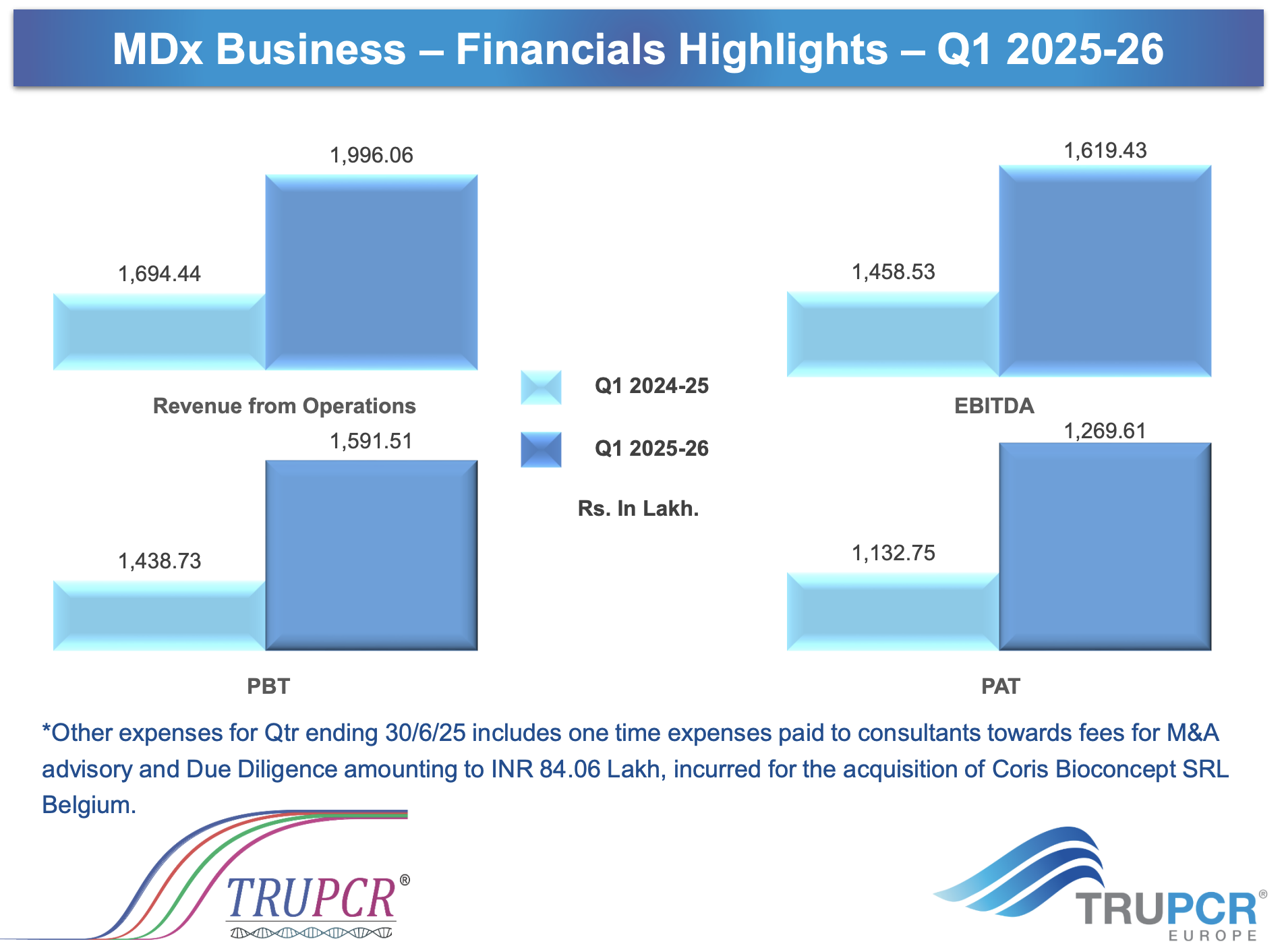

Diagnostics Revenue of 19.9 cr (+18% YoY), Diagnostics PAT of 13.5 cr (+19% YoY) - excluding one time Corus transaction cost.

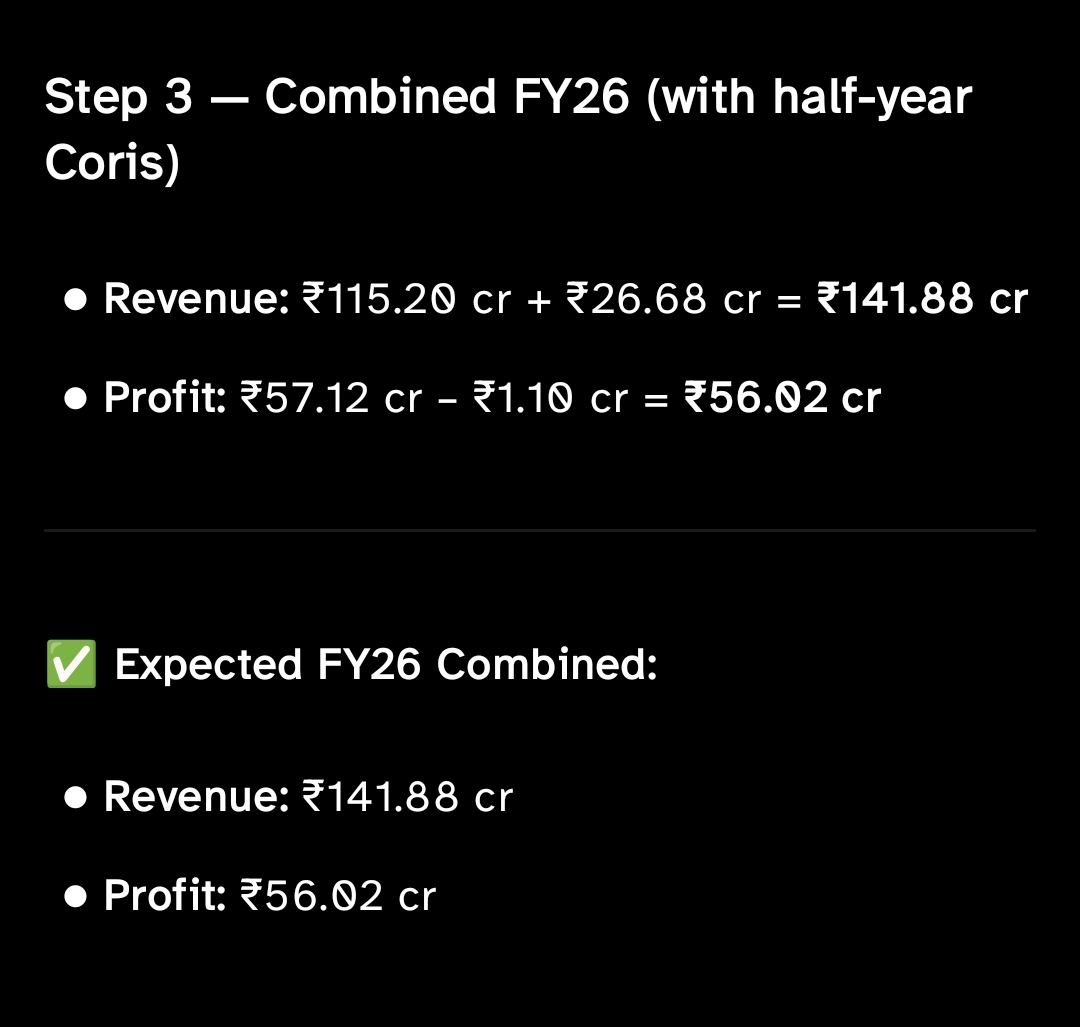

Guidance for Corus Bio to become EBITDA +ve within one year (so FY26-27). Corus Revenue was ~52 cr in calendar 2024.

“We will continue to do more acquisitions to best utilize the available funds”.

IMO looks like there is good visibility now for 30%+ organic & inorganic revenue growth for the coming years, from the Corus acquisition & scale up. Other M&A would be incremental to this. Corus gross margin is 59% which is similar to 3BB (65% in Q4) so they will need to rationalize overheads in Belgium to drive profitability. Quite confident they can do it since the UK business is profitable already.

Misuse and overuse of antimicrobials in humans can occur when they are prescribed inappropriately. Inappropriate use is when antimicrobials are prescribed when they are unnecessary (such as using antibiotics, which are only effective against bacteria, to treat a viral infection), using the wrong antimicrobials (not prescribing the most suitable one for the particular syndrome), or using antimicrobials for longer or shorter than necessary.54 According to a Public Health England report in 2018, 20% of prescriptions for antibiotics in primary care in England were inappropriate.55

Better use of diagnostic tools can reduce inappropriate prescribing.56 Diagnostic tools are those which can help diagnose what infection a patient has, thereby helping clinicians determine with accuracy whether a patient needs an antimicrobial treatment and, if so, which one.57 For example, diagnostic tests can check whether an infection is caused by bacteria or by a virus.58 DHSC told us that it wanted to make sure that people who need antibiotics get them, but only those that they need, and that people who do not need antibiotics do not get them, but the diagnostic tests available are not yet adequate to allow clinicians to make that really clear distinction.59

The 2019–24 NAP had a target to be able, by 2024, to report on the percentage of prescriptions supported by a diagnostic test or decision support tool. However, this was not achieved due to continuing limitations with data, including diagnostic test results not being recorded digitally, as well as a lack of a central diagnostics data source. There is no quantitative target on diagnostics in the 2024–29 NAP.60 However, there is a commitment to improve support for clinical decision making in order to reduce avoidable use of antimicrobials, including through “adequate availability” of diagnostic tests.61

Lord O’Neill told us that although DHSC and its arm’s-length bodies have done a decent job in some key areas, they have not really progressed diagnostics. He is of the view that diagnostics should be embedded across the entire health system, which would improve productivity as well as addressing AMR.62 Dr Partridge told us that while there was progress in getting test results more quickly the NHS should be trying to move more diagnostic tests to where the patient is receiving care, and relying less on an external laboratory.63 We also received a number of submissions emphasising the need to invest further in diagnostics. These included evidence from the Cystic Fibrosis Trust, which highlighted the need to prioritise diagnostics because fast diagnosis of AMR lung infections was critical for people with cystic fibrosis.64

NHS England told us that it is more optimistic about the future use of diagnostics. It told us that there would be “an explosion” of point of care diagnostic tests as well as a very bright future for their use once the evidence base is ready. It agreed that it needs to engage more with GPs about prescribing and said it was monitoring use of antibiotics by pharmacists.65

Under the Pharmacy First scheme introduced in early 2024, patients can now consult pharmacists directly for several minor illnesses and conditions that previously required a GP visit and the pharmacist can prescribe medicines if necessary. NHS England commented that early evidence from Pharmacy First was that GPs were following the relevant protocols, and it had not seen any increase in the use of antibiotics. However, we have also seen a report of a March 2025 study claiming that patients with a sore throat are twice as likely to be given antibiotics by a pharmacist in England than they are in Wales. An author of the research study said that one possible reason for the difference might be the use of diagnostic tests for patients in Wales.66

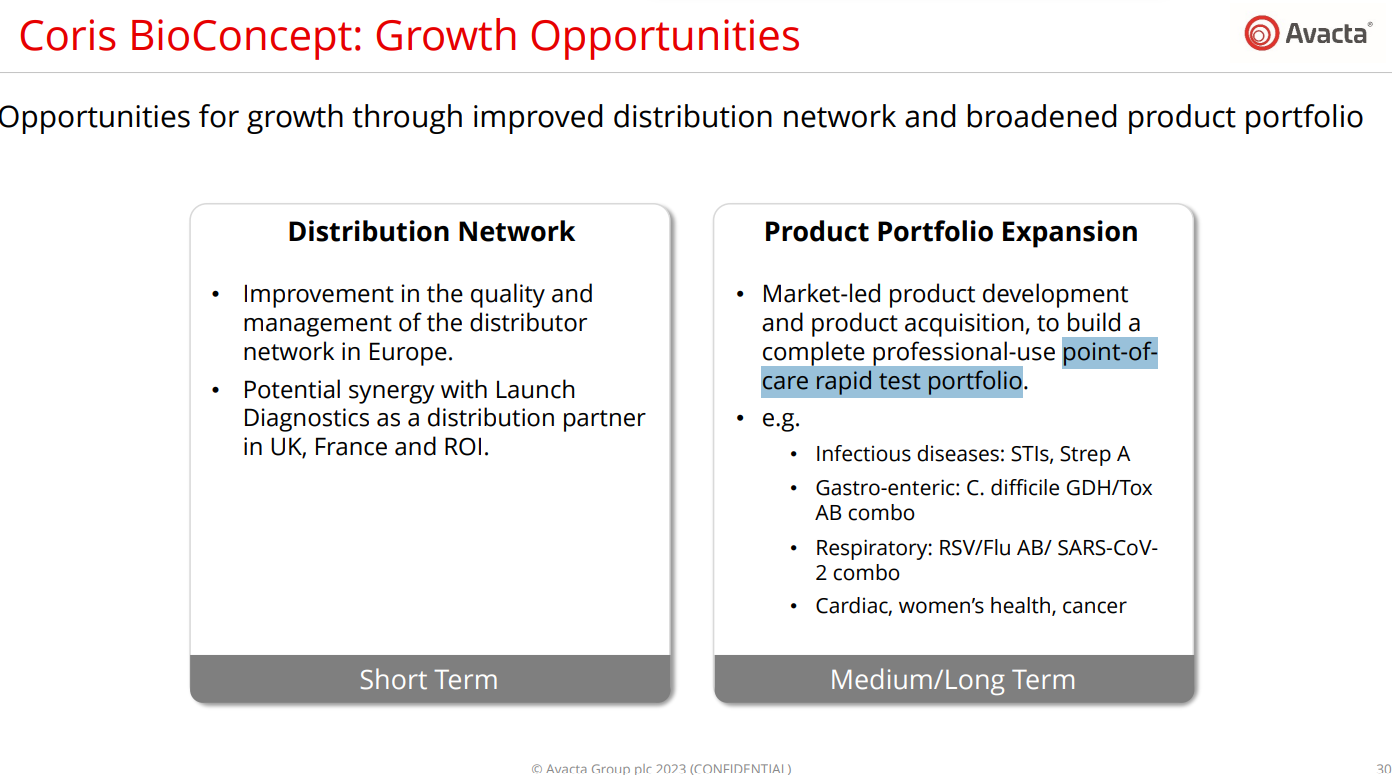

Part of the report on AMR tabled in UK parliament mainly the part relevant to 3B’s AMR business

Corus while boosting topline growth will drag down operational margins and profitability at least for another 4-6+ quarters (even if one does a linear straight line prediction taking current numbers of Corus As-Is).

Let us hope management discusses the strategy of how they plan to make Corus profitable.

Got interested in this after the recent fall. I went through the Q1 presentation and identified key triggers and monitorables to track. Fed them to Chat GPT and after multiple iterations of Q&A, made these concise and pointed notes. I found that doing this makes it easier to track and validate quarterly results to determine if 1) Topline and Bottomline are heading in the right direction, even if there are certain one-offs or valid aberrations 2) if the management’s guidance is holdign up 3) If the management is walking the talk

Debtor Levels & Credit Policy:

Target: Sequential reduction in receivables and DSO each quarter; management aims to gradually tighten credit terms.

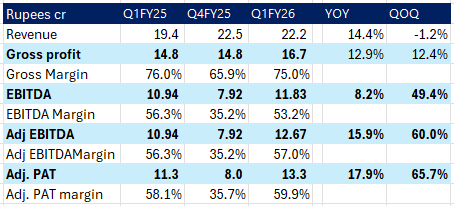

This Ebitda margin is only for the Corris business that they recently acquired. The core business will have similar margins to what they have now. The combined margins will drop slightly but not to this extent.

Started reading about this company; few things that is bothering

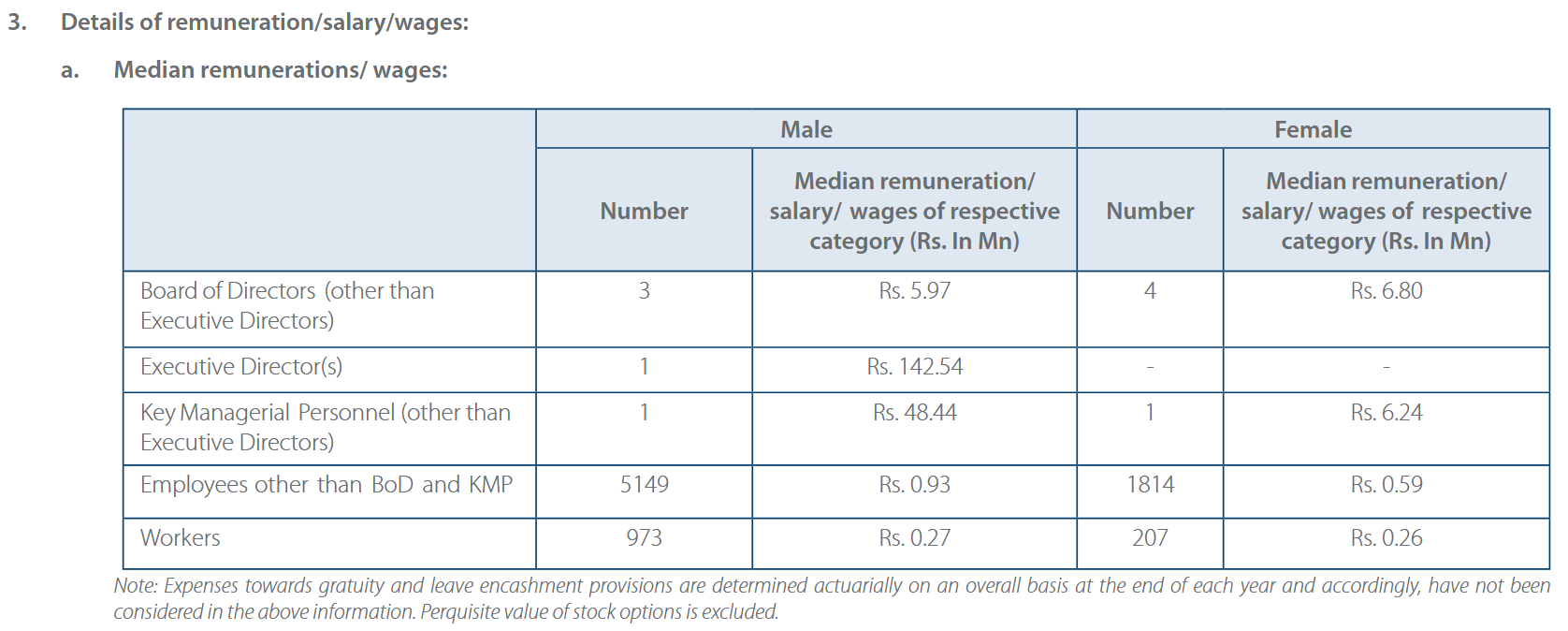

Their employee count is around 43-49 from last 6-7 years, For an R&D base company, is the employee sufficient enough to generate future growth or are they full dependent on inorganic growth, I mean you require more than 49 employee to run a 1000+ crore company specially when company is not making a digital product or service and median remuneration for employees is around 2 lakh, A R&D based company getting employee who are willing to work for Rs 16600 per month seems bit off to me, any member knows about it

The employee cost and employee strength does not make sense. Also their UK subsidiary also must be having some employees which would be paid in pounds (read higher pay). Even after all this the average pay comes around 2-3 lac per head including around 1 Cr package of the KMP (Average would be a lot lower if we remove KMP salary).

I have highlighted these things in my earlier post. It seems really fishy how the company is managing the business with so few and underpaid employees. Are they Subcontracting their operations? Will have to check RPT for that.

In the concall, the promoter highlighted that manpower costs in India are relatively low, but cautioned that future salary increases could lead to margin contraction. In India, sales, marketing, and technical support have been outsourced to VGT, and since this is contracted work, it is recorded under other expenses rather than employee costs. The promoter also mentioned that packaging of testing kits is handled by labor from the agro-chemical division.

That said, there still remains some gray area in how manpower-related expenses are reflected in the financials.

Detechgene, a Cologne-based biotech startup, recently secured €3.2 million in its second funding round. The company is still at a very early stage, with a limited product portfolio focused on mobile molecular diagnostics. Its post-money valuation is estimated to be in the range of €10–15 million. This benchmark may serve as a useful reference point when assessing the valuation of Coris, particularly if Coris operates in a similar domain or stage of development.

Given that 3B Blackbio DX is a research-intensive and an asset-light business, it is important to dig deeper on the issue around employee cost and headcount. There are 3 very valid concerns raised in this thread that confused me more than others:

Why has the employee count remained stable despite the superlative business growth?

Why is the cost per employee unchanged across the years?

Why is the cost per employee and number of employees so low given the high R&D capabilities/achievements claimed by the company?

I’ll share what I have learned about this subject in the last few days.

TL;DR version for those who just want the gist:

Director’s Report only covers the standalone entity (ag-chem piece) till FY23.

So employee data we are looking at in Director Reports is not a reflection of consolidated business growth over the years.

Stagnant employee count is in synch with the stagnant ag-chem business over the years.

AR 2024 is the first report after amalgamation of ag-chem with diagnostics divisions. Data in this AR supports the above two points and provides insights into employee costs of molecular business.

Analysis of data from AR 2024, LinkedIn and Perplexity broadly justifies the average salaries at 3B

Higher women participation and Bhopal-based operations also explains the salary levels at 3B

Headcount and cost figures for 3B Blackbio are comparable with that of peers.

Conclusion: After adding this context, data related to employee cost and headcount is justified.

Disclosure: Invested. Biased. No transaction in last 30 days.

Read on for the longer version. I’ll try to keep it crisp.

1. Director’s Report only covers standalone business

All the employee-related data we are looking at are covered under the Board of Director’s Report in each AR.

The reporting requirements of Director’s Report are covered under the provisions of the

○ Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 (link),

○ Companies (Accounts) Rules, 2014 (link),

○ Section 197 of Companies Act, 2013 (link) and

○ Section 134 of Companies Act, 2013 (link)

When read together, professional experts interpret these provisions to require that companies prepare their Director’s report based on standalone financial statements (link, link and link).

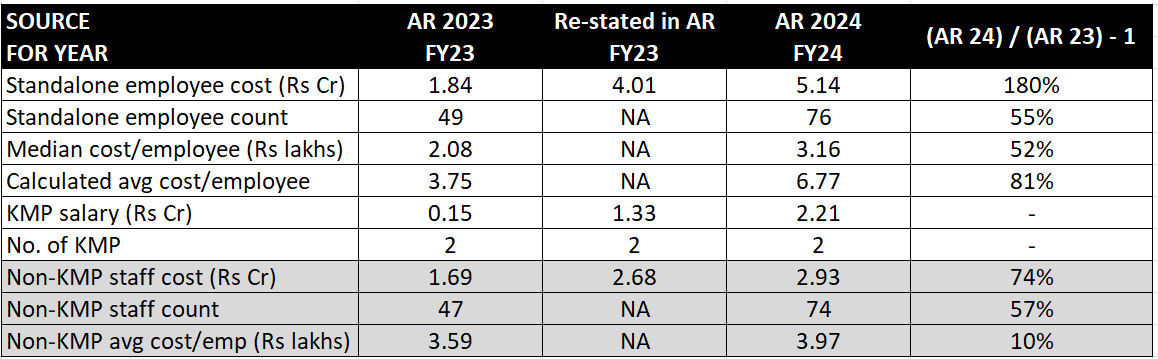

Hence, the employee count and median remuneration figures prior to FY24 pertain to the erstwhile standalone business of 3B Blackbio Dx (i.e., Ag-chem business of erstwhile Kilpest India Ltd)

That is the reason why we don’t see any meaningful increase in employee count or median remuneration from say FY17 to FY23, despite strong revenue growth over the years

Note: Standalone sales only pertain to the agrochemical business or Kilpest; cost/employee = staff cost/staff count x 100

3. Director Report post amalgamation gives a clearer picture

The amalgamation between 3B Blackbio Biotech India Limited and Kilpest India Limited was effective in FY24 (approved on 9th August 2023). The amalgamated entity was named 3B BlackBio DX Limited.

After the amalgamation, the standalone business includes erstwhile ag-chem business along with the Molecular diagnostic, excluding TRUPCR® Europe (UK Subsidiary).

Hence, the AR of FY24 shows a sharp increase in the standalone employee cost, headcount and median cost/employee. In fact, salary cost for FY23 has also be restated upwards from Rs 1.81 cr to Rs 4.01 cr.

This further confirms the fact that prior years’ figures were not reflecting the progression of the molecular diagnostic business.

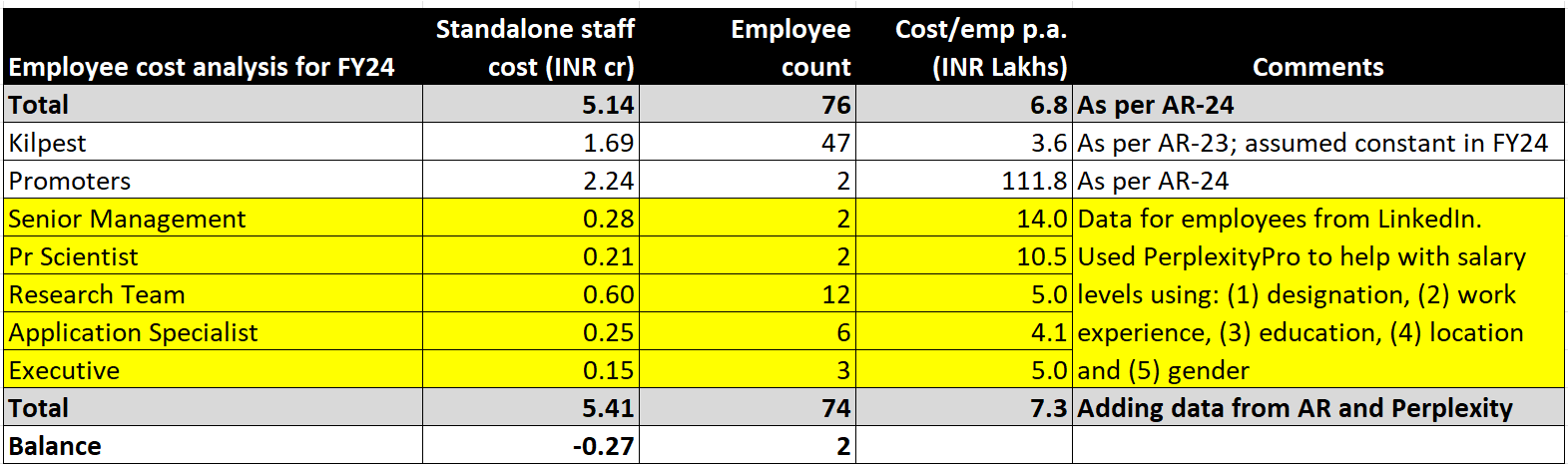

4. Data from AR 24 + LinkedIn + Perplexity suggests that cost/employee is fair

Sifting through LinkedIn profiles of 3B Blackbio employees shows that there are 14 members in the scientific research team, 6 application specialist and 2 senior management executives. 14 of the 25 employee profiles were women.

I used Perplexity to estimate the salary of each employee based on their (1) designation, (2) work experience, (3) education, (4) location and (5) gender.

After adding all the data, we get a difference of Rs 27 lakhs (5% of total employee cost).

This difference can also be explained to some extent by possible double counting. Some senior employees who are showing 3B Blackbio as their employer today, at one point were employed by Kilpest.

However, after looking at these figures, the reported employee costs and salary/employee in 3B’s Annual Reports make more sense now and do not seem completely out of whack.

5. Higher women participation + Bhopal-based operations

Of the 14-member research team bios on LinkedIn, 12 are women. Of the total 25 employee profile on LinkedIn, 14 are women i.e., 56% of the total workforce in the molecular diagnostic division (which in turn accounts for more than 80% of the total staff cost).

As per data from some companies like Syngene & Metropolis (snippets below), there are instances where women on average draw lower income than their male counterparts.

I admit that that is a gross generalization. But I am merely stating some facts as they are, if it explains low median remuneration at 3B to any extent.

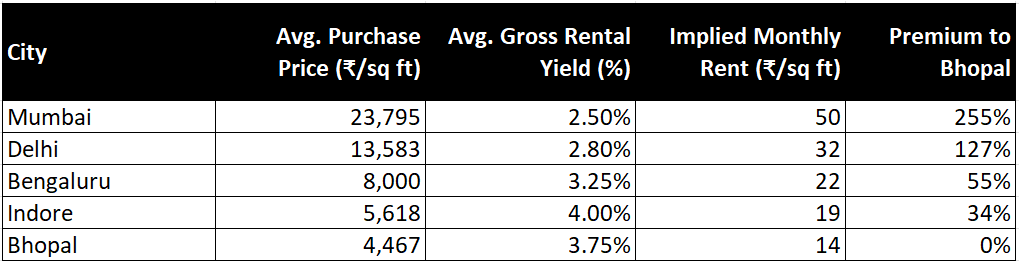

Furthermore, 3B predominantly hires and employs staff in Bhopal. Hence, salary levels are expected to be lower compared to cities like Mumbai, Bengaluru and Delhi.

Discussion with a few friends from Madhya Pradesh also gave me the same understanding; that given the lower real estate cost and other cost of living, salary levels are lower in Bhopal.

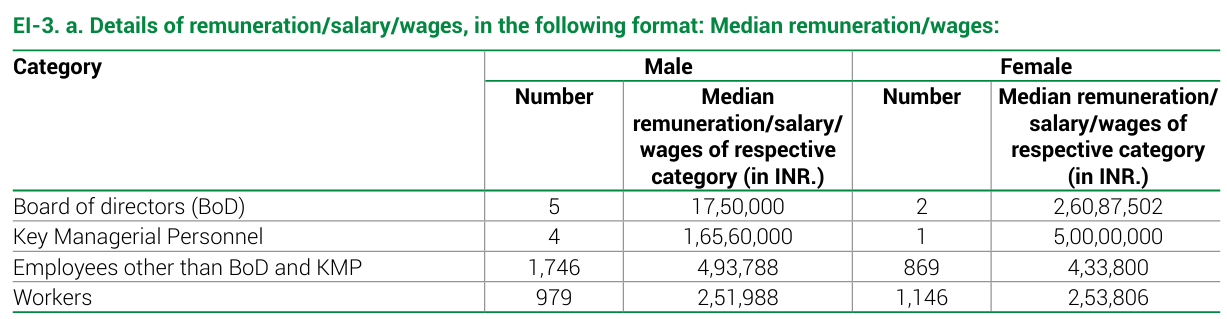

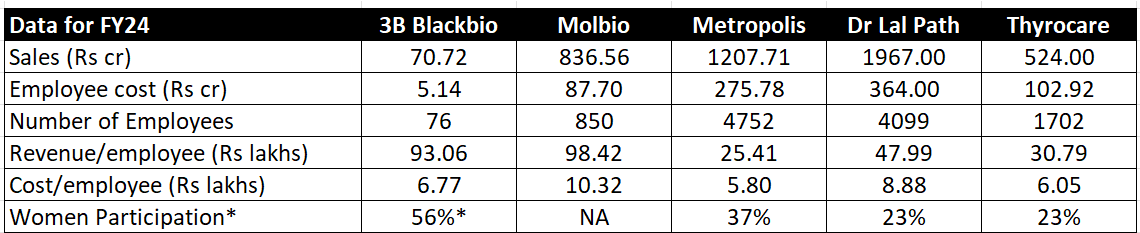

I compared the employee-related data with other diagnostic companies. |

Before going through the comparison, let us keep in mind that 3B (1) has a higher women participation in the workforce and (2) has Bhopal-centric operations |

Having said that, figure of cost/employee is comparable with most firms and revenue/employee is comparable with Molbio (which is also into molecular diagnostics).|

*Source: Annual Reports; Molbio DRHP and LinkedIn for 3B Blackbio

Conclusion:

Thanks to the concerns raised, I learned more about the disclosure requirements in Annual Reports.

When we put all the employee-related data in context of (1) which entity each AR data pertains to, (2) the geographic base of operations and (3) demographic mix of the work-force, the figures make sense.

Comparing the data with some competitors provides additional comfort.

Will update the thread with any additional findings on the subject

Disclosure:

I have tracking position in the company (~1% of portfolio). No transaction in last 30 days.

I am not a SEBI registered advisor or analyst. This is not a recommendation.

The above is purely my opinion from reading the information in the public domain. I wanted to share the data and my analysis with the community for improving our collective understanding.

I have made errors in the past when analyzing, forecasting and valuing businesses. Kindly rely on your own analysis while deciding the next course of action.

I just have one question, can the company sustain current margins or we can face mean reversion since the margins are at 53% now! Anybody has any insights,

in my personal view margins will take a hit at consolidated level due to the fact that acquired business is not profitable as yet. as the unit economics of acquired business improves, margins should start improving. To some extent price has cooled off with market factoring margin decline.

How much of margin hit and by when things can improve, you better write to company management to get an indicative answer.

Disclaimer: Invested, biased, no buy, sell or hold recommendation. do your own due diligence.