Background

3M India Limited is 75% owned subsidiary of 3M Company, USA. In 1988, 3M India began its journey as Birla 3M Ltd, a joint venture between 3M Company and the Birla Group. In 1991, Birla 3M India was listed on the Indian stock exchanges and only in 2002 did the company’s name change to 3M India Ltd. It’s the seond only listed 3M group beside 3M Inc in United States.

The Company manages its operations in five operating segments: Industrial, Health Care, Safety and Graphics, Consumer and Energy. In India, the Company has manufacturing facilities at Ahmedabad, Bangalore, Pune and has a R&D Center in Bangalore. 3M India’s five business segments bring together common or related 3M technologies that enhance the development of innovative products and services and provide efficient sharing of business resources. Most 3M products involve expertise in product development, manufacturing and marketing, and are subject to competition from products manufactured and sold by other technologically oriented companies.

For more details about parent company please visit following link

https://investors.3m.com/overview/default.aspx

3M India Limited is a technology company. The Company’s segments include Industrial segment, Health Care, Safety and Graphics, Consumer and Energy.

Source: FY18 Annual report

Research driven business:

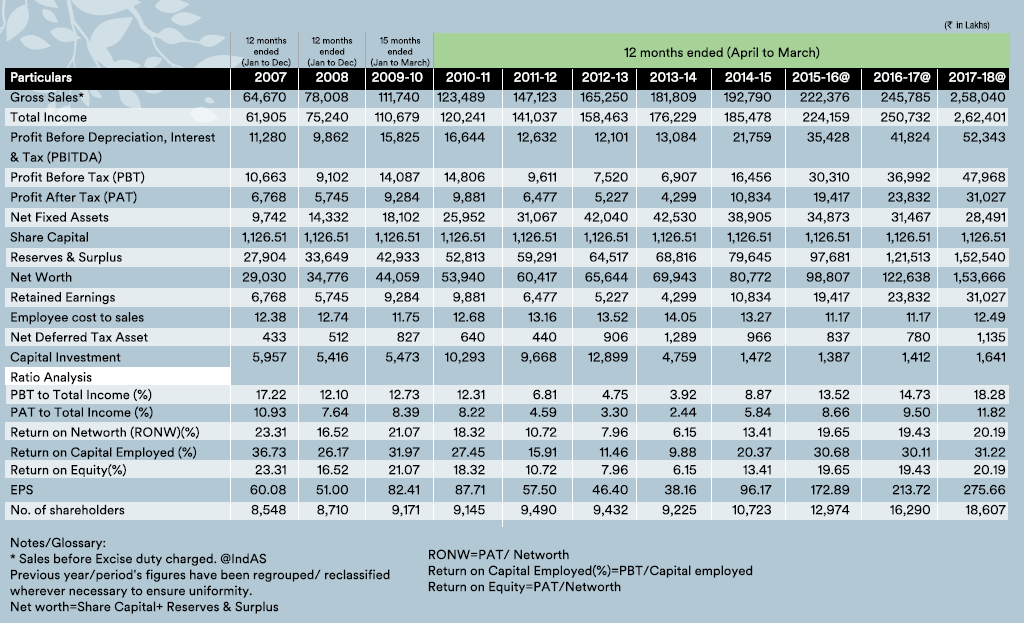

During FY10 to FY18, 3M india has spent Rs 481.03 Cr on R&D with average of 3.23% of sales. Very few MNC have utilised Indian subsidiary for research. 3M India research initiative has resulted in major success with nearly 100 patents filed by 2016. The research unit focus also developing products specific to Indian market.

Globally 3M is among the most innovative company with nearly 113,000 patent filed over the period.

Critical subsidiary for parent:

In very few countries 3M has subsidiary with 75% equity holding. In 2017 form 10K filed by 3M with SEC, the minority interest item has explenation which give understanding that beside India, none of the other major country 3M has minority partner.

Further, during intial period, 3M has supported Indian subsidiary by waiving of royalty payments. Find extract of relevant portion from Annual report of FY18 of 3M India.

During FY10-18 period, total royalty payment by 3M India to Parent is Rs 156 Cr which is lower than Income earned from Parent for Contract Research of Rs 158 Cr.

Lastly, 3M US has a fully owned private limited company as subsidiary by name 3M ELECTRO AND COMMUNICATION INDIA PRIVATE LIMITED which was registed in 1989. The company is now in process to merged with 3M India. Details of financial and other terms of merger are in enclosed presentation.

https://multimedia.3m.com/mws/media/1585456O/agm-2018-presentation.pdf

The company would be making total cash payment of Rs 590 Cr. 3M electro reported net profit of Rs 22.8 Cr during FY18, which mean acquisition P/E of around 26 times. While amount paid is probably at higher end of unlisted private limited company, it ensure that 3M India would be the only entity for business in India for 3M USA.

Business Propsect:

3M India growth prospect are highlighed by management in presentation made to sharheolder in AGM of 2018. It is very difficult to project future sale and profit growth as there are more than 10,000 product of 70,000 product marketed by 3M US. What is interesting is despite industrial growth in India being lower during last 4-5 years, 3M Industrial segment has been showing very healthy profitable growth duing the same period.

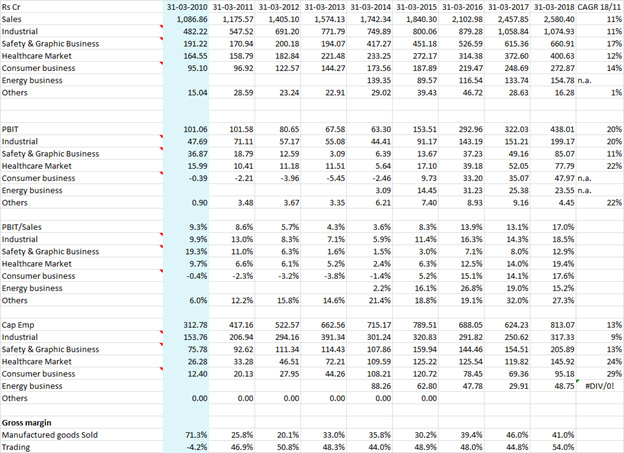

Segmentwise Sales and PBIT

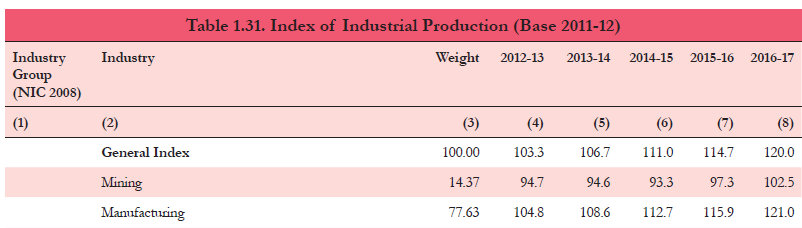

While Index of Industrial production (as published in Economy survery of Jan 2018), has growth at CAGR of 3.7% p.a. during FY12 to FY17 period, 3M India Industrial sales registered CAGR of 8.9% p.a. during same period. Even after adjusting for inflation of 3% p.a., as against nominal growth of 6.7%, Industrial segment sales has outpaced Indian Industrial growth. Industrial segment PBIT had registered growth of 21.5% p.a. CAGR during same period.

That give confirmation that 3M India can grow profitably even in difficult market conditions.

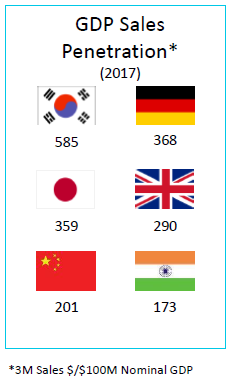

3M India in its presenation to Shareholder has shared interesting graph which indicates sales in USD/ mn USD nominal GDP. As expected, India GDP penetration is lower than most of the countries.

If we compare same with other industries, the gap appear to lower (with China being almost at same level to India). Having said that, mutiple product, superior quality and near mononpoly situation may assist 3M India to register higher growth.

It is pertinent to note that the gross margin on traded sales (traded sales- purchased finished goods) in 3M India has been in very high range of 44% (lowest during FY14) to 54% (highest during FY18) during FY11-FY18 period. Average Gross margin around 48% which indicate very high pricing flexiblity of the company.

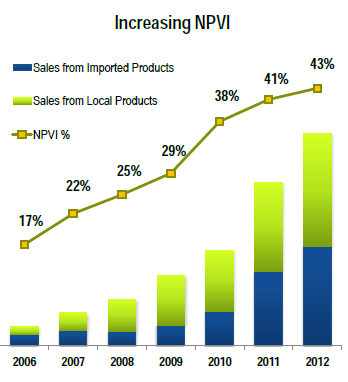

The most critical aspect on 3M India business operations is to understand Indian market and “Indianise” product or service it offer to the customer. Find enclosed article which explain concept behind launch of Car Care units by 3M India. Nowhere in global market, 3M has such srevice being provided. However, looking at Indian market characterstic, it develop a structure which can address customer need at the same offer to leverage of mutilple product the company has to offer to customer.

The same article in 2013 provide aspiration goal of 3M management to reach USD 1 billion by 2017 which it defintely failed to meet on Topline for sure. In FY18 sales of Rs 2500 Cr is not even 50% of the stated sales goal. However, from 1 store in 2010, the company has successfully 100 stores in FY2018.

Risks

High Related party transaction

3M India has very high portion of purchase which is sourced from related party. While the shareholder approve the related party deals, still it may not rule out the risk of unfavourable treatment to the minority shareholders.

Having said that, the company management has shown high integrity in business conduct. Further, I have no knoweldge of unfair treatment being given the minority shareholder in past.

Exchange rate volatility

3M india is exposed to exchange risk volatility (USD INR) due to high level of import traded products and neglible exports. In past, adverse exchage rate movement has adversely affected the company quarterly financials.

However, most of the products marketed by the company are innovative and much superior quality and performance. As a result, it emjoy high pricing flexiblity (kind of monopoly in many of products) and pass on same within 3-6 months period after rupee depreciation.

Very high valuation

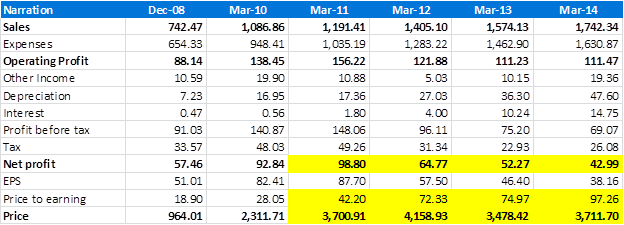

3M India would be among the most expensive company if one consider P/E multiple as valuation parameter. At market price of Rs 20,700 it is trading at Trailing 12 months PE of around 68 times which is super rich valuation.

It may be interesting to note that since March 1994, closing PE for 3M India has been average of 74 times, (Median 63.8 times, Max 638 times and Min, 15.4 times). So rarely company come in attractive value zone for investor, only 21 months of 299 months, closing PE was less than 20 times while on 172 months of 299 months, the company traded at PE higher than 50 times.

3M Past price data.xlsx (38.0 KB)

Incentive to Indian Top Management

3M india executuve compensation have stock option of 3M USA. This may be concern for minority shareholder as Top executive performance would be more align to parent then Indian business. However, 75% stake of parent in subsidiary and also no past incidence of wrong conduct on part of Global management specifically adversely afffecting minority shareholder rights address this concern to an extent.

Link to Business of 3M along with other details.

Disclosure: I had tracking position in the company more than 3 years and recently added as Core holding in my portfolio. My view may be biased due to my investment. Further, I am not a SEBI registered advisor. Investor shall do his/her own due diligence and consult investment advisor before making investment decision,

.

.