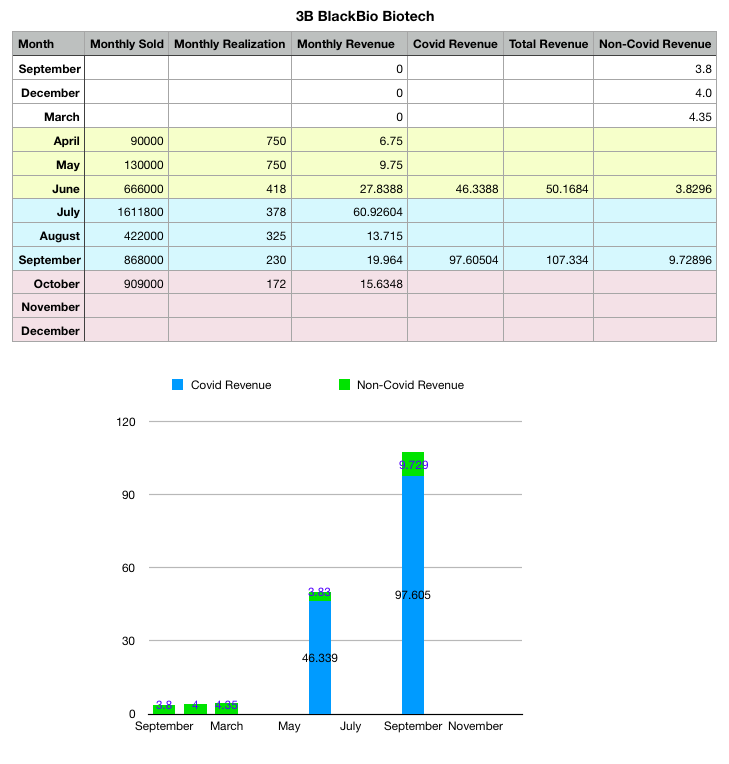

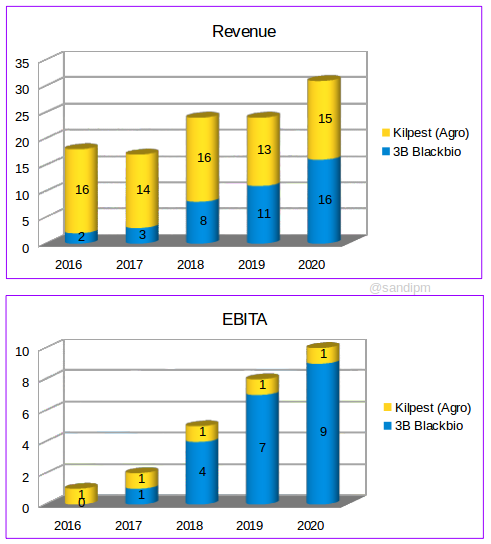

I am also keenly watching the growth in the non-covid business. I think there is some mismatch in your data for covid revenue. I did the same exercise and here is what I’ve got:

The outcome is really encouraging. Operating leverage, raw material price normalization and new customer addition have placed them in an exciting growth path.

Edited: Adjusted the covid revenue of 5 Cr from RNA Extraction Kits for June (2Cr) and Sept(3Cr) Qtr

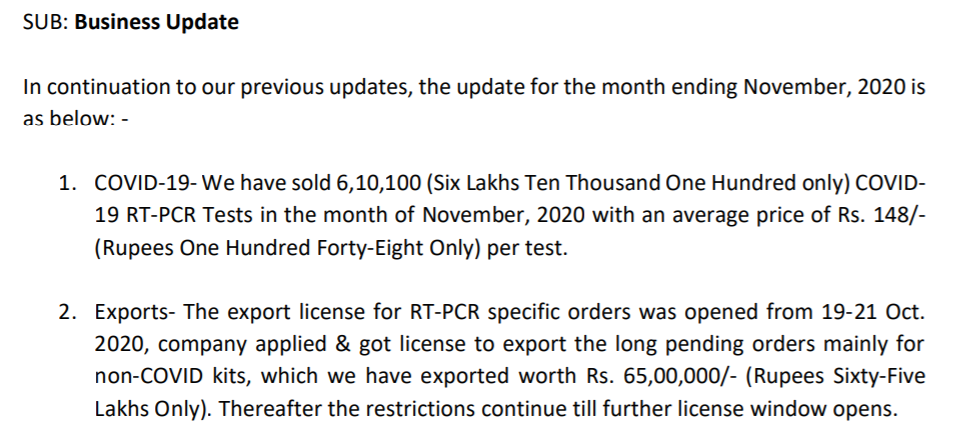

I think that there is a part of revenues in your non-covid data which belongs to the covid related segment. Remember Kilpest is not just manufacturing and supplying RT-PCR kits but also Viral RNA Extraction Kit. They received an order dated 09- 06-2020 for supply of 5,00,000 tests of TRUPCR® VIRAL RNA EXTRACTION KIT from HLL Infratech Services Ltd, on behalf ICMR. Total value of order is Rs. 5.09 crores, including GST, avg realisation around Rs. 100. Source- https://www.bseindia.com/xml-data/corpfiling/AttachHis/9ae5972e-de76-48ae-b817-cb08f502162e.pdf.

When you take this into account, the growth replicates their historical growth rate which was around 40-50% for FY19 & FY20.

You are right about the RNA kit revenues which I’ve included in my calculations now. I’ve taken 2 cr in Q1 and 3 cr in Q2 for this into Covid revenues. They’ve not announced any further sales of RNA Kits post this order which was for the govt. Growth in Q2 in non-Covid is still 150% over last year’s base after this adjustment.

The Pfizer vaccine will not make its way to India for logistical and commercial reasons. At $39 for a two shot dose, it is out of reach for the Indian govt. Our current best hope is the Oxford University vaccine at $2-$5 per dose.

Given the cash in the hand of the company, if they can expand business in Latin America and Southeast Asia, growth will not be a problem. Kilpest may get enough time to switch to other businesses.

As recent analysis suggests in the below article.

Heathrow Says Covid Tests Needed for Years Even With Vaccine.

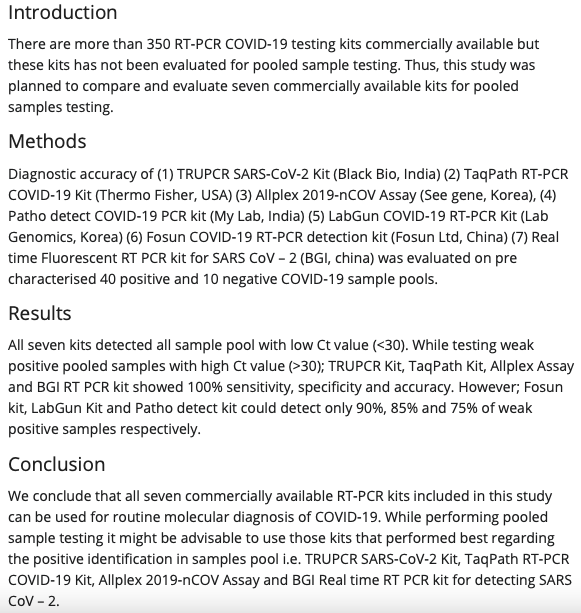

Further to my previous post about Tata Medical Center’s evaluation of 3B’s Covid-19 test kit quality, here is a newly published peer reviewed research article “Evaluation of seven commercial RT‐PCR kits for COVID‐19 testing in pooled clinical specimens” in the Journal of Medical Virology. Reproducing the exec summary below. Full report available here: https://onlinelibrary.wiley.com/doi/10.1002/jmv.26691

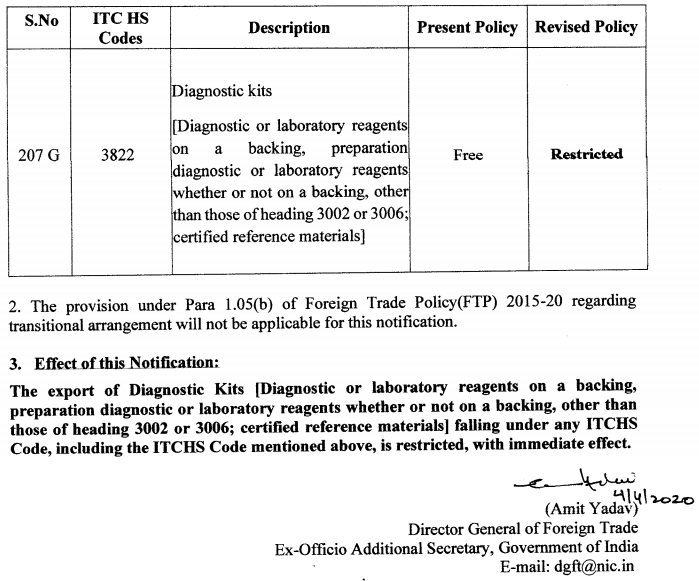

Export restrictions are major show stopper for kilpest. In international market their kits can fetch far higher prices, given the top class quality and performance of their TRUPCR kits.

The inroads into export channels would have created long-lasting and sticky customers.

I hope given the glut of kits in india at throwaway prices, exports should be liberalised.

Why I consider kilpest management honest and ethical:

This is very subjective and there cant be any yes/no type of answer. Specially for a microcap company, its really difficult to get much information about the management. But we have to gauge them from their various small steps and take a clue.

Few things that I have noticed for Kilpest management:

Mr Dhirendra Dubey and his brother nikhil dubey didnt take any salary from 3B Blackbio for the first 5 years of its operation, until the company became profitable. Even after that the salary was not much. They added incentives of max 1% of net profit in 2017 and increased it to 1.5% ,this year.

Kilpest withdrew Care rating after submitting the lenders NOC, what I noticed for small companies, they just dont cooperate with the agency when dont need any further loan (recent example is kanchi kapooram), as withdraw and if needed re-initiate rating involves some cost and they try to evade that. Officially withdrawing rating is a good sign of corporate governance, is my understanding.

When pandemic hits us, they pro-actively given a clarifiaction to the exchange that they are yet develop covid kits, as they already had some other kits having name coronovirus. They continued this transperent communications to all stakeholders on every business development.

Dr Akhilesh Rawat (PhD, Molecular Oncology), head of R&D in 3B Blackbio is associated with the company since last 8 years and almost all the senior resources are associated with the company since long (chekced in linkedin) indicating low attrition. I was reading this book, Intellegent Fanatics Project by Ian Cassel and found one common trait in all the intellegent fanatic is that they cared for their employees extra-ordinarily. I believe, to create a successful and sustainable business, there have to be a motivated and proud human resource pool for a long time, which kilpest have, it seems. They recently pulled off some good talent (ex. Dr. Satyabrata Bag, PhD in molecular microbiology)

Excellent points which I completely agree with. To these I would add:

Consistently downplaying their results and not providing any exuberant guidance. On the other hand we see blue chips touting 90% of pre-Covid levels as bullish.

A fair and clean restructuring proposal of the company which did not shortchange minority investors.

No unnecessary media appearances or press releases. For e.g. it is quite remarkable that the efficacy of 3B’s Covid-19 test has been found to be at par with global giants like Thermo Fisher and Seegene, at a much lower price point. Their test is better than Mylab’s which has Serum Institute’s backing. 3B’s non-Covid tests have also been appreciated in reputed publications. However, we did not hear these things from the company and had to dig them up ourselves.

I’m keen to see how they plan to allocate 100+ cr of surplus cash given that its not a capital intensive business. Should expect a nice dividend at year end for sure.

I do not see such regular business updates from many blue chips as well.

Going by their track record, I am confident about the utilization of funds in hand.

They may speed up on completing the amalgamation as a diagnostic company and listing it on NSE as well and that might attract other institutional investors.

I hope the Government eases the regulations for exporting the kits.

I am pretty sure market will give the fair valuation to this gem.

Are we at the end of a bullish trend in Kilpest? With the stock performance it looks like that it is a temporarily hyped stocks likes of Mangalam Drugs, Intense Lasa etc. Perception of the market changing with every Months update…Did market think of it as a Punters stock? @ayushmit Sir plz throw some light here.

The company enjoys high margins, which is attractive to competitors.

High debtor days of more than 6-8 months is alarming. While this may be due to their marketing strategy, I am hoping to see these going down given that the visibility of the company in their customer labs increased manifold during the pandemic.

The market size of their products seems to be small/uncertain. IMHO, PCR test is more suitable where even small contamination or infection has to be identified, such as in forensics and probably in oncology.

The company has been partially lucky that RT-PCR has been the preferred way to test for Covid in many parts of India (and the world), leading to a huge opportunity that the company took benefit from, generating approx Rs 100cr in cash. Except for lack of exports, the results during the pandemic exceeded investor expectations.

Here are a few impending positive news that may lead to re-rating over the next few months:

completion of amalgamation and name change to 3B Blackbio DX (This will increase the visibility of the company in the eyes of more investors),

start of exports which will act as a stepping stone for new revenue streams in the future,

launch of new products like NGS, antigen tests, thus increasing its target market size, and

utilization of cash for acquisition of a company having complementary capabilities.

Going ahead, the company must focus on risk reduction, primarily of the small market size.

Kilpest might not be directly comparable with those commodity players, as the company was rapidly transforming to be a molecular diagnostics player over the last few years. Current valuations can be justified even with the earnings from non-covid business, growing at 40% annually.

Thank you, @msandip for your comparative chart. Many of us are comparing with HEG. Even the Forbes article which you posted above also mentioned the same things. But in my opinion, there is much fundamental difference between the two comparisons. HEG made a significant profit from a one-time price surge

]. Though they made a significant amount of cash, I think they cannot increase the capacity because of not increase in demand. Secondly, they were not able to convert it into other business. However, In the case of Kilpest, even if we are thinking of subtracting covid from the business, it has an opportunity to convert the cash into other diagnostic business. As per the track record, they are capable of doing so. Even at present, the valuation of Kilpest, COVID minus diagnostic business, is at par with other diagnostic businesses. In my opinion, as they were able to catch the COVID opportunity, with their experience, so quickly, they will also be able to catch the other opportunities efficiently. The long-term prospect is still intact.

HEG did not have the opportunity to jump a similar kind of business as HEG’s business is capital intensive. See the asset-light nature of diagnostic business.

Everything will depend on the strategy taken by the management.