Find enclosed key points dicussed on Aarti Industries on Q3FY18 earning call held on Feb 5 2018.

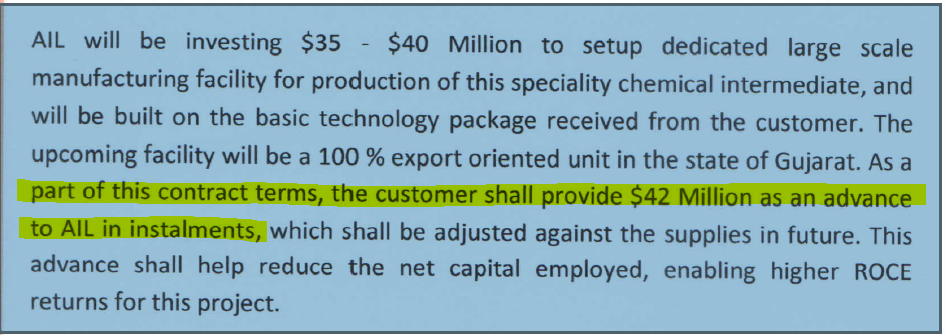

1) SABIC contract: The company would be receiving USD 42 million as Advance for future material supply. So funding would be minimal at the company end. In addition, SABIC would be supplying intermediate and technology support. The product is current manufactured by SABIC and they found Aarti being suitable partner for future requirement. For Aarti, since this is a very large size order with stable growth over couple decade and also establishes it as a strong partner in global market. Hence, while margin on the project would be lower, IRR would be significantly higher (due to no investment except for working capital). The company has yet to get environment approval for this project. They already have part of land. They expect environment approvals (for both outsourcing projects) to come in couple of months. From receipt of enviroment approval, it would take around 15-18 months to complete installation and commence the operations. The resultant capacity is specific for one product and alternative use would be limited. The company generally does IRR of 15-20% on the project, however, due to Capex support from Partner, IRR on this project would be significantly higher.

2) Rs 4000 Cr Contract over 10 years: This contract is higher margin contract as technology for same being provided by Aarti industries is a benzene based product from Aarti specialty products. The client of Aarti is a large MNC with topline higher than USD 10 billion. After contract term, Aarti would be able to utilise same plant to manufacture other products. The management expect to reach full capacity and sales value within 2-3 years of commencement of plant.

3) Market risk

a) Exchange rate risk: In multi year contract, either client or Aarti hedge for the exchange rate. In case it is Aarti responsibility, Aarti entered into forward contract to mitigate exchange risk.

b) Crude price: In almost all product, Crude price relate hike in input cost are passed on to customer within 1-3 months. Given the volatile input and end product prices, the company focus on absolute margin rather then % margin. Generally, when crude price were lower, margin are constant in USD term and hence as % of revenue is higher and vice versa.

4) Volume growth expectation:

In Second half FY18, the company guided 10% volume growth vis same period in FY17. In Q3FY18, it achieved volume growth of 8% and expect to achieve around 12% growth in Q4FY18. In FY19 Volume growth are expected to be better then FY18. Further, going forward, with two contract in hand, the company expects around 10-15 over next few years.

The company has achieved Nitro Toluene plant utilisation at 25% which is expected to reach around 50-70% level during FY19. At current utilisation level, the company is not breaking even while during FY19, with around 60% utilisation, it would achieve breakeven.

In Pharmaceutical business, the company could ramp up production due to some new product launches. It also intend to expand some drug intermediates which is expected to drive sales growth in FY19.

In Home and Personal care business, the company has installed powder processing units. The margin in powder processing products are better than liquid products. While one machine of powdering is already operational, the other two are under implementation. On commencement of these units, the company is confident to report higher margin then what were reported in past. The company has two set of client. One is large reputed MNCs who source material regularly from the company. The change on oleochemical is passing through for such customers. For other customers, the prices are open. Further, nearly 25% of open businesses is exported.

5) Seperaration home and personal chemical

In the coming AGM, the company may consider to hive off Home and personal chemical business from Speciality/Pharmaceutical business.

6) Capex: During FY19, the capex may be higher than Rs 500-600 Cr normal capex depending on implementation of new contact plants. The company is increasing Hydrogenation capacity which is expected to commence in FY19. Beside this, there would normal debottlenecking and expansion at existing product lines.

Discl: Aarti Industries is among my Top 5 holding. I have sold small quantity of my holding during last 15 days to align my portfolio allocation in equity. My view may be biased due to my holding. Investor are advised to do their own due diligence before taking any action. While I attempt to cover all points, there may scope of transmission loss/miscommunication and reader shall take note of this factor while reading this post.