The guidance of 15-20% is for Indian business.

But yes they have reduced guidance for UK business from 40% to 20-25%.

Im not sure if exports is included in this guidance.

1 Like

PPT for Q3 mentions guidance for India MdX business as 20-25%

“The Total Addressable Market (TAM) in India for Molecular Diagnostics (MDx) is between 300-400 Crores out of which we have a share of 12% - 15% and are the market leaders. The industry is expected to grow at 8% - 10% for the next few years due to adoption of MDx by more labs & hospitals. Considering this, we will continue to grow at a rate of 20% - 25% for this year which is in line with our expected growth.”

But the ppt this time (Q4) says

- The Total Addressable Market (TAM) for Molecular Diagnostics (MDx) in India is estimated at approx.₹350–450 Cr.

- We hold a 12%–15% market share, positioning us among the market leaders.

- The MDx industry is projected to grow at 8%–10% CAGR over the next few years in India due toincreasing adoption across diagnostic labs and hospitals and government projects.

- While this growth is attracting increased competition, we are hoping to grow at 15%–20% for FY 2025–26, backed by our extensive product portfolio and strong market presence over the years and high-qualityproducts well accepted by the customers.

So India Mdx guidance has been reduced

10 Likes

in India Business they had exceptional income in Q2 and Q3. this may not come in this year. Hence i think they have reduced the range. Overall, they have always tried to temper expectations. Always been prompt to highlight one time gains.

4 Likes

Continuing to make inroads into Europe through partnerships

14 Likes

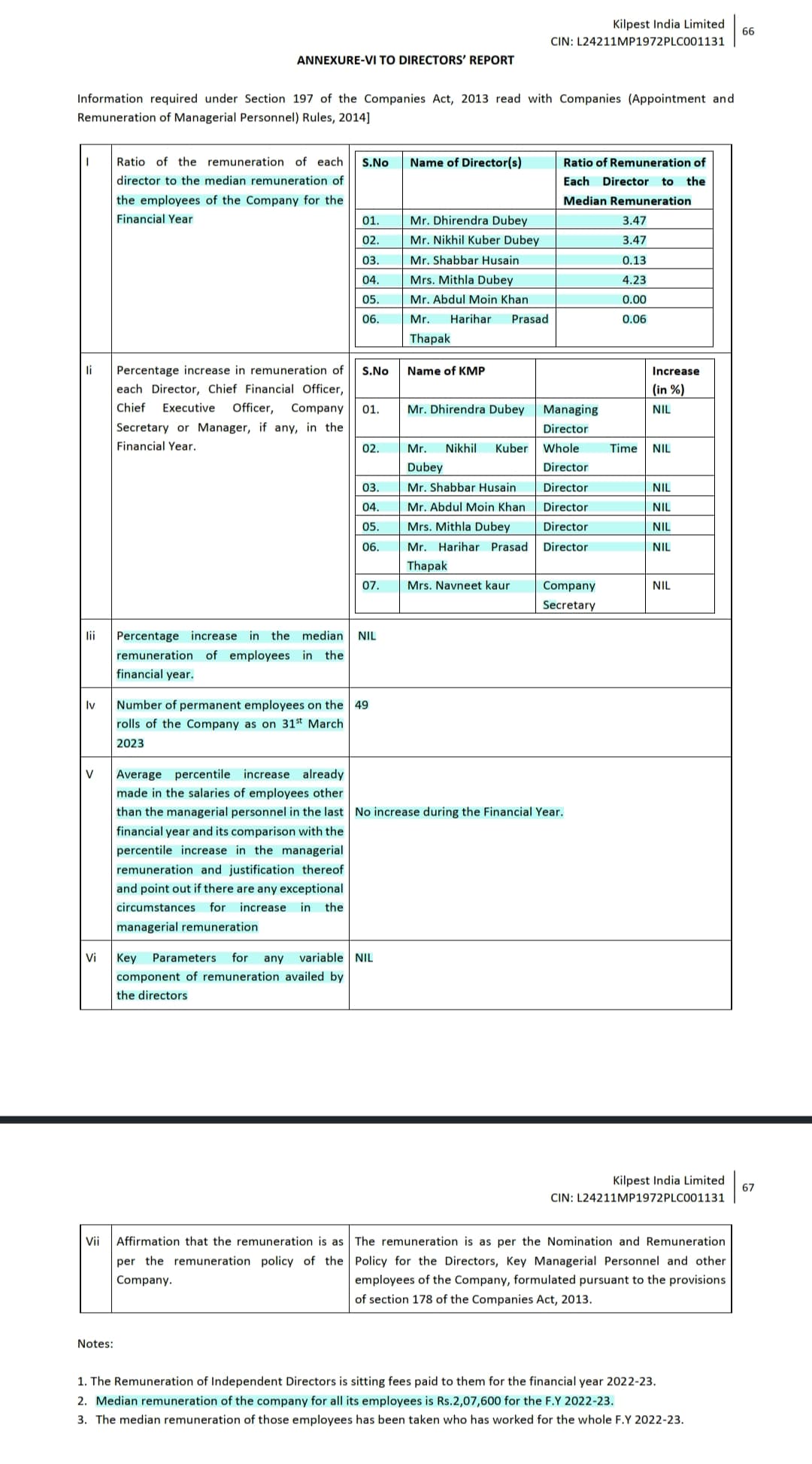

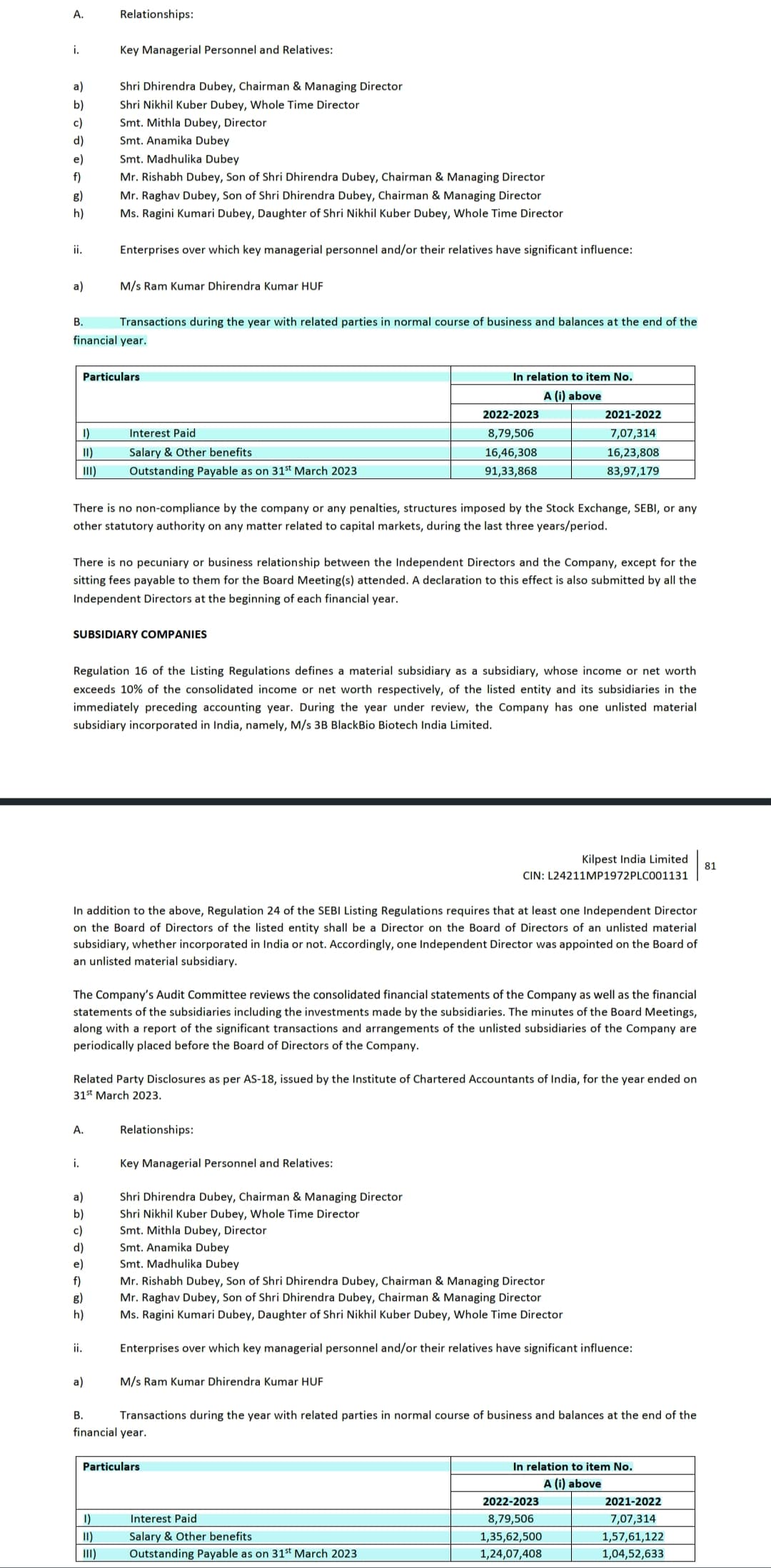

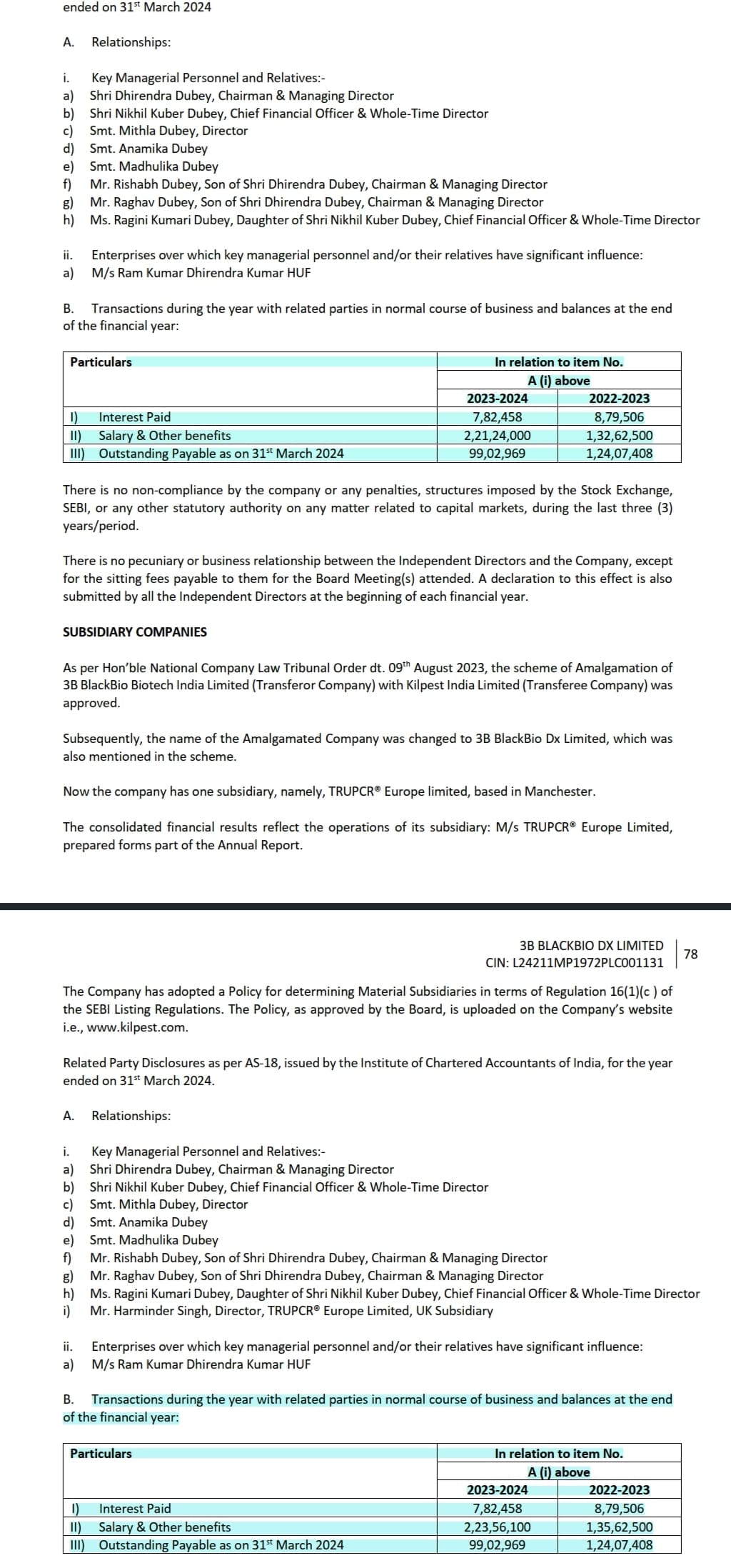

I was going through 2024 and 2023 annual reports and following things are confusing me (refer highlighted portion):

Year Apr 22- Mar 23: AR 2023

Kilpest was merged in Nov 23. Only one material subsidiary was there namely 3B Blackbio biotech india ltd

- The promoter group salary on company level is 16.46 lac while on subsidiary level it is 1.35 Cr. How come such variation?

- In table denoting RPR, interest is paid to promoter group but still the payables are increasing from 83.97 to 91.33 lac at company level and from 1.04 Cr to 1.24 Cr at subsidiary level. Why the payables are increasing after interest payments? Are there any other payables? If so where can i find those details?

- The average increase in employee salaries is NIL. The average increase in employee salaries except KMP is also NIL? How come it is? Never seen a company not increasing employee salaries. Is it inflation proof? Also with 49 employees, the average salary is 2 lac which is very less as per industry norms. There is no department wise bifurcation given for the employees.

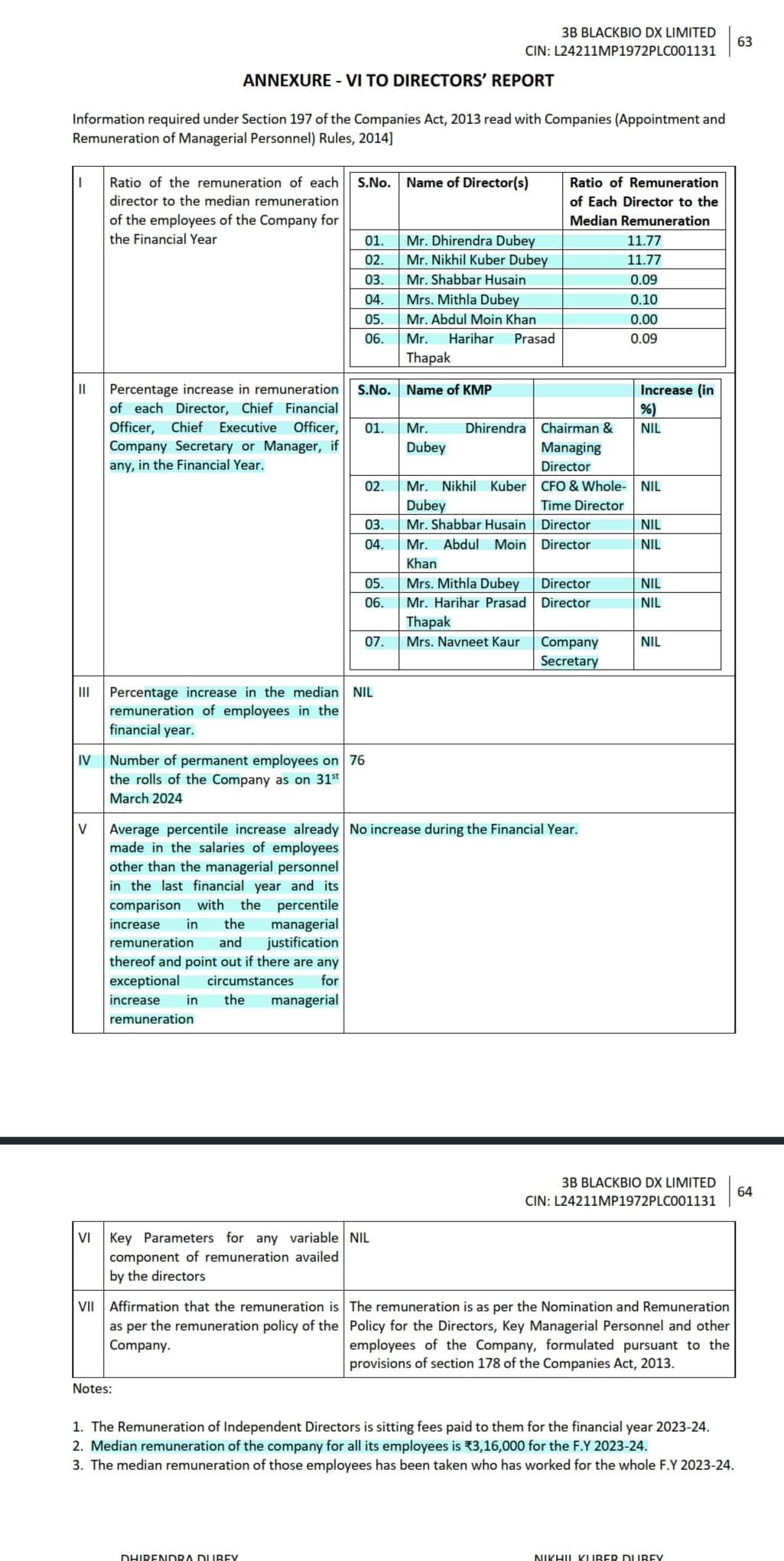

Year Apr 23- Mar 24: AR 2024

After merger, there is only one material subsidiary namely, TruePCR Europe.

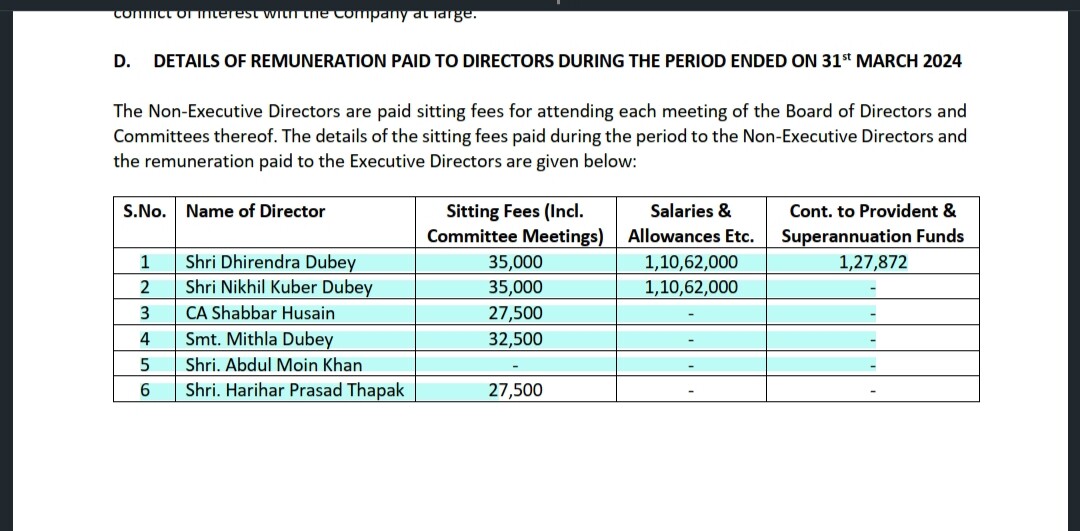

- The promoter group salary on company variation 2.21 Cr while on subsidiary level it is 2.23Cr. In FY 2023, it is 1.32 Cr and 1.35 Cr respectively. Clearly the salary of promoters have increased heavily. But in remuneration table, it shows the average increase in employee salaries is NIL. The average increase in employee salaries except KMP is also NIL? How come it is? Again the company is not increasing employee salaries. The average salary is 3.16 lac which is clearly more than 2 lac in previous FY but the salary increase is NIL in the remuneration table. Very confusing…

- The company level salary has increased from 16.46 lac to 2.21 Cr. On subsidiary level from 1.35 Cr to 2.23 Cr. No explanation as to why such astronomical raise?

- Promoter salary to median salary is 3.47 in FY 2023 and 11.77 in FY 24 which also indicates increase in year wise salary.

Pardon my mistakes if any.

Dis: studying with no investment as of now.

8 Likes

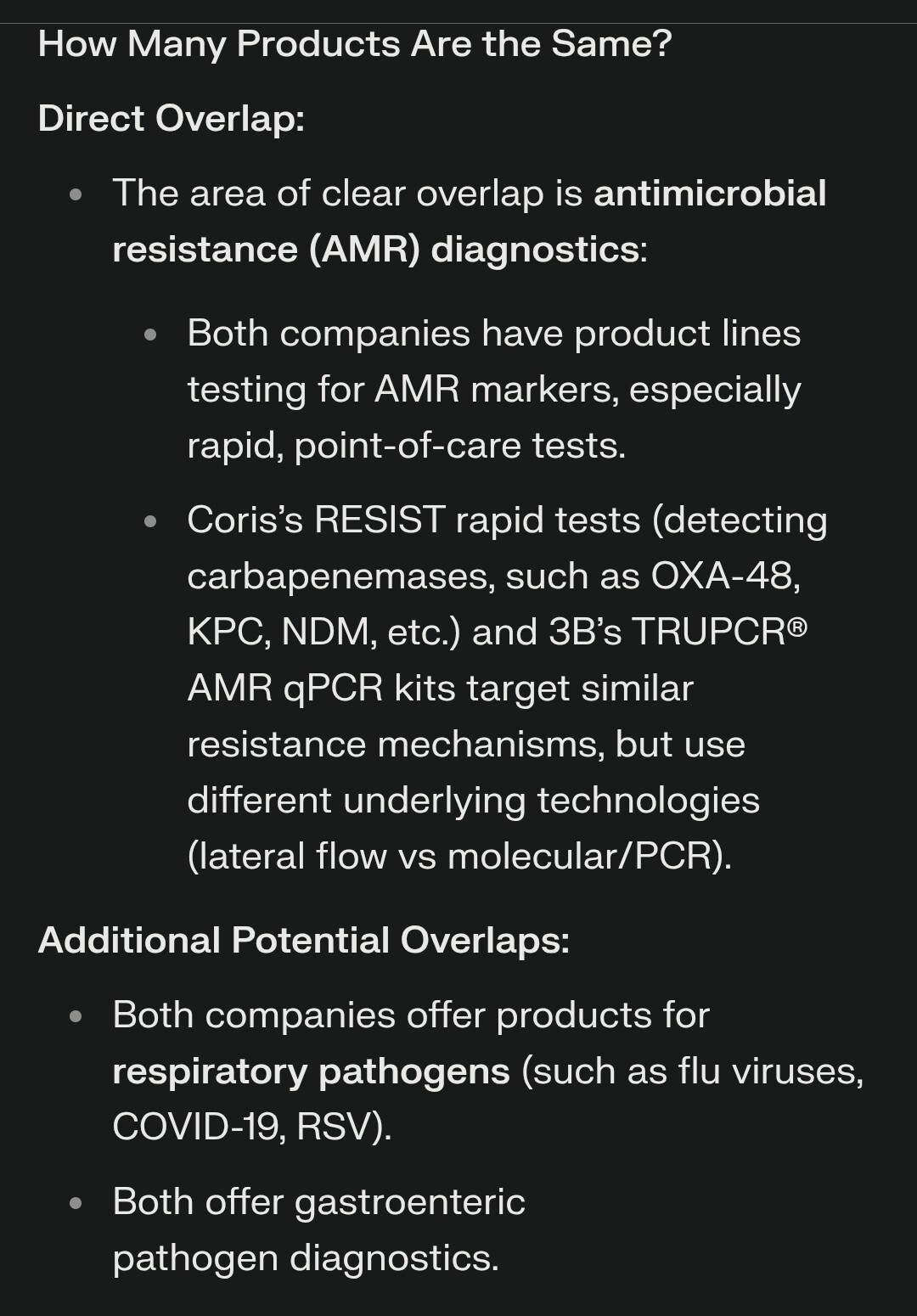

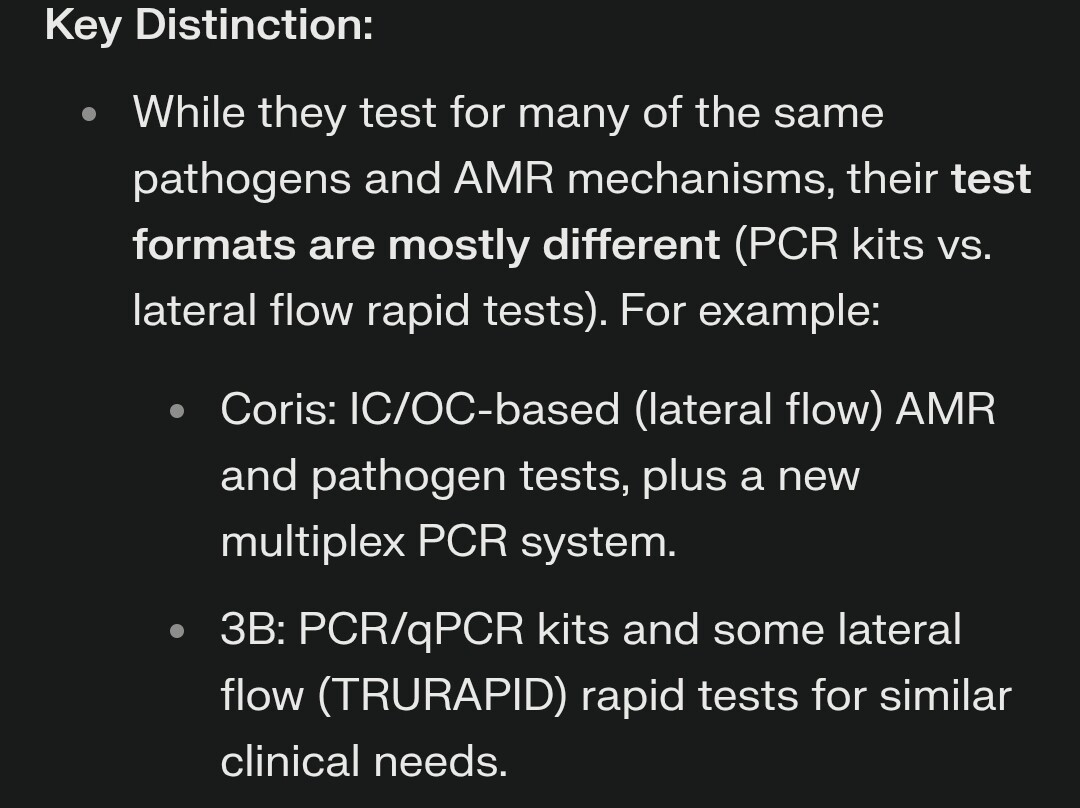

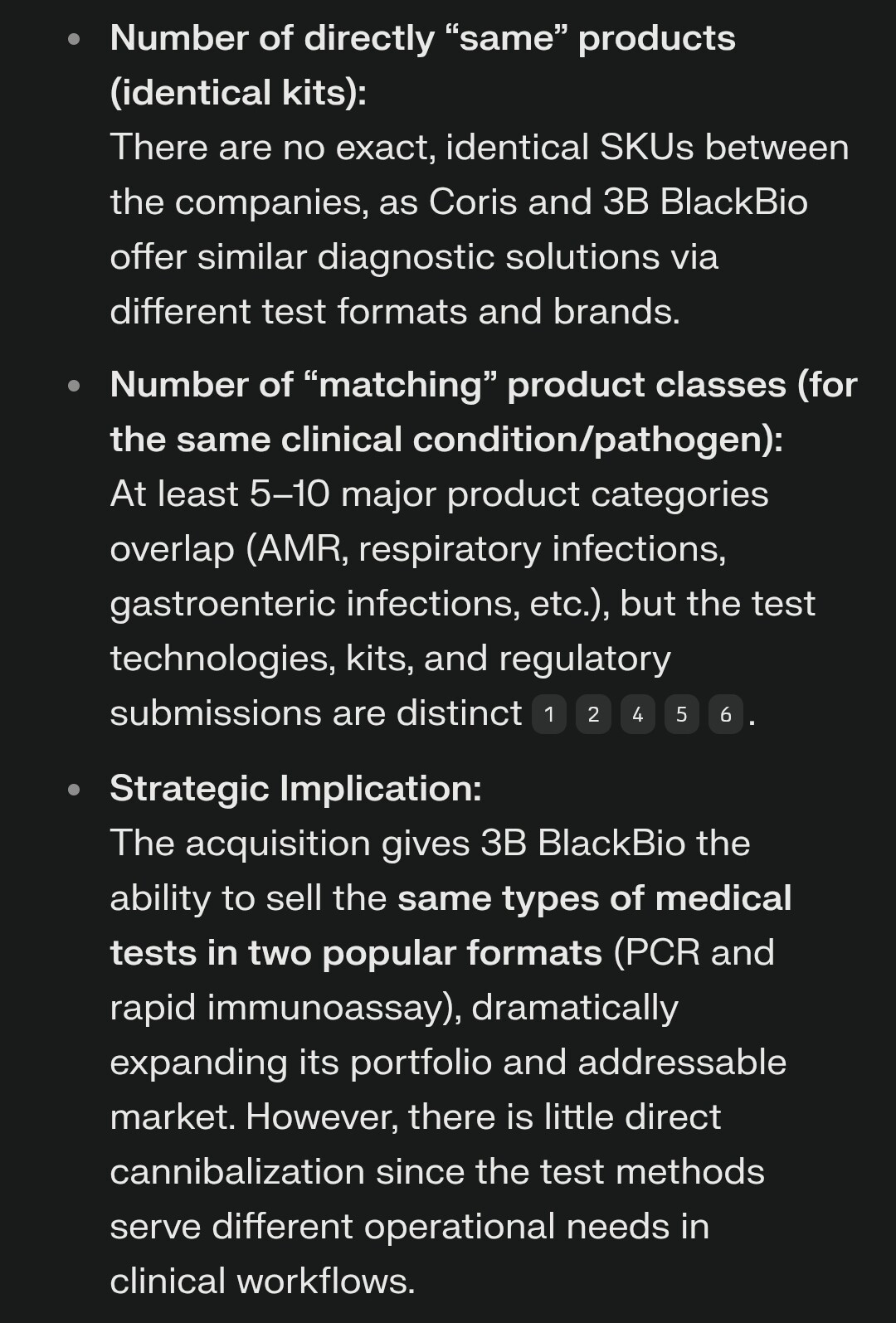

3B BlackBio Dx Ltd., along with its subsidiary TRUPCR® Europe Limited, will acquire 100% of Coris Holding SRL, a Belgian company specializing in antimicrobial resistance diagnostics, from Avacta Group Plc for a total of up to ₹30.87 crore (£2.765 million, converted at ₹111.67 per GBP based on current exchange rates). The deal involves an upfront cash payment of ₹24 crore (£2.15 million) and a potential additional payment of up to ₹6.87 crore (£0.615 million) based on performance. The acquisition is expected to be completed by September 10, 2025. Coris, which reported FY24 revenue of approximately ₹58.28 crore (€5.22 million, converted at ₹111.67 per EUR), will become a subsidiary of 3B BlackBio Dx, enhancing its global in-vitro diagnostics portfolio.

13 Likes

Doesnt the deal look too good to be true…a niche business generating 58 cr in topline annually sold for 30 cr. Unless this was a fire/distress sale.

2 Likes

Although the top line is 58cr

The EBITDA is around negative 2 cr.

Hopefully they give more info about the acquisition in the quarterly results ppt.

Also the top line has been flat for past 3 years.

5 Likes

2025.07.28- Coris-catalogue.pdf (5.7 MB)

Disc: Invested

1 Like

Claude.ai search result on financials of Coris Bio Concept:

Initial Acquisition (June 2023):

Avacta Group acquired Coris BioConcept for an upfront cash consideration of £7.4 million (US$9.3 million) on a debt-free/cash-free basis, with a potential earnout cash payment of up to £3.0 million (US$3.6 million) based on future business performance BloombergMitrade.

Subsequent Divestiture (2025):

In the year ending 31 December 2024, the Group reported a noncash impairment charge of £6.8 Million as a result of this disposal, indicating that Avacta has agreed to sell Coris BioConcept.

Operational Details

Facilities and Workforce:

Operationally, Coris employs 35 members of staff split across Production, Sales, Marketing, Quality Control, Regulation and Administration. In March 2023, the business completed the construction of a new 10,700ft² production, offices and warehouse facility in Gembloux

5 Likes

Press release from Coris

1753714145247.pdf (293.2 KB)

5 Likes

Finally the cash gets put to use. It will be crucial to unserstand what 3B intends to do with Coris and what the unit economocs and profitability metrics will be. This adds almost 60% to the sales number, so is a very significantly acquisition. If anything will promot the 3B management to do an earnjngs call, it nay be this.

6 Likes

Looks like an amazing deal. 70% lower purchase price than what Avacta Group paid for Coris just 2 years ago. A quick study of Avacta shows the company is in the doldrums with their stock down 90% from Covid highs and they recently exited another investment in March – so clearly a distress sale which 3BB has capitalized on.

At 25 cr - 30 cr purchase price, 3BB is giving up 11% - 13% of its cash reserves in exchange for an immediate +50% increase in top line, new product line and access to Coris’ distributorship in 60 countries where they can now co-sell TruPCR products. Judging by how the HS Bio / TruPCR acquisition turned out, we should reasonably expect this management has line of sight to profitability and investment payback in 3-4 years. Coupled with the organic growth from TRUPCR business, there is reasonable line of sight to doubling revenues to 200 cr in the next 1-2 years which growth was not visible at the end of Q4 (leading to some multiple compression).

Credit to 3BB for patiently waiting for a deal that met the valuation thresholds and still reserving ~90% of their dry powder for reinvestment and M&A.

28 Likes

3BBB plans to conduct quarterly earning calls going forward.

16 Likes

No mention of earnings call for Q1 in the results date announcement. Can someone please email the MD to confirm? I have already emailed them requesting to start con calls but not received a confirmation.

2 Likes

Do you have the email id of the MD? Many of us should write to him.

2 Likes

I have sent an email. Thanks Apurva for sharing Mr Dubey’s email id. I’d urge all investors to write to Mr Dubey as well.

Putting the contents of my email down as a reference:

Dear Mr Dubey, I hope you are well.

I have been a long term shareholder in 3B BlackBio, and I want to congratulate you on the excellent work you and the management team have been doing over the years. I also want to take this opportunity to congratulate you on the successful acquisition of Coris. From your press release, it seems like there will be a lot of synergies between 3BB and Coris.

I am writing to you to request if you may consider doing an earnings call, so investors like us and the broader market can learn more about how this acquisition will his will strengthen the long term prospects for 3BB. I my experience, I believe that the market wants to know more about 3BB, and an earnings call will be a great opportunity for the company to put its vision forward and engage with minority shareholders. I also truly believe that with more information available, there can be significant value unlocking for the business from the broader investor community.

I read a recent report from the AEC fund who ate also long term investors in 3BB, and it said that they were in touch with you regarding potentially starting quarterly earnings calls. I truly this will be a gamechanger in the company’s journey and will help it to achieve its true potential.

Look forward to listening to you on the earnings call.

Best

Vineet Jain

20 Likes

Got the following reply from Mr Dubey ![]()

Dear Vinit ji,

We are planning Earnings Call, post Q1 results on 14th in the week following ..

Details will be shared in update next week.

Thanks

Best Regards.

Dhirendra Dubey

Founder CEO

30 Likes

Thank you @Vineetjain111 @Apurva_Dubey for driving this excellent development on behalf of all investors here!

7 Likes

Company hosting Q1FY26 concall on 19th August, 5.30pm

9 Likes