Bought this stock around 320 level. resurgence of new covid variant and fresh lockdowns will help get additional increase in the revenue IMHO.

stock is shown good rebound from 290 levels. What i have noticed technically is that there is a change in its earlier pattern of continuous UC and LC since last few months and volumes are consistent. Above 350 stock should be in bulling range. lets see if it reaches this before their next qtr report is out.

Does any one know if government has lifted restriction on export for Covid test kits ?

I got out of Kilpest with 2% profit. i was hoping for change in government policy wrt export but 120 rs per kit is not helping.

I am still hopefull of a very good dividend as this company has habit of giving dividend and they have got more than 110 cr in cash. lets see if there is a turn around and i might invest again.

Could be true cant say but they hae also purchased own shares from the open market for rs 275 but i think that was to expectation of government removing ban on exports of kits .

i have bought very few shares @300,this has a strong support at around 275 to 300 levels ,currently i am treating this as a short term bet with triggers like government allowing on export of kits or a good dividend.

Judging by the past record of the management they have been good in allocating funds and generate good revenues they are planing to invest and if the capex seems reasonable.

But news like these if true can be serious wealth destroyers best example is take solution,plz keep me posted if you see any red flags in insider manipulation of stocks

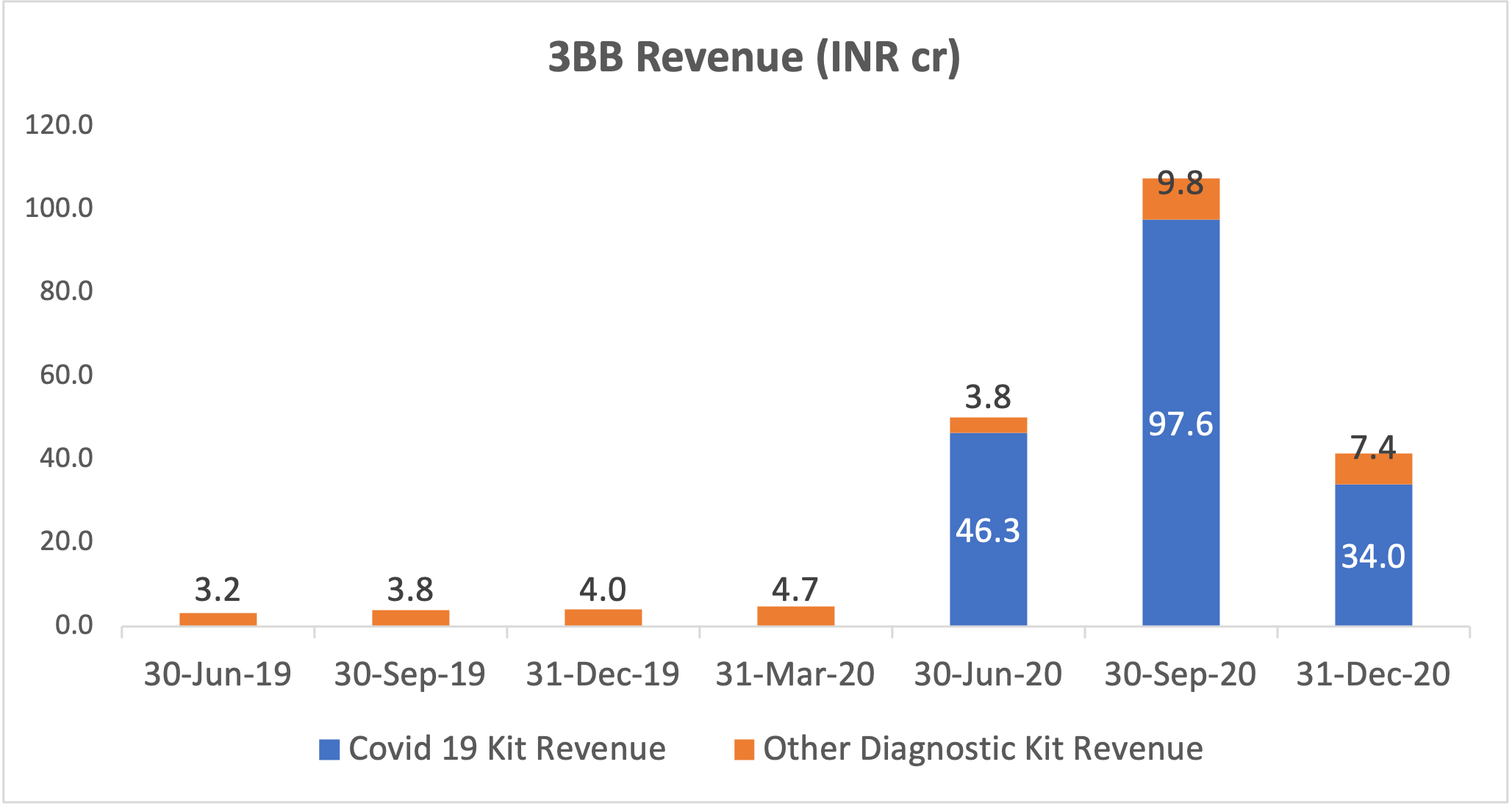

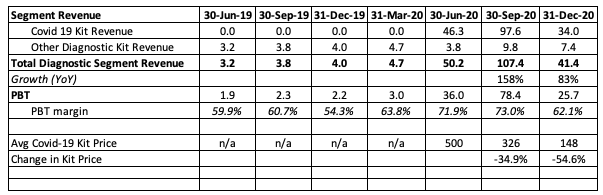

Strong results from Kilpest. Both legacy pesticides and diagnostic kits business have done well. Non-Covid diagnostics business momentum continues (+83% growth YoY).

Number of customers increased to 400+ from 300+ last quarter and 180+ last year

Potential increase in market share in Covid business in India as smaller players might shut down as demand falls. Future Covid revenue should be around 1 cr per month

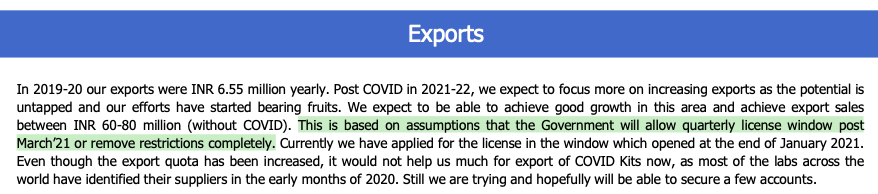

Seeing good potential and traction for non Covid kit exports post Covid, targeting 6-8 cr in revenue vs. 0.65 cr in FY20

Cash usage - Will do an acquisition or share buyback with focus on shareholder return

Expecting a large dividend next quarter

Planning to commercialize TRU NGS and TRU RAPID products in next 2-3 quarters

Good results…

Covid has helped the company to strengthen its balance sheet, getting customers and improving brand image which will certainly help in future growth at rapid pace…

Pre covid growth in dignostics was more than 40 cagr and with such cash balance, company can grow in both organic and inorganic way as sector itself is growing at more than 15 cagr

As company has applied for kit export, we can expect for some orders which would certainly fetch higher margins than india…

one can expect fund inflow after crossing 500 cr market cap…

Very good results and as everyone could calculate beforehand about covid kit revenue i was particularly waiting for non covid biz. I am going to talk about non covid biz now. Historically they outperform their targets this time it is same. One must also notice that the target set by management is on increasing base and are well above their earlier targets of growth. With fast recovery in daily life they could show 100% growth in topline very easily. Comments about cash utilization give us sense of good capital allocation practice. With approx. 100 crore cash we are getting this company at less than 10 PE, assuming 30 crore yearly revenue. With medical sector at boom and higher allocation in budget this looks like a sweet opportunity at present. New product TRURapid may dampen their ROCE but it would be good for faster topline growth and then valuation may catch up. One should also consider that the management is low profile type, after getting in to news for good reasons many times. They have not exploited this opportunity to come on TV and painted rosy picture. Always believed in doing better than saying. I m impressed with them.

A very good pick for longterm.

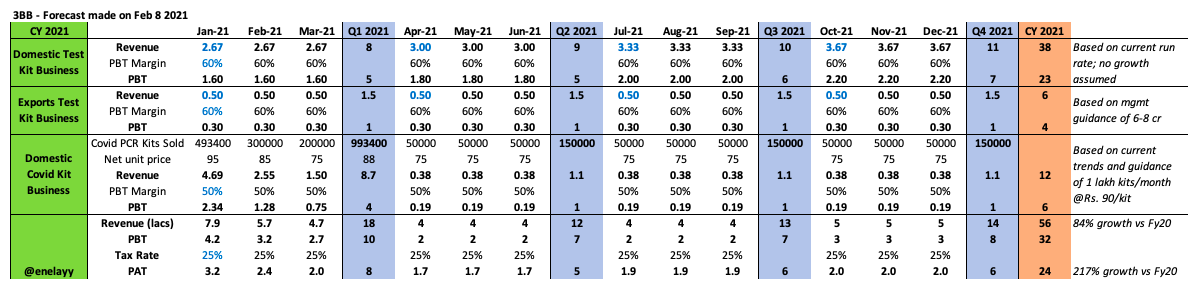

Made some high level projections for the year ahead. Using this to track performance against company guidance and get a sense of how the core business (non covid) is valued currently.

I expect Kilpest do around 56 cr of revenues and 24 cr of PAT in 2021. I think these estimates are quite reasonable:

Ignoring pesticide business (15 cr revenue and 3 cr PAT for FY21)

Ignoring interest income from cash reserves (5-6 cr)

Covid business will continue for much longer than people are expecting

This means that the core business is currently valued at 10 p/e. This business has been growing at 53% cagr for the last 3 years.

Capital allocation - Optionality from 100+ cr of cash reserves

Kilpest plans to deploy cash in FY22 in an acquisition, or if there are no suitable opportunities, they will do a share buyback. The only guidance we have right now is that they are looking at opportunities in the diagnostics sector. To my mind, they are either looking at 1) kit manufacturers to acquire scale / new products / team / clients or 2) diagnostic labs for forward integration.

Dhirendra Dubey & Prateek Goel spoke at this conference. Good insights on 3B’s compliance culture, how they scaled from 5,000 to 1 lakh kits a day last year, process of getting the US FDA approval etc.

This is great development. Means stll next two quarters covid business may continue with improved margin basd on export opportunity. Hope they will find opportunity in non covid business too in US.

Covid has helped in great way in term of customer acquitition, brand building and customer relationship development. Now there is less doubt of non covid business growth. 50 cagr growth seems achievable for years due to lower base and industry growth structure.

Presentation by Dr. Akhilesh Rawat (Head of R&D) on their Oncology PCR kits and an interesting peek into their upcoming NGS panel. 3BB segment starts from 1:48:50 onward

Testing has gone up massively in the last few days and I won’t be surprised to see new testing records in the coming month with the improved affordability and availability of tests.