Seems typo error…will complete in Jan 23

1 Like

Aaron Industries installed steel embossing machine.

Steel Embossing machine impresses patterns on stainless steel sheets.Import substitute as 90% of such sheet was being imported to India.

Only company in India capable of offering more than seven varieties of embossing patterns on stainless steel sheets

AARON_22022024111733_PressRelease_22022024.pdf (1.6 MB)

6 Likes

Aaron Industries acquired new machine from Salvagnini for the fabrication of elevator components. Production capacity to multiply by at least 3 times, lead to better efficiency and quality with reduction in costs.

AARON_01032024123109_PressRelease_ImportofSalvagniniMachine_01032024.pdf (1.6 MB)

5 Likes

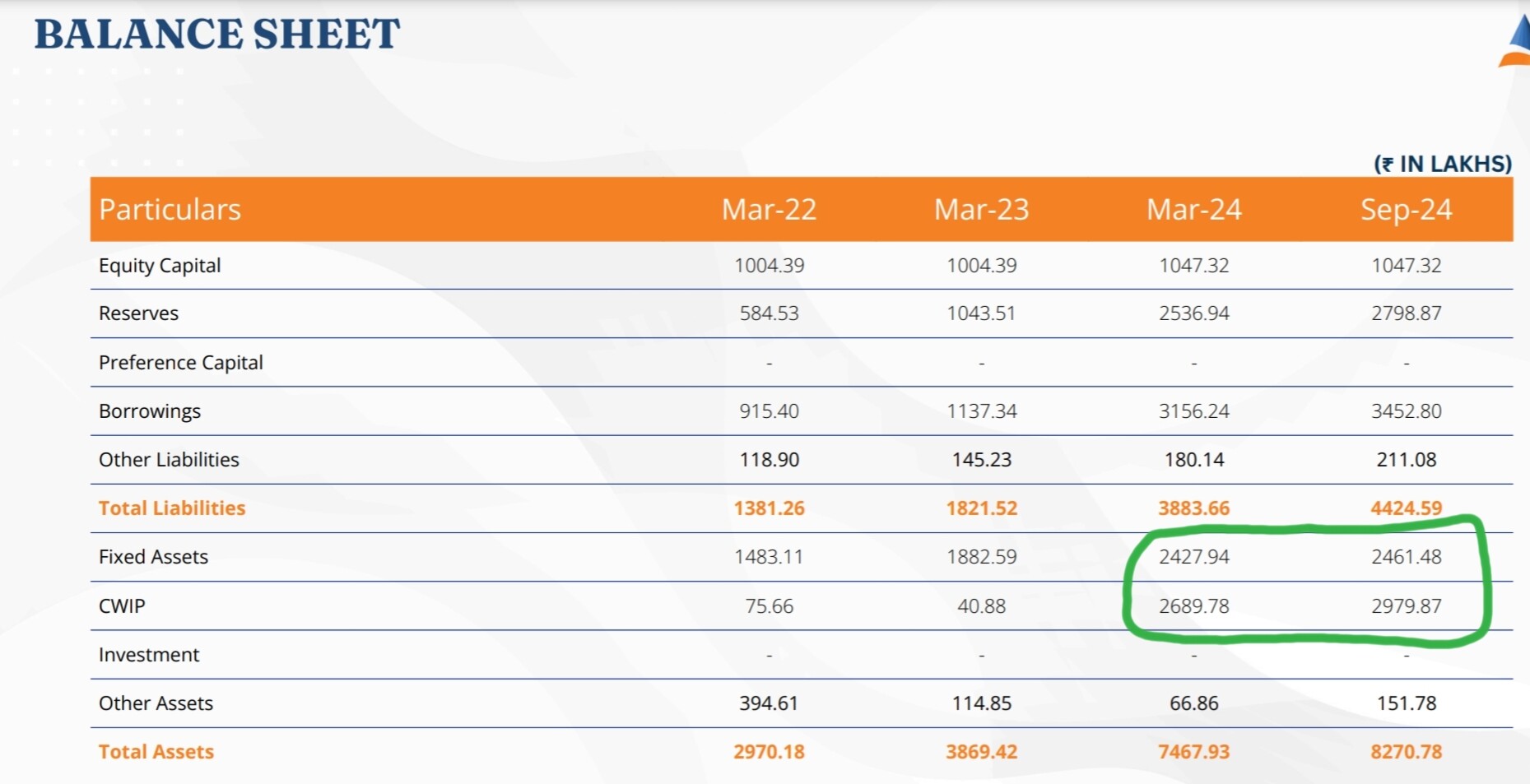

Capex Update:

As per the recent quarterly results of Mar’24, we have noted the CWIP of Rs 26.90cr, which is more than the double of existing net asset block. The majority of the capex is allocated to the Greenfield project at Unit 3 in Block No.251, Plot No.B-2, Royal Industrial Park, Vill. Moti Pardi, Ta. Mangrol, Surat - 394120, Gujarat, India. This unit is outfitted with machinery purchased from Salvagnini particularly for the manufacture of elevator components. This advanced equipment is currently in the installation phase.

The company has also engaged in brownfield growth, including upgrades to existing machinery. These changes are designed to boost productivity and operational efficiency.

The unit 3 is expected to be operational by July 24 and remaining capex will be completed within next 2 months.

Two new branches opened in 2023-2024, one in Ahmedabad and the other in West Bengal. These new branches are now in the early stages of expansion, and their performance is expected to significantly impact the company’s results in the current fiscal year 2024-25.

Reason for drop in elevator segment margins:

In the latest quarterly results, we saw compression in the margins of elevator segment, with the operating margins dropping from 47% to 36%. As per the management, below are the primary facts underlying the drop in margins:

Inventory Management: Company has proactively removed dead stock, which while necessary for operational efficiency, impacted their short-term margins.

Optimized Inventory Levels: To improve their inventory cycle and avoid tying up finances, company has adopted a strategy of maintaining lower inventory levels. This strategic shift, though beneficial in the long term, has contributed to the margin reduction in the short term.

Going Forward:

Post completion of capex by Ju’24; the company is expecting a significant improvement in top and bottom-line. Further company has no requirement of further debt in FY 24-25. Their main focus remains on efficiently managing their existing resources and ensuring the successful completion of Unit 3.

14 Likes

Recent Developments:

Capex delayed:

The delays in the construction of their new manufacturing Unit-3 primarily attributed to several factors beyond their immediate control. These challenges included adjustments required for the installation of specialized equipment, unexpected structural issues necessitating reconstruction efforts, and more recently, disruptions caused by an unusually prolonged monsoon season and associated labor shortages. The company is now more proactive and assured that every effort is being made to bring this project to fruition within the revised timeline of December 2024.

Post Capex Completion:

Post installation of new Salvagnini machine for the fabrication of elevator components, the business expects to boost production efficiency by threefold. The company now has a 3-3.5x asset turnover. As a result, based on the net asset block of Rs 50 crore following capex completion, the company may generate a topline of Rs 250-300 crore. Operating leverage will become apparent starting in Q4.

Reason for losses in Steel polishing division:

-

Raw Material Procurement: AIL procure stainless steel 2B coils from suppliers. These materials are initially booked under the Steel Polishing Segment as a purchase.

-

Processing and Transfer: After undergoing cutting and polishing in the Steel Polishing Division, the processed steel is transferred to their Elevator Division on a challan basis (cost basis). This internal transfer ensures that the majority of the processed steel is used within the company.

-

Revenue Generation: The primary objective of this division is not standalone profitability but to ensure a seamless supply chain for their elevator products, thereby reducing costs and dependencies in the long run.

Jun’24 results:

The company has reported a decent set of numbers with highest EBITDA margins at 19.2% despite a notable increase in employee costs and other expenses y-oy and q-o-q. This increase is primarily attributable to their expansion initiatives, including the opening of 2 new branches and current capex.

Disclaimer: Invested from lower levels and recently scaled up. No buy/sell recommendation by any means.

11 Likes

Is all of the capex coming into elevator division or is it part elevator and part steel polishing division?

The company has not provided any segregation.

The new Salvagnini machine for the manufacturing of elevator components will improve production by multifold. Please go through the below video:

5 Likes

Hi…

Aaron Industries was listed in September of 2018, and you can read their annual report of 2019-20, which includes their growth philosophy.

The market cap was barely Rs 20cr, but they were confident in their strategy and philosophy for growing. (Read past annual reports)

Few points to be noted in last 5 years about the performance of the company:

- Top and bottom lines grew by 36% and 48%, respectively.

- The fixed asset block has been increased from Rs 8cr (2019) to Rs 24cr (Rs 26 cr in CWIP).

- The debt to equity ratio is always less than one.

- A consistent cash conversion cycle of 140 days maintained.

- Operating margins have improved from 11% in 2019 to 19% in the last two quarters.

My only concern is that management doesn’t do con-calls and hence the information is limited. However, they used to respond any investor query over the email with full details in a timely manner.

Disclaimer: Invested from lower levels and biased. No buy/sell recommendation by any means.

8 Likes

@Shanki_Bansal

Thank you so much for your inputs.

Few pros and cons are there like

Good promoter holding

EBIDTA/interest is fine

No concalls etc.

What is your take on promoters

Honesty, risk mitigation, sustainability, how they treat employees.

Thanks in advance

can someone explain how the earnings are going to look like going forward? And whether or not this is a reputable company within the elevator space

Please refer the above post

AARON_28102024155416_InvestorPresentation_28102024-compressed.pdf (2.4 MB)

Decent Q2 results posted by Aaron, stable topline around 18 crores with margins at 17.5%.

Good thing - First ever PPT shared by the management.

The Capex to yield additional revenue of 150 crores going forward.

3 Likes

Is the capex completed/completed partially?

If yes why hasn’t the cwip amount converted to fixed assets?

What gives them right to win? They have done capex what gives visibility of going ahead to have additional revenue of 150 cr from this? Is there any thing special to them?

Disclosure: new to to the company & studying the company

Please go through the below posts:

1 Like

Found the transcript of AGM in their website

The construction of Unit 3 to be finished by Q3 and then it will add to revenue.

" Additionally, I am excited to update you on the progress of our company’s Unit-3, which is

currently under construction. Despite facing numerous challenges during construction, we

expect it to be completed by December 2024. Once operational, Unit-3 will substantially

enhance our capacity, driving significant increases in our revenue and overall growth

Looking ahead, I see tremendous opportunities for sustained growth in our product range. Weare continually exploring new avenues to expand our market presence and enhance our profitability. All indicators point towards a promising future, and we are strategically positioned to capture these opportunities and further improve our margins"

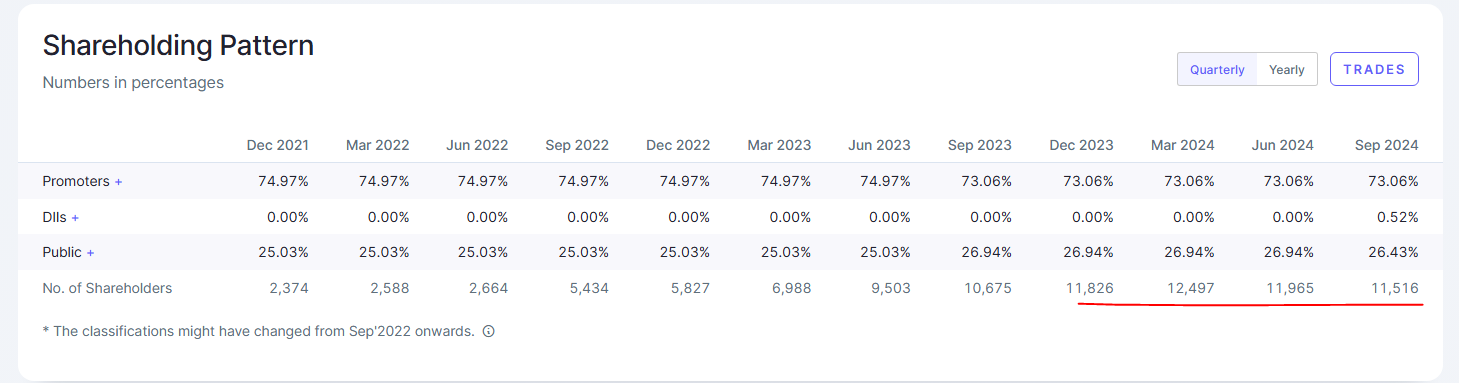

Number of share holders reducing in past couple of quarters. It’s a good sign imo

Disclosure: not invested. will take a tracking position.

2 Likes

Capacity expansion is still not live…

AARON_09112024120428_Update_09112024.pdf (601.0 KB)

1 Like

Latest Update on Capex:

AIL has clarified that the ongoing capital expenditure (Capex) project is still under development, and the recently shared PPT contained a typographical oversight.

The target capacities for this CAPEX, which is expected to be operational by December 24, are as follows:

The elevator division :

| Product | Existing Capacity (Per Month) | Targeted Capacity (Per Month) |

|---|---|---|

| Elevator Cabins | 150+ | 300+ |

| Automatic Doors | 2000+ | 5000+ |

| Safety Frames | 50+ | 100+ |

Other Components: Supporting parts and accessories for cabins, doors, and frames, which form an essential part of their product line, cannot be measured in specific unit terms.

In Stainless Steel division :

| Product Name | Existing Capacity (Per Month) | Targeted Capacity (Per Month) |

|---|---|---|

| Matt Polishing | 50+ Tons | 150+ Tons |

| Mirror Polishing | 50+ Tons | 100+ Tons |

| PVD Coating | 700+ Sheets | 2000 Sheets |

| Decorative SS Sheets | 500+ Sheets | 1500+ Sheets |

| Embossing | - | 100 Tons |

| Press Plates | 100 Plates | 100 Plates |

Note on Capacity Utilization:

All are interconnected in production process. For example, sheets may pass through multiple steps—such as embossing, matt or mirror polishing, and then decorative SS finishing—before reaching the final product stage. Thus, each process step contributes to a cumulative production journey for a single end product, and as such, the capacity utilized in each stage cannot be simply summed up as an overall utilization figure.

The primary focus area of the company is matt polishing, mirror polishing, PVD coating, and decorative SS sheets due to increased demand and customer interest especially post installation of embossing machine (put to use in Feb '24 update); which is now commercially operational. Company has delivered trail batches to key clients and once they confirmed their complete satisfaction with the product quality, production will start in full swing.

Way forward:

AIL is expecting at least an additional topline of Rs 150cr on conservative basis post commercialization of CAPEX and successful installation of Salvagnini machine. The company is expecting to maintain EBITDA margins at 20% plus. At present, company do not foresee the need for further long term debt.

13 Likes

Capex update:

The construction of new manufacturing unit (Unit-3), located at Block No. 251, Plot No. B-2, Royal Industrial Park, Village Moti Pardi, Taluka Mangrol, Surat - 394120, Gujarat, India, has been successfully completed ahead of the revised schedule.

Company is now preparing for the next phase, which includes commissioning and testing

the production equipment. Commercial production is expected to commence shortly.

AARON_16122024142326_UpdateonUnit-3.pdf (523.5 KB)

2 Likes