Thanks for wonderful thread Sahil. Guess the most critical part for success going forward is your item # 22. Spend on R&D and results delivered by scientists. Just a follow up question based on your conversation with the microbiologist:

Understand the cost and the impact to govt tenders but how does 3BB kits compare in terms of quality with that of Thermofisher and Applied Biosciences and will it potentially have a larger positive impact on the private health sector going forward?

2 Likes

It is not deferment of taxes, taxes are paid every quarter as advance tax and accordingly deducted from Cash flow statement. However, just as an accounting treatment they are parked in two control accounts (kind of) 1. advance tax reflecting taxes paid and 2) provision for taxes, thus on one side shown as current asset (advance tax) and other side current liability (provision for tax) and net impact would be zero. Feel free to discuss over DM or call, if needed.

4 Likes

Continuing my scuttlebutt i talked to 1 investor who is also invested in kilpest and did some scuttlebutt of his own. So this is second hand information. I trust him and dont see any reason for lack of trust but with that disclaimer he has helped me answer 1 key question I had: to what extent is kilpest/3BBB part of large institutions’ supply chain.

- SRL has been using their tests since last couple of years

- Metropolis also does so as confirmed by their lab ( a doctor) here in Chandigarh. Mostly onco tests.

- Thyrocare I am not too sure as their doc did say they use it but didn’t sound confident regarding which tests.

- Lal path lab has its own sourcing so don’t think they are going to source from the company.

- They already have NGS capability (they procured the machine in Apr 2018 as per disclosures). But commercial launch in India wouldn’t make sense as some companies (thermo fisher) are selling it below cost just to get a foothold. Main market is US where it gives great remunerations (all this via a doctor friend who heads the administration in a govt hospital here & his wife is the head of diagnostics). So launching it would make sense only once exports open up completely and both the company & the customers are sure about no supply chain issues.

For me personally 1st 4 points are important. This demonstrates the quality of the kit and the strength of the brand even more.

Disc: Invested and Biased.

17 Likes

From my scuttlebutt on this last year ( with one of the thyrocare centers) --i got the info that antibodies test was done from kits of another company (not kilpest) --they were not sure about testing kits in general that time

3 Likes

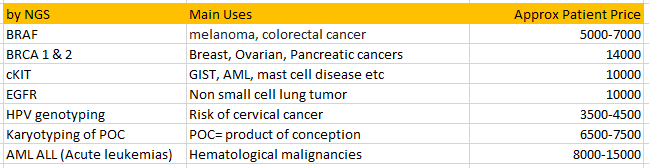

Can you please provide what is the cost of NGS in general and what is the market size of it? and what could be the expected margin in US?

Even if thermo fisher sells at lower cost, there is always a probability to penetrate as big clients always keep more than one supplier to reduce dependency on single supplier…

Mentioned some rates here.

NGS rate average is 3-4x than PCR. These are patient charges.

Kit(test) price is usually 1/2-1/5 of patient rates.

4 Likes

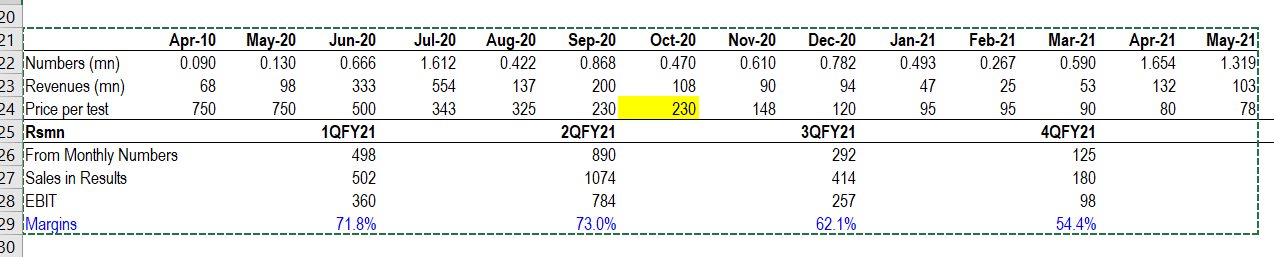

My collation of 3B Black Bio RTPCR monthly test data and quarterly numbers. Based on this its obvious EBIT for 1QFY22 and 1QFY22 are going to fall sharply YoY (because of a massive price crash in selling price per test). Has anyone figure out what is the non RTPCR revenues, EBIT and steady state revenue and EBIT for RTPCR with some workings?

Company had Rs75crs market cap and has gained Rs340crs market cap due to Covid

2 Likes

Off course I have glanced through the thread. You are assuming I havent in your message.

The conclusions I am reaching are, there was a one off opportunity which company exploited. But now there are two many companies competing for same pie. Prices can crash more which will lower EBIT margins. So even with higher tests per qtr company will make much low EBIT and PAT yoy.

4 Likes

Kilpest owns 87.44% of 3B Black Biotech. Do you know who owns the balance? When does the amalgamation become effective?

Any idea when 3 B will be demerged from kilpest?

Shareholding of 3B Blackbio:

Source: Valuation report

The amalgamation will be deemed to have taken place on 1 April 2020.

1 Like

Thanks,but I cud not understand.

3 B is not listed,so how can I buy shares of it?If I buy kilpest,how will the other entity demerge?

3BB will be merged into Kilpest and the parent co. will be renamed to 3BB Dx. Those 13% of 3bb shares listed here will be coverted to Kilpest shares at an exchange rate of 1 3BB share = ~8 kilpest shares.

We as shareholders of kilpest need not do anything, the parent company’s equity will be slightly diluted is all. Our earnings are already diluted since we only get 87% of 3BB EPS so that should not be affected

2 Likes

Sorry for interruption but profit estimation would be very futile at this stage as the dynamics of this RT PCR or say Molecular Diagnostic Kit industry is changing rapidly. Revenue jump and profit jump would definitely be there and that would be easily be north of 20% as per management but this management has outperformed itself every year and every quarter be it COVID times or Non COVID times.

3 Likes

Hi Sahil, All,

Though I am positive on the overall industry dynamics and present positioning of Kilpest/3B Black Bio, but intention of this post is to have discussion on some negative aspects involved, which are as under-

-

Don’t you think that Covid business was black swan event for them and otherwise not too much achievements in kitty for kilpest/3B Black Bio?

-

Growth rate of 40% in 3B Blackbio business in past does not have too much relevance because of low base effect.

-

Management seems not too aggressive. For instance, they have been working on RAT from last so many months, but no successful completion till now. I don’t have any doubts on integrity and transparency of the Management.

-

Too much cash for them to handle considering their past experience, so risks of wrong deployment or diworsification is high.

-

Entire story around potential of 3B Black Bio is forward hope story only.

Could you please share your thoughts?

D- Invested and intention is not to create negativity but to understand/mitigate the risks involved.

10 Likes

Highly likely profits will fall in current year. Just wanted to understand what others think. @ravish 20% growth on FY21 profits is wishful thinking.

I disagree. Have you read my posts? If you have, i don’t have anything to add.

Growth rates have nothing to do with base. See Alphabet, Amazon. Everything to do with size of opportunity and growth triggers. Request you to Please carefully read my previous posts if you havent to understand the growth triggers. New products, tie up with new clients, cross selling to new clients, market size going up 5x due to covid (go through posts to understand why this change is likely to be irreversible). Note that I have not forecast a growth rate, it is very difficult to do so. Whatever that number is, as long as management wants to grow, that is all that matters. Whether it is 25%, 30% or 40% is irrelevant, investment is sound.

Please understand how diagnostic kit design works. this involves lot of trial and error like any R&D heavy industry, failure is a part and parcel of the game. One cannot expect 100% success all the time. The failure does not demonstrate anything on the aggressiveness. 9 women cannot give a birth in 1 month. R&D is inherently a sequential process. Patience is of essence.

diworsification, disagree, please read how they plan to deeploy cash. ‘wrong deployment’ is all based on hindsight, in hindsight one can always say everything as right or wrong. But businesses work on experiments. Some work, some dont. Need to evaluate management processes; not outcomes.

Same point as 1st one. Disagree, Please read previous posts to know more. ![]()

Let me also add what the key risks are imo:

- Now that story is somewhat discovered, valuations are only going up. At some Valuation, it won’t make sense to buy.

- Competitive intensity can increase as a result of covid related windfalls most cos will make. Will need to see how this plays out.

- As 3bbb’s clients grow larger, some % of them at least would look to backward integrate and create kits themselves. See Dr lal path for example.

Imo best way for kilpest to derisk would be to forward integrate by opening a B2C franchise. Would take care of all 3 concerns. 3 birds killed with 1 stone.

13 Likes

Hi @sawhneyvivek, you sound apologetic for asking very relevant questions, please dont’

Counter views are alsolutely needed to keep eveyone honest

I will attemot to share my thoughts on your questions:

1 & 2: Covid maybe was a black swan event and in my view, all estimations of 3BBB should be made keeping the core business minus covid in mind (although it almost seems like a consensus opinion from my many doctor and pathologist friends that covid is going nowhere for a few years in spite of vaccination - so that revenue, however small with reducing kit prices, will be a bonus).

I don’t entirely agree that the pre-covid growth rate has no relevance. In fact if anything, I think covid will accelerate growth for the non-covid molecular diagnostic industry as a whole. Established players with top notch R&D will stand to benefit.

3 & 4: Agree and this is a relevant risk imo. They are making all the right noises though - clearly saying that they will wait patiently for the right acquisition opportunity to present itself, or else return the money to shareholders at a future date. Also the valuation report of 3BBB shows the aggressive revenue and profit targets for the company going forward (PAT of 150cr by 2025). So Covid has definitely given them a lot more confidence, and industry tailwinds area powerful force.

5: It is a bit of hope, but thats what narratives are, aren’t they? We have to keep tracking the progress on implementation against this narrative. That said, imo at a 15-20 sans covid PE and good growth projections, a competent (and transparent) management, top R&D capabilities, large industry tailwinds, and almost a quarter of the market cap as cash on books, the risk-reward looks very compelling

8 Likes

Many investors are mistakingly writing off Covid testing too early (they wrote it off last year and they will write it off again with the 2nd wave in India receding). It is correct to assume that Covid testing revenue will fall for 3B Blackbio but it would be unwise to assume it will go to zero. In fact, it may contribute meaningfully for years to come.

-

First, we have to acknowledge that the world has changed and some things aren’t going back to normal. Read about testing in “Covid free” or “nearly Covid free” countries like Israel, Singapore, Australia, Hong Kong etc. They haven’t stopped Covid testing. India (4% fully vaccinated) is years away from reaching their level at current vaccination rates. Even the US (46% fully vaccinated), which is doing phenomenally with vaccines, is preparing for a testing strategy well into the future - https://www.wsj.com/articles/covid-19-testing-could-be-a-viable-long-term-business-bet-11622991601

-

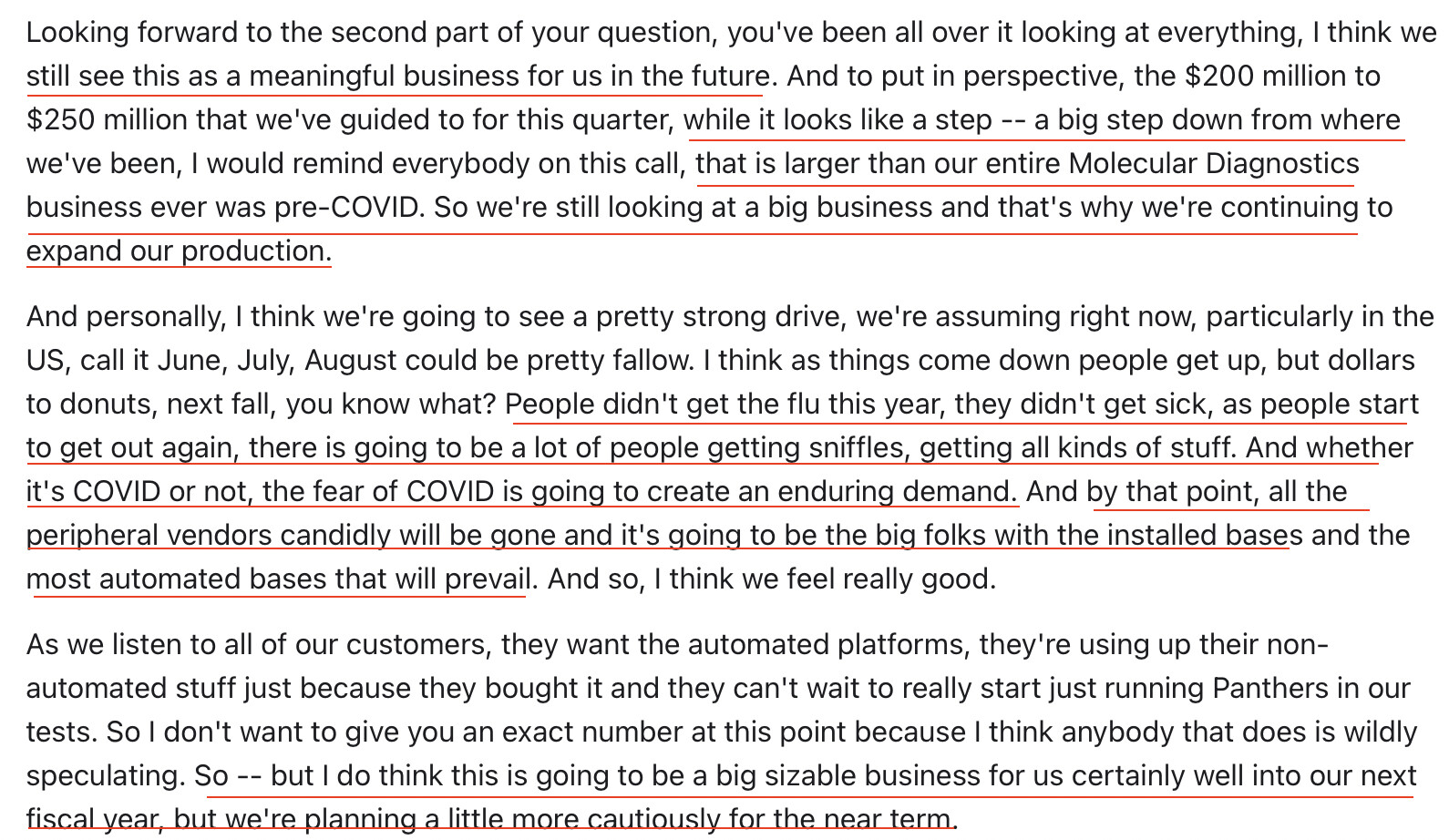

Second, let’s look at what global testing giants are saying about the future of Covid testing. Here is an extract from Hologic’s last investor call in April. For context, Hologic is an $18 billion molecular testing leader, they’ve sold over 100 million Covid kits generating over $2 billion in revenue since the start of the pandemic.

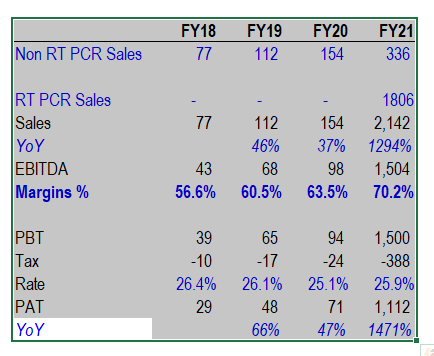

3B Blackbio will do ~30 cr in Covid testing revenue in Q1 FY 22, also larger than their entire molecular diagnostics business pre-pandemic. As Covid testing falls, the business will become unviable for the new entrants allowing established players like 3B Blackbio to gain market share. Prices of Covid tests will increase as economies of scale reduce. A very important point above - “Whether its Covid or not, the fear of Covid will create an enduring demand”. Read this thrice to absorb it, at the personal level and then at the family/community/national level. Will countries, especially the rich ones, ever risk experiencing a pandemic again?

-

Third, we cannot discount the possibility of multiple new waves of Covid in India.

-

Fourth, we must factor in scenarios beyond testing specifically for Covid. Covid tests might become part of larger flu panels. Have flu symptoms? Get one multiplex test to figure out what kind of flu it is. Such tests are already available and quite easy for Kilpest to develop (they already have several multiplex panels):

- Fifth, tests will likely remain essential for international travel. Even if you take a conservative position, and say 1 year from now only outbound international travellers will need to undergo a Covid test in India - that’s nearly 3 crore tests a year based on pre-Covid outbound travel.

- Sixth, as India opens up, non-Covid tests will naturally increase, probably at a higher level than pre-Covid due to increased testing infra, public awareness, fall in testing costs etc.

On the one hand, they have not aggressively developed antigen tests and home tests. It would have been great if they did. On the other, they aggressively developed their PCR test (2nd in country) and scaled up 100x to meet the demand. We need to view these decisions in context of the size of the company. There are around 5 Indian companies comparable to 3B Blackbio - Mylab, Sidak, Ubio, Angstrom and NextGen Invitro - who have both RT PCR and rapid antigen Covid tests approved by ICMR - not a very long list.

Definitely a risk but until we see where the cash goes it remains an asset. Here I do want to point out that the Girik Capital duo - Varun Daga and Charandeep (who together with the promoters own ~50%) bring substantial experience and will be valuable mentors. Here’s some info on them for those interested - Alpha Moguls | The Best-Performing Portfolio Manager In 10 Years Swears By Buying High, Selling Higher

15 Likes

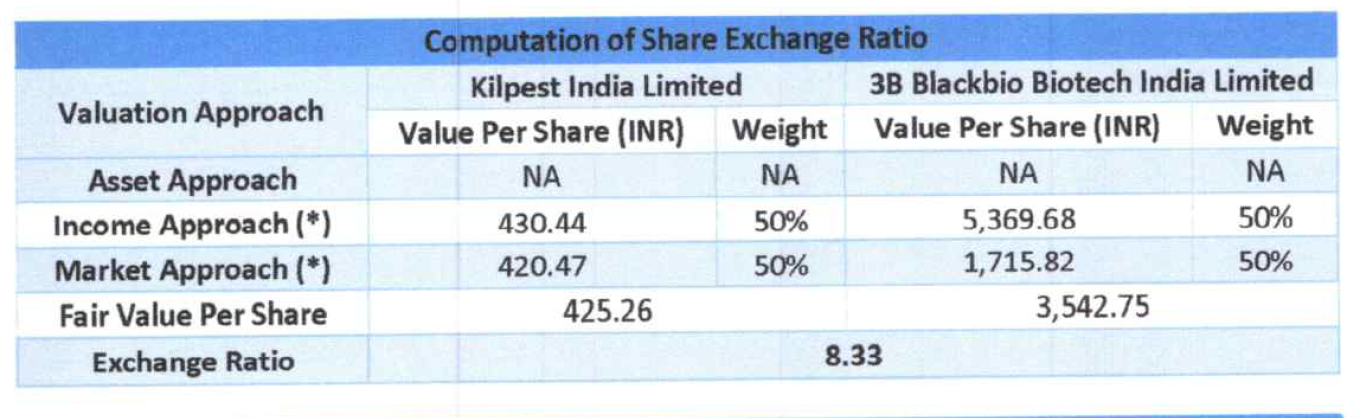

I wouldn’t use the projections in this DCF for my earnings estimates. Valuation is an art and not a science. I think the DCF valuation has been adjusted upwards to compensate for the lower market multiples value to arrive at a “fair value” of 363 crore for 3B Blackbio. This valuation was done in September 2020 and is a very fair value imo for minority shareholders which didn’t result in significant dilution.

You have to look at the overall valuation methodology followed and not the DCF alone.

The valuer used a market approach and income approach to value 3B Blackbio and gave an equal weightage to each. The market approach use the EV/EBITDA and EV/Sales multiples of Thyrocare, Dr Lal and Metropolis and applied them to FY 20 earnings of 3B Blackbio (pre-pandemic) giving it a value of 1,715/share or only 175 crore. To adjust for this I’m assuming they increased the DCF value to 5,369/share or 550 crore leading to an equal-weighted value of 363 crore.

Obviously with hindsight and the second wave we can say this was a low valuation. If you take historical growth rates on the non-Covid business and model current Covid trends, you shouldn’t expect them to grow this quickly. If they do then even your 1200 cr market cap estimate will be very low ![]()

1 Like