There has been a whole lot of doubt around the company because of change in management. That’s why the stock has been consolidating for a long time. But this quarter has turned out to be excellent. Hope it continues the moment.

1 Like

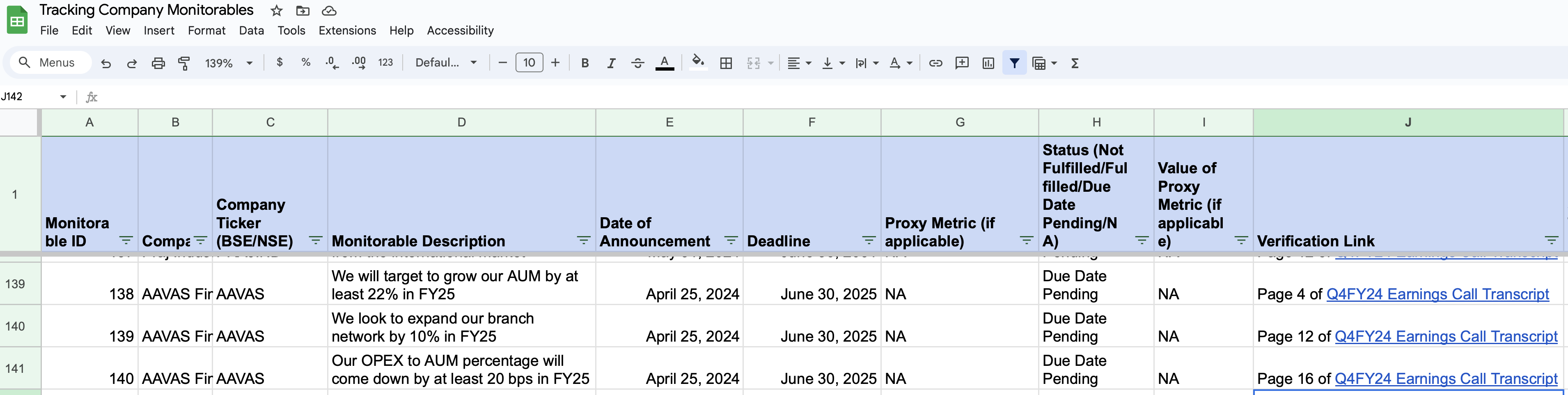

Hello,

In the below tracker, I have started tracking important company goals for AAVAS Financiers.These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-2.xlsx (123.5 KB)

15 Likes

Wow! Thanks for sharing this @aadhar.aggarwal. Such a nice way to track and understand/evaluate management quality basis the guidance. Some managements keep on shifting the goalpost but have proven themselves in the past. Not sure how one would analyze such scenarios.

This is specially helpful as a quick feedback mechanism for working professionals. Gratitude for sharing the file ![]()

2 Likes

So since they own a combined 26.47 percent stake, selling this stake would necessitate an open offer to acquire another 26 percent from public shareholders. Was reading up on this SEBI rule and this is done to ensure that public shareholders have a fair opportunity to exit the company during substantial ownership changes, protecting the interests of minority shareholders. So if this goes through, will the new entity do a buy back? Does anyone know how this works and what is the potential impact during such scenarios?

2 Likes

Hi All , Any one having the idea for Q1 2025 , Business update.

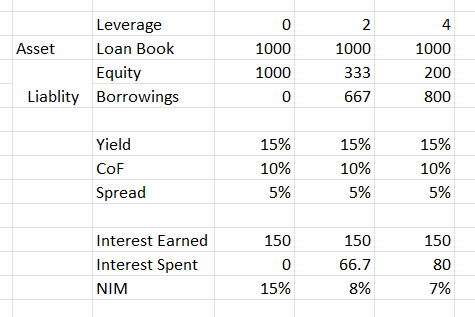

In the latest Credit rating by ICRA, they mentioned the following

Going forward, the NIMs are likely to be under some pressure on account of the higher gearing.

Can someone please explain why NIMs is related to gearing?

From my understanding, gearing is the debt that the company can take, which implies that they can take more debt (according to the statement), which means that either the ROA reduces or they can give out more loans as they’ve more leverage.

How does NIMs come into the picture? Is it because of the ROI at which the new gearing have been given to the company?

Thanks

1 Like

If the interest expenses on borrowed funds is high, it might compress the NIM if the increase in interest income is not proportionate to the increase in interest expense. So need to understand where the new funds are going to be deployed into. If it is for high-yielding loans, NIMs can improve also.

1 Like

Its simple, whenever leverage increases, NIM will decrease, even if yield, cost of funds, spread remains constant.

Its because when leverage is low majority of source of fund is equity component for which there is no interest payment, but as and when leverage increase, % of equity component in source of funds decreases and % of borrowed money increases which increase the interest paid which automatically decreases NIM. Same happens in RoA also. Its just mathematics, nothing to do with business ability or inablity, high yield or low yield, high or low cost of borrowing.

Now when a company is raising money at 9% when leverage is 2, then in most case very same company will raise money at few basis point higher, say 9.2%, when leverage is 3. When you add this to above calculation NIM will further contract

8 Likes