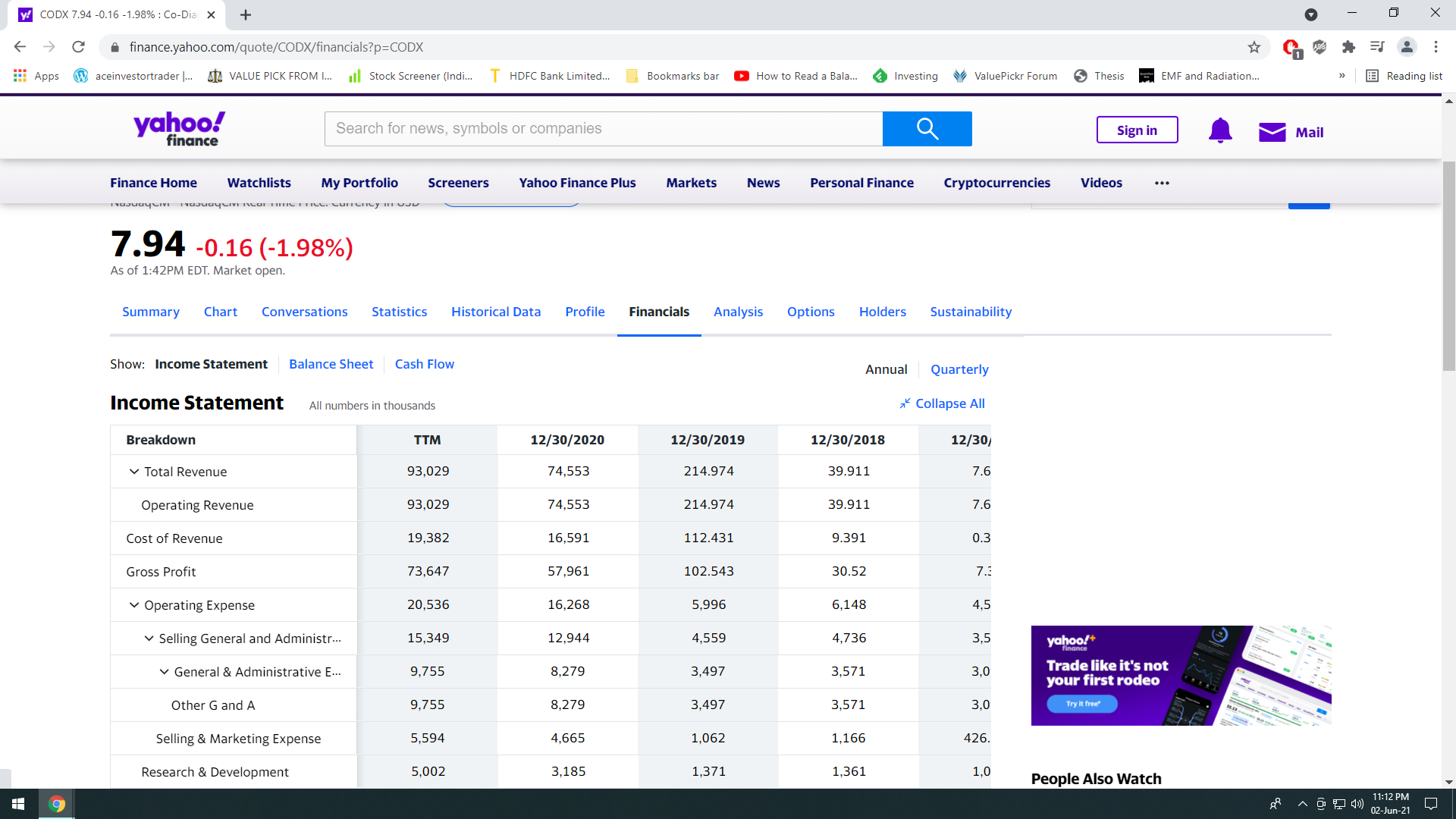

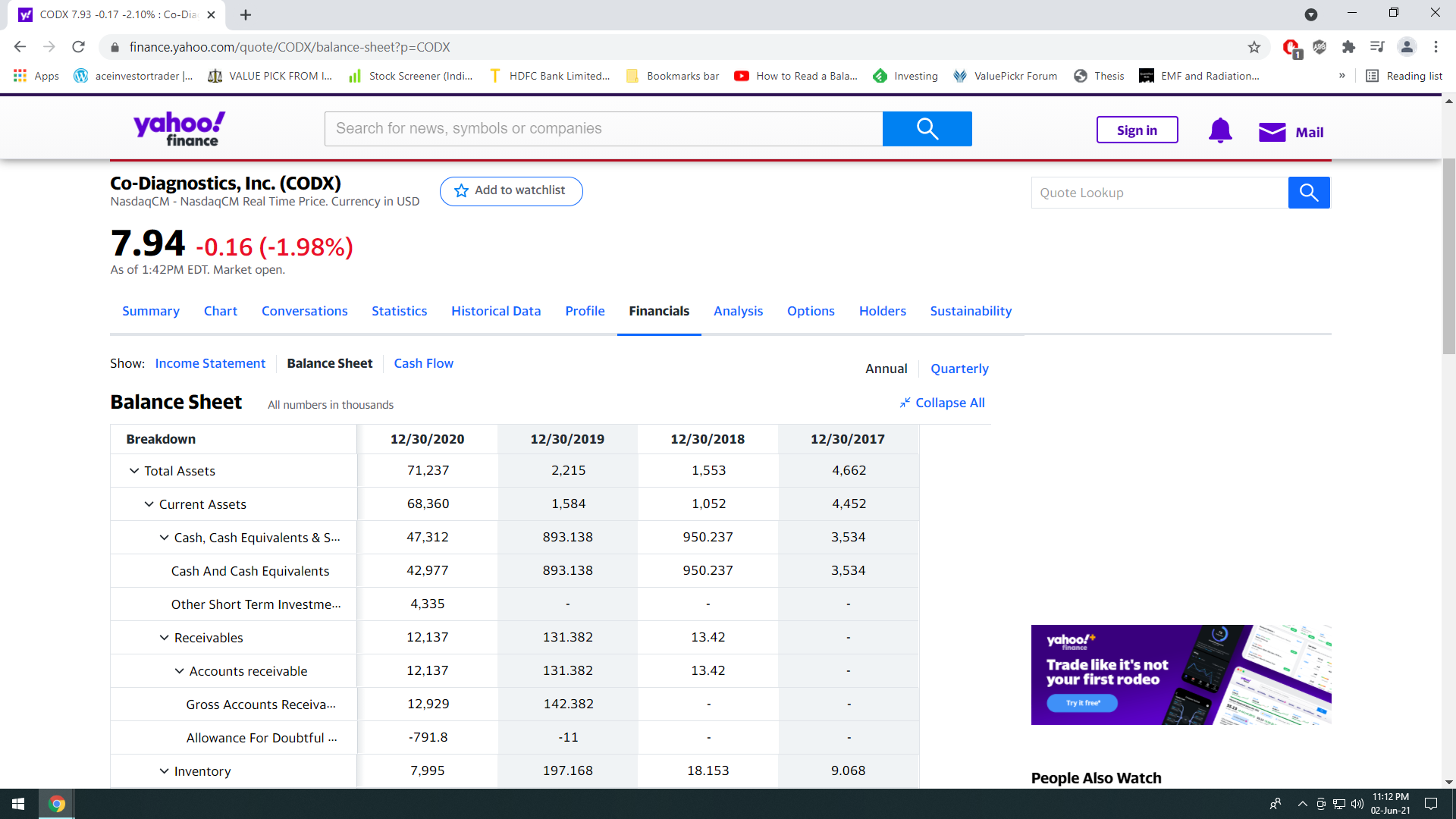

- how can a company have 100x fixed asset turns (look at revenue in Sep quarter, look at fixed assets) and 70% margins.

@sahil_vi Agree on the above point, needs more clarity.

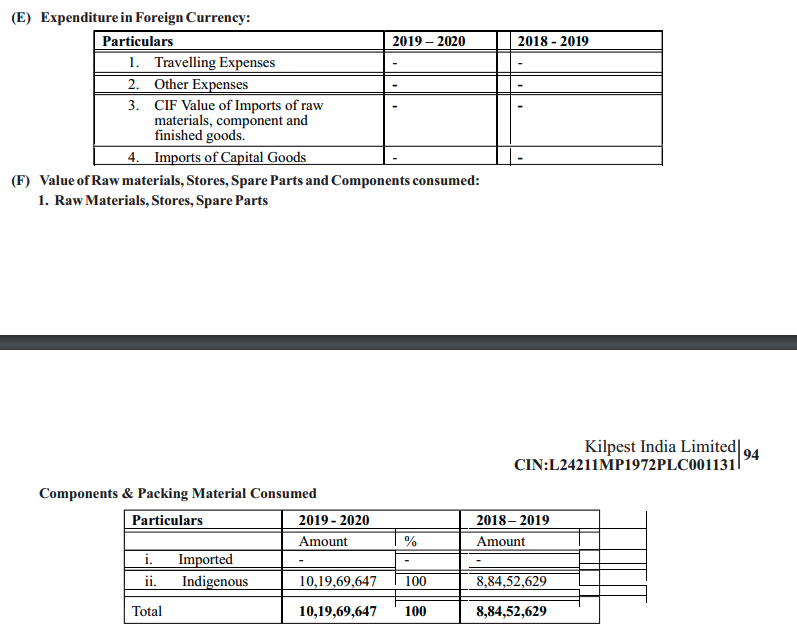

On some calculations from screener their consolidated gross block = 8.32 and standalone gross block = 5.78.

So 3BB Gross block = 2.54 cr

If we take May business update (stable raw material cost and low but profitable realization - 13lakh kits @ 80 per kit), and extrapolate that to a 12 month figure, that makes approx 120cr sales for a 3 month period

So asset turn at this moment is ~47x, still a very high number but we need industry references as biotech seems more R&D and science/IP intangibles based rather than on the gross block.

Plus receivable days is very high too so as their 3b sales increase hoping to see this reduce this annual.

We should ideally get more clarity on these questions in the AR/balance sheet front in the next annual report, or atleast i hope so.

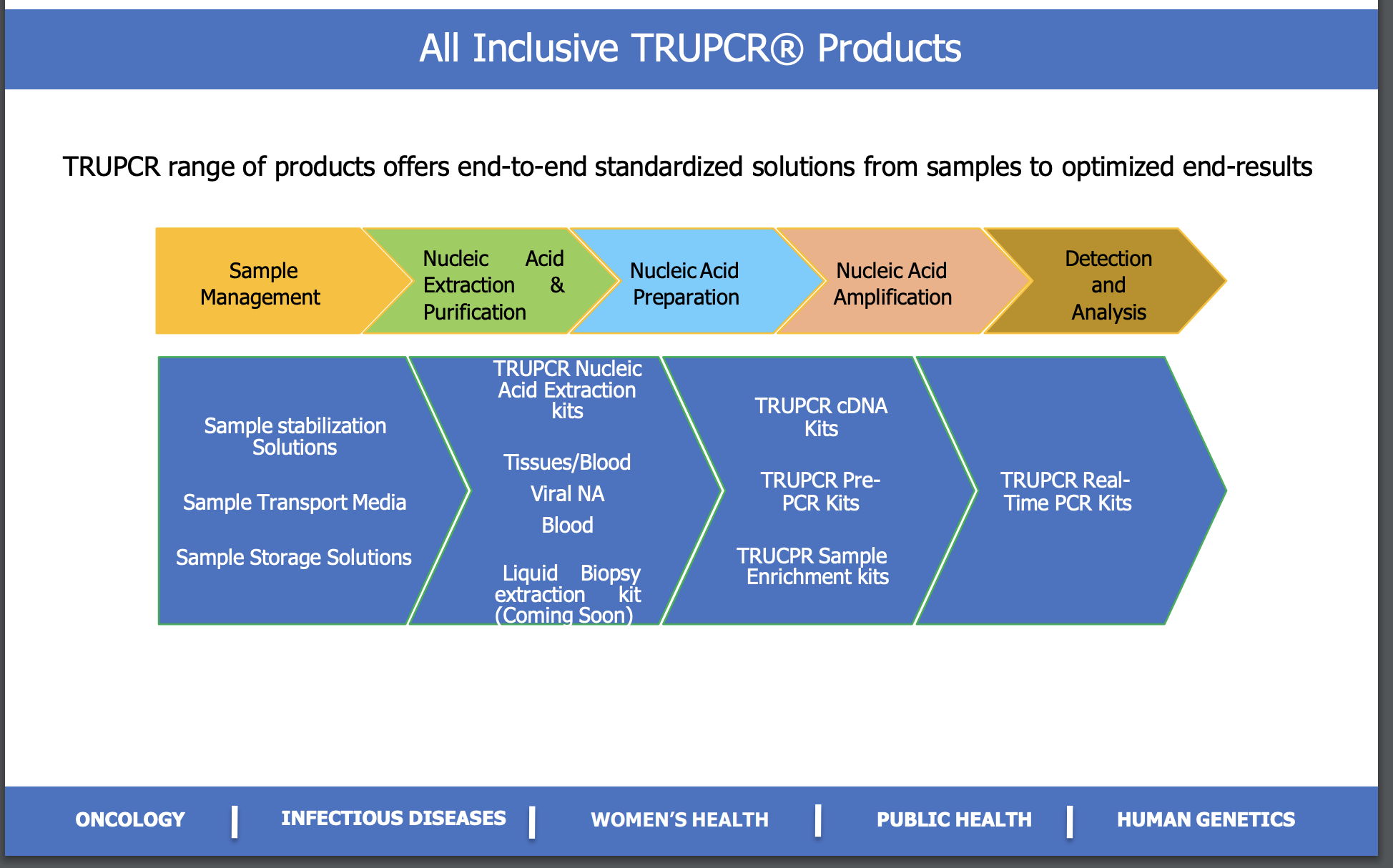

What is the key value add for this company? That seems to be the enzymes which go into the diagnosis kits. Eg:

This snapshot from their investor presentation gives us non-biotech people some insights regarding what their value add is -

r,

Still diving deep to get a more concrete idea about what all work and science goes into these kits but maybe a rewatch of their conference talks might help

I believe the science is key here, so without understanding the entire value chain and the unit economics of PCR (and NGS in the future) kits, we can’t really judge the financials

We do have their MD on record saying that they churned out upto 100000 tests a day, and they also mentioned multiplexing so maybe that’s how the 100000 tests were possible with very few kits?

13,19,000 (Thirteen Lakhs Nineteen Thousand) COVID-19 RT-PCR Tests in the

month of May, 2021 with an average price of Rs. 78/

In their filing, like above they always mention “tests” and not kits, so we would need more clarity before extrapolating to number of kits produced.

In meanwhile would appreciate if anyone could express their opinions on these questions.

In meanwhile would appreciate if anyone could express their opinions on these questions.