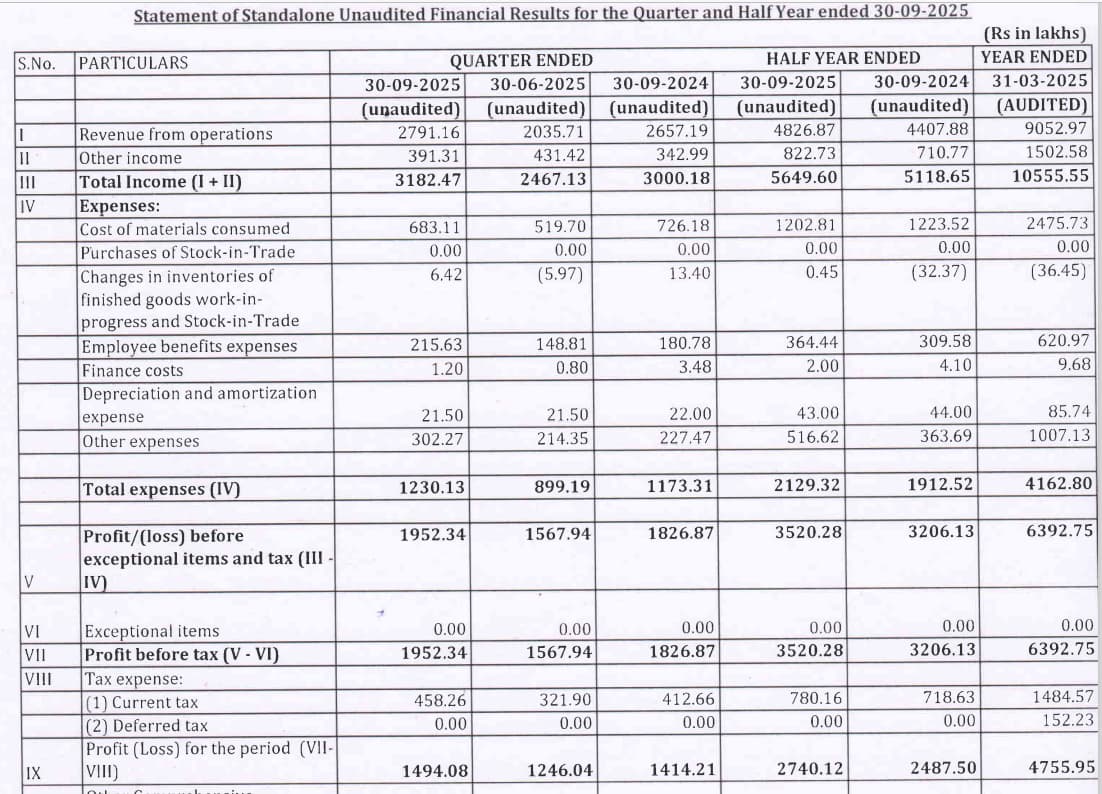

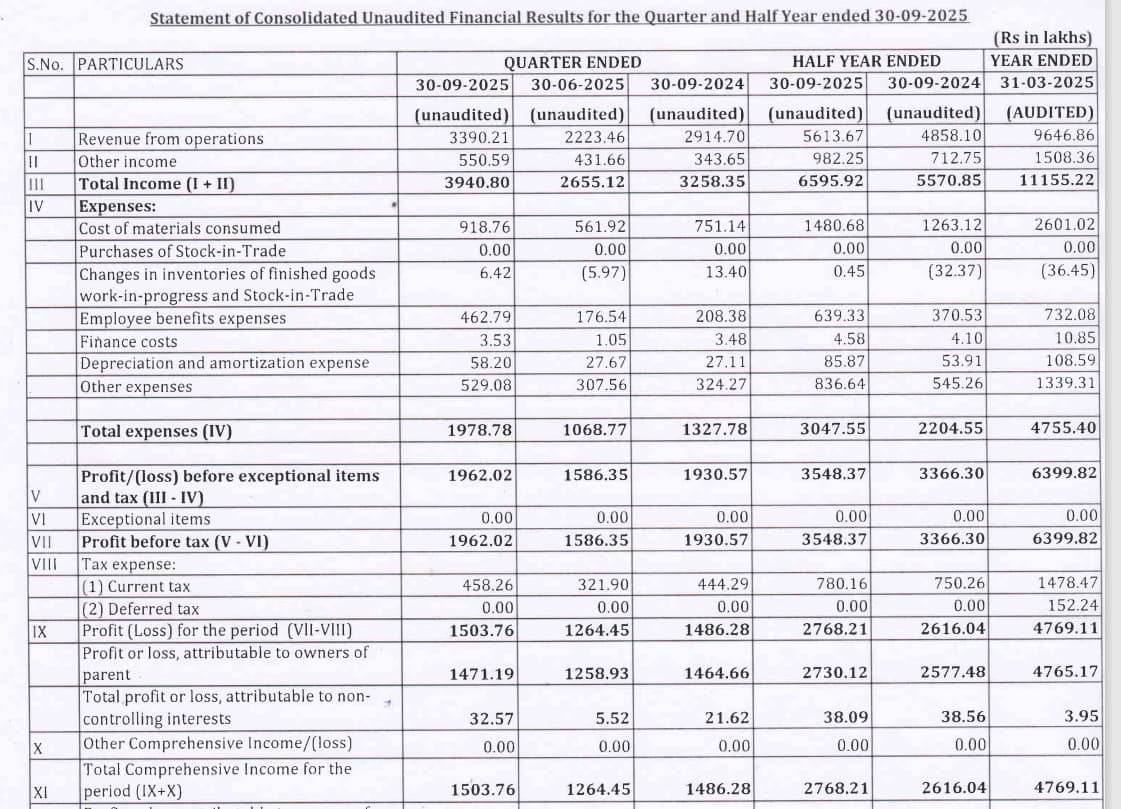

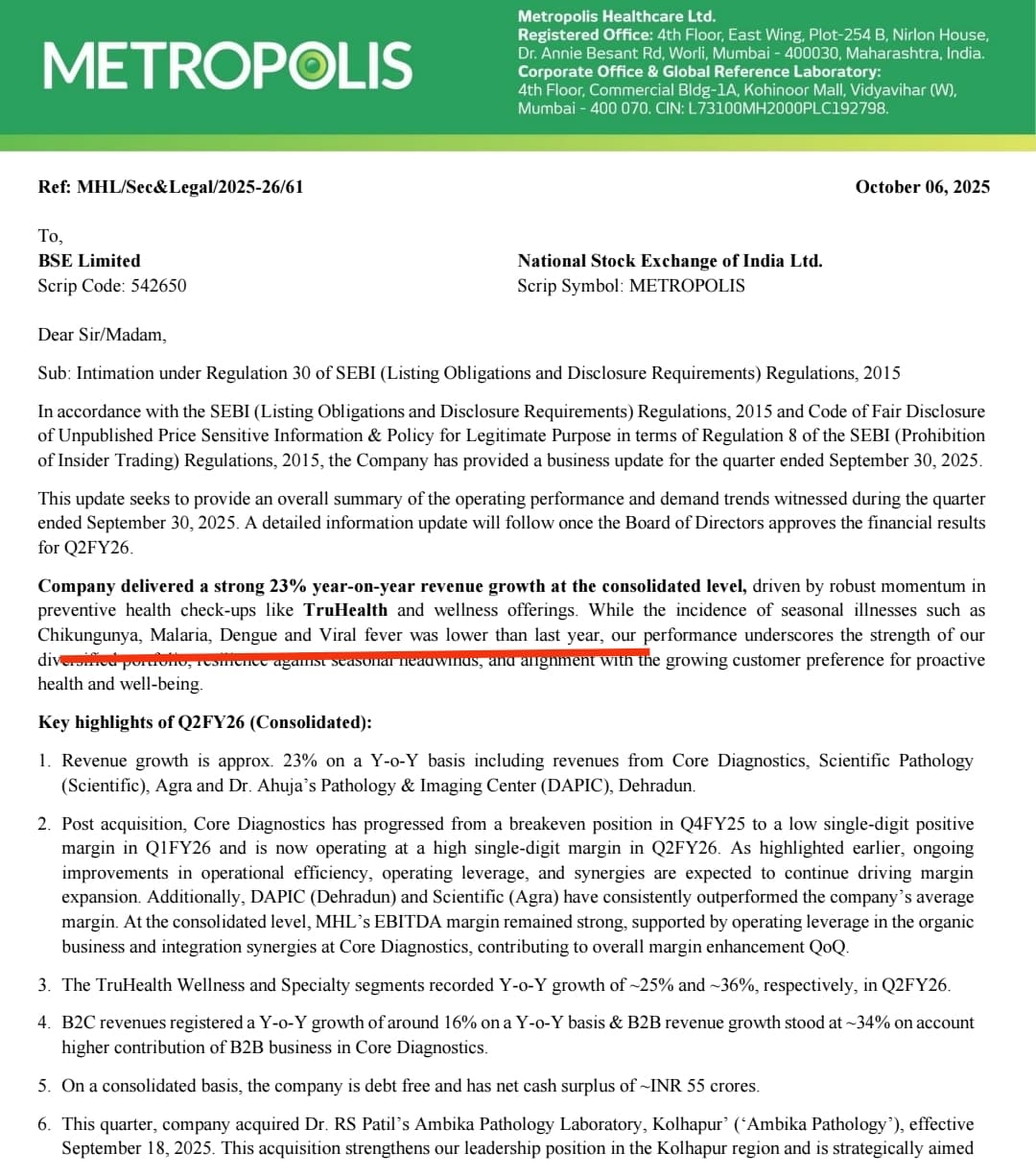

This was business update of metropolis

Probably should expect muted numbers for 3BBB YoY

Molbio diagnostic has filed DRHP few months back. Link here. Company is backed by temasek & Motital Oswal PE. To me it look like competitor company of 3B blackbio but not sure why they havent shown them as peer

SEBI mandates the companies to disclose the accounting ratios of peer companies. But it doesn’t mandate exactly what peers must be used. Molbio will definitely include higher valuation peers to justify their valuations.

Quick read through initial pages of DRHP suggests it is in early stages compared to 3B. Largely business comes from central and state governments at this stage and up to 60% revenue is from TB detection.

In addition, it has IP license from Bigtec (essentially a subsidiary of the company), for micro PCR technology for detection of diseases across a spectrum of diseases.

Based on cursory analysis, 3B looks ahead at this stage. Need to study more on this for firming up a view.

I was bit puzzled when coris had 58.7 % gross margin and negative ebitda.I was wondering if employee cost is not included in grossmargin.we know the employee cost being high as mentioned by mgmnt. But marketing and R&D expense is included in EBITDA calculation. I guess R&D expense will be expensive component which is making it negative.

AI response : Coris’s 58.7% gross margin means that for every €1 in sales, it keeps nearly 59 cents after paying for the materials and labor required to create its diagnostic products.

Negative EBITDA: Weakness in operating expenses

“we see EPS growing at 20% for the coming three years” : commentary on 3BBDx by Seven Canyons Advisors.

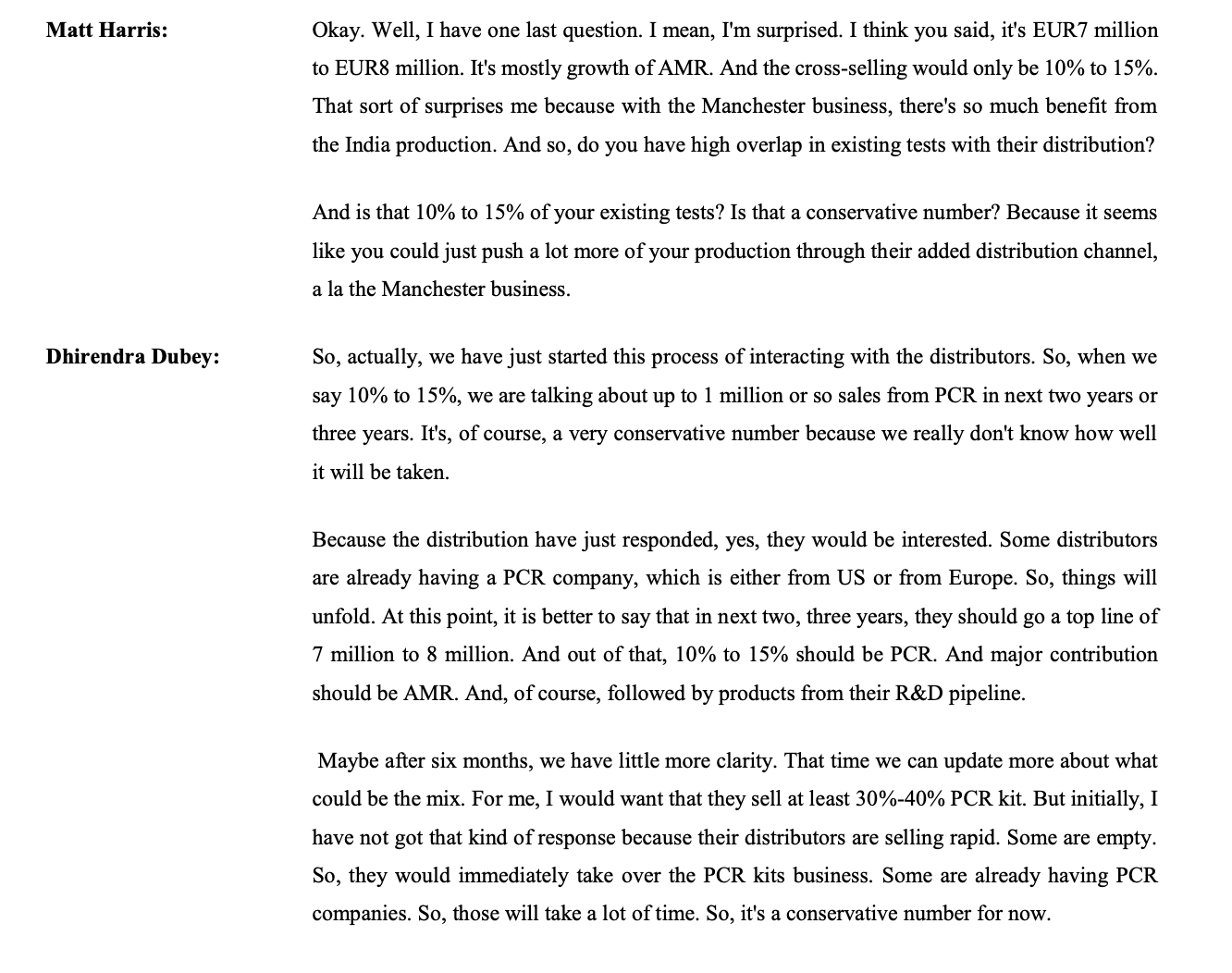

The reason for growth mentioned in report were asked by them in concall and i understood management clarified none of those are in plan presently.(i.e. 1. mfg in india and supplying to belgium or 2. cross selling a significant protfolio. Management said 10 to 15% cross selling maybe in next year or so. 3. 20% profit growth for next 3 years. Although 3b as stand alone may acheive but consolidated profit growth will be much lower due to unprofitable operations at coris for next few years)

This means that this letter to be not taken at face value.

Disclosure : significant holding.

Decent numbers.

Revenue should significantly start picking up from Q3.

Few things I liked from ppt-

This was an awesome quarter in my books - especially given the really tough YoY comps from Q2 FY25 which the market didn’t expect they could meet/beat which is why the stock has corrected so sharply. Few things that stood out to me -

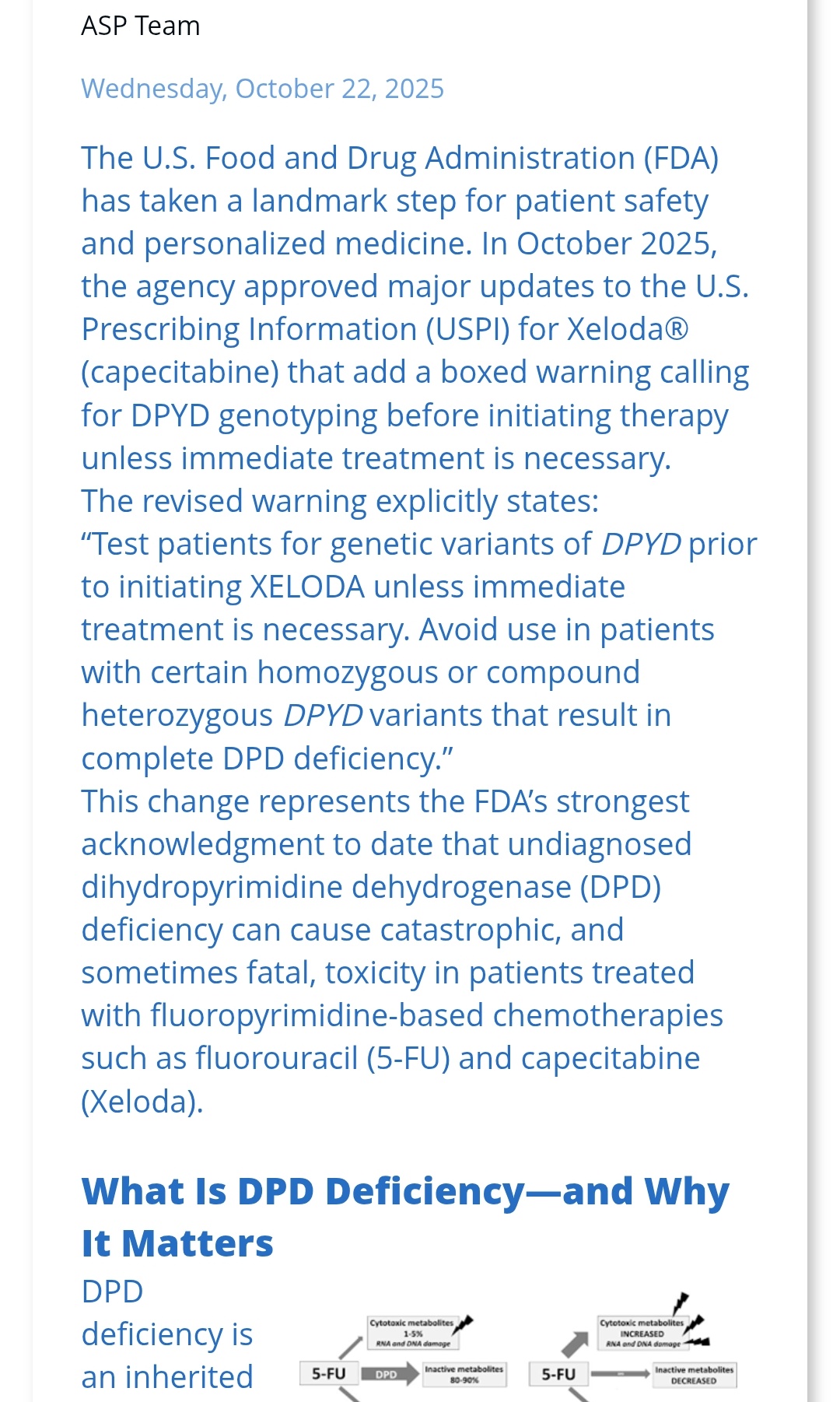

Another interesting development that can bode well for 3B is FDA mandating DPYD testing for Xeloda. Indian authorities may follow suit at some point.

A Milestone for Patient Safety: FDA Adds DPYD Testing Requirement to Xeloda Label BLOG

Investor presentation. There is no mention of NSE listing

https://www.bseindia.com/xml-data/corpfiling/AttachHis/351b9755-ddaf-4a3c-967e-07f8f28e5338.pdf

Coris has launched it’s new PCR brand “Diagentis” beginning the cross sell of 3B BlackBio products to its distributors. This strategy was mentioned in the Q1 investor call.

Feels like the stock is completely disconnected from fundamentals recently. At some point today this was trading at less than 800 cr enterprise value (market cap minus 230+ cr cash balance) which is a 50% discount to other Dx company multiples.

Company should grow revenues 50% this year and PAT by 15-20%, with further profitability acceleration next year once Coris turns profitable.

I made a simple DCF valuation model assuming 20% core DX revenue growth (India + UK) and 10% Coris growth. EBITDA margins are aligned with management’s guidance - 55% for core business, 10-15% for Coris post FY27. For simplicity’s sake I ignored any dividend or acquisition assumptions which results in the cash balance growing quite a bit. I see a clear runway for 20%+ PAT growth as they expand globally with very high ROICs while remaining debt free and requiring no equity dilution. Fair value per share comes to 3,283 using a discount rate of 15%. One can justify a further reasonable valuation discount for lower liquidity/ small cap risk etc. All the assumptions can be adjusted in the Assumptions tab. Would appreciate any feedback here or via DM to poke holes in the thesis.

The price action was broadly in line with expectations following management’s announcement of the Coris acquisition. Because Coris operates at structurally lower margins, its consolidation is margin-dilutive for the overall business. Markets typically derate companies undergoing such transitions.

A similar pattern was evident in Sanghvi Movers, where the stock’s valuation compressed from a P/E of roughly 40x to about 14x because management decided to enter Wind EPC business which is lower margin business but higher ROCE business. In the same vein, 3B has derated from 41x to 21x and now appears to be entering a value-buy range.

Sanghvi Movers works in cyclical sector so 14x PE is reasonable for this but 3b blackbio doesn’t works in cyclical sector it works in healthcare sector so it’s reasonable PE must be in between 40x to 60x and reasonable price in between 2400 to 3600.

I’m my opinion there are few reasons plaguing the stock:

1)low liquidity, can go up down easily

2)growth projected by management, for core business was around 20% which is less. Usually market expects small/microcap companies to grow at a much higher pace.

3)earning fluctuates a lot(seasonal)

4)management in general is conservative

5)works in a niche sector with less TAM and big global competitors.

We can talk in length about Amr, NGS, digital pcr but the bottomline is it’s not bringing significant revenue.

Very detailed article on the company:

Any thoughts on how the EU FTA can impact 3BB. This is what I got from Gemini Pro:

—————–

Based on the detailed provisions of the India-EU Free Trade Agreement signed on January 27, 2026, here is the exclusive “Bull Case” for 3B BlackBio DX.

Molecular diagnostics manufacturing is chemical-intensive. 3B BlackBio currently imports high-grade enzymes, buffers, and master mixes, often from European suppliers (like those in Germany/Switzerland) or their global hubs.

The Positive: The FTA eliminates import duties on Chemicals (currently ~10-22%) and Specialized Plastics (currently ~10-16.5%).

Impact: This lowers the “Landed Cost” of raw materials. Since 3B BlackBio’s selling price in India is stable, these savings on the input side will directly expand their Gross Margins.

To stay competitive against global giants, 3B BlackBio constantly upgrades its R&D and manufacturing infrastructure. The best molecular testing machinery (PCR machines, sequencers, automated liquid handlers) comes from Europe (e.g., Qiagen, Roche, Eppendorf).

The Positive: The FTA slashes duties on “Optical, Medical, and Surgical Instruments” (currently up to 27.5%) and “Machinery” (up to 44%) down to 0%.

Impact: Future capacity expansions or R&D lab upgrades will be significantly cheaper. This lowers the capital intensity of growth, improving their Return on Capital Employed (ROCE).

Currently, 3B BlackBio serves Europe largely through its UK subsidiary, TRUPCR Europe Ltd. Post-Brexit, moving goods from India $\rightarrow$ UK $\rightarrow$ EU created friction (double paperwork/tariffs).

The Positive: The FTA grants 0% duty access for Indian medical devices entering the EU-27 directly.

Impact: 3B BlackBio can now ship directly from its Bhopal facility to distributors in France, Germany, or Italy duty-free. This improves price competitiveness by ~5-10%, allowing them to undercut Chinese rivals who still face EU tariffs. It transforms their business from “UK-centric” to “Pan-European.”

European diagnostic giants are actively looking for “China+1” suppliers for white-label manufacturing.

The Positive: With zero duties, 3B BlackBio becomes an attractive CDMO (Contract Development and Manufacturing Organization) partner for European brands.

Impact: A European company can now outsource the manufacturing of a specific PCR kit to 3B BlackBio in India and re-import it to Europe with zero fiscal penalty. This opens up a new B2B revenue stream beyond just selling their own “TRUPCR” brand.

| Driver | Old Regime | New FTA Regime | Benefit to 3B BlackBio |

|---|---|---|---|

| Raw Materials | 10-20% Duty | 0% Duty | Immediate Gross Margin Expansion. |

| Machinery (Capex) | ~25%+ Duty | 0% Duty | Lower cost for R&D/Factory upgrades. |

| EU Market Access | 2-7% Duty | 0% Duty | Price competitiveness vs. Chinese kits. |

| Supply Chain | Complex (via UK) | Direct | Faster logistics & lower friction costs. |

I think the actual gains or loses is a bit tricky to determine. We have to consider that 3BBB now has a EU subsidiary.

Gains :

3BBB can sell kits in the EU at lower tariffs under the trade deal, but the catch is that the EU still requires very strict regulatory compliance. To meet these standards, manufacturing costs will likely increase.

AMR and other products manufactured at the CORIS facility could be sold in India. But I feel some CORIS products are already being manufactured in India, because I can see these products listed on 3BBB’s product pages. At the same time, India doesn’t show up as a client on CORIS’s website.

Loses:

Competition could increase as more EU diagnostic companies find it easier to enter India.

In the last concall, management said they are not really facing tough competition from MNCs because those players usually don’t cut prices. But with tariffs coming down, this might change, and EU companies could start pricing more aggressively.

Regarding your point on import of enzymes, 3BBB mention they have in-house enzymes production, you can see it in the 3BBB site

Overall I still don’t know how things will pan out.