Some key highlights of FY17 (from investor presentation):

Board of Directors in its Meeting held today i.e 19th May, 2017 gave its in-principle nod for demerger of its Home & Personal Care business

Co has declared a dividend of Rs 1 per share

Commercialized calcium chloride facility at Jhagadia (Gujarat) in Q1FY17

In Q2FY17 commenced commercial production at multipurpose Ethylation unit at Dahej SEZ, Gujarat. The Greenfield Ethylation unit is first of its kind to be set up in India and has adopted Swiss Technology with a capacity to manufacture about 8,000-10,000 tpa of Ethylene derivatives

In Q2FY17, commenced commercial production of its 2nd Phase at PDA facility in Jhagadia, from 450 tpm to 1,000 tpm

In Q4FY17, operationalized captive co-generation power plant at Jhagadia, Kutch and Vapi.

Co now has a total of five power plants – two at Vapi and one each at Jhagadia, Kutch and Tarapur; which would help reduce power costs significantly

Operationalized Solar plants with aggregate capacity of 697 KW across five locations

In Pharma, co successfully closed USFDA facility inspection at Tarapur initiated in Q3

Aarti Ind has signed a 4,000 cr 10 year contract for a global agrochemical intermediary. Co is to invest 400 cr and the sales are expected to start from 2020.

Expected sales are evenly spread out with operating margin of 40% vis current margin of around 20-22% as per the interview. The company is likel to incur capex of Rs 400 cr over next 3 years with debt equity mix of 1:1. Equity would be mostly funded from internal accruals. Overall good development in the company.

Discl: Among my Top 3 holding and my views may be biased due to my interest in the company

Please refer the video link in the moneycontrol link. Management indicated 40% EBITDA margin.

Dhiraj the catch here is lower asset turns. This entails 400 Cr capex for yearly 400 Cr revenue or 1x asset turns. So even at 40% EBITDA it will correspond to 20% ROCE, since Aarti’s base asset turns are 2x+.

The deal is of huge significance in terms of capabilities and more such similar opportunities in the future.

I completely agree with you. Hence, my last comment that overall it is good development for the company. If company can enter into further couple of such relationship, that may take it to next orbit.

Also, a 400 cr capex assumed as capital employed with 40% EBITA would give 160 cr. Even assuming depreciation of Rs 40 cr (10% to capex), PBIT would be 120 cr. So ROCE on incremental capex would be 120/400 cr being 30% as my calculation. Let me know your view on same.

Annual report highlight of Aarti Industries Ltd FY17

Excellent letter by Mr.Rajendra Ghoghri. Must read for some one interested to understand chemical industry. Key point

Excellent client relationship and diversified product portfolio

“We generated more than 85 per cent of our 2016-17 revenues from customers with whom we had worked for five years or longer; virtually every single customer reported a larger quantum of purchase; and yet, our largest customer accounted for no more than 9 per cent of our 2016-17 revenues, indicating business broadbasing and corresponding de-risking.”

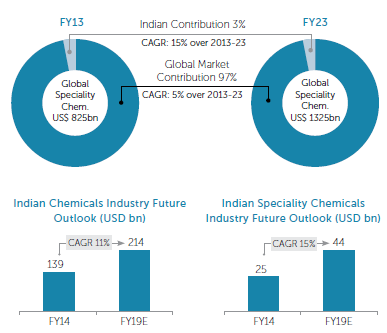

Global trends in chemical trade

a) Increased dominance of China in Global trade with price being lower than conversion cost from other players in past

b) Increased ageing in skilled manpower in Ageing country and also higher cost of manufacturing in developed countries leading to higher outsourcing

c) Black swan in global environment leading to higher focus of industrial companies top management on fre fighting then to manage the business

d) Increase in demand from developing market with changing lifestyle and increased per capita income in addition to more global market open leading to higher export demand

In view of above global chemical players have moderated their spending on production to stategic products and focus more on marketing and product development. They have also rationalise no of vendors from many to few with large volume.

“a larger number of global industrial players are graduating from vendor enlistments to strategic

partnerships;; the conventional cost arbitrage model is being replaced by knowledge arbitrage; short-term opportunism is being replaced by long-term stability and sustainability.”

Chaging in Aarti status from Vendor to Parter, "While vedor is outside customer personality, partner is extension of customer personality

Most vendors offered customers a value that was derived out of a cost arbitrage; at Aarti, we graduated to a knowledge arbitrage that resulted in our offering enhanced product value to the customer’s table"

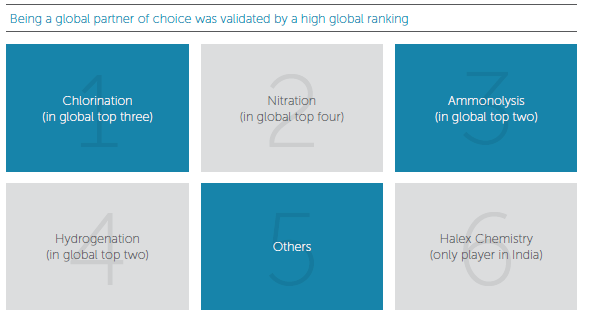

The company invested Rs 250 Cr in SH&E (Safety, Health and Environment) during last 5-6 years. Aarti has been REACH compliant since 2011. The substantial impact of REACH will come in play following implementation of Phase 3 from June 2018 that would regulate any chemical supplied to EU at quantities of 1 tonne or moew per annum. Aarti is the largest producer of benezene derivatives in India and one of the leading global manufacturer enjoying 25-40% of global market share across various products. Aarti derive nearly 82% sales from benezene derived speciality chemicals.

The company has acquired 358,000 sq , mt. (~85 Acre) land for future expansion with cost of Rs 60 Cr.

@dd1474@basumallick I have a very elementary question was hoping you could help me understand better. Aarti industries cFCF for last 10 years is 150 cr but still they have taken on almost 1100 cr debt in this time. Cash balance is only 83cr. Even if I take dividends into account that’s only 293 cr in the last 10 years. can you please help me understand why they would need this kind of financing and where I can see this money being put to use? I have used screener data for standalone business.

Can you please provide working for your calculation of free cashflow from operation? Generally, the company continue to increase capacity for future volume growth as well as new product launches. That require capex which is funded from mix of debt and equity. Over period, the company has judicious and prudent to use debt and equity by managing gearing. Over last 10 years, gearing of company has been in range of 1-1.4 times. Over last decade, the company has managed ROE of more than 20% as per screener data with sales cagr of around 14% p.a.and net profit cagr of 24% p.a. In last decade. It is definitely not a company which has huge free cashflow generated from operations like FMCG and limited capex required. However, the company has edge in research and quality control due to which able to generate special niche for itself in global market. I believe probably only Atul limited would have superior product range in Indian market when compared to aarti Indudstries. All other chemical company have generally 1-4 products while Aarti has multiple products. Please read annual report of fy16 and FY17 in case you are interested in the company. I shall revert on free cashflow question once I get detail breakup of elements which are included in your free cashflow calculation.

@dd1474

Thank you very much for your reply. I am invested in the company since 2015 and am aware of all the points you have mentioned. In fact that is why I invested. However, recently while looking at the numbers again after reading this year’s annual report, I noticed this and could not understand, hence thought will ask on ValuepIckr in order to learn.

I have used screener standalone data 2009-2017, as per which,

cCFO = 2312 Cr

cCapex = 2160 Cr (Net Block +WIP change during the year + Dep)

therefore, cFCF = 152 Cr.

But still Debt has gone up from 483 Cr in 2009 to 1545 Cr during this time. I would have thought that if a company has +ve FCF after Capex, then it would not depend on debt to grow. But in this case I am surprised that isn’t the case. However, I do notice that their Interest coverage ratio is pretty ok (5+) so your point about them maintaining their capital structure within a range is very valid.

They have paid dividend of 282 Cr during this time and interest of 852 Cr. So does this mean that the debt inc was to basically fund the dividend payout and pay interest? If yes, as the numbers seem to be suggesting, is it a good sign?

So based on your calculation, the increase in debt is kind of matching with interest and dividend payment. So one way would be to repay debt rather then dividend to shareholder. Howerver dividend paid is not large amount ~ 200 crore over ten years to make material difference to the company gearing.

While your analysis suggest that there are not large free cashflow, which I agree, what I like is growth in topline and bottom line with consistent 20% ROE. The business has become world class and it is growth phase and may continue to remain so for decade or so. For a manufacturing company, it would be difficult to get free cashflow in substantial volume. It might make sense for us to do similar work on Vinati organic, Atul limited, Sudarshan chemical and other peers to understand better. I do not have right or wrong answer to your question.

What I would try to find another business model strong enough as aarti and having similar or favourable valuation and growth prospect and switch over whenever I come across. Till then would continue to remain invested. I would closely look at gearing and credit profile and that management of aarti has managed reasonably well. I do not expect aarti to get gearing of 0.5 in short term as that would mean it may have to slow down on Capex. Similarly would also not like gearing up by 1.5 times as that would easily take company in debt trap.

Thanks for bringing out valid point and let us get more insight after looking at other chemical company as well.

Discl: among top 3 holding and investor are requested to do their own due diligence before investing.

I looked at Sudarshan, Vinati and Atul. Sudarshan is similar to Aarti in that it has not been able to generate enough FCF over the past 9 yrs to be able to fund all of its Capex. So it has also had to take on debt to fund its growth. Vinati and Atul on the other hand have generated enough FCF so that they have grown without having to depend on debt. Vinati has used the FCF to pare its debt and is almost debt free. Atul’s net debt is also less than zero and is sitting on a large cash on its BS.

The inference I can draw from all this is that all of these 4 companies have/will probably grow but when the environment becomes tough, the stress will show up faster in the case of Aarti and Sudarshan. Atul and Vinati have the greatest margin of safety and will probably withstand this stress for longer.

Partially agree and partially disageee. If aarti is developing product capability and research lab (as it suggested in last con call), it would hit operating margin for some time and hence free cashflow would be lower. The most important thing is future free cashflow then past. If there is no change in business from last decade to to next 10 years then I would fully agree. Howerver during last decade first 5-6 years, china had literally taken chemical companies to ride which is no more seem to be case. Second change is US/EU companies want to balance china dependence with another creditable partner. This is positive tailwind along with negative tailwind of strict environment norm. I am not saying that Vinati and Atul are not good. What i am saying that future can not be replica of past. I may be completely wrong after 5 years. But definitely do not see last decade being same as next 5 years.

Thanks Dhiraj, I see your point and that is my investment thesis for Aarti Industries as well. As you rightly mentioned in your earlier post, the key monitor able will be the leverage in the BS. As long as the coverage ratios are within range, I guess it will be an interesting journey for the next few years.

Specialty chemical firm Aarti Industries’ board will meet later this week to consider a proposal for buyback of its shares, the company said today. “A meeting of board of directors is scheduled to be held on December 21 to consider a proposal pertaining to buyback of the fully-paid shares of the company,” Aarti Industries said in a BSE filing. It, however, did not elaborate on the size of the buyback.

I seek views from fellow members on this action and the picture going ahead in next 2 years.

Disclosure: Invested in both personal and family portfolio.

I feel there is nothing much on table to play this buyback, Its just 1% of total outstanding shares.

If you see shareholding pattern there are around 1 Cr shares held by retail < Rs 2 lac category.

Individual share capital upto Rs. 2 Lacs = 10775125.

Buyback size is around 8 lac shares of which 15% will go to retail < 2 lac category, I don’t see very big conversion ratio.

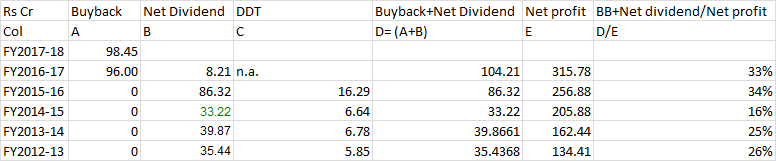

I believe the current buyback announcement by Aarti Industries is more to be consider as part of Dividend rather as buyback in traditional understanding. During December 2016 also, the company did buyback at price of 800 when ruling price was around ~700. This buyback was also kind of dividend payment, which more tax efficient.

Since 2016, post dividend > 10 lakh per annum covered for Tax, many companies are declaring dividend as buyback. Any buyback, which is less than 5% of outstanding equity and promoter participating, in my understandng is dividend payment (which otherwise reduce cash by 15-20% for dividend distribution tax from company gross cashflow and also taxable at more than 10 Lakhs in hand of receipient). Same if declared as share buyback, it would be considered as tax efficient as it would subject to long term capital gain tax (since tender through exchange involve Security transaction tax, it amount to nil capital gain for holding more than 12 months as in case of other equity share sale on exchange).