Hi, Can anyone share the Nuvama report.

Thanks

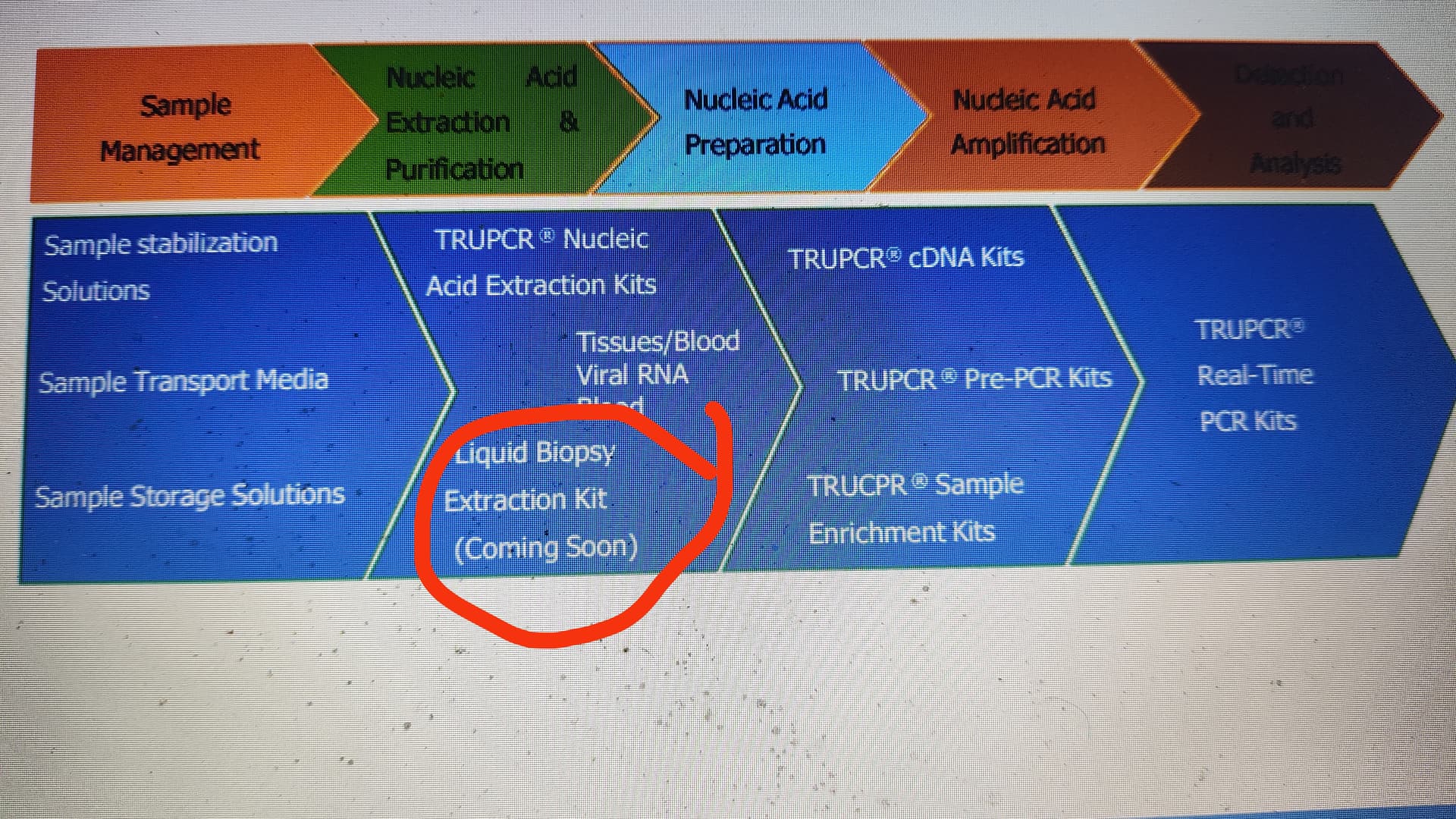

While going through investor presentation, stumbled upon the following:

The growth rate is 2x, 12% CAGR compared to 6.2% CAGR in nucleic acid extraction.

Definitely a positive development and addition to the trupcr product lineup.

17 Likes

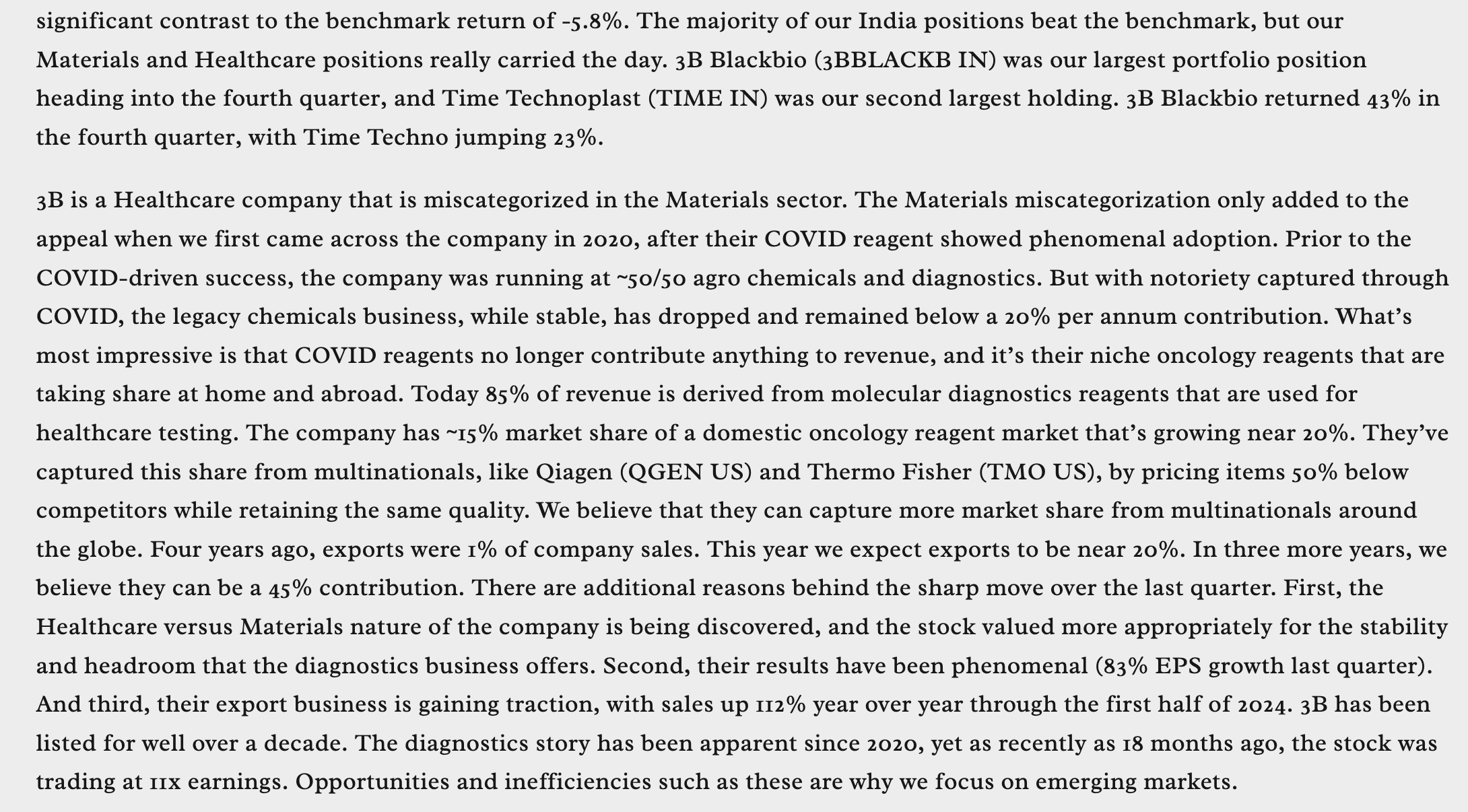

Quarterly commentary from Ark Global Emerging Companies - FII with 1.9% shareholding in 3B BlackBio as of Dec-end. It is the largest portfolio position in this fund.

21 Likes

Distributor in Ireland

9 Likes

Do the current margins seem sustainable?

With spread of Covid, demand for testing kits should go up. Looks like good times ahead for 3BB.

3 Likes

Disappointing results. Company says order shifts to Q1, but still the decline in revenue was a surprise.

Only silver lining was they are taking market share in Indian mdx market.

2 Likes

3B BlackBio Dx Ltd. Results (FY 2024-25)

- Overall Performance Assessment: Strong Annual Growth with Quarterly Volatility

- Positive Full-Year Trajectory: The company has demonstrated robust growth for the full fiscal year 2024-25, with significant increases in Revenue (up 30% YoY), PAT (up 48.5% YoY), and EPS (up 48.6% YoY). This indicates a healthy underlying business momentum and effective execution over the longer term.

- Q4 Volatility & Seasonality: While the full-year results are strong, Q4 2024-25 showed a dip in both revenue and profit compared to Q4 2023-24. This quarterly fluctuation is attributed by management to seasonality in certain diagnostic kits (Flu, Dengue, Chikungunya) and the deferral of some international orders into Q1 FY 2025-26. This highlights the importance of evaluating this business on an annual or year-to-date basis rather than focusing solely on individual quarterly results due to its inherent cyclicality.

- Key Strengths and Growth Drivers

- Robust Molecular Diagnostics (MDx) Business: The MDx division is clearly the primary growth engine. With a 12-15% market share in India’s MDx market (estimated at INR 350-450 Crore) and an industry growth projection of 8-10% CAGR, 3B BlackBio is well-positioned for expansion.

- Aggressive Growth Targets: Management’s guidance of 15-20% growth for MDx in FY 2025-26 and 20-25% for international business (especially TRUPCR Europe) demonstrates confidence in their market strategy and product acceptance.

- Strong Product Pipeline & R&D Focus: The planned launch of Digital PCR (dPCR) and new NGS panels (e.g., PAN-MYELOID, BRCA Plus) signifies continuous innovation and a commitment to expanding into high-growth, advanced diagnostic areas. The successful development of AMR rapid tests also adds to future potential.

- Strategic Business Model (Reagent-Rental): The establishment of over 15 long-term contracts under the Reagent-Rental Model, projected to contribute 20-25% of total revenue, is a significant positive. This model provides a predictable, recurring revenue stream, enhances customer stickiness, and offers a competitive advantage.

- International Expansion: The nearly 97% increase in export sales in FY 2024-25, driven by the UK subsidiary, indicates successful global market penetration and diversification of revenue streams.

- Agrochemicals Stability: While not the primary growth driver, the agro-chemical division provides a stable base with minimal debt, focusing on government tenders and exports.

- Key Challenges and Areas to Monitor

- Seasonal Volatility in MDx: The Q4 performance underlines the impact of seasonality in infectious disease testing. While understood, investors should be aware that quarterly results might not always reflect the true annual growth trajectory.

- Margin Sensitivity to Product Mix: The dip in Q4 margins (35.72% vs. 38.22% YoY) suggests that the sales mix, particularly the lower demand for higher-margin seasonal products, can impact profitability. Maintaining or improving overall margins will depend on the successful integration of new products and continued focus on high-value segments.

- Execution Risk on New Products/Regions: While the product pipeline and international expansion plans are exciting, successful commercialization of new assays (dPCR, NGS) and deeper penetration into new geographies will be critical.

- Future Outlook and Recommendations

- Positive Investment Thesis: Overall, the results present a compelling investment thesis, driven by strong annual growth, a dominant position in a growing MDx market, a robust product pipeline, and strategic revenue models.

- Monitor Growth Drivers: For investors, closely monitoring the actual growth rates in the MDx division (especially new product adoption and international sales) against the management’s ambitious targets will be key.

- Impact of Order Shifts: The “adjusted” Q4 numbers (Revenue ~INR 22.94 Cr, PAT ~INR 8.20 Cr, EPS ~INR 9.57) provide a more complete picture of what Q4 could have been, mitigating some of the concerns about the reported dip. This deferred revenue will likely boost Q1 FY 2025-26 numbers, which is a positive.

- R&D and M&A: Continued investment in R&D for new product development and strategic M&A activities (as mentioned in their priorities) could further accelerate growth and market leadership.

In conclusion, 3B BlackBio Dx Ltd. Is a high-growth company with a strong strategic vision, particularly in the MDx space. While some quarterly fluctuations are expected due to seasonality and operational shifts, the overall annual performance and management’s forward-looking guidance indicate a promising outlook.

15 Likes

Margin pressure is now a reality. Diagnostic Segment results margin reduced to 67.5% in Q4 2024-25 from 73.1% in Q4 2023-24. Read “While this growth is attracting increased competition” in page 16 - investor presentation- Business Outlook – MDx (Q4/2024-25). To maintain growth as per plan, revenue has to grow offsetting margin contraction. Next quarters to be watched. Things like NSE listing, buy back, stock split not mentioned in investor presentation.

7 Likes

Here are the annual Profit After Tax (PAT) margins for the past four fiscal years:

- FY 2021-22: 50.00%

- FY 2022-23: 45.30%

- FY 2023-24: 43.31%

- FY 2024-25: 49.44%

The average PAT margin over these four years is approximately 47.01%.

While we observed a Q4 FY 2024-25 PAT margin of 35.72% (compared to 38.22% in Q4 FY 2023-24), this was specifically attributed by management to: - A seasonal fall in demand for high-contributing diagnostic kits (like Flu, Dengue, Chikungunya).

- Orders being shifted from Q4 FY 2024-25 to Q1 FY 2025-26.

As you can see from the annual figures, the company’s margins have consistently stayed within a strong range, with FY 2024-25 showing a robust 49.44%. The Q4 reduction appears to be a temporary, seasonal impact rather than a fundamental change in the company’s long-term profitability.

For particularly diagnostic segment, there should not be any concern untill it remains above 60, and as management guiding 25% growth in exports there is less chances of major margin drops. But Q1 will show better picture.

5 Likes

I found these new products very interesting. Can anyone throw some light on these? Like what’s TAM and who are the competitors.

2 Likes

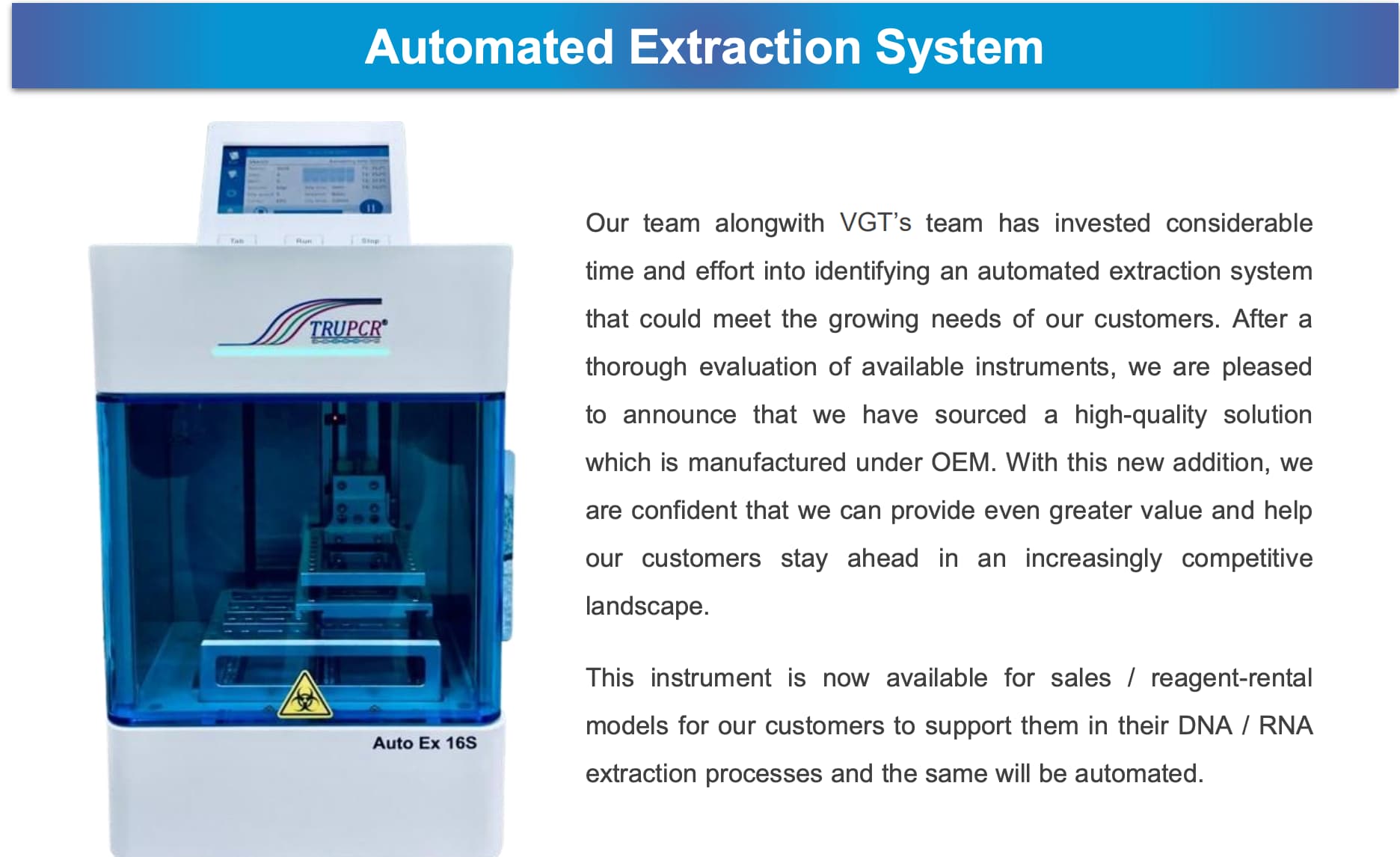

Product Summary: Auto EX 165 by TRUPCR

The Auto EX 165 is an advanced automated DNA/RNA extraction system developed by TRUPCR in collaboration with VGT. Designed for research, diagnostics, and academia, it supports PCR, sequencing, and molecular diagnostics. Key features:

- Available via sales & reagent-rental models

- OEM-manufactured

- User-friendly interface with digital display and biohazard safety features

Market Size (TAM)

The global market for automated nucleic acid extraction systems is projected at USD 5.02 billion in 2025, growing at a CAGR of 8.1%. The broader nucleic acid purification market will reach USD 9.77 billion by 2030, driven by automation, precision medicine, and molecular diagnostics.

Key Competitors

- Thermo Fisher – KingFisher Apex Dx

- QIAGEN – QIAcube, EZ2 Connect MDx

- Roche – MagNA Pure LC

- Beckman Coulter – Biomek Workstations

- Aurora Biomed – VERSA, ADNAP

- Esco Lifesciences – Automated extraction platforms

- MP Bio – MPure-96™

Other players: bioMérieux (easyMAG), PSS, BioChain.

Technologies used: magnetic beads, silica matrices for research & clinical workflows.

5 Likes

what is the pricing of these machines

10 to 25 lakhs approx for mid sized..

Competitor Systems & Approximate Pricing

| System | Manufacturer | Estimated Price (INR) | Key Features |

|---|---|---|---|

| KingFisher Apex | Thermo Fisher Scientific | ₹75–80 lakhs | High-throughput (24–96 samples/run), magnetic bead-based purification, touchscreen interface, cloud connectivity. |

| QIAcube HT | QIAGEN | ₹1–2 lakhs | Automated nucleic acid purification for 96 samples, suitable for high-throughput labs. |

| MagNA Pure LC | Roche | ₹50–60 lakhs | Automated system for nucleic acid isolation, suitable for various sample types. |

| Biomek Genomic Workstation | Beckman Coulter | ₹60–70 lakhs | Flexible automation for genomic workflows, including nucleic acid extraction. |

| VERSA Automated Workstation | Aurora Biomed | ₹40–50 lakhs | Modular design for various applications, including DNA/RNA extraction. |

| Automated Nucleic Acid Extraction System | Esco Lifesciences | ₹30–40 lakhs | Compact system designed for efficient nucleic acid extraction. |

| MPure-96™ aNAP System | MP Biomedicals | ₹25–35 lakhs | High-throughput system for automated nucleic acid purification. |

4 Likes

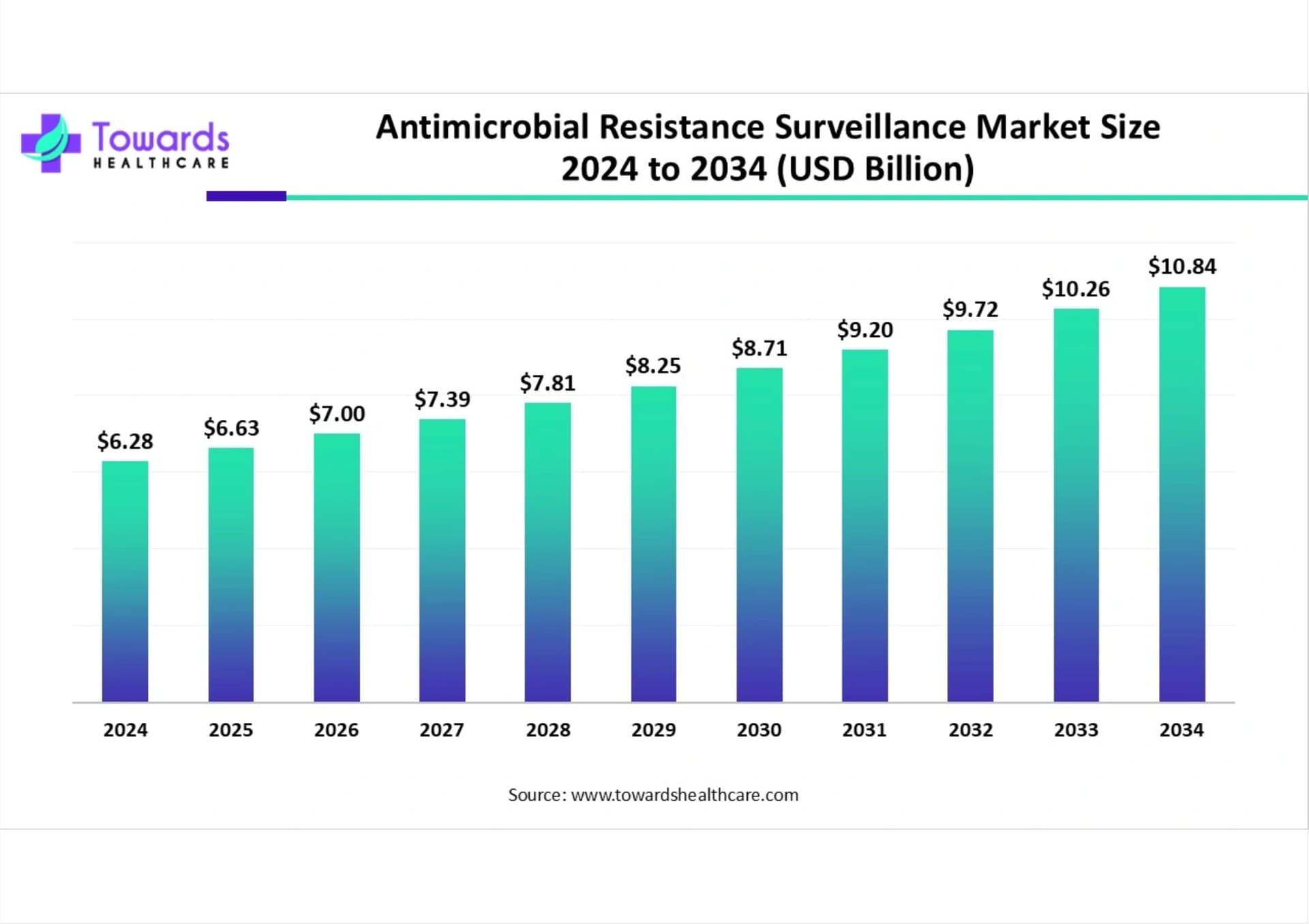

AMR Diagnostics market:

-

Global Market Size: In 2024, the global antimicrobial resistance diagnostics market was valued at approximately USD 4.6 billion. It is projected to reach USD 6.7 billion by 2030, growing at a compound annual growth rate (CAGR) of 6.5% from 2025 to 2030 .

-

Regional Insights:

-

Asia Pacific: This region generated USD 1.05 billion in 2024 and is expected to grow at a CAGR of 7.8%, reaching USD 1.64 billion by 2030 .

-

China: In 2024, China’s market size was USD 245.1 million, with projections to reach USD 394.6 million by 2030, growing at a CAGR of 8.3%

-

Major Players: Abbott and Thermo Fisher, Molbio Diagnostics in India.

[Source: ChatGPT]

4 Likes

Management has been talking about AMR for more than an year now. I get it that it takes time for research to translate into topline…but I feel it’s about time we see some traction in AMR.

Also management should do concalls…it will help build.investor.confidence.

I felt today’s spectacular crash was a knee jerk reaction and that the long term story is shaping well.

Disc.: invested and biased and bought some more today

4 Likes

Absolutely agree. AMR is a massive long-term opportunity and 3B BlackBio seems well-positioned with the right research focus. While it’s true that deep-tech innovations take time to convert into revenue, we should start seeing some traction soon given how vocal management has been.

Today’s sharp fall looks like a classic case of illiquidity-driven panic, not a reflection of fundamentals. The long-term story remains very much intact and is only getting stronger.

A management concall or regular updates would be a game-changer at this stage—boosting confidence and helping the market better understand the unfolding value.

8 Likes

Well said, concalls are the need of the hour for investors. Need to improve liquidity.

Disc: Invested, still holding full quantity.

4 Likes

Guidance has also been reduced from 20-25% to 15-20%.

Disc: Invested

1 Like