I can not find these figures in any documents. Can anyone provide snapshot or this document for reference?

https://www.bseindia.com/corporates/NOCUnder.aspx

projections here, without covid, difficult to digest

3 Likes

Can you please post the snapshot as I am not unable to find in this document.

You can go through the entire report. Has projections for both companies

2. Valuation Report.pdf (6.2 MB)

1 Like

Prateek Goel, HCO of 3B BlackBio biotech has told that they were importing WHO certified reference material for their kits.

They have other molecular diagnostics kits as well, not just covid19 kits. Please go through this video from 22nd minute.

7 Likes

@sahil_vi As per my understanding, Reference material for RT-PCR kits are RNA Reference material, which are target gene fragments for virus detection. Certain reference materials acts as ‘control’ also.

1 Like

On simpler words, these reference materials are standardised genetic sequences which are complimentary to certain portions of viral genome and helps us in detecting the SARS COV2 more accurately.

5 Likes

I think this is correct. I was able to find recent document submitted by 3B Black bio to USFDA for revision of their EUA authorization:

EUA-blackbio-trupcr-ifu.pdf (1.2 MB)

This is a good read for anyone that wants to understand the test. And also what changes they have submitted to USFDA for revised EUA grant (which was granted few days ago).

One table would be of particular interest to this group:

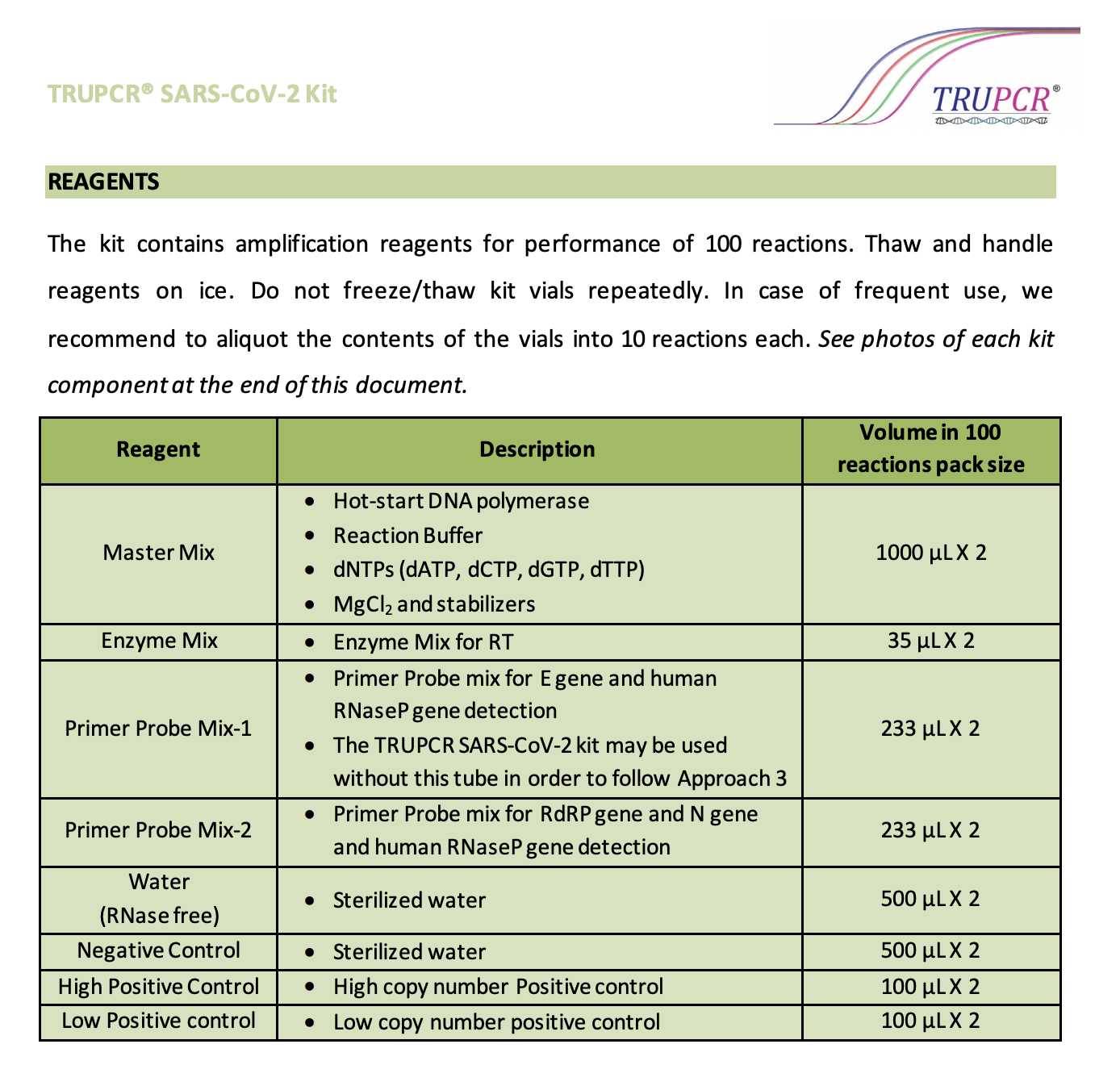

As we can see, most reagents are in very small quantities. Even the highest quantity required is 2mL for 100 tests. This works out to 20 microL for 1 test. Works out to 20L for 1,00,000 tests. Believe this level of manufacturing can be done easily in the labs they have. Thus it is definitely possible that they manufacture the reagents in-house since quantities are small. This USFDA document has verified your hypothesis ![]()

This website is very useful to track whether any indian competitors got EUA for their kits, and how this market is shaping up:

https://www.fda.gov/medical-devices/coronavirus-disease-2019-covid-19-emergency-use-authorizations-medical-devices/in-vitro-diagnostics-euas-molecular-diagnostic-tests-sars-cov-2#individual-molecular

Disc: studying, have tracking quantity.

9 Likes

To track company’s tall claim of exponential profit growth, can only be known by its Export data. We need to get export data month wise so that we can have track on trends. One thing is also clear that without carrying full fledge operation in US and UK (more importantly USA) this is not possible at all so exports are to be tracked closely. If any link or site that can provide this specific data then please share here.

Going to now answer my own questions. Have watched several 3B Black bio videos, read IPs and a few auxiliary documents + this thread + last few Annual Reports. Will divide this post into various sections and answer questions as per the section.

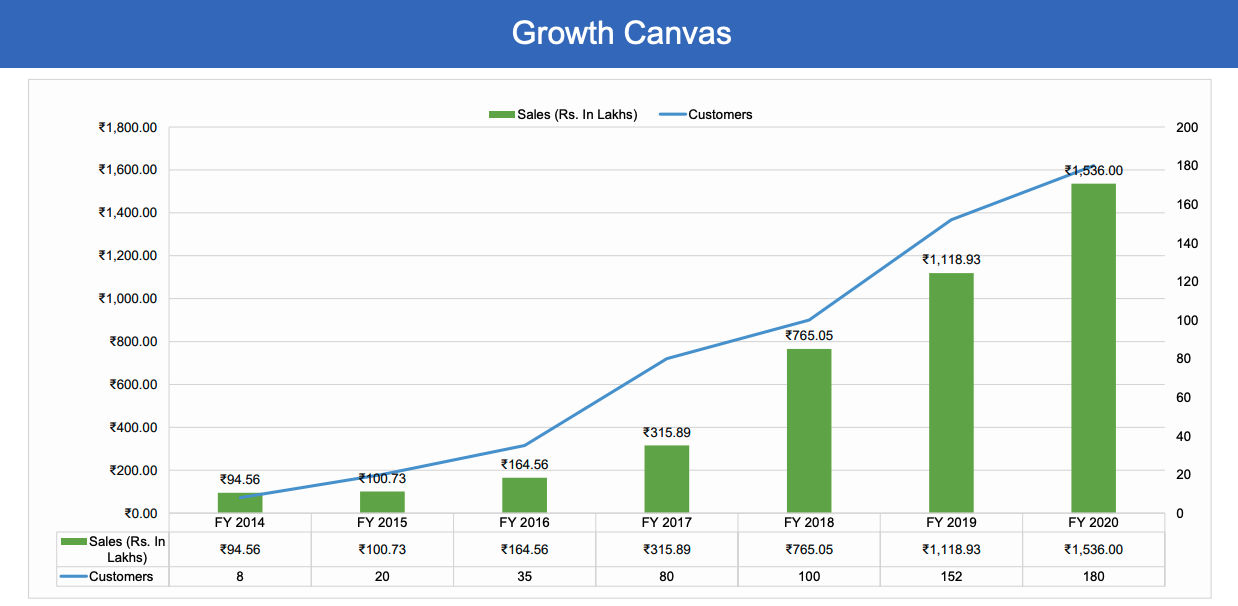

Growth

If we look at the growth of 3B black bio pre-covid, we can easily see the high growth rates.

Higher growth rates have continued in pandemic year (ex-covid as well) due to larger customer case (will come to this later). One can find many posts in this forum with exact data, such as this one: 3B Blackbio DX Ltd - #406 by enelay by @enelay.

What we will now analyze are some key future growth triggers/drivers:

- Acceleration of Molecular diagnostics penetration: As per this ICMR latest report: Exception(404) | Indian Council of Medical Research | Government of India there are 2600 molecular diagnostics laboratories testing for covid-19. A year ago, this number was 400. The Pandemic has caused an extreme acceleration in the penetration of molecular diagnostics among diagnostics centers in India. All of these new labs are possible clients for 3BBB. I wish the pandemic ends early, and we never see another one. But the small silver lining is that molecular diagnosis (faster, more reliable, accurate than older methods) penetration has been accelerated by several years in a matter of a year. Cross-selling to these newly created molecular diagnosis labs would be one key growth driver.

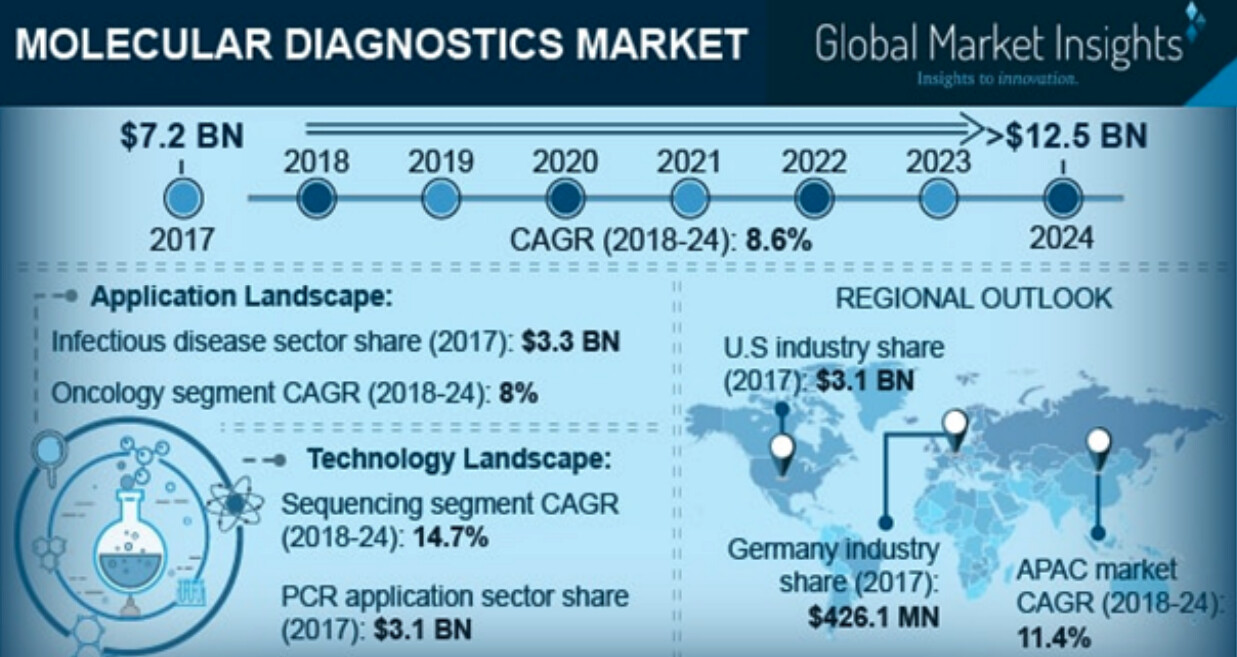

- Industry growth: The molecular diagnostics industry itself was growing at ~8.5% (pre-covid) at global level (making it one of fastest growing industry). APAC region was growing at 11.5%. Diagnostics is a fast growing industry too, which we can tell from Dr lal path’s pre pandemic growth rate of ~15% for topline. In fact Lal path’s post pandemic non-covid tests are also growing much faster now (even accounting for low base effect). How sustainable this is, remains to be seen.

- New products leading to higher cross selling: Company is constantly producing new products. This increased product development will allow higher cross selling to existing clients and ability to capture larger share of client wallet. We already see this in the numbers. In Feb-20 company used to get INR 45M from long-term contractors (7 such contracts existed). In Feb-21 this has increased to 70M. This is a growth of 55M%. Company is able to capture larger share of customer wallet.

- Growing exports: Due to pandemic certain restrictions, company’s exports have been hard to scale. One such restriction is that government only provides 3 month export licences at a time. This creates uncertainty in client’s mind about the supply chain. I quote directly from Feb-21 presentation: “In the coming year, our main area of focus would be exports once the restrictions are lifted.” In FY20 company was able to do exports of INR 6.5M. in FY22 Company aims to do exports of INR 60-70M modulo government license restrictions. The sustainability of exports will become clearer when we look at the quality section.

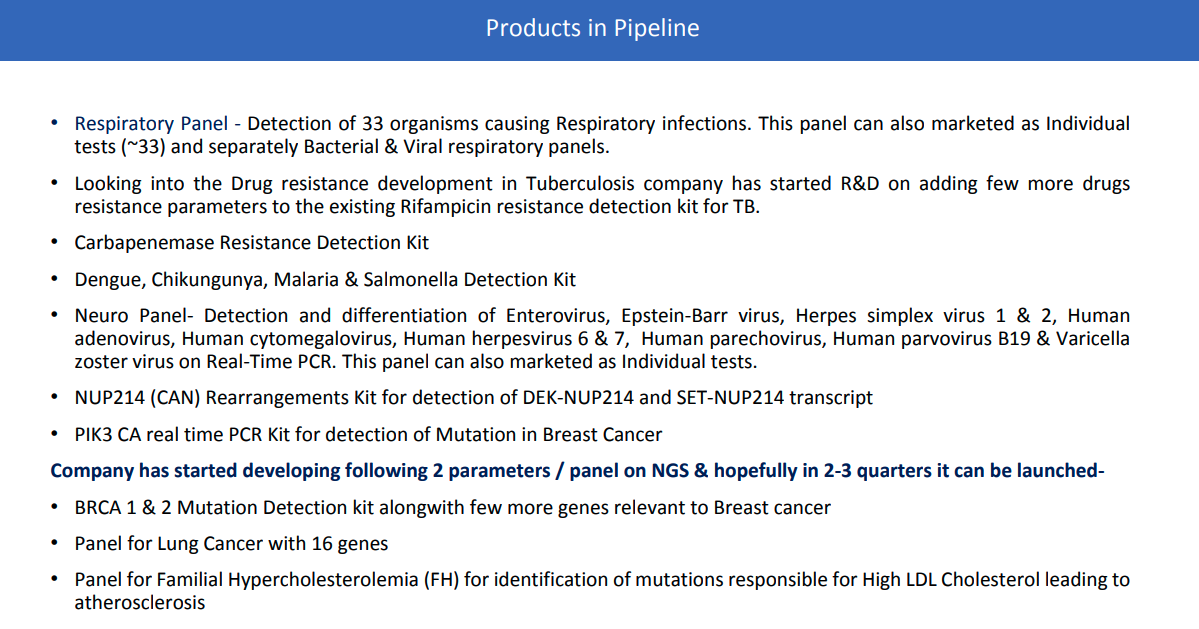

- One of the key products being developed by COmpany is NGS: Next Generation Sequencing. Here is a good video to understand 100,000 feet view of NGS sequencing. In essence, this will enable millions of sequencing reactions to be analyzed in parallel. Of course this is only the very basics and high level view. I would also study in more depth in upcoming months. Company is expecting to commercialize its NGS kits in next 2-3 quarters. Following tests would be first launched: BRCA 1 & 2 Mutation Detection kit alongwith few more genes relevant to Breast cancer; Panel for Lung Cancer with 16 genes; Panel for Familial Hypercholesterolemia (FH) for identification of mutations responsible for High LDL Cholesterol leading to atherosclerosis.

- Inorganic growth opportunities: Company is already sitting on 100cr cash. Will generate more from the last and next few quarters of Covid tests. My estimate is that if we see no new covid waves (hopefully), company will end up with 120cr of cash due to covid tests. In addition they also plan to hive off their Kilpest business. As per valuation report post As per company’s DCF, kilpest alone is worth 5-20cr. This 125cr of cash would enable co to pursue inorganic growth. Multiple options exist. For me personally, best capital allocation would be R&D investment to improve quality of R&D even more (more on that later). Next best would be forward integration by buying a small but high quality diagnostics front end. Would reduce the growth rate and unit economics, but would enable sustainable growth. The probability of terminal value increasing would be high. Next best would be a buyback. Next best would be an acquisition in molecular diagnostics space. This is because they already have a very good organic growth opportunity in their niche. Won’t make much sense to acquire anyone IMO since this is a very capex light business, easily scalable.

Quality and Durable competitive Advantages

Let us try to answer these questions by quoting examples which demonstrate the quality of 3B’s assays.

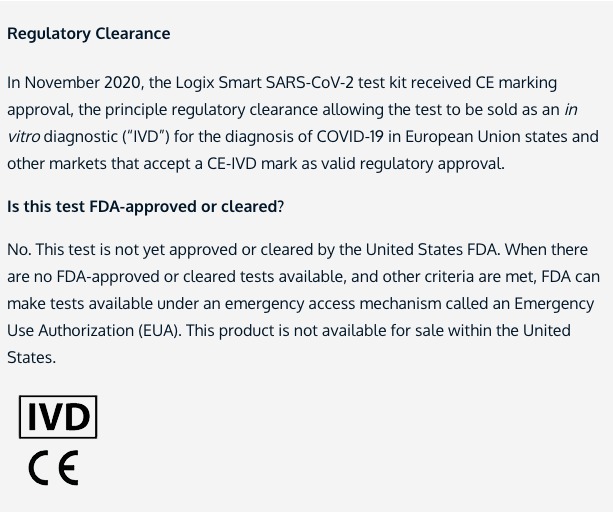

- 3B’s covid kit is the ** first and only (as per my limited knowledge, full verification would require going through 245 companies which I havent done) indian covid RT-PCR kit to be approved by USFDA under EUA**. To understand how difficult this is, I quote 2 examples: One of their American competitors (who make their kits in US and in India) called Co-diagnostics have this on their website for their covid-kit:

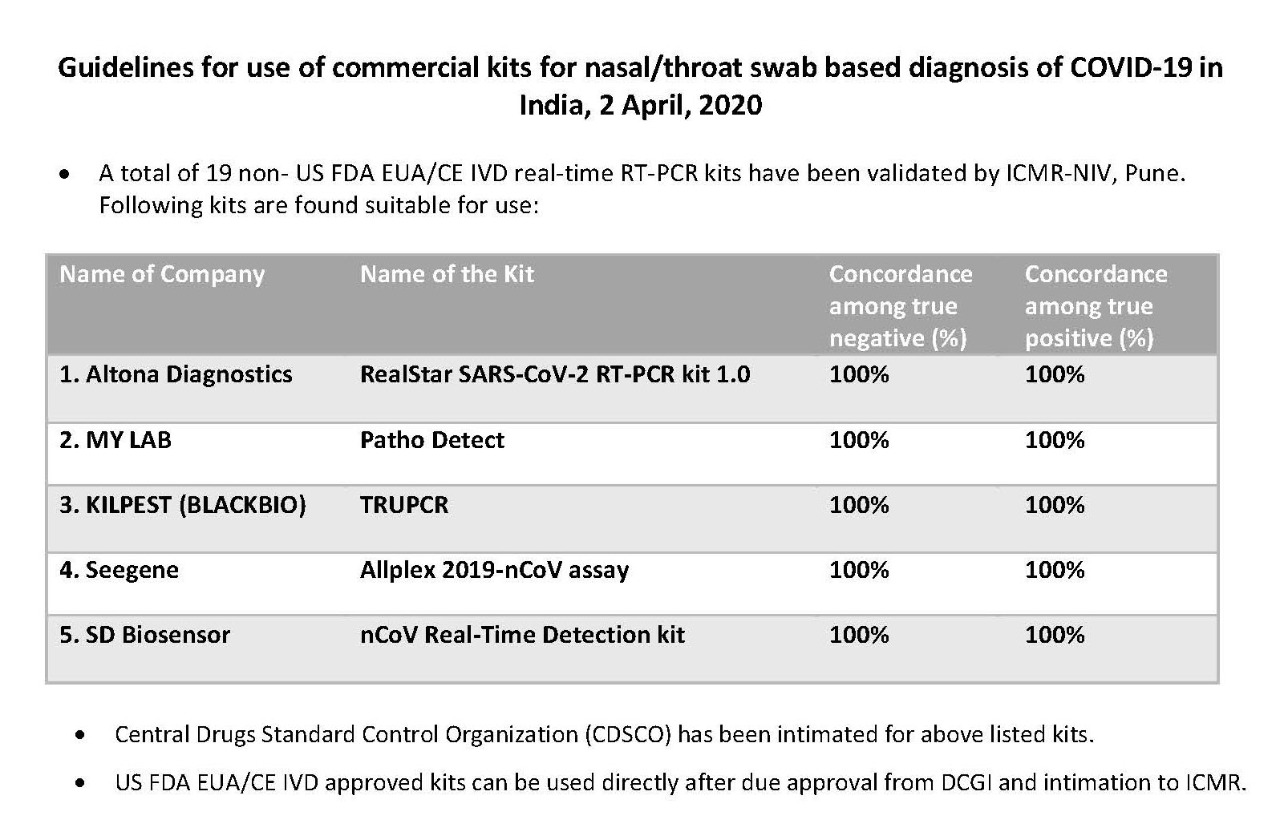

Even American molecular diagnostics company was unable to get their RT-CPR kits approved. Also, from discussions with other members, it appears that MyLab was also trying to apply for USFDA approval, but I can verify that they have not received it. - 3BBB’s TruePCR covid test was one of the first 5 to be approved in India. https://twitter.com/ANI/status/1245782603350839296?s=09 At that point in time, the accuracy required for approval was 100%. Subsequently due to the covid waves, ICMR reduced the concordance with TP?TN required to be 75% and subsequently removed the requirement altogether since we needed more kits. This has definitely reduced the quality of the testing, due to influx of low quality kit manufacturers and chinese kits in Indian market.

- While 3BBB is selling its kits at Rs 70-80, Indian government is procuring kits at Rs 26/27. 3BBB’s refusal to sell at that price point itself points to superior quality of their kits. Also, out of 180 odd kits available in India, only 40 are indigenous: Now, 179 COVID 19 testing kits available in India; about 40 indigenous - BusinessToday This gives us some sense of how many sub-par quality kits we have and that the competitive intensity might be a little overestimated.

- In a recent Video that I was watching, 3B’s head of commercial operations called out that NIV pune used their kits in conducting Covaxin trial. This is a fairly sizable endorsement of their quality.

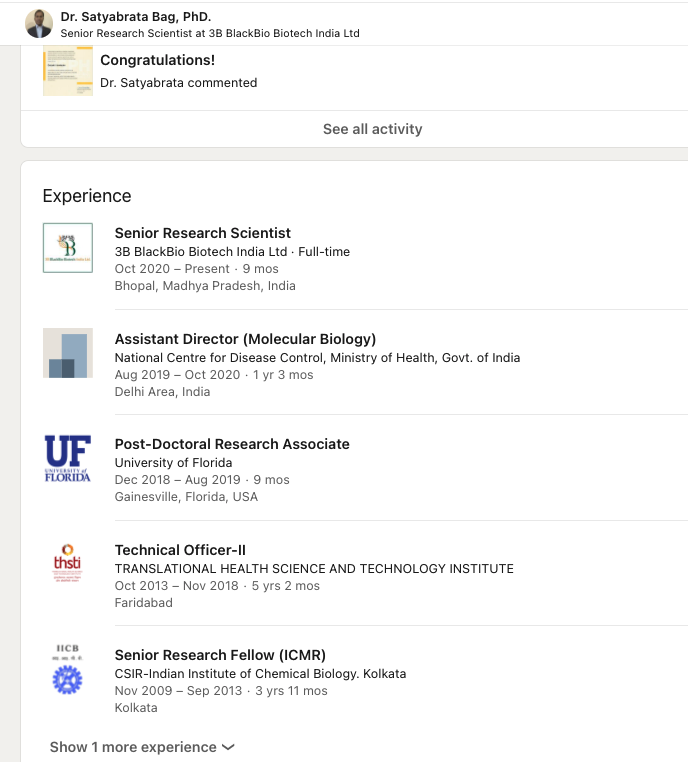

- Their pedigree of employees is fairly great. Just look at the experience which one of their senior scientists comes with:

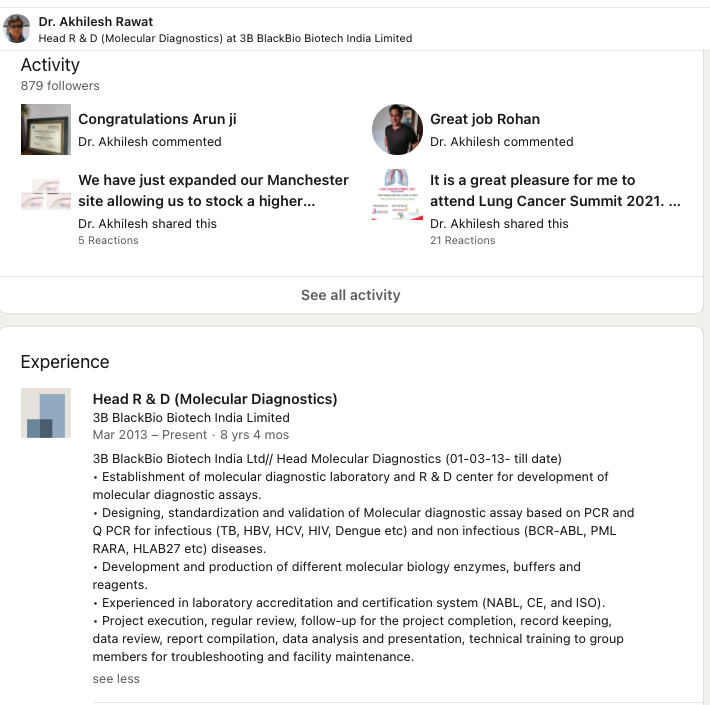

Their head of R&D has been with them for 8 years. Shows their ability to retain senior key management.

- I think the key strength of this company is its employees. And their combined R&D experience rearching, developing, validating and quality controlling the kits. This is core biotechnology. To be very honest i do not understand at a very basic level how one makes an assay. I will work on improving that. But it is clear the company focuses on quality. See this youtube video on quality of diagnostics in India: 3B Blackbio DX Ltd - #444 by Dr.Midhun They QC every batch. They test on client specific machine and model to ensure they are able to guarantee the quality.

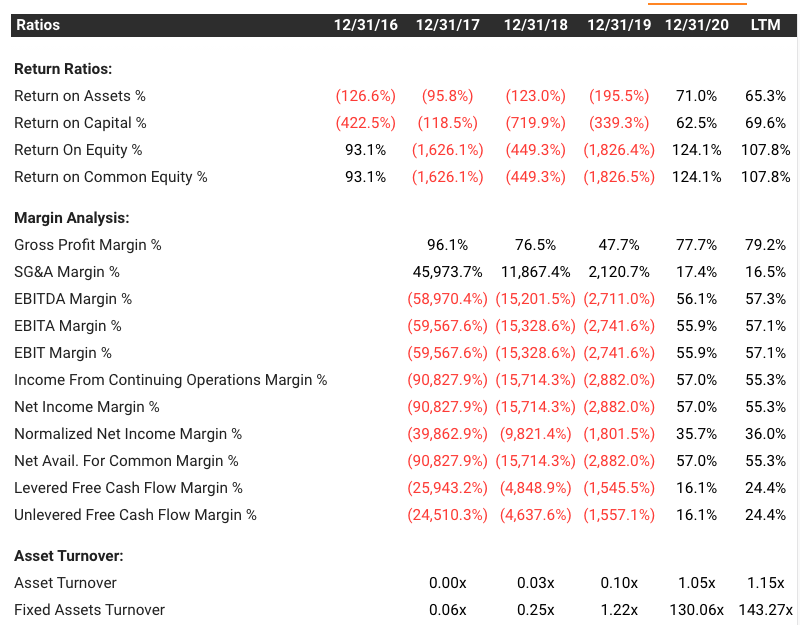

Unit Economics, Margins

Let is answer these through a few points:

- We can observe the US listed similar business co diagnostics pointed out in this post by @ravish and see the tikr website for this co. They have similar fixed asset turns and margins which sort of tells us about the industry structure and the fact that this industry itself is requires More of Scipex (science and scientist expenditure) rather than Capex (Capital expenditure):

. As i also posted about yesterday, the high asset turns are because enzymes required are at microgram level. In essence, reason they were able to scale from 5000 tests per day to 100000 tests per day is because their capacity utilization was hardly 5% or lesser pre-covid. - Margins are high because of the very high value add and quality added. They buy simple raw materials, import the DNA/RNA/genetic material of the disease or markers they want to identify then work to impart their knowledge into this simple set of materials in order so that together it constitutes a testing kit (apologies for the value description; i really need to read or listen or watch on how a testing kit is made). They charge for their quality. As demand for covid tests went up, so would the supply of raw materials have increased, this is why they are able to maintain margins while selling kits at 70 rupees now, versus Rs 750 a year ago. The margins are for the knowledge expertise and quality they impart in the product. While they can only control the output price to a certain degree (at least until they increase their brand power), they are able to control margins, as long as there are no supply chain disruptions.

- Working capital is fairly good for the subsidiary 3BBB. Kilpest has high QC due to the agri business. Just need to subtract balance sheet for standalone from consolidated to work out the numbers.

- Due to the decent WC, very low fixed assets required and high margins, unit economics are wonderful to say the least. ROCE of 117% in December 2021 quarter.

Valuations

Possible simplest section. 120cr of cash, 5-20cr more cash coming some time in next 2-3 years (discount it as you must), a core business growing topline at 30-40% powered by research and development of new products and cutting edge of diagnostics biotech. Non covid business of 35-40cr with PAT margins of 45%, you do the math. Use PE, PEG, DCF, relative valuation (no indian listed peer but do have US ones). Everything screams undervaluation to me.

Key unanswered questions and risks

- Are they able to sell to large labs and hospital chains like Apollo, Manipal, Dr lal, Thyrocare. Are these backward integrated? Similarly, when their current clients grow big, they can decide to backward integrate into testing kits (metropolis already did this by acquiring Hi tech labs).

- Their high-quality indian competitors like MyLab flush with cash could decide to provide larger discounts, worsening the margins and unit economics.

- Microcap so all associated risks. I personally protect against downside by keeping position size small and pyramiding up with consistent business performance and management execution on guidance.

Lastly, thanks to everyone who had offline discussions with me. Although the words here are mine, the ideas and information comes from many people. @aga.ayush11 @msandip @arjun0s and many others. Also thanks to everyone who patiently answered my questions here on the forum. This is what successful collaborative investing looks like Imho. Together, we question each other leading to deeper insights and understanding.

Disc: invested, increasing position, not a buy or sell recommendation.

32 Likes

Great work Sahil, you are definitely lifting the quality of research in this thread.

A couple of points on your note:

-

The valuation of Kilpest’s standalone business (pesticides) is 5 - 20 crore as per the valuation report, the rest of the value comes from its investment in 3B. I would just assign 0 value to this business.

-

Regarding quality and competitive advantages, the efficacy of 3B’s Covid-19 test has been found to be at par with multi billion global giants like Thermo Fisher and Seegene, at a much lower price point. Their test is better than Mylab’s which has Serum Institute’s backing. 3B’s non-Covid tests have also been appreciated in reputed publications. Check out these two posts for more: 3B Blackbio DX Ltd - #338 by enelay and 3B Blackbio DX Ltd - #338 by enelay

-

3B is a research organisation and not an assembly shop. They operate like a typical biotech company, discreet about their operations and maintaining a minimal media presence. In fact, if you compare them to Mylab, one would say that marketing is their weakness considering how much mileage Mylab gets in the press. However, I think this reflects Mr. Dubey’s personality of underpromising and they focus on marketing to their actual customers and not the public at large.

-

Based on what I’ve learnt so far, most molecular diagnostics companies have a very narrow area of expertise with a few products that become exceptionally valuable. For e.g. consider Grail, a company that is making a multi cancer screening test called Galleri. This test is not even commercialised yet and Illumina is buying Grail for $8 billion.

Illumina defends Grail valuation amid much cheaper Exact-Thrive deal | MedTech Dive

According to the company, there is a huge opportunity post Covid given 3B’s large product suite and the expansion in molecular testing infra worldwide. I’m quoting Mr. Prateek Goel (Head - Commercial and owns 5% of 3BB) from this video around the 45 min mark https://www.youtube.com/watch?v=Jd9OaVcCkSs

Pre Covid we always had a challenge of how to expand our business, how to let others know what we do, how to let others use our kits, and how they can utilize our kits. There is a great opportunity standing in front of us post Covid because 3B BlackBio has more than 100 molecular tests, we have the broadest menu in the world to offer from infectious diseases to oncology to human genetics and what Covid did is that it has created the infrastructure across hundreds of laboratories in India. I just saw yesterday the last update from the ICMR website is there are 2400 molecular laboratories in the in the country which were less than 500 before.

We are looking at expanding our business in other segments like oncology panels and infectious panels. Gone are those days when people want to do sequential testing - a PCR test for one parameter then another one and then another one - first organism second organism third organism waiting for three days for the culture to come or if the genetic mutation is not present then look for another genetic mutation. Now we’re looking at speedy recoveries and for that we need speedy tests, so people want more and more information. What we’re doing at 3B BlackBio is creating a lot of panels. Not everybody can afford to do NGS there are very few labs even though there are hundreds of NGS in the market there are very few hospitals and laboratories who are successful in pulling it off because of the cost of the reagents and the proprietary technologies. What we’re doing is we’re enabling labs to utilize their real time PCR platforms and still be able to perform tests on multiple pathogens when it comes to infectious diseases in one test. For example, in our respiratory panel we have 34 organisms in one test. Similarly for oncology, we have gone up to AML panels, ALL panels and leukemia fusion panels where we are detecting 18 - 20 different transcripts, mutations, point mutations, insertion/deletions in one test. What we’re offering is a lot of syndromic disease panels, a lot of oncology panels to our users so that they can utilize the existing infrastructure capabilities what they have achieved during the Covid times to further strengthen their molecular testing.

13 Likes

I clearly mentioned assembly in context to high asset turnover, so that others can understand.

In biotech, only R&D backed companies can survive, its very basic.

I dont use word like “research organization” for 3b as of now.

R&D team always needs expansion. I remember R&D head was unaware about CRISPR.

They are very strong in PCR & NGS.

Disc: Invested since 70 levels

5 Likes

Excellent work @sahil_vi

I would like to share a video on Next Generation Sequencing that tries to explain all the basics and how big of an opportunity it could be. Video has English subtitles.

She also talks about a ‘Nebula version’ which I have watched and she believes that investing in the diagnostic front end companies that actually do the NGS testing would be the best option. She says that she is not an investor.

On a related note Ark Invest’s (US based AMC) owner Cathie Wood has talked about NGS as one of the disruptive innovations for the future, in a podcast. She is invested in some biotech companies with good R&D pedigree including in CRISPR Therapeutics co-founded by the 2020 Nobel prize (Chemistry) winning scientist - Emmanuelle Charpentier. Wood’s critics do note that neither she nor her team appears to have any technical expertise in any of the fields that ARK Invest is invested in.

The specific ‘potential’ here is that in order to make the ‘personalized medicine’ that NGS technology can make, a certain gene type needs to be ‘sequenced’. Sequencing of gene types is better explained in the first video I have linked. It appears that Indian gene type is not very ‘sequenced’ but the European gene type is fairly sequenced. This also includes the European descended population in the North America as far as I understand but genetic variations do exist.

So as time goes on Indian gene type sequencing itself will be a big opportunity and that will require some years worth of work. I am not clear on how NGS based machines / testing panels figures into this but provided that 3BB can launch a good NGS machine / panel, the European market is a high potential space.

All of this is a ‘far into the future’ view but I thought I should add on to this.

8 Likes

I am not saying CRISPR will replace PCR, its very costly and new method.

3b can’t be “Research organization” until they have all answers.

As an investor, my duty is to keep pressing co till the best is achieved.

I even mailed company in past regarding development in lateral flow assays, CRISPR etc and even got reply also.

I have never been negative on company and parked good % of pf here, but much more yet to be achieved …

7 Likes

Another listed competitor Ambalal Sarabhai( CoSara Diagnostics) which is in JV with Co-Diagnostics USA. I am sharing a Video of their Trade Fair presentation it will help to see how easy it could be to do testing with PCR

another link about CoSara.

2 Likes

I will analyze some competitors of 3BBB’s RTPCR kits to understand how they fare. There are so many of them that I am prioritizing by the initial 5 that were approved by ICMR:

-

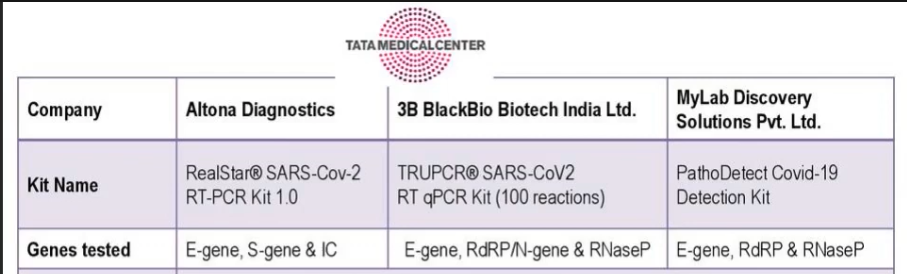

Altona: They do not detect the RDRP gene. As per the video shared by @enelay the doctor mentions that RDRP has highest specificity for detecting Covid among all genes. The altona test does have USFDA EUA so in that sense is as good as TruePCR. Note that it is based out of germany, not an Indian manufacturer.

-

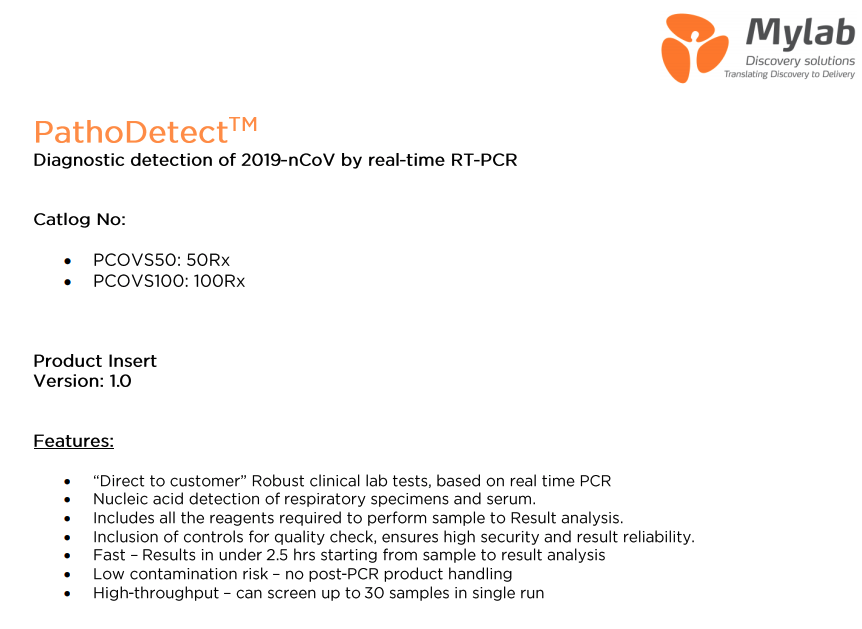

My Lab: While TruePCR has moved to a 1-tube assay, MyLab still has only a 3-tube assay. This is actually higher impact than we realized and is also beautifully covered in the video i linked before. A lab using MyLab RTPCR can only do 30 tests at a time since each test requires 3 tubes. This means 3x lower throughput than latest TruePCR Covid test. 3x lower testing rates. 3x lower revenues for the lab. Also, their tests take 2.5 hours compared to TruePCR’s 1.5 hours. Again, a factor of 1.66x lower revenues and throughput (the video mentions Mylab’s test takes 1.5 hours but all Mylab documentation points towards 2.5 hours so i am going with what MyLab is telling me assuming video made a typo). MyLab also does not have USFDA EUA approval.

- Seegene: A korean listed competitor. BTW, also have very high margins, high fixed asset turns. Verifies our hypothesis about industry wide high margins and fixed asset turns. Co was making decent profits and has decent growth pre-covid as well (this was not the case for co diagnostics). Was valued at 25x TTM earnings pre-covid. This throws some light on what a reasonable valuation for 3BBB might look like in steady state with decent growth (15% top line growth over 5 years). Single tube test. TAT of 1.844 hours (slightly higher than TruPCR). Seems to match TruPCR on almost all parameters.

- SD BioSensor: Korean private company. Also USFDA EUA Approved. Their website gives a 404 error for the covid test product. Here is a google cached version from 31st may 2021. Looks for RDRP and E gene but not the N gene. In this way, slightly inferior to TrurPCR and Seegene. The number of tubes is not mentioned anywhere from what I can tell.

- Co-diagnostics/Ambalal Sarabhai: (not included in ICMR initial approval but including since they are also a competitor: Ambalal does not own the tech or the product. I concluded this because ambalal website redirects to Co-diagnostics whenever there is a link about products or technology. The real brain is Co-diagnostics. As I stated before, their test is not yet USFDA EUA approved. Apart from that, could not figure out how many tubes it uses. Only looks for RDRP and E gene not the N gene and in that way is similar to SD Biosensor test. Takes 1.5 hours.

A next level of analysis would be to figure out what these tests are selling for in India currently. Would enable us to understand whether TruPCR has any cost advantages, specially over the Korean tests which are high quality and similar to TruPCR tests.

Disc: Invested, studying, biased.

16 Likes

Good stuff. This paper might also help as it has other kits from major manufacturers like ThermoFisher and some comparison parameters we can use to get more insights on how these kits measure up in the real world -

https://onlinelibrary.wiley.com/doi/10.1002/jmv.26691

This study results show higher analytical sensitivities, specificity, and accuracy of the TRUPCR SARS-CoV-2 Kit, TaqPath RT-PCR COVID-19 Kit, Allplex 2019-nCOV Assay, and Real-time Fluorescent RT-PCR kit for detecting SARS CoV-2 (BGI)

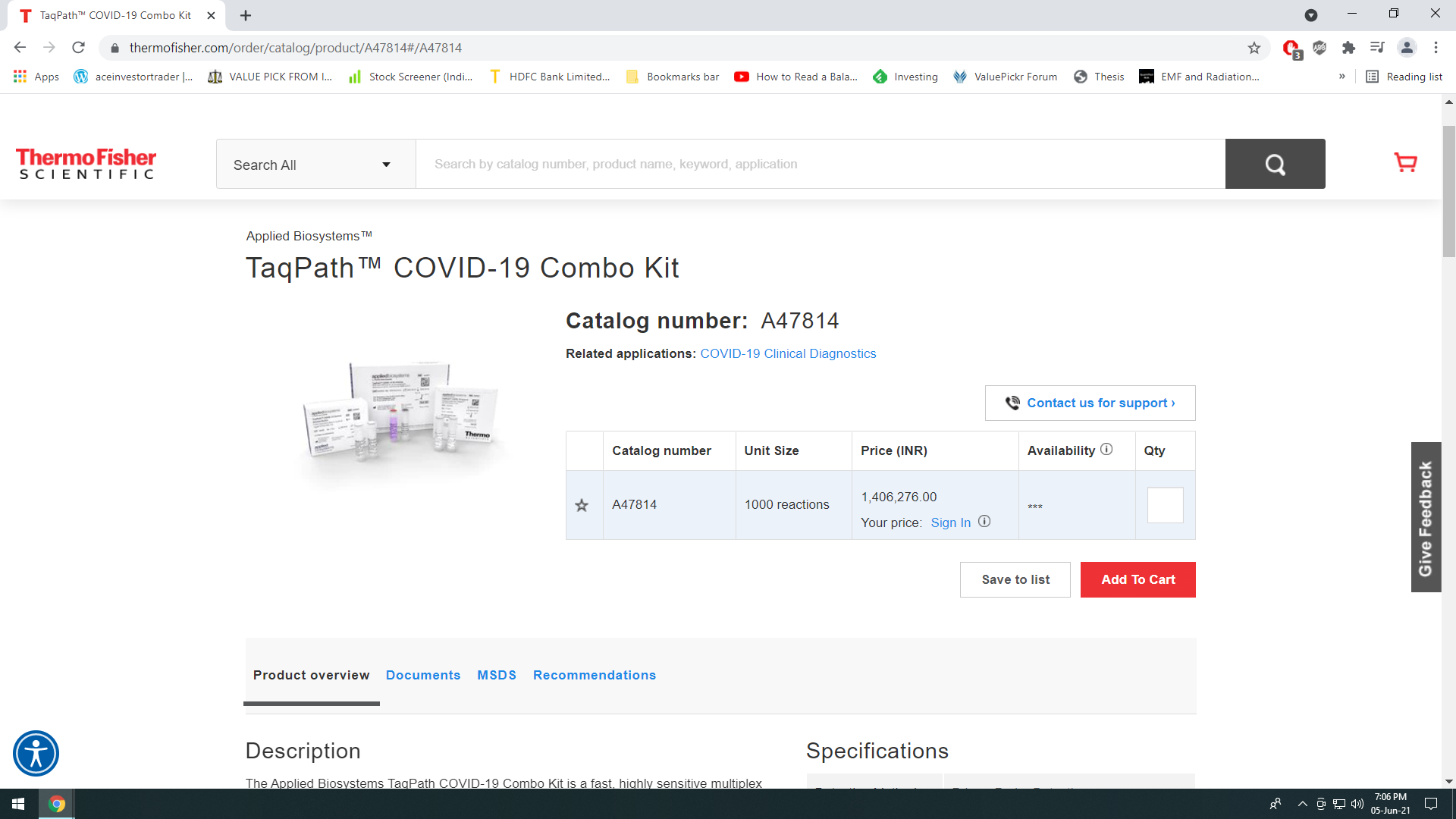

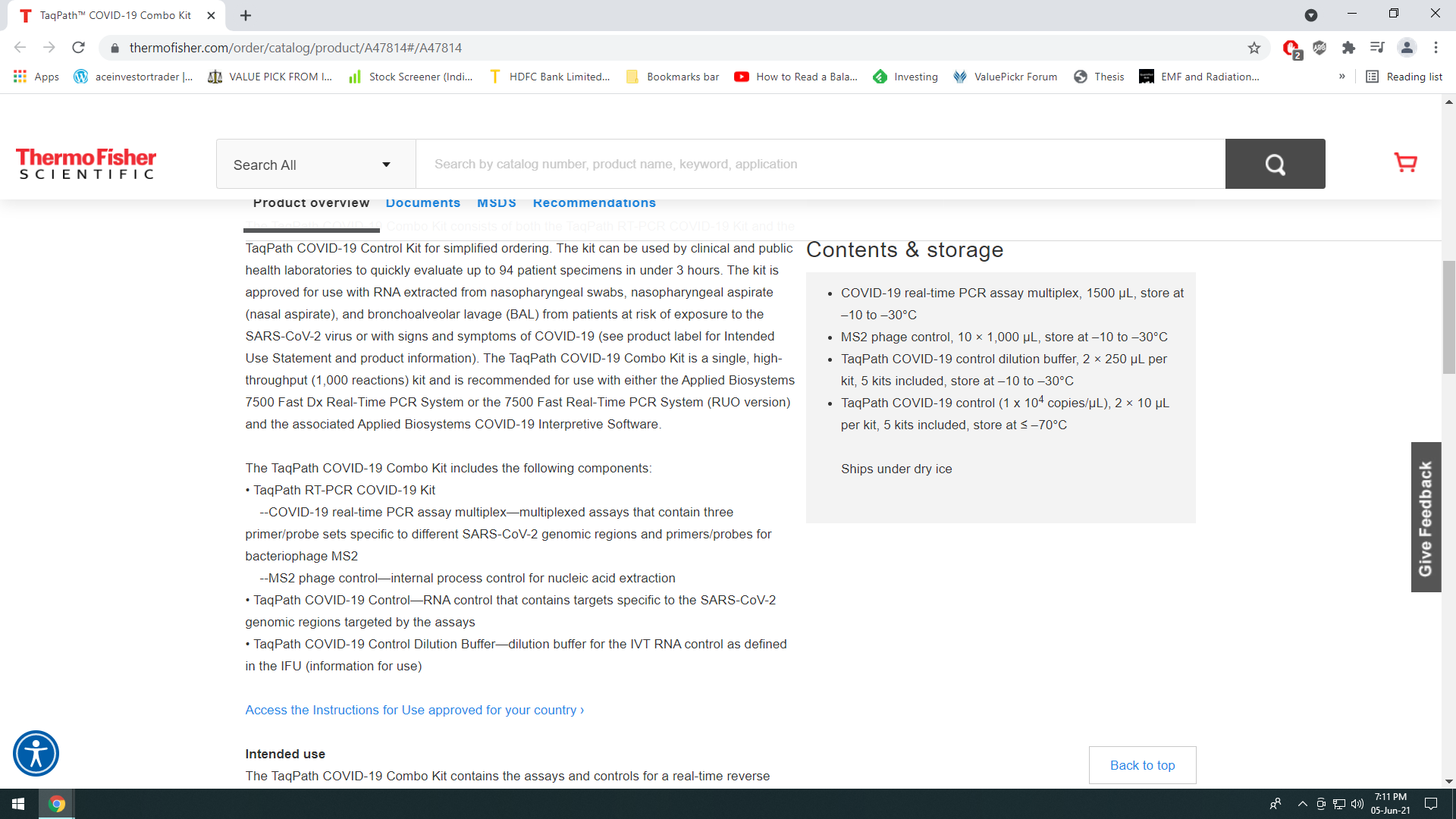

The ThermoFisher kit (TaqPath) can be our baseline on export pricing since it’s the most well known of the competitors and most likely selling in the US/EU.

Edit - TaqPath™ COVID-19 Combo Kit

5 kit combo for 14 lakh INR

- COVID-19 real-time PCR assay multiplex, 1500 µL, store at –10 to –30°C

- MS2 phage control, 10 × 1,000 µL, store at –10 to –30°C

- TaqPath COVID-19 control dilution buffer, 2 × 250 µL per kit, 5 kits included, store at –10 to –30°C

- TaqPath COVID-19 control (1 x 104 copies/µL), 2 × 10 µL per kit, 5 kits included, store at ≤ –70°C

Quite surprisingly, this diagnostics website is giving TRUPCR kits a score of 100% on sensitivity and specificity vs the thermofisher one with 93.5% (no calculations are mentioned so advisable to take with a pinch of salt)

https://www.finddx.org/product/trupcr-sars-cov-2-rt-qpcr-kit-version-2-0-i/

https://www.finddx.org/product/taqpath-covid-19-ce-ivd-rt-pcr-kit/

3 Likes

Thermo fisher costing north of ₹ 280/- per tests. (1400000 for 5 kit X 1000 reactions= 5000 tests.

1400000/5000= ₹280/-)

With the help of @shrikantbhaskar1 and plz refer below link and image.

https://www.thermofisher.com/order/catalog/product/A47814#/A47814

This product contains 5 kits so i am assuming 1000 reaction in each.

1 Like

Thanks how did you get this data ?