this TTM EPS has a one one off income of December Quarter - expect dec eps to be around 3.5 this time - so after dec results - TTM eps will be 16 - reduce 16% = 13.5 - so PE will be 525/13.5 = 39

3 Likes

Where-ever it pleases us, we will show figures exclusive of Termination Income & Shortfall Fee to drive appropriate comparison and at other places, we will conveniently avoid ![]()

Investor presentation:

7 Likes

1 Like

has anything changed fundamentally for chemical sector? why growth is stagnating? why margins are under pressure? will this change in future?

any good article analyzing this sector? please share.

2 Likes

As the result seasons are nearing, attaching the complete 3 quarter concalls to brush up the management commentary and accordingly take position for forthcoming fiscals.

Results are out!

Again they are conveniently taking the lower numbers i.e. without termination and shortfall (for YoY Revenue and EBIDTA) to show better growth compared to FY22 ! Request someone who has been following this closely to comment on the results.

Highlights from MD V Gogri’s commentary:

Positives:

- For the current fiscal 2023-24, the firm is looking at volume growth of around 25 percent. Part of that volume will come from our non-regular market because regular market demand is under pressure.

- Discretionary side demand seems to be recovering from at least the first quarter of FY24.

Negatives

- EBITDA growth will be lower (than revenue rate), we will be targeting around 20 percent growth in EBITDA for FY24

- Some global demand is still under pressure on the discretionary side because of higher interest rate.

General commentary:

- Company is targeting revenue growth of about 30 to 45 percent over two years (at constant raw material cost).

- Some inventory correction is also taking place. So the feedback we are getting is that quarter-on-quarter, demand should increase on the discretionary side in FY24

- Exports will be continuing - around 50 percent of the sales will come from export

5 Likes

Aarti Industries Q4 results highlights -

Company infra -

16 manufacturing plants

11 ZLD plants

05 Co-Gen power plants

02 R&D centers

6000 employees

Sales breakup(FY 23) -

India- 52 pc

ROW- 15 pc

N America- 13 pc

Europe- 11 pc

China- 6 pc

Japan- 3 pc

Total Sales @ 6620 cr

5 yr sales CAGR @ 22 pc

5 yr EBITDA CAGR @ 15 pc

Key strengths -

Global leader in Benzene derivatives. Among top 3 in chlorination and nitration. Among top 2 in hydrogenation

Fully backward integrated, low cost, sustainable mfg ops

100+ products

1100+ customers

End user industries -

Agrochems-30 pc

Pharma-20 pc

Pigments-12 pc

Additives-26 pc

Polymers-10 pc

HPC- 3 pc

Products in pipeline - 40 plus, half of these to be made in India for the first time

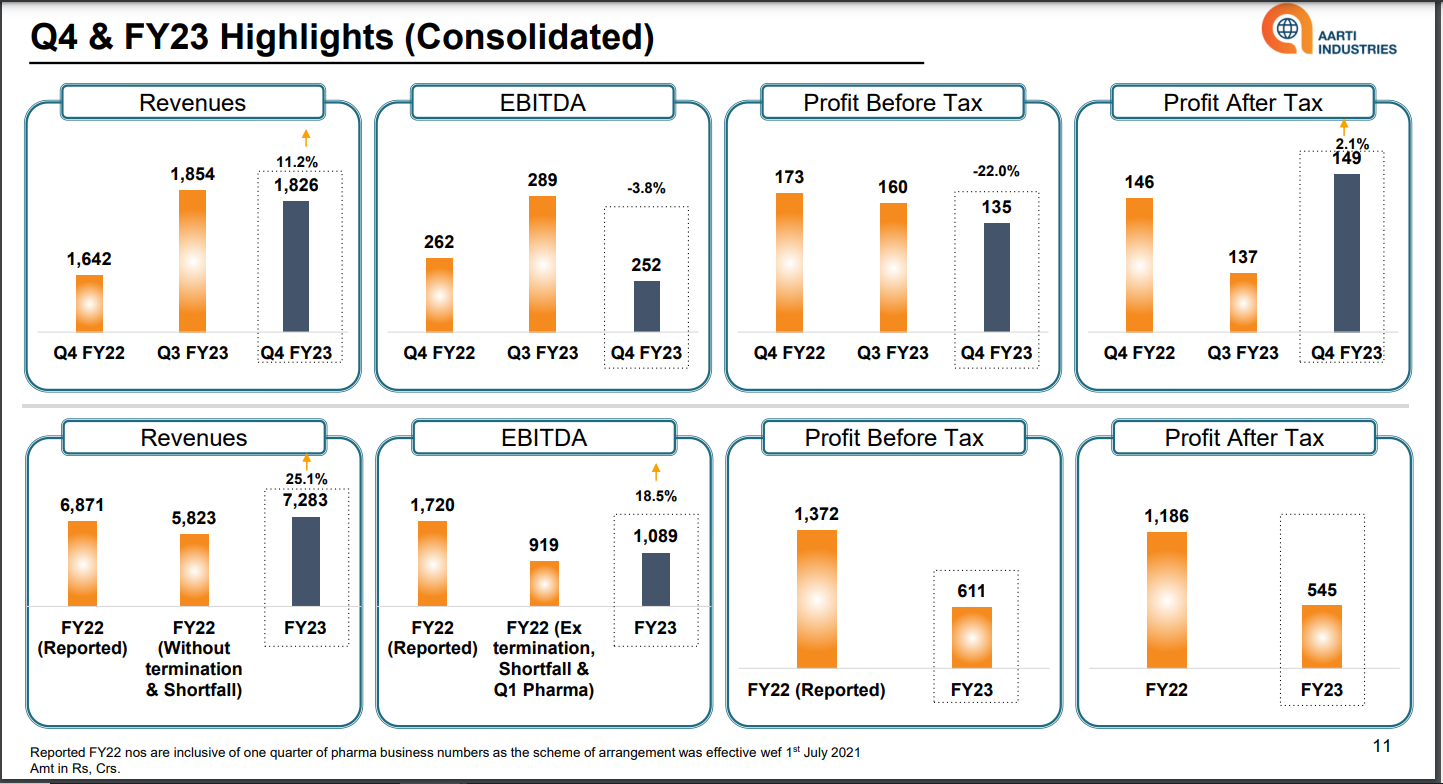

Q4 highlights-

Sales- 1854 vs 1642 cr

EBITDA- 252 vs 262 cr

PAT- 149 vs 146 cr ( due one time tax write back )

Contribution from value added products- 85 pc

Debt/Equity - 0.58

Comments on Q4 performance -

Increased volume from higher volumes and higher sales of value added products

EBITDA impacted due-

Maint shut down of one Acid plant and Kutch Unit

Slowdown in off take of dyes, pigments (textile related).Green shoots visible wef Q1

Except energy, other RMs were higher QoQ

Updates-

Commercialised 02 spec chemical blocks(for agro and pigment intermediates-for captive use)

02 more blocks to be commissioned in next 02 yrs

3rd long term contract commissioned last yr to be ramped up this yr

Macro concerns wrt demand continuing. Likely to improve in FY24

Targeting 20 pc EBITDA growth for FY 24 ie around 1320 cr vs 1090 cr for FY 23

FY 25 guidance - EBITDA of 1700 cr @ 25 pc margins due ramp up of new facilities and increased op-leverage

FY 26 and beyond - EBITDA to grow at 25 pc CAGR due zone 4 ramp up and better utilisation of zone 1,2 and 3

Other important comments-

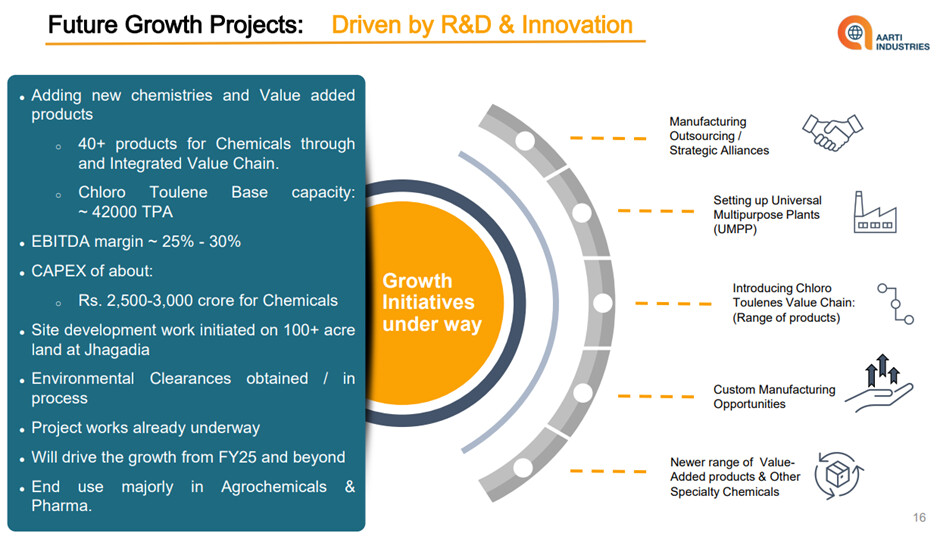

Capex spends for FY 23 at 1300 cr

Entered into a 20 yr supply arrangement of Nitric Acid with Deepak Fertilisers to secure the key RM

Capex guidance for next 2 yrs at 1500 cr each for expansion into chloro-toulenes, which is a difficult to make product. Will target both exports and import substitution

Expect 25 pc volume growth in FY 24. EBITDA growth to be slower ( @ 15 pc or so ) as exports to non regulated Mkts increase

Global slowdown impacting demand of discretionary products

Expect employee costs to moderate going fwd in percentage terms as topline grows in FY24

Margin difference between regulated vs non regulated Mkts are as high as 10-15 pc at GM level

Supplying to both patented and non patented agrochemical makers

Long term, Europe likely to lose mkt share wrt energy intensive products as overhang of high energy prices continues

Not losing mkt share to China post China opening up

Nitro Chloro Benzene volumes to pick up in Q2

Tax rates to be around 15-17 pc next FY

Expect some debt increase in next 2 yrs as operating cash flow may not be able to absorb all capex spends

Volume growth for FY 23 has been 15 pc plus

Capacity expansions in FY 24,25 will be in NCB, Acid plant (up 22 pc), Ethylation (up 3X), Nitro Toulene

Post ramp up of capacities in FY 25, expect an asset turn of about 1.5 times

Working capital reduced post demerger of Pharmalabs

Disc: intend to add slowly on dips. Holding a small tracking position

15 Likes

aggressive capex is the best use of cash generated, demand will pick up, margins will improve, Aarti Ind will be ready with capacity

2 Likes

The PAT/CFO conversion for Aarti Industries. (FY19-23) as per screener data, comes to around 130%. What would be the reason for this? Also post the demergers will this sustain going forward?

Extremely high depreciation due to capex and finance cost.

While calculating Cfo:- both Depreciation and finance cost get added back.

If there is a good amount of difference between cfo and pat (120-130%+). It also points to operating leverage being present in the business…

Given chem cos are going through a hard time- only in better times the gross block can be utilised.

Disclaimer:- no holdings. Tracking like a hawk.

29 Likes

So margins mean reversion + destocking in future could be the triggers for growth.

1 Like

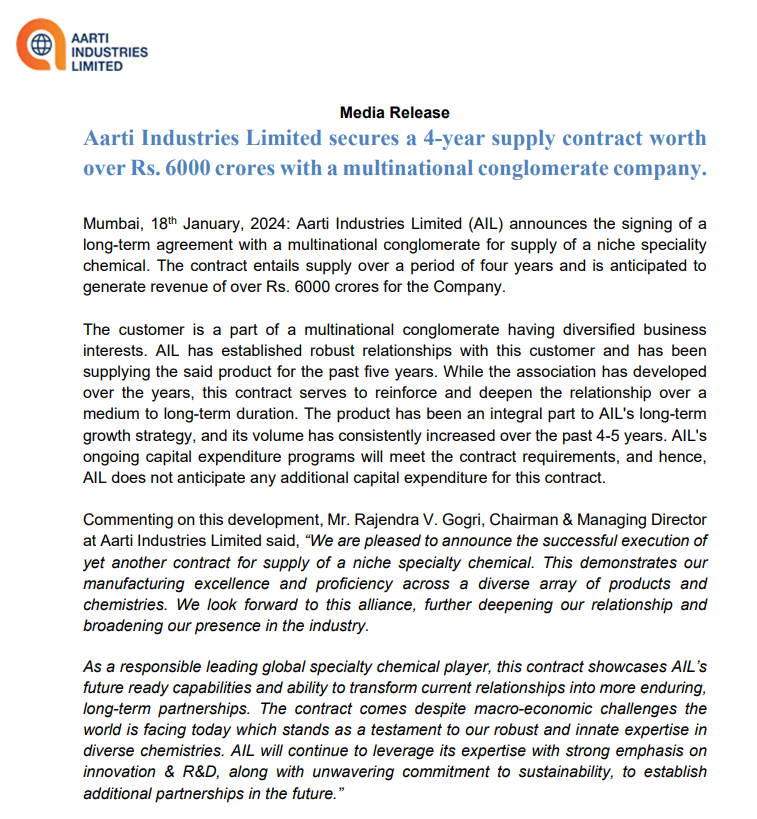

Aarti Industries Limited (AIL), today announced that it has entered into a 9-year long-term supply contract for the supply of a niche agrochemical intermediate with a global agrochemical products and solutions company. The contract offers AIL a revenue potential of approximately over Rs 3,000 crores over a period of 9 years, with the contract supplies commencing from current fiscal year. This product (agrochemical intermediate) is an integral component of AIL’s existing integrated product portfolio, with AIL being a leading manufacturer of this product in India. AIL’s current CAPEX plans, across its existing manufacturing locations, are sufficient to meet this contract requirement and the company does not anticipate any additional CAPEX for this.

7 Likes

EXCLUSIVE Sources to

Bayer Group likely to have tied up with Aarti Industries Contract was cancelled earlier with another global agro-chemical player Aarti Ind : Due to confidentiality reasons, we cannot comment or share any details of the entity.

2 Likes

Aarti Industries Whats Happening ?

Company Corrected 50% Peak in last 2 years and now started forming Base

Largest producer of Nitro-Chlorobenzene, Benzene and Lowest cost producer of benzene in the world and have diverse portfolio of basic chemicals, agrochemicals, speciality chemicals and intermediates, which are extensively used in the manufacture of pharmaceuticals, agri-products, polymers, additives, pigments and dyes

Multiple Long-Term Contract during FY17-FY19 Mfg Outsourcing, Product development and these contracts are under ramp up and can add 1000 Cr Sales and all contract are at less utilisation level

Agro chemical division business facing downturn nearly 30% Down overall

Benzene Price Volatility leads to inventory losses which is likely to cool off now

Company Business into B2B and having Shallow Cyclical in nature leads to ups and down in the operating margin and overall growth in every 2-3 Years

Capex Guidelines Rs 3000 Cr for next 2 Years 50% for existing products and rest for the new product Chlorotoluene in Jaghadia India with Integrated Operation chain and will have 20% of the Global Capacity and whatever capacity they have built will be at 70%-90% Capacity Utilisation level by FY24 End

Thesis

- Company has Given Guidance Earnings to 3X By FY27 on FY21 As Benchmark based on above expansion and product mix with higher value-added products

- Company have been maintaining CFO/EBITDA Above 75% despite B2B business Model

- Company has Big Marquie Clients recognised Globally

- Company has Strong management with Technical Know How >30 Years

- Company will be able to take benefit of operating Leverage in few years

Anti-Thesis

- From the current Outlook company seems to sleep more at least for next 1 Years

- Company debt will mount and Deprecation too may lead to poor earnings for next 1years Minimum

- How company able to pay such debt to be Noticed

- How Orderbook of the Company at Current stage and going forward

- Over Capacity and if China starts dumping company may suffer

Epigral Coming On Smaller Scale " Chlorotoluene"

16 Likes

Thanks. Good overview.

One question: How can one know if there is dumping happening from China or elsewhere in general? How do market participants get to know that? I have seen this in the past that a few times that stock prices start correcting only after several weeks do we know that the correction is due to dumping. How can we know this closer to when the dumping starts?

1 Like

Hi @Kapil22

listening various Con Call from same indutries you can verify the same ,is it only with this company or happening same with peers for better Clarity.

1 Like

Another indicator that decides dumping can happen or not is how Chinese economy shapes up. Since Chinese economy is slow and domestic demand isn’t much there, dumping has happened. So tracking Chinese economy and its credit growth can be one macro indicator. Cyclical upswings in chemicals can be due to Chinese credit expansion.

9 Likes