Research bytes./ Even some company uploads on their website.

Not able to use research byte.com every time it gives error while verification of contact no…For weeks now the problem remains the same and not able to use it…

Aarti Industries…Last few years Data shows its Debt is increasing continuously and D/E ratio is always above 1 and currently 1.32. Is High Debt a concren here ? Any valid justification to remain so high Debt from past few years ? Not so good at Financials just a observation from my side.

The demerger announced has been executed. Came across this article on the details of the demerger.

Also @ramanhp shared some details on this before.

Article. - Aarti Industries: The Right Chemistry for a Bright Tomorrow

@basumallick your views on this ?

They are in the midst of major capacity expansions. However, they have been always a slightly debt heavy company, which is something to be careful of.

Aarti Industries Ltd

Key Highlights Of Q3FY19 and Nine Month FY19 Results

Financials

-

Q3FY19

- Revenue grew by 28 % to Rs 1268 Cr compare to last year same period

- EBTIFA grew by 39 % compare to last year same period

- EBIT grew by 44 % to Rs 206 Cr compare to last year same period

- PAT grew by 47 % to Rs 133 Cr compare to last year same period

-

Nine Month FY19

- Revenue grew by 36 % to Rs 3646 Cr compare to last year same period

- EBIT grew by 48 % to Rs 560 Cr compare to last year same period

- PAT grew by 49 % to Rs 345 Cr compare to last year same period

Key Highlights

- Company have entered into forward contracts to hedge the currency movement. Further provided on revaluation gain to the extend of Rs 6.12 Cr as on Dec 31st 2018

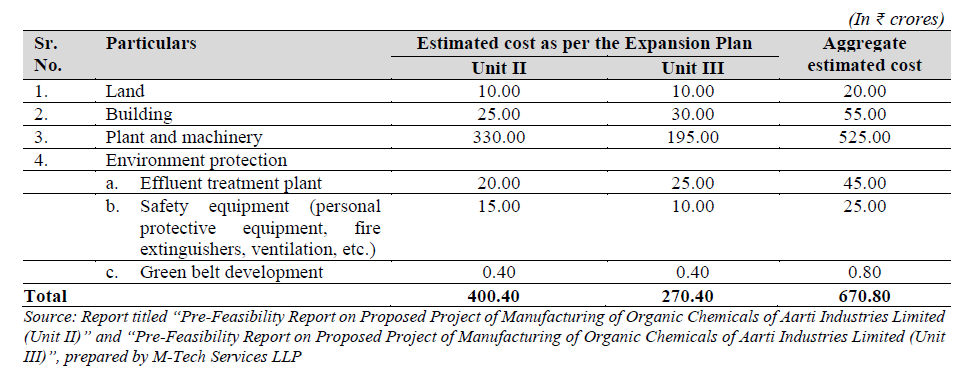

- Invested about 528 Cr in CAPEX in Nine month FY19 and current on way projects include specialty chemicals and plant at Jagadiya and Gujarat , acid reconciliation plant , CAPEX for long term expansion in Dahej and pharma intermediate , Debottle necking and expansion in pharma and specialty chemicals.

- Quarterly growth was spread across three segments :- Specialty chemicals , Pharmaceutical and Home & Personnel Care that grew by 37 % , 21 % and 8 % respectively.

Segmental Highlights

-

pecialty chemical business

- Represent 80 % overall revenue there was continuous margin expansion with higher utilization capacity including product mix also allowed company to expand margins on the back drop of increasing raw material cost which are typical build into a part of mechanism in selling price.

- Volume in specialty chemical grew by 4 % in Q3 FY19. Crossed 17700 Mt of Banzyne during Q3 FY19 as against 18,350 MT in Q3FY18.

- BOD approve an investment to the extent of Rs 150 Cr for expanding the NCB capacity from 75,000 Mt per annum to 108,000 Mt per annum. This expanded capacity would be coming into two phase :- Phase-1 in FY20 and Phase-2 in FY21.

- Achieved 80 % utilisation in Specialised unit at Dahej SEZ. For nitrogen the plant at Jagadiya which become operational last year at 33 % utilisation.

-

Pharmaceutical Segment

- Continue to sustain momentum in business , Revenue grew by 23 % YOY in Q3 FY19 to Rs 171 Cr and 34 % YOY 9M FY19 to Rs 513 Cr

- EBIT expanded 79 % YOY in Q3 FY19 to Rs 30 Cr and 22 % YOY to Rs 85 Cr

- Improved profitability based on higher capacity utilization and focus based on product basket such as zenthin derivatives and pharma intermediate in regulated markets.

-

Home and Personal Care Segment

- Margin were impacted due to improve in improve cost and change in product mix

- Demerger of this segment is on track.

Outlook

- On Multi-year deal company is going to commissioning plant in second half of FY20.

- Nitro Chloric project will be commission in two phases :- One in FY20 and another in FY21 because it is a brownfield De-bottlenecking.

- Acid plant will shut down in Q4FY19.

- Out of two long term contracts one is going to commissioning in FY20 and another in FY21 and substantial portion of revenue can be seen from FY21 from first.

- Company has recently announce another block construction for Intermediates. It will take at least one year to get commercialised.

- Over long term company expect debt to equity from 0.8 to 1.2 and in this year.

4 Likes

Debt to equity is already at 1.35…am i missing something here…they want to reduce the debt or increase it to fund expansion ?

Their debt pattern seems to be on increasing trend in last few years.

1 Like

Aarti Industries signs $ 125 million multi-year deal.

1 Like

A good initiation report on Aarti Inds from Axisdirect. Covers the business well.

Aarti Industries Ltd - Initiating coverage - Axis Direct.pdf (2.3 MB)

6 Likes

The above report on Seya Industries which is also into Benzene chemistry, seems to state that there are signs of Chinese supply coming back online after supply disruption due to environmental issues. Did management give any updates in the Aarti Industries Q3FY19 con call? They have previously always maintained that this is a significant tailwind they are enjoying.

The management in past had mentioned that the shift from China to India producer is more structural for International customer as they wish to diversify their sourcing. So while some China capacity will come back, they are mostly large companies but will be tough for unorganised producers to comply with tough environment norms.

Interesting names meeting Aarti Industries.

Sr.

No.

Name of the Institutional Investor

- Malabar Investments

- Temasek Holdings Advisors India Private Limited

- SBI Life Insurance Co. Ltd.

- Abakkus Asset Manager LLP

- Max Life Insurance Co. Ltd.

- Steadview

ArtiInvestors.pdf (861.1 KB)

2 Likes

Vanguard acquired 4.16 lakh shares of Aarti Industries at an average price of Rs 1425.32.

Overall deal value of 59.35 Crores.

1 Like

Mostly all in midcap space…That’s imp.