The Annual Report 2021 for Kilpest India has been shared on their website but it is not yet on the exchange - https://kilpest.com/upload/Kilpest%20Annual%20Report%202021.pdf

For those who have followed this thread and the recent investor presentations, there seems to be nothing much new in the Annual Report at least from a quick read. The management discussion and the director’s reports are not talking much about future growth plans. I am assuming that they are keeping a lot of the plans close to their chest because coming out in public domain is not going to help very much.

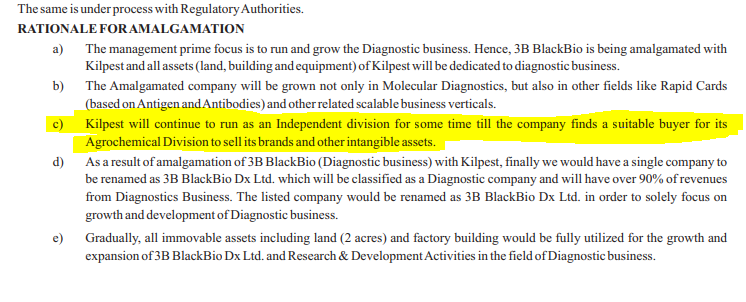

Edit - They have shared points on the scheme of amalgamation for Kilpest into 3B BlackBio Biotech. Couldn’t find a mention of listing on NSE in the AR but they did mention it even in the last investor presentation, so it will happen in time, I guess.

They mentioned that they are working on developing Antigen / Rapid card type tests, I see that as good.

From what I understand by reading RHPs of recent IPOs of diagnostics labs, molecular diagnostics is urban centric and it will take time for rural areas to start installing such technology. Kilpest / 3BB mentions that it will take time to spread their customer base in molecular diagnostics, take time to develop the trust in India. . Even the medium sized diagnostics labs like in the latest IPO Vijaya DIagnostics, seems apprehensive of the expense of getting into Molecular Diagnostics.

One thing is that molecular Dx growth in India will be slow but the other thing is that the growth is going to look almost like J-Curve exponential when it comes. It will probably be around the time when almost all the large players are near to completing their necessary capex to shift to Molecular diagnostics and NGS type testing. Still good for the long-term investor.

They did not talk much about exports except that they are venturing into export markets. They said that 3BB is being viewed as ‘on-par’ with foreign multinational by big labs. This sounds good.

Going by a recent CRISIL study of the diagnostics space that has been mentioned in a few of these recent Diagnostic company RHPs, pathology testing commands a higher share of the diagnostics market. Typically, a battery of tests is prescribed under a single pathology test panel for a single patient. CRISIL estimates that Pathology tests are 57% of the market while rest are radiology, implying 43% of the market. This makes an addressable market size of Pathology tests of 40,470 crores. Pathology tests are expected to grow at a CAGR of 12% or more from FY 2020-23, with an estimated market size of Rs. 550 billion or 55,000 crores.

The products made my 3B BlackBio Biotech maybe commanding a much smaller portion of this market size in its revenue pool. Maybe 1/10th of that testing revenue may go to testing kit makers so 4000 crores market size (roughly). While I have no numerical basis to say this, it is a fair assumption that most diagnostic chains and in-hospital diagnostics facilities are still to complete their shift towards molecular diagnostics. This is due to the (at least) perceived high cost of ‘technology advancement’.

Copying from Vijaya Diagnostics RHP

“High cost of technical advancement - Risk for Diagnostics centres

Diagnostic centres have to constantly upgrade their technology to stay ahead of the competition. However, these upgrades not only involve significant capital investment, but also increase maintenance cost, thereby increasing overheads. Capital intensity is higher for advanced radiology and molecular diagnostics, which require high-end equipment.”

Of course this is the case of a smaller, regional diagnostics chain and the larger players are already making this shift but it appears to me that current cross selling opportunities in India are limited. The AR 2021 mentions that the subsidiary is a market leader in India and well recognized so the first-mover advantage might play out.

Trying to figure out the market size for testing kits in India and the competitors market share in Molecular Diagnostics has been a bit difficult.

Edit - Related reading - Article from February 2020 - Molecular Diagnostics A Path To Improved Healthcare - BW Healthcare

The market will grow with the entry of new players, its far too early to worry about losing market share

The market will grow with the entry of new players, its far too early to worry about losing market share