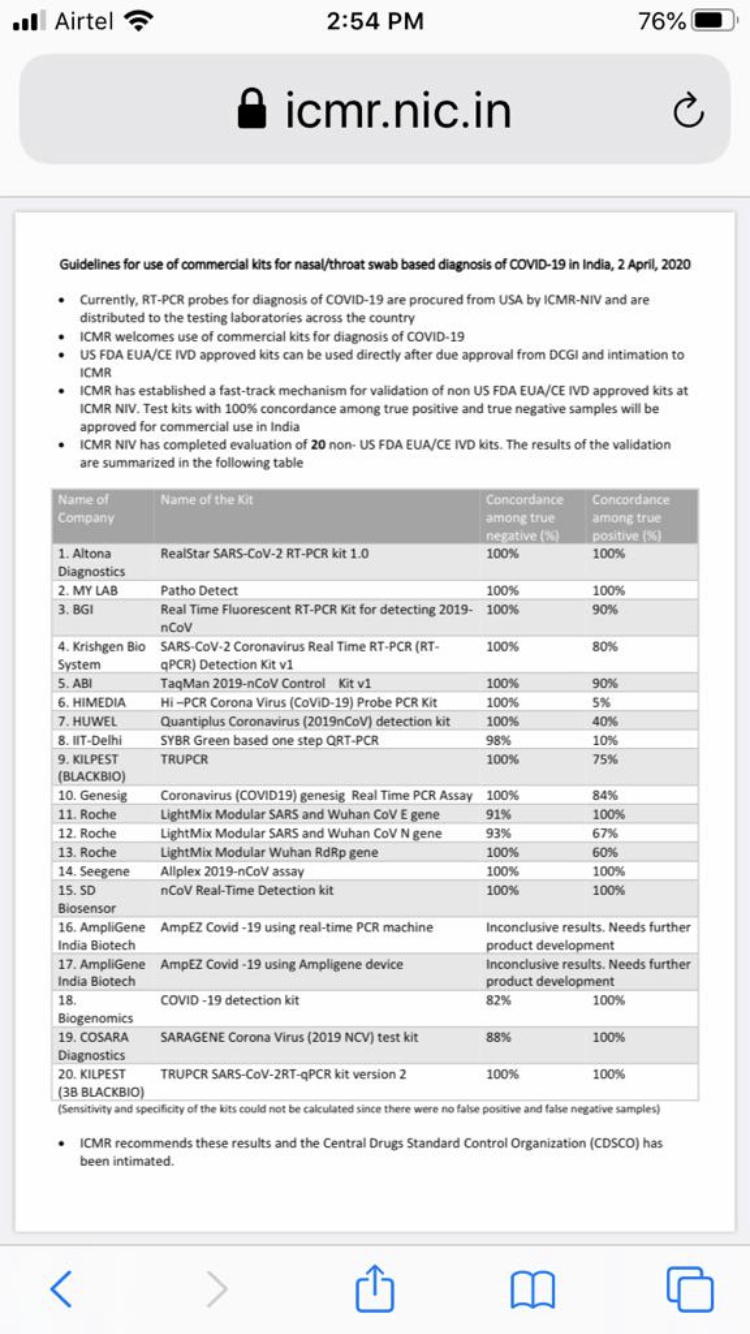

Approval has been given only for them who have shown 100% concordance among both true positive and true negative.

ICMR communication on 02 Apr 2020. See serial No 20 where Kilpest has 100% for both positive & Negative each.

1 Like

Rapid antibody test kits for coronavirus put on hold till further notice. Good for RT-PCR cos.

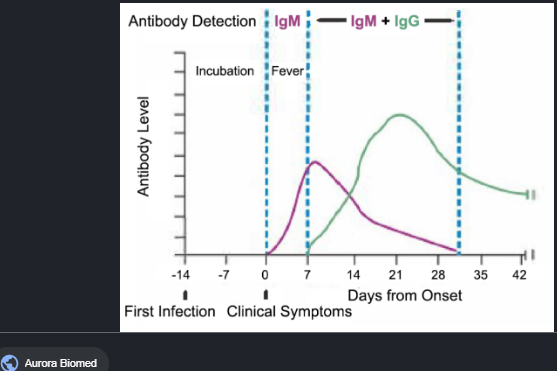

Antibodies develop on or after symptoms. (or even sometimes very low to undetectable in some patients), can be used just for surveillance as per WHO.

Again sharing an old article:

Now ICMR published this on H1N1. Page no 32 suggests TRUPCR (3B Blackbio) performed equal to or better than few established players. Also you can find, on google, few research papers published using TRUPCR kits. Pages 38-51 shows assets required by such companies. We can match assets with above article. So this is knowledge driven business, not assets driven.(This is a risk factor also!!)

HTA_of_various_RT-PCR_kits_for_the_diagnosis_of_Influenza_A_Call_for_Comments.pdf (813.1 KB)

Main risk factors:

(1) Maintain assets in form of employees

(2) Raw material availability

(3) Development of newer technologies, this might open new opportunity or destroy co.

Raw material is in high demand and thats why such collaborations are happening.

Serum Ins.’ Adar invested in Mylab, interesting to know at what valuations?

Mylab posted turnover of 6 crs, while 3b did 12-13 cr.

4 Likes

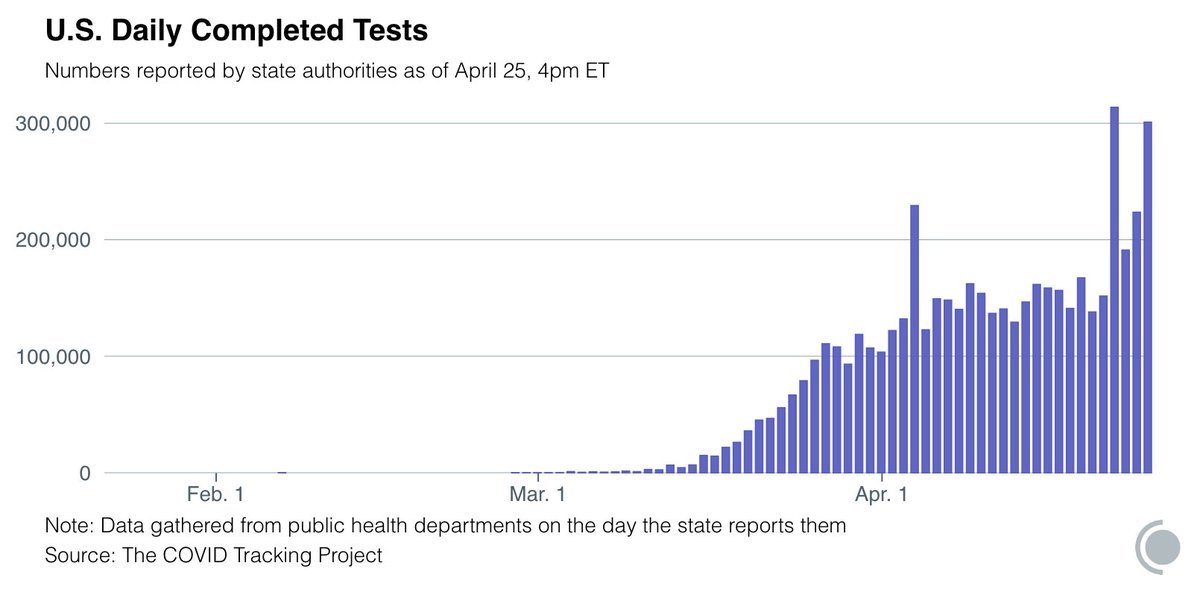

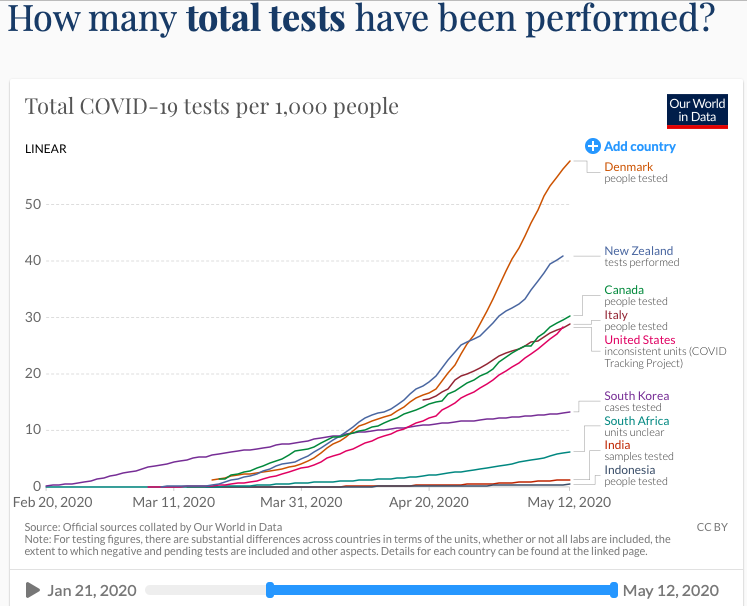

India testing numbers are very low.

Last few days we are testing around 30000/day. (don’t know how much PCR or Rapid).

USA now conducting around 140000 tests/day.

Evenif we take 10 active suppliers for PCR kits, run rate for a co comes at 3000 tests/day.

Assuming 60-90 days of active period for covid, a co can sell 2-3 lakh tests, quite below what they are predicting. (especially mylab is creating too much hype like 20 lakh tests /week or I am missing something).

kilpest targeted 5-10 lakh tests.

Until test rate doesn’t go up, can’t judge.

But long term future looks promising. (I am always optimistic ![]() )

)

1 Like

USA now conducting 3,00,000 tests/day.

10x more than India. Demand for kits in India will remain soft until testing ramped up.

Risk: Slowing corona elsewhere in world may flood market with imported kits.

1 Like

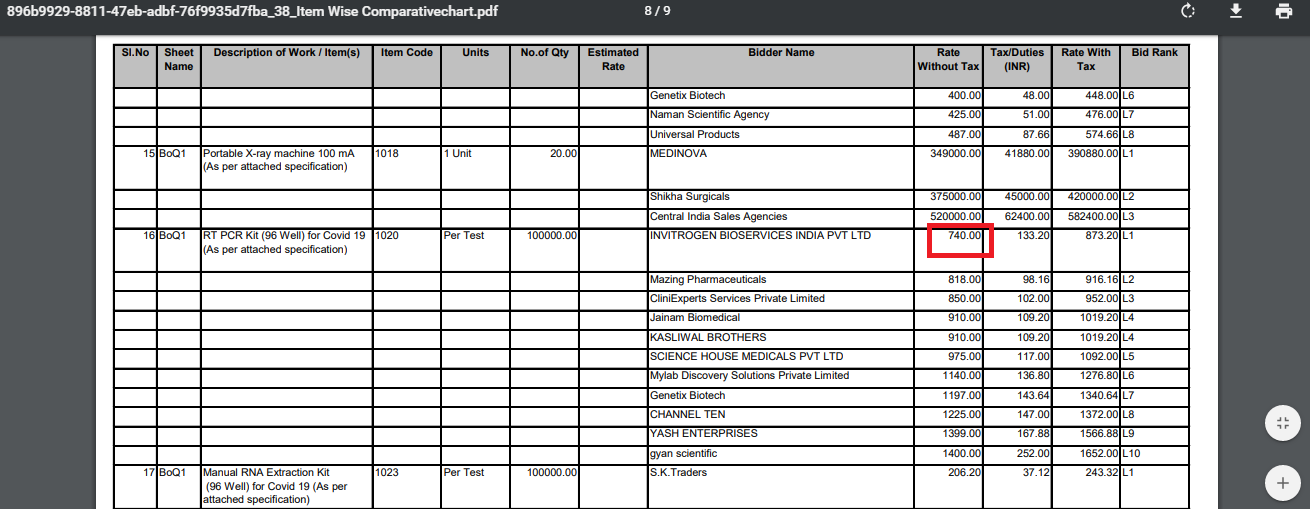

Price range approved by ICMR is Rs 740-1150 for RT-PCR and Rs 528-795 for Rapid Test. No test has been procured at Rs 4500. Any Indian company wanting to supply at lower rates is welcome to contact ICMR : Indian Council of Medical Research

this is big positive if chinese players are out

2 Likes

Invitrogen bioservice india pvt ltd was disqualified to place order for ICMR tender of 30 lakh test kit. They mite try to sell it here.

List_of_firms_not_considered_for_RT_PCR.pdf (186.2 KB)

1 Like

Jai hind

3 Likes

Good update.

They aimed to produce 2lakh tests till april end as per article, but made 1,05,000, and sold 90000.

So that gives them topline of roughly 9 cr.

No doubts on assets, ethics as of now.

Ramping up capacities upto 40-50K/day is quite bullish tone.

ICMR recently said India testing at 45-50k/day and aim is to touch 100000 tests/day.

So kilpest wants to control 50% of market !!!

Remember there are 65 bidders who got rejected in ICMR tender, and outcome of that tender is yet to come.

65 rejected , so assuming that much active suppliers, difficult to control 50% market share.(unless kilpest solely wins ICMR tender for 25 lakh tests)

Opinions are welcomed.

2 Likes

That 65 bidder rejected are some what distributors or sub agents. If you see the list of 65 dealer rejected 2 top companies Altona and Invitrogen Bioservices India Pvt. Ltd (who claims to ramp up production by 1 million test per week got rejected.

There are 17 main producer of the kit as on 23 april 2020, of which 2 were rejected. so even if the kits order is split between 15 producer then also kilpest get share ratio of 166,000 kits. Already having order in hand of 200,000 test , company can easily achive 25cr topline in the month of April itself that almost 2 time there turnover of whole of 2019.

Real_time_PCR_tests_23042020.pdf (22.1 KB)

2 Likes

Lets have a rough calculation:

suppose they produce 8 lakhs tests throughout the year. considering sales of 1000 rs per test.

Assumptions:

- As there is scarce of raw material as said by company, Higher production is difficult.

- Margins would be lower due to ICMR price pressure and raw material scarce which generally leads to higher prices

So for 8 lakh tests leads to revenue of 80 cr.

If we consider 15% EBIT margin leads to profit of 12 cr…

If I consider PAT of 10 cr, at 12 multiple(lower multiple due to lower margin and uncertainty of virus), leads to market cap of 120 cr

Positives:

Big market to snatch with immediate demand

Initial approval of kit is added advantage

Negatives:

Margin may not high due to higher raw material price & unavailability

ICMR disclosed test price of 750 to 1100. so kilpest’s test price is on higher side which may hinder in getting orders

Higher competition. Big player can jump and snatch market share

Agri business would make further losses in this environment which is not considered in assumption and can reduce PAT

Your calculations are very much defective, dont give rough calculation based on your assumption at least consider past margins or may be margin trends to come to any results. You are also talking only about COVID testing what about other products? They may be loosing one quarter of revenue from other products but not whole or future years. This is a temporary kick to its revenue and profit. I have been talking about this company so many times as per my information they aim to grow in mid twenties. Also go through investor presentations, mentioned few rate contract in Rajasthan and Kerala and few long term contract. These steps give them a headstart and less competition in future as this type of business would become supplier sensitive and wont be easy for hospitals and specifically private labs to go with other partner. I just surfed on some of India’s largest Biotech Companies who boast presence in many country but have revenue of sub 100 crore and also saw the test available with them…you just think of any disease or complication they have test for it.

Coming to your valuation, it seems absurd to just value it for COVID. They are making 5 crore PAT already, add it to your calculation and also give some growth to this. I dont know how market is giving it valuation but i think presence of some Top shareholders in shareholder list is becoming a hindrance in its journey.

I have tried to show the Trade Receivables of 3B Black( in Lacs)

FY 12-13 / 13-14 / 14-15/ 15-16/ 16-17 / 17-18 / 18-19/–Hy20

Sales–67----94------100----163----315----765----1119-- ------700

TR—7 --------32 ----- 28------39—102-- ----232-- --437------- 531

In my opinion this trade receivable trend shows revenue from long term contract and rate contract. Also notice that highest sales of kilpest is done in Q2 so the Consolidated Q2 Margins looks suppressed. Look at the margin with increase in sales from 3B, margins are also increasing, interest component is going down. A substantial part of the profit is going to promoters now in terms of salary and dividend by 3B. May be they want to buy more of kilpest but with 3B’s money.

Disc: holding

2 Likes

Vaccine to be invented sooner than later it seems. So one should calculate the fwd pe of 2 3 year considering covid19 a short term(one to two year) event. Though everything seems rosy as of now, it may not sustain for long term.

Disc: Invested

Vaccine is totally different than Immediate treatment. Vaccine requires lot of approval so takes lot of time some where i read about 5 to 10 years. For Immediate treatment they might allow directly but in general as we go for vaccination of Infants it will take lot of time for such. Considering even it becomes available for treatment testing is sill required to to whom vaccine shall be given. In short Testing will continue.

Disclaimer: Invested and added more near 52 week high.

1 Like

Agree on this point but At this point each company is on expansion mode. Say My lab is targeting 1 lac kit per week and expanding thereafter.

Going fwd, It will be difficult to capture market share without reducing prices and competition is gonna increase.

If govt. decides to open economy in future and make decisions to live with corona, people behaviour may change to remain self quarantine and avoid testing as there is no cure.

Some hospitals are advising people to quarantine without testing as its an only cure.

Testing helps at present to identify hotspot at present but lockdown can not be implemented forever. So going fwd if govt adopts herd cimmunity concept, there would be no jeed of testing everyone except critical cases.

IMO the bigger questions are what will Kilpest do with this opportunity and recognition, will they be satisfied with this extraordinary year or leverage it to go to the next level as a business? Will value created be shared with minority shareholders? When will they complete the demerger and list 3B BlackBio?

Testing demand will exceed supply for a long time even with new entrants coming in. Testing in India is very very low currently and the first Covid+ curve has not even flattened yet.

There will be future waves as seen in Singapore, Europe and Wuhan, China as well. We will need tests to meet current demand and then stockpile tests for future use as well.

Wuhan which was declared “Covid-free” ordered 11 million tests to be conducted for all its residents after 6 cases emerged.(Wuhan to test all residents for coronavirus in 10 days after new cases emerge - CNN)

Vaccine development timeline is highly speculative and the best experts (Dr Fauci, Bill Gates etc) have said it is at least 12 months away. Then there is the process of mass production and administering the vaccine to the entire world. The only way to reopen the economy effectively is to keep testing…

Disc . Invested

4 Likes

Please support your revenue estimates with some information or calculation or else it would only become speculation. VP forum does not allow this type of behavior. Please do not post any post for sake of posting or this thread will become useless. We need healthy and constructive discussion at this moment. Current time can be life changing time for this company and may be for many of the investors here. So just do constructive discussion you should be able to back up your claim even me or anyone can give revenue estimation without any knowledge. This thread is being observed by many outstanding investors, they can be helpful if and only if you people behave properly.

Please forgive me for my comments but its also correct.

1 Like

Here is simple calculation:

company is producing 10000 tests per day and order is increasing daily as per company filing

company is planning for 50000 per day capacity

at 1000 per kit price, company can generate 1 cr per day revenue even if it fully utilise current capacity

so if we estimate avg of 10000 kits per day revenue for the rest of the year it can reach around 250cr plus…