Does anyone know the differences in the pharmaceutical offerings of this company vs those of Aarti Drugs?

1 Like

The company is evaluating for demerger of pharma segment. how does it unlock the value for shareholders?

Does anyone know the long-term contact sizes? 1st and 3rd long-term contract? and term size?

Question to ValuePickers who are familiar with this business:

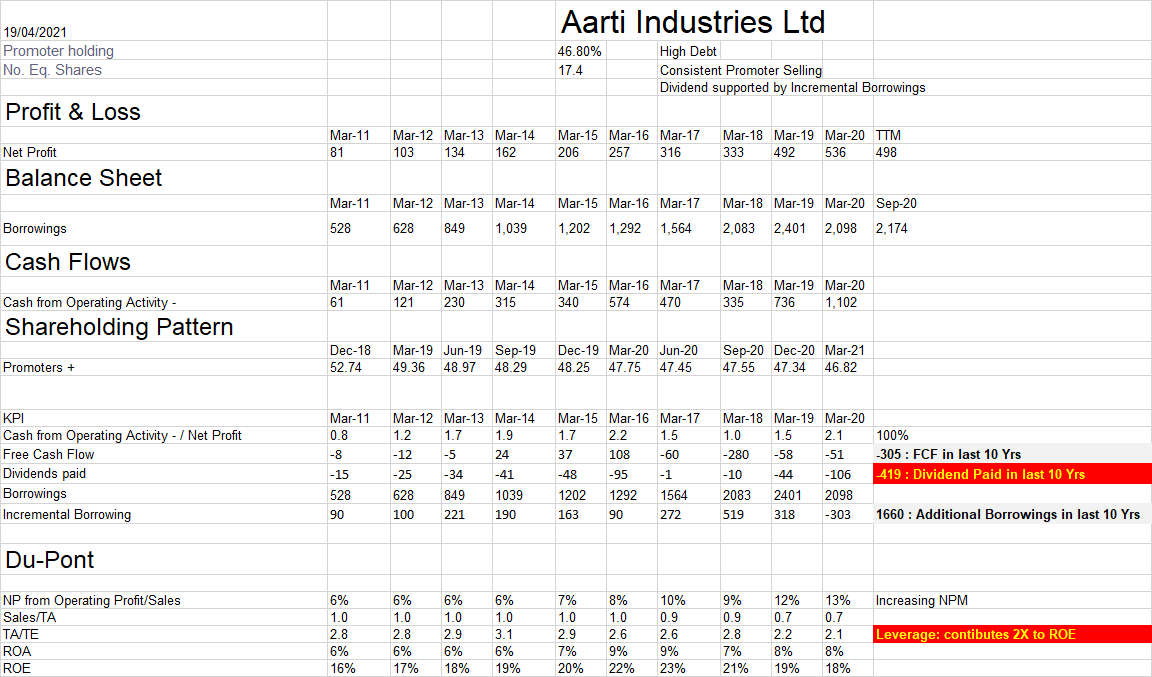

What’s management’s rationale for YoY increase in borrowings? I understand that sales are growing and business is doing higher capex on YoY basis to monetize newer opportunities. However, the perplexing inference from numbers are :

1- Dividend is supported using borrowings (25%- 419 out of 1660- of incremental borrowings are distributed as dividend) when 10 Yrs of data is accounted.

2- 2X leverage resulted in respectable ROE of 18% in FY20 else the ROE would have been ~ 13%

Details as below:

Data Source: Screener.in

3 Likes

Why is company issuing bonus share and at the same time raising fund of 1500 crs.

Can any one explain the rationale

I am not sure why they do this but this is not first time. Few years back they announced buy backs immediately followed by QIP. They keep paying dividends but take on more debt yoy.

Maybe they feel obliged to make existing share holders happy, not sure.

Issuing bonus shares is book entry where bonus shares are issued out of reserves and surplus, while fund raising is required for growth of company. So, both are separate.

4 Likes

Is that mean reserve and surplus is not cash?

One more doubt, the compensation received on account of cancelled contract, why is it recorded as revenue? Shouldn’t it be recorded in cash flow only?

Reserves and Surplus are all the cumulative amount of retained earnings recorded as a part of the Shareholders Equity

Issue of bonus shares - is a book entry

Generally cash transaction should have been there but the companies during bonus issue just adjusts the reserve & surplus and increases the total no of shares

So just change of pockets

2 Likes

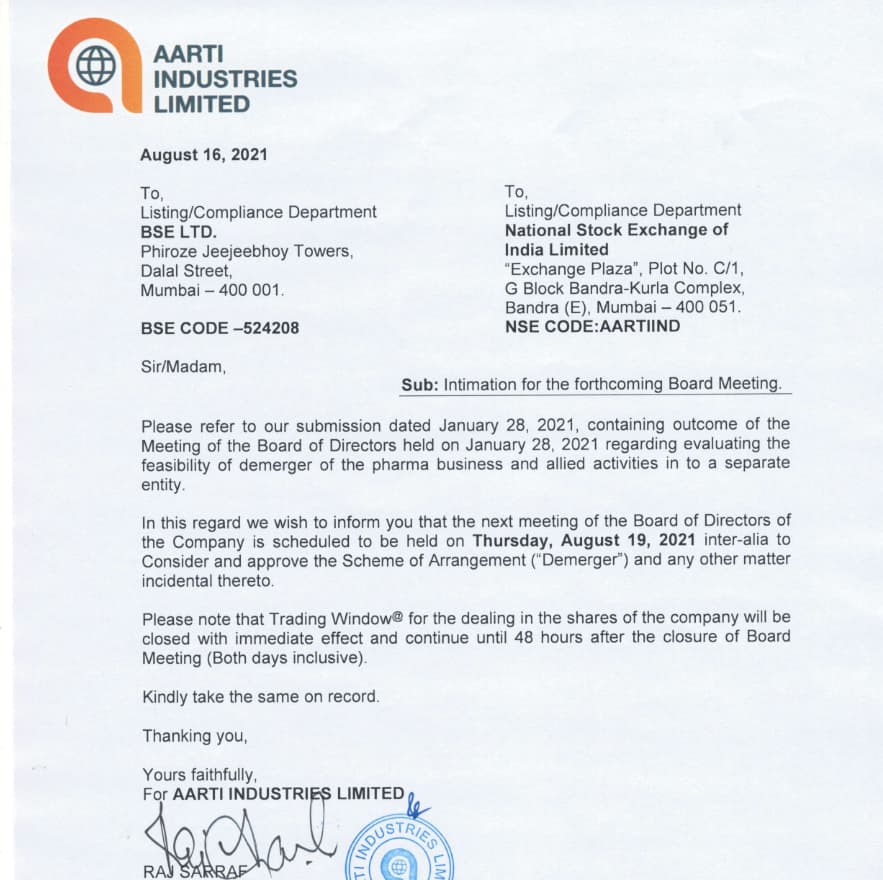

Detailed proposal for demerger is out:

Pharma business and allied activities will be demerged into Aarti Pharmalabs Limited (formerly Aarti Organics Limited) and it will make an application to BSE and NSE for listing.

“Issue equity shares on a proportionate basis to the member of Demerged Company whose name is registered on the register of member as on the Record Date, in the ratio of 1(one) fully paid up equity share of Rs. 5 each in ‘Aarti Pharmalabs Limited’ (formerly known as ‘Aarti Organics Limited’) (“ Resulting Company”) for every 4 (Four) fully paid up equity shares of Rs.5 each held in ‘Aarti Industries Limited’ (“Demerged Company”)

Thoughts and comments invited from people who can understand the entire scheme and help others explain it please.

Disclosure: Held small quantity and traded multiple times. Added a large quantity recently banking on the management that has been pro-investor.

2 Likes

Anyone having detailed analysis of Pharma Business? How to compere with other player?

Ramipril can do wonders for Aarti Inds . Demerger can be a strategy to grow the API including this one.

1 Like

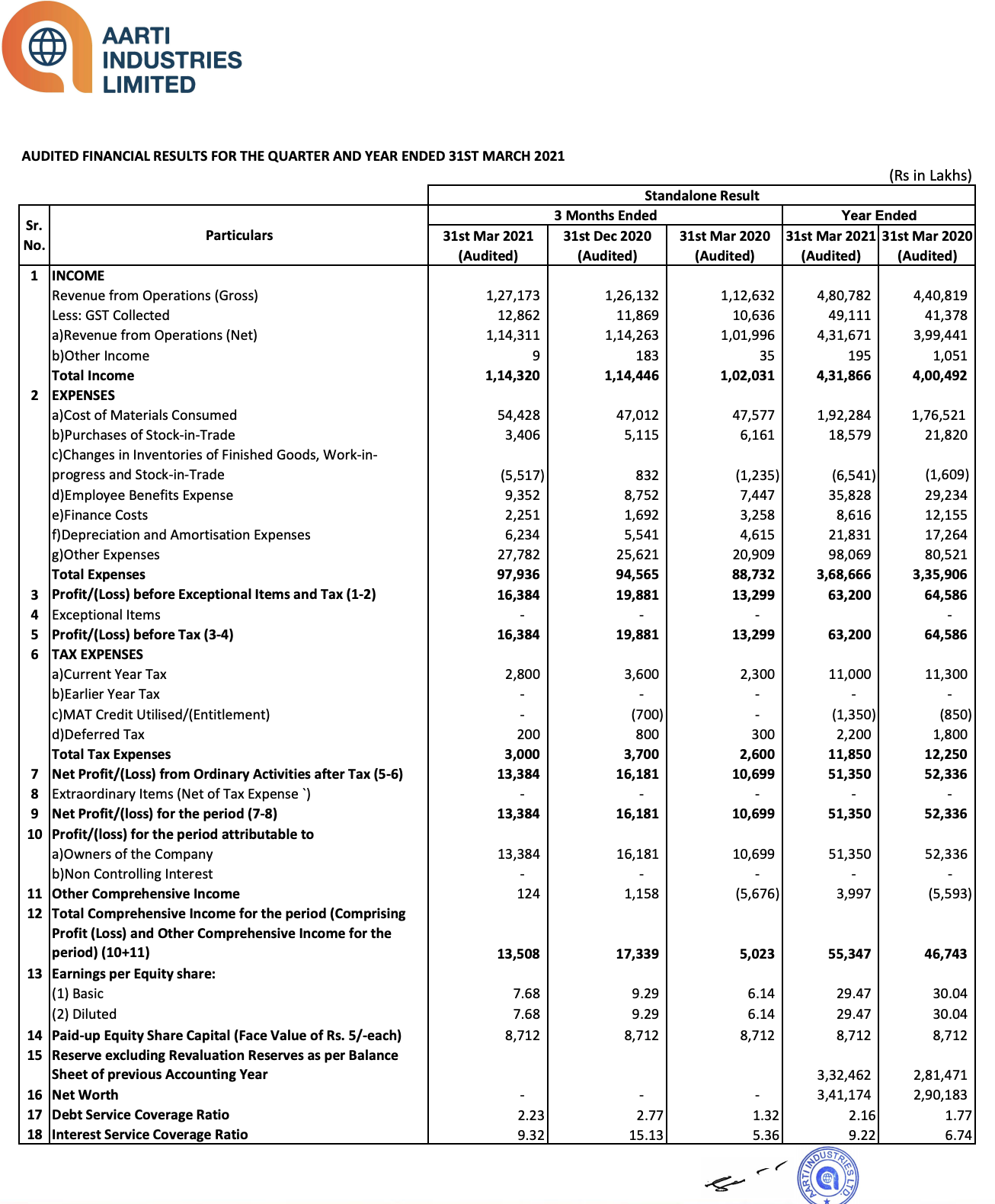

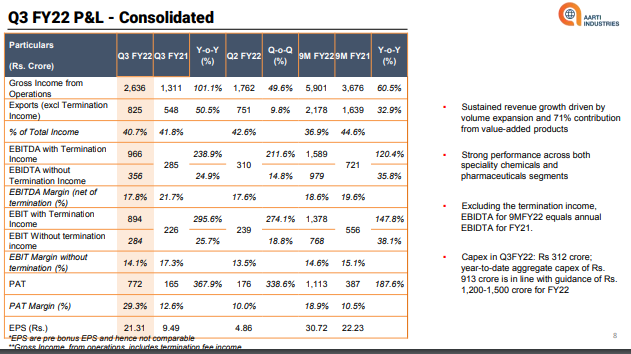

Q3 Results

Note 3.Revenue from Operation for the quarter and nine months ended December 31, 2021, is inclusive of accrual of Termination fees of Rs. 63,125 Lakhs arising on account of the

termination of a long term supply contract by the customer. The Notice for termination of this contract was received by the Company and the disclosure related to the same

was given to the respective Stock Exchanges on June 15, 2020.

It seems the result is not so good . So to look it as good, they added one time receipt as sale and increased their OPM to 41% so that it looks like an excellent result…

It is hard to notice from first look that this adjustment has been made by the company. You have to go deeper in notes to notice this adjustment. Further, you have to manual calculation to know the exact growth of sale and profit.

Not a good practice in my opinion

Disc: not invested

4 Likes

Furthermore, I think they should show this amount in cash flow statement and not in PL statement.

In my limited understanding, the company provide requisition information in the presentation/release explaining imact net of one-time/exceptional items. Even Aarti Industries has done same in their presentation in Q3FY22. Enclosing revelant slide for everyone reference.

As per above slide, even after adjusting onetime income, while EBIT margin is under pressure, absolute EBIT has shown 38% growth over last year, which I believe is excellent.

Dislosure: Holding and among my Top 5 holding. Have sold marginal position last week. My view may be biased due to my holding. Not a SEBI registered advisor, nor recommneding any investment related action in the company.

5 Likes