What do you think of valuations at this point?

Is it in overpriced category or upcoming capacity commencement subsidises the premium valuations ?

1 Like

Hi,

I’ll leave it up to you whether the stock is underpriced or overpriced.

However, based on the past performance, a few things should be considered:

a) The business has performed exceptionally well in recent years, and even with significant capital expenditures for a small company like Aaron Industries, operating margins are still increasing.

b) As we all know, when it comes to capex, opex rises first and operating margins fall till capex is fructified.

c) Considering a nanocap and past performance, the business has been able to command a premium valuation for past many years.

Important points from first con-call:

a) The company has over 1500 customers, with 70% being recurrent. In 2018, the company ventured into SS sheets as a backward integration.

b) Increased urbanization and multi-story building construction will drive further need for elevators. Even elevators have become a need in G+2 and G+3 bungalows and residential structures.

c) The company has increased its automatic door capacity from 2000 to 5000 per month as stated in the above posts (now at 80% utilization and 58% revenue contribution).

d) Management has clearly said that they don’t require any additional leverage for working capital and the same will be taken care from the internal accruals only. It is to be noted that due to installation of new automatic machine the production efficiency would be improved by 3x and will reduce the lead time from 20 days to 5 to 7 days. As a result, they are now completely focused on growing their order book and network.

e) It is worth noting that they are the sole supplier of embossed stainless steel sheets after Jindal. Embossed stainless steel sheets and designer cabins are in high demand in the bungalow and low-rise commercial categories, including malls and showrooms. Architects are also inquiring embossed SS sheets for facades or reception backdrops.

Considering the above facts, I believe company should report a topline of Rs 105-120cr and Rs 140-160cr in with EBITDA margins of 18-20% in FY’26 and 27 respectively.

Disclaimer: Invested from lower levels and biased. No buy/sell recommendation by any means.

12 Likes

Company has released video of their new facility…

6 Likes

We will be visiting the new plant site at Kosamba, Surat of Aaron Industries on 22nd Jan. If you have any queries please DM me…

AARON_18012025163911_PlantVisit_18012025.pdf (2.1 MB)

4 Likes

Kindly update after meeting with management. What is their growth plan,order book and compatition with their peers.

1 Like

Plant Visit: Aaron Industries Ltd (Discovering a Hidden Gem in Elevator Components)

Date of Visit: 22nd Jan’25

**Visited By: @Anurag477 @Dakshay

Left to Right: Shanki Bansal, Amar Doshi, Anurag Jain, Dakshay Parwani, Paresh Naik and Karan Doshi

Capex incurred in last year of Rs 32cr approx. Break up as below:

- Fully automated Powder Coating machine – Rs 6-6.5cr (still not operational and would

require another 45 days or so) - Fully automated Embossing machine - Rs 4 – 4.5cr (operational)

- Fully automated door machine (Salvagnini) – Rs 22-23cr (operational)

- Automated Assembly Line (would require another 45 days or so)

As we know, AIL have 2 business verticals:

- Stainless Steel Polishing

- Elevator Components Division

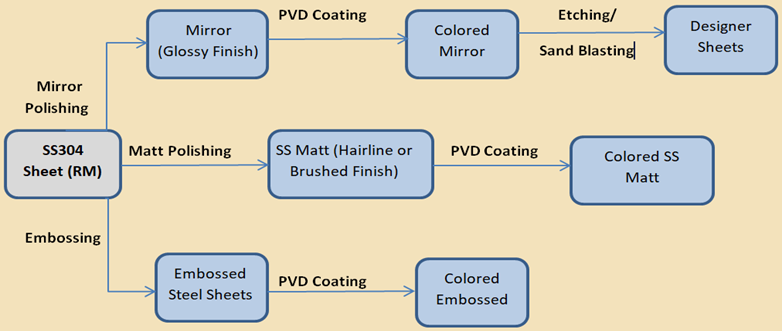

Stainless Steel Polishing Division process flow:

We have seen in stainless steel division has 3 variety of finishes – Mirror, Matt and Embossed design and the process flow is represented as above. Below are the varieties of designer sheets in various colors and combinations:

Elevator Division: Company used to manufacture all kinds of Autodoor systems, Elevator Cabins and other components:

Stainless steel sheets are inserted from the top and the machine is used to cut, bend, punch, and mold them in 60 seconds, according to the system’s size and specifications. It requires minimal human intervention only for loading and unloading. Prior to this it was tedious task due to multiple machines and labor work involved for cutting, bending and punching. As a result, we can clearly perceive an improvement in efficiency following the installation of the Salvignini Machine.

Growth drivers and future potential:

a) Automation and Capacity Expansion: AIL has left no stone unturned till date to tap India’s burgeoning elevator business. Unit 3, from polishing to final goods, is currently scheduled to be automated, considerably increasing the company’s productivity. The company is now manufacturing 1800 to 1900 doors per month, with a current capacity of 2000 doors (to be increased to 5000 doors). Paresh Naik (ex-Reliance Industries) is completely focused on expanding the order book and entering new markets.

b) Why Aaron? (Key USPs)

- As we know, big brands such as OTIS, Kone, Jhonson, Mitsubishi, ThyssenKrupp Elevator, and Schindler only offer standard cabins and elevators. AIL is best positioned to meet the expanding need for mall and residential beautification, as evidenced by the 100+ designs shown above. They can now emboss logos and other designs based on the buyer’s specifications.

- Company has launched their loyalty program to reward their recurring customers.

- Company has recently got approval for Fire certified autodoor system, which can restrict Fire from entering the elevator for minimum 2 hours.

c) Outlook and Growth prospects:

- Depending on the number of floors, the cost of an elevator component might range from 40% to 60%. As an illustration, the elevator component makes up 40% of the elevator in G+ 3 residential villas because only 10 doors are needed (2 on each floor and an additional 2 on the base floor); but, if the project is G+20, the same will be 60% due to higher number of doors requirement. The government has revealed 30 skyscrapers in Gujarat’s four largest cities: Ahmedabad, Surat, Rajkot, and Vadodara. Skyscrapers: 30 Skyscrapers Sanctioned in Four Major Cities by Gujarat Government | Ahmedabad News - Times of India

- Out of 30 skyscrapers, 25 are in Ahmedabad and company has opened a new branch in Ahmedabad- to provide better and smooth service to our customers and enhance new customer base. https://nsearchives.nseindia.com/corporate/AARON_08012024153040_NewBranch_08012023.pdf

- The non-availability of a goods lift or an elevator big enough to carry in case of a medical emergency in tall buildings in Gujarat is turning into a big issue. Under the Gujarat General Development Control Regulations (GDCR), there are two categories for elevator installation in tall buildings. For a building with a height of 10-21 meters, at least one elevator is needed. However, if the building has more than 30 units, one lift is mandatory for every additional 30 units. For buildings having a height between 21 meters and 70 meters, at least two lifts are mandatory, provided there is one lift for every 30 units. https://thesecretariat.in/article/most-residential-high-rises-in-major-gujarat-cities-lack-big-elevators

- The company has recently on boarded OMEGA a midsize player in elevator segment. In Ahmedabad, OMEGA has tied up for few skyscraper projects for elevators. Hence AIL can be benefitted.

- The new embossing machine in the steel polishing section is the only one of its kind in India, second only to Jindal (but even Jindal doesn’t have as many designs). Currently, the machine is operational, but the volume is low and is being internally consumed. Going forward, management aims to increase the sales volume from this embossing line to external customers since these designer sheets can be used for beautification such as designer doors, designed walls at the office or mall reception etc.

d) Management Quality (Trustworthy, Capable and Ethical): - Management is visionary, humble, down to earth, trustworthy and ambitious.

- Appointment of Mr. Paresh Naik can be highly beneficial and strategic move. Mr. Paresh Naik possess over 35 years of experience in sales and marketing, including 20 years with Reliance Industries. He has led various retail teams on a PAN India basis and possesses a deep understanding and experience in building network and marketing products across the country.

- Management is now focused on building order book as their entire capex will be operational by Mar’25, hence the current quarter is vital for the company growth.

Risks involved:

- AIL is dependent on China for key raw material i.e. SS304, hence currently maintaining the raw material inventory of 75 to 90 days. Going forward with increase in sales company may require additional short term borrowings to cater their working capital need.

- The EBITDA/ CFO conversion is less than 50%.

- With the installation of the Salvagnini machine, the management plans to enter contract manufacturing, aiming to take volume orders from major lift manufacturing companies like Johnson, KONE and OTIS which may impact the current margin profile.

Conclusion:

I believe the company is on right track to cater the growing demand in elevator segment. With a wide range of sheets in different colors, such as Rose Gold, Golden, Matt finish, digital designing, and embossed, the company can now reach a large number of end users, including those in the commercial, residential, mall, and hospitality sectors, by offering outputs that are tailored basis customer requirements.

Now whether they will be able to scale up in a big way? Only time will tell.

Disclaimer: Only for educational purpose, and not a stock recommendation by any means.

20 Likes

Aaron industries capex is live now…

AARON_07042025130618_CommercialProduction_07042025.pdf (2.9 MB)

Some insights

AARON_07042025140116_MagazinePublication_07042025.pdf (3.1 MB)

3 Likes

AIL reported its highest ever topline of Rs 77.5cr…

4 Likes

Dear Mr Shakti, I am new to the forum. However please help me with the following

- It seems after going through the discussion major part of the moat hinges on the embossing machine and Salvagnini machine. As mentioned earlier by you the entire system put together costs around 32-33 Cr. This is not a huge amount which can be a entry barrier

- Other point being made that established players are not offering designer cabins. Not entirely true. Kone launched designs in 2021 as per the following article. Therefore is design the entry barrier or Aaron is supplying these designer sheets to Kone. In the 2nd case how many marquee customers does Aaron have. Is Aaron the only supplier to the established elevator companies in India. This can be a moat for the company. However given the low capital requirement this may not be sustainable and MNCs always like to have multiple suppliers to derisk supply chain

1 Like

1 - I don’t think there is a clear moat in this. But they have been on point on the execution so far and that is what been driving the growth

2 - Aaron’s clients are not leading players like OTIS. From what I have read it is mostly Tier 2 or 3 players who they supply to.

2 Likes

Any idea why this capex change does not reflect into fixed assets?

In the latest balance sheet, we can still see fixed assets at around 25cr and CWIP of 32cr? Is there new work in progress?

2 Likes

I had stated that Rs 32-35 crore capex is huge for a company of Aaron’s size. Furthermore, the designed SS sheet is currently imported from China and In India after Jindal, Aaron now manufacturing (but even Jindal doesn’t have as many designs as per the management during last call)

Kone Elevator India has only limited number of designs, but Aaron has over 100 plus designs with the option of customization. They can now emboss logos and other designs according to the buyer’s needs. The elevator industry is fragmented, with approximately 40% of the market dominated by unorganized operators. They used to provide elevator components to small OEMs in Gujarat, Rajasthan and Maharashtra. However, with current capex, companies are now focusing on long-term agreements and contracts. The current market size of elevator industry in India is close to Rs 40,000cr as highlighted by the management in the Nov con-call.

The capex was completed on 7th April.

3 Likes

Thank you Shanki, my bad! Also, appreciate all the details and research you have done on this so far. Your inputs have been very helpful!

Dear Mr Shakti Thanks for the prompt response and clarification. Really appreciate. My point precisely being why the bigger players are not sourcing from Aaron with the capabilities they posses. As you had rightly mentioned the organized market is 60%. Does it mean the establishe players still import competing products from China. Has there been any effort from Aaron’s side to supply to Tier 1 companies.

Pardon my ignorance to any point that was already discussed in this regard

3 Likes

A short summary on company’s latest concall

It is very strange to see very lack lustre performance from Aaron. There has been a lot of discussion in this forum regarding huge target market size. But inspite of latest Capex, latest Qtr results and profit is not at all confidence boosting. So it is crystal clear to me that the company has no MOAT. Inspite of this, it is being quoted at a PE of 100. Really staggering. It is beyond me to think that who is buying this stock when dozens , if not hundreds of better performing companies with tremendous growth out look are available at one tenth of its valuation.

We small investors frequently lament our luck for stock crash. But if we buy such stocks at prevailing valuations, it is at our own peril.

NB- I may be wrong in my assessment. But this is posted for general consumption and precaution to be taken by small retail investors like me.

3 Likes

I see trailing PE at no more than 65 currently.

And listening to guidance, FY26 forward PE stands at < 40.

Considering, 120cr topline at 10% PAT (which is historic & I’m not assuming any operating lev for this FY) ~= 478/12

I consider the valuations to be fair - fairly high, but definitely not exorbitant and 100PE of sorts..

2 Likes

Thank you Kushal for your observations. When I mentioned PE of above 100, it was a fact as per Q1. If you feel it is fairly valued, it is ok with me if you want to justify the valuation. My point is frequently retail investors become sentimental about stocks and shy away from critical observations from stocks they are invested in. And this is why they become losers.

After all we invest in stocks for gain. And so different investors employ different mechanism to increase their return, like fundamental, technical, momentum, thematic, sectoral, etc. So if you feel that out of 4000 stocks Aaron will give you good return then my best wishes are with you.

2 Likes