1 Like

15-Jun-2020 AARTIIND Aarti Industries Ltd. SMALLCAP WORLD FUND INC SELL 15,97,950 854.71

15/06/2020 524208 AARTIIND SMALLCAP WORLD FUND INC S 1,000,000 855.00

total almost 26L shares sold today in NSE and BSE

NSE data - approx 51L shares traded with 74% delivery.

Mgmt commentary of no impact on next two year performance/guidance/margins

Asset stays with Aarti and can monetize it in addition to settlement amount.

Invested and added today

1 Like

Capex of 400Crs and receiving 800Crs without operation cost in 2 years? Isn’t it great deal?

2 Likes

I have the same question. It has been a while since the demerger was announced.

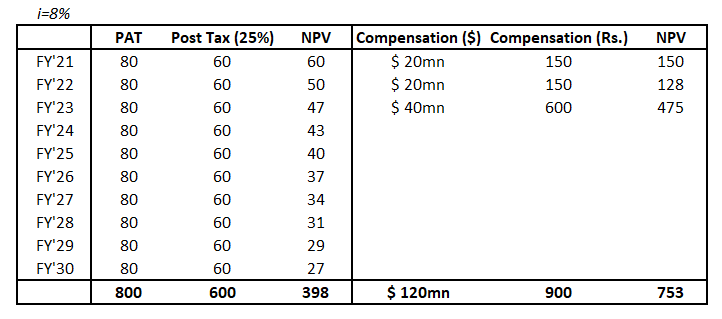

The impact of cash flow on account of termination of contract: Since Aarti Industries was to get 80crs/annum as PAT (20% margin) and due to termination it likely to receive a compensation cash flow of $20mn each in FY21 and FY22, and $80mn in FY23, below is the calculation of NPV of the same:

You are not accounting for the fact that the asset is already built and the company can use it and sell to other clients and also make other products. So, the outcome for Aarti is actually not bad as I had mentioned initially.

10 Likes

Incremental update on 20th June ( 20May and results concall being earlier)

Tone seems much more cautious and border case pessimist compared to concall which seemed much better - could be just my way of looking at it. No mention of Above key project cancellation ( was covered in call adequately).

- Non essential biz(40% topline) to see contraction

- Supply chain issues - transport/labor/port and so on

- Project commencement delays likely- deferment of some sort on milestones

Add to it incessant selling by part of promoter groups. Raising funds for charity on almost every few days basis?? Wouldn’t it be more constructive to find a strategic/fin investor rather than this part by part approach.

2 Likes

Continuous selling continues from the promoter group … Size is not that big but kind of unsettling that why will people keep selling a good business.

2 Likes

Demerger - Aarti Inustries - Aarti Surfactants

We can see aarti surfactants being listed

3 Likes

| S.No. | Name | CMP Rs. | P/E | Mar Cap Rs.Cr. | ROE 10Yr % | ROE 7Yr % | ROE 5Yr % | ROE 3Yr % | ROCE3yr avg % | Debt / Eq | M.Cap / Sales | Free Cash Flow 10Yrs Rs.Cr. | Free Cash Flow 7Yrs Rs.Cr. | Free Cash Flow 5Yrs Rs.Cr. | Free Cash Flow 3Yrs Rs.Cr. | Free Cash Flow Rs.Cr. |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Pidilite Inds. | 1463 | 84.2 | 74339.71 | 27.08 | 26.95 | 27.55 | 26.22 | 35.58 | 0.06 | 12.08 | 4469.36 | 3711.02 | 3363.63 | 1950.68 | 835.62 |

| 2 | Aarti Industries | 1015 | 36.24 | 17684.8 | 21.84 | 22.34 | 22.73 | 21.7 | 16.93 | 0.7 | 4.1 | -237.19 | -221.51 | -293.47 | -357.4 | -23.44 |

From last 10 years…not even single year free cash flow generated?..is it not a red flag?..Please advise.

1 Like

ICICI Direct has initiated coverage on Aarti Industries

I agree with your view, but FCF turned negative after year ended Mar 16. But CFO has increased significantly and once the capex intensity reduced for Aarti Industries,it will surely make lots of free cash.main question is Can we trust the management for execution and its business model.

Nice to see your views. Negative FCF is a component of red flag study, not necessarily a red flag. Companies in ‘heavy investment’ mode can have negative fcf for an elongated period due to continuous CAPEX. Separately, it is important to track other metrics i.e. CFO/Sales, capex capitalisation trend, CFO/EBITDA, leverage, matching of cumulative CFO to PAT etc.

Although, financial shenanigans can still exist despite everything looking rosy on books.

Good luck.

1 Like

Nirmal Bang has initiated coverage on Aarti Industries.

1 Like

Conference call takeaways

The Specialty Chemicals segment reported sales of Rs 11.09bn (32%/24 qoq/yoy). The

growth was on the back of higher volumes and better capacity utilization. However EBIT

margin remained lower at 17.1% (-680bps/+170bps yoy/qoq) on account of one time

effort to push higher volumes in the discretionary spend basket at lower margins in nonregulated markets.

Update on Multiyear supply contacts: (1) With the US court verdict to ban the Dicamba

herbicide in Q1, ARTO and its partner have mutually agreed to cancel their 10 year

supply deal with an adequate compensation for ARTO. However, the US Environmental

protection Agency has recently given a five year extension for use of Dicamba

formulations. Hence, ARTO expects incremental business from its earlier build

intermediate plant developed dedicatedly for Dicamba intermediate. Guides the 2nd

phase plant commissioning in Q4 and expects to supply the intermediate in India &

China region. (2) The 2nd multiyear contract is delayed due to equipment supply issue

and Covid led lower demand. Guides to commission the plant in Q1FY22 (vs H2FY21)

and expects 50% utilization in the first year. (3) 3rd contract should start in H2FY22.

The Pharma segment continued its healthy growth momentum with sales at Rs 2.21bn

(15%/21.7% qoq/yoy) and 700bps/+200bps yoy/qoq jump in EBIT margin to 25.5%. This

was driven by increasing contribution from regulated markets and value-added

products. However, ARTO guides for a healthy segment sales growth of 15-20%p.a. for

next few years. The growth will be supported by strong visible demand and continued

Capex of Rs 1.50bn in FY21 and Rs 1bn p.a. thereafter.

ARTO guides for incremental revenue of Rs 20bn for specialty chemicals over next 2-3

years as it’s continues with its aggressive Capex plans of Rs 10-12bn annually.

FY21 Guidance: Flat FY21 earnings (due to Covid led global uncertainties) but confident

about 15-20% earnings CAGR over 3-4 year on the base of FY20

7 Likes

Good interview on the prospects going forward in FY22 and FY 23

Disclosure: Invested and this is not a recommendation to buy or sell. I am not a SEBI registered advisor.

2 Likes

Interesting development on the contract that was canceled, possibly the sales might still ramp up post the commissioning of Dicamba Intermediate plant

1 Like