@Patel_Bhai

I have got Aarti PharmaLab share credited in my demat account. Also, Aarti Pharmalab declared dividend of Rs 2 per dividend with 17 Jan 2023 bring record date. I assume Aart Ind Investor who got share on restructuring would be eligible for dividend payment as same being held by an investor on record date.

After almost 8 years plus holding, I have systematically reduced my Aarti Industries holding to around 1% of my portfolio. Over the period, there were great turning points in investing, companywise and market wise, from Demonetisation, GST implementation, Covid related uncertainty, China+1 to Getting 3 long term contracts, termination of one high margin long term contract and constant selling by promoters during the period. My decision to trim my holding was mainly due to my estimate stable to lower profit for Aarti Ind in FY23 as FY22 has significant income booking from termination fees for agreement. Also, I had significant exposure to Specialty chemical including Aarti Industries/ SRF/ Transpek Industries/Andhra Sugar/ Kama Holding (SRF holding company). Among all companies, I found Aarti Industries being reasonably valued considering in capex and growth prospect.

In my Investment Career, Aarti Industries has special place. In absolute amount wise, this company has rewarded me highest post tax realized wealth in my more than 25 years of investing career. I would always be grateful to the management of the company for this support.

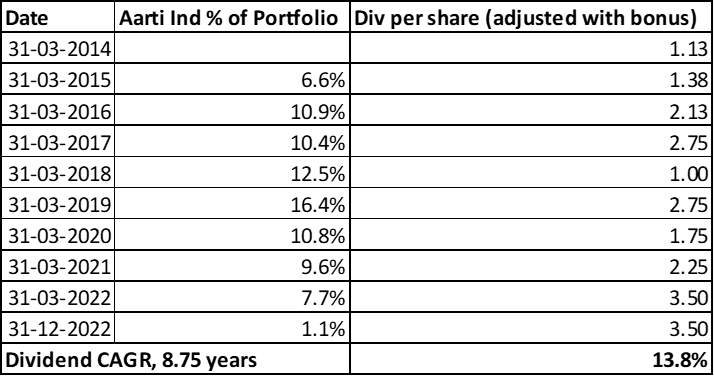

Find enclosed my Aarti Industries holding in my portfolio (I have not considered Surfactant and Pharma lab in my calculation).

Despite large capex, the company constantly increased dividend at CAGR of 13.8% (adjusted for bonus), plus two tender buyback and two bonus issue. This growth in dividend was main factor which assisted me hold the companies over long period. Aarti Ind and Eicher were two investment which I made during August 2014 and September 2014. By December 2014, Eicher was 18% Weight in Portfolio while Aarti Ind was 8%. Despite great performance from Eicher and my higher conviction, my XIRR (including dividend) from Eicher as on 31 March 2022 was 17% (over 7.5 years) while for Aarti Industries was 47% (over same period). Though Eicher I started selling within year of holding, Aarti I continue to hold. By September 2018, Aarti Ind even exceeded Eicher (partly due to selling of Eicher shares and partly due to superior performance of Aarti Industries, reflected in market price). From Sep 2018 to Dec 2019, Aarti reached as top holding for me with more than 16-18% of my portfolio.

I did not have any view when I invested in Aarti Industries that it would be the highest absolute wealth creator for me in next 8 years. This again reinforce the point, at least for me, I do not understand how business and valuation would change over period. Also, in my view, I was lucky to hold for long period and skillful to read annual reports and con call to develop my conviction in the company.

Since I had been regular contributor to the thread, I thought to update the forum members (apology for being late by 6 months only  )

)

Thanks VP members for being major force to assist me to develop my conviction in the company and management for such wonderful execution. I wish we all are lucky/skillful to have many such Aarti’s being identified early and held for longer period when the company is performing.

Discl: I am not SEBI Registered advisor. I am not suggesting any investment action. Reader shall do her/his own due dilgience. My view may be biased.