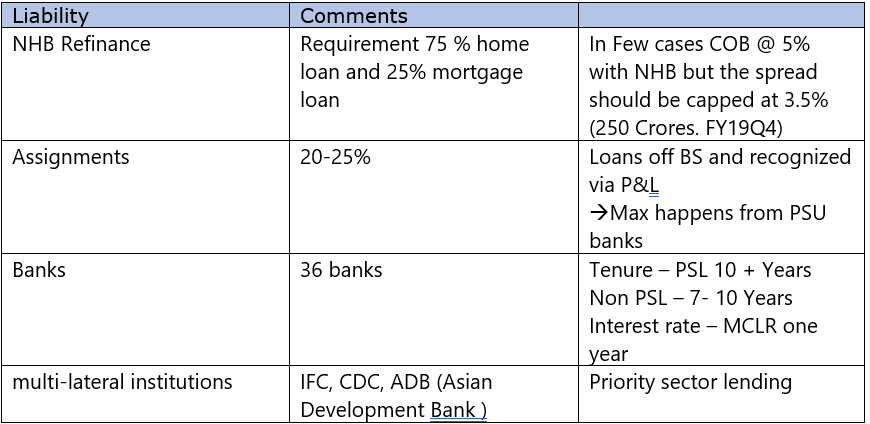

More details on Liabilities

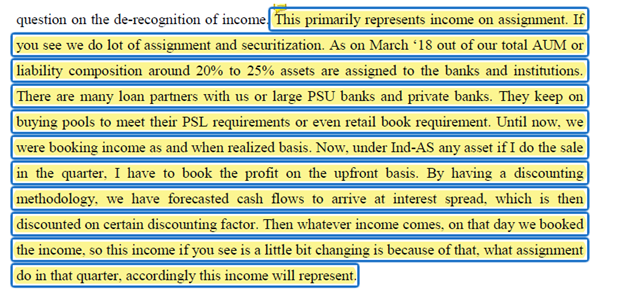

Assignments: as the group assets are under priority sector , Banks would buy the assets on to bank books to adhere to RBI norms. The loans so sold out would be taken off the BS.

Collections:

Company has 350 +team of 12 collection officer’s + 12 lawyers (as on FY 19 )

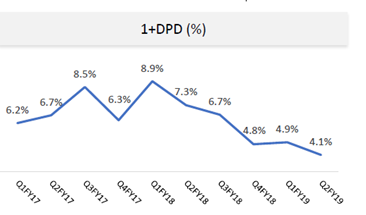

Company has target of keeping the 1+DPD (days past due) less the 5% and where able to adhere to the same up until Covid-19 hit them.

Asset quality as on FY 21 Q3

GNPA at 1% and net NPA at .72%

1+DPD at 8.21% almost equaling the peak during demonetization timing Q1 FY 18 was at 8.9%

AAVAS has been hit by Covid-19 and the full impact is yet be seen and with second wave yet to peak I feel there would still be lot of pain to come by.

Company in concal has stated that two customers segments which have been much impacted due to covid are 1) hospitality (2-4% AUM) 2) school and around infra (school transport , stationery )

Expansion:

Company is taking a block of 5 years to develop in four states.

2011 to 2015 has concentrated on Rajasthan, Gujarat, Maharashtra, MP and Some parts of NCR.

2016-2020 has developed Chhattisgarh, Haryana, UP and Uttarakhand

2020+ has started Himachal Pradesh.

Target of 40-50 branches per year

Branch breaks even in 6 -12 months based on the town and category of branch and avg monthly business per back is around 1.25cr to 1.5 cr

Snap of competition:

To be tracked:

- Covid-19 Present and second wave impact as companies’ customer would have the highest impact of all.

- 1+DPD as per the company 10-15% of this turn to NPA as at present its at 8.4%

- MSME loans, for some reason I have not seen much discussion around this segment both in AR and concalls (I have sent mail to investor relation in 1st week of April , but they informed that they could update only after Q4 number release)

- Expansion, company has gone go to new states (Chhattisgarh, Haryana, UP and Uttarakhand) after 60-75% tehsil level penetration in the first 4 states, but I felt they are expanding to next set of states too early without exploring the depth of present set – its an unfolding movie would love to watch the play.

- Opex reduction, company has been successful in using technology to reduce the opex in the past (FY 19 -3.8% and FY 20-3.4%) reduced by 40 bps.

Company is planning to keep up with the reduction and target 40bps for next 2-3 years. - Leverage: company has plans to leverage at 5-5.5 once A rated and 7-8 once rated at AA.

Aavas has been grow at good rate over the past 10 years and has been able come strong out of demonetization, But with covid-19 impacting its customer range the most would the company be able to come out with flying colors …lets see the movie unfold .

Disc :: Please consider my views biased and do you diligence.

I thanks two mentors who helped me with ABC and beyond of banking with there online video’s

- Ishmohit Arora

How does Banking work and why doesn't Cash Flow matter? - YouTube - Digant Haria, Partner, GreenEdge Wealth

THE BASICS: NBFCs SECTOR SIMPLIFIED WITH DIGANT HARIA - YouTube

Indian Investing Conclave