Regarding the criteria for circuit revision, via BSE:

These pro-active measures are taken based on the analysis/ processing of alerts generated based on various parameters and other inputs like news, company results, etc. The broad parameters considered for generation and analysis of alerts are price movement, top ‘n’ turnover, Securities traded infrequently, Securities hitting new high/ low, Securities picked up for rumour verification, etc.

Not very clear if you ask me.

The Securities picked up based on the preliminary analysis/ enquiries are forwarded to the Investigation cell for further examination/ investigation.

The site is supposed to give detailed rationale of the surveillance action but there are no such details.

Personally, I dislike these 2% filters as they prevent price discovery, and are unseen in other stock markets.

HS BioLabs expansion into Europe is good news for 3B Blackbio / Kilpest in case exports of Covid or non-Covid diagnostic kits start soon in a big way. Thanks to the government controls, it is already quite late for Covid exports, but I hope start of exports is just a matter of time.

Is it more feasible for 3B Blackbio to export the ingredients of the kits, and then HS BioLabs assembles them in Europe?

Having already displaced a number of global diagnostic suppliers in the UK with TRUCPCR, HS BioLabs is set to replicate the same success throughout Europe.

Not sure if the above is really true given that 3B Blackbio does not have large exports revenue in the past.

I am holding this share since long time when it was at 26 rupees and I was not having any clue of fundamental analysis.

At the moment though company looks well positioned to establish itself as a brand in diagnostic space.

USFDA approval for its kits also tells us that it has quality manufacturing and procedural practices.

And even if Covid goes away or there will be a vaccine or alternative cheaper methods like blood oxygen level/x-ray scan for early detection, world population and corona spread is so huge that sales won’t vanish overnight, plus once one method gets established for detection of decease it stays there for some time. So I believe the sales engine will keep firing in coming years.

Plus the kind of cash company is generating, it will give management confidence to expand/acquire.

With PE of 9-12, and even half the sales of FY20-21 in coming years, I feel stock has room to go higher.

Since I am holding this since ages, I am positively biased

This article throws some light on the gov’s dysfunctional kit procurement program. Mumbai is facing a shortage of RT PCR kits after the lowest bidder in a recent 12.5 lakh kit order (GCC Biotech) supplied faulty kits with high false negatives. Similarly last month POCT Services was banned after they won a tender for 12.6 lakh kits @ Rs. 78/kit (!!!) and then later refused to supply the kits. Another interesting data point for Maharashtra is that 50,000 out of the 90,000 tests per day are RT PCR tests with the rest being anti gen tests.

This kind of crazy bidding at Rs. 78 is probably why 3B is avoiding the gov procurement channel and focusing on private labs where there is enough demand and sensible pricing.

This also suggests that the quality of 3B’s tests is high to be accepted by the private labs without any issues so far.

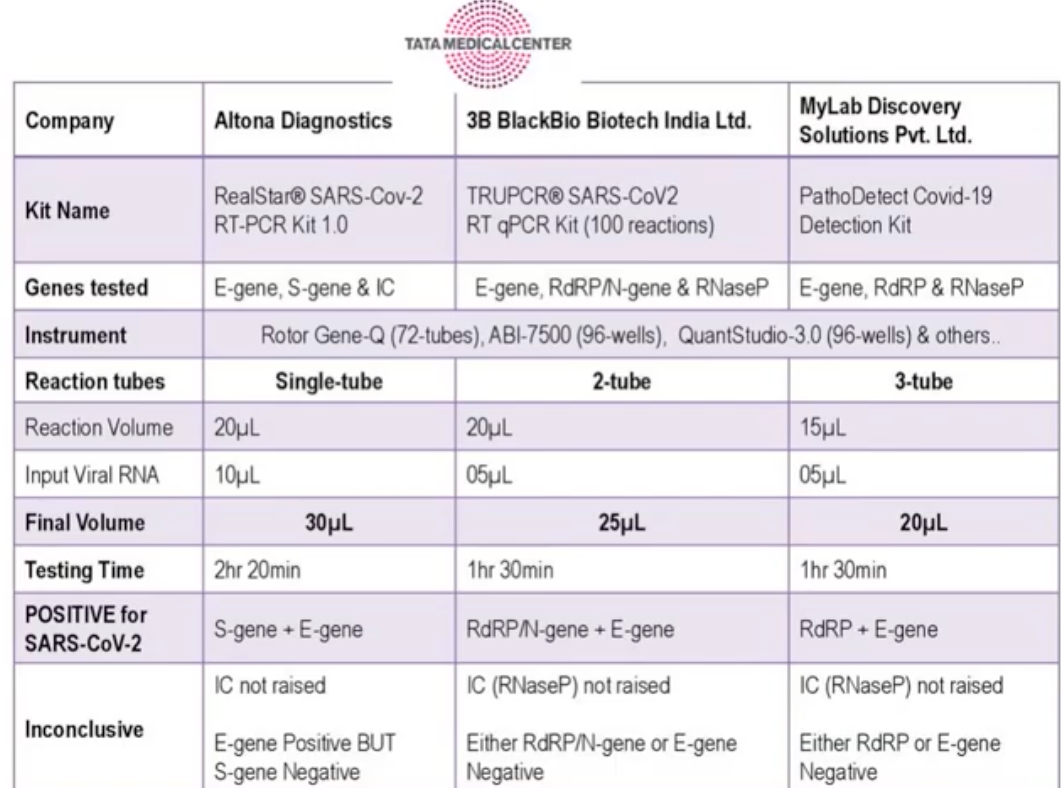

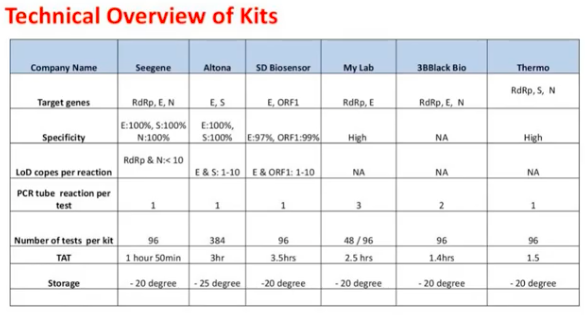

I saw an interesting video recently from Tata Medical Center (Kolkata) where a senior doctor compared various RT PCR test kits being used in their lab - Altona, 3B BlackBio, MyLab. TRUPCR is one of the kits discussed and this is a good watch for anyone who wants to understand RT PCR testing in detail. Note that the video talks about TRUPCR v1.0 (2 tube assay) after which 3B launched v2.0 which is the single tube assay (the presenter mentioned this as well).

1 tube assay is always superior - less time and less manpower required. Number of tubes is directly proportional to the amount of time taken to set up the assay - i.e. 3 tube = 3x the time required vs 1 tube. Someone using the Mylab kit will run 100 tests in the same time it takes to run 300 tests on Altona / 3B. Each tube is set up manually which compounds the risk of lab error in multi-tube tests as well.

Tests targeting the RdRP gene have the highest analytical sensitivity

3B test has the lowest turnaround time of 1.4 hours

Their lab is using these 3 kits for their technical superiority and price. Need to use more than 1 vendor because availability of kits is sometimes difficult.

Seegene kit (the one used widely in Korea) is good but requires a RT platform which is not widely available in India. Selection of kit depends on RT instrument available in the lab.

While testing could peak in the next few quarters, the pandemic is likely to have a long tail. Only a widely available vaccine is likely to damp demand meaningfully, and even then it won’t erase the need for testing. It’s possible that one of the front-runners in vaccine development will gain emergency authorization by late November, but that’s a best-case scenario. Relatively few doses will be available at first as drugmakers ramp up manufacturing, and distribution will take time. Vaccines likely won’t be broadly available to the general public until a fair bit of 2021 has passed, and it will be even longer before most receive it. The hard truth is that it will be a while before the virus is well-controlled, vaccine or not. In the meantime, testing is a good business to be in.

This is what I have said before…testing won’t be stopped for near future. I have said many times that this management does talk less and do more. In my thinking new products like rapid test and results in few minutes will be more beneficial as per the above article MNCs are minting money through innovation. The company is in sweet spot and management has a long experience they knew this biz…they have started MBD biz in 2010 and knew it from core…if we go through annual reports and presentation u will notice that they have been managing well all the way and guidance were always beaten by huge margin. My money is on the management now…as company has given me multibaggar return. Management can make it big. Just think how much money can be made by Export. Once the export ban is removed this share will give us tremendous return.

Disc: Holding …trimmed my position due to overall market rally.

Business update for Oct out. Kilpest sold 909,000 Covid-19 tests @ average price of Rs. 172 in Oct -> total sales of 15.6 cr. Highest single month sales barring July which had the large tender order. Prices have corrected in line with market trends.

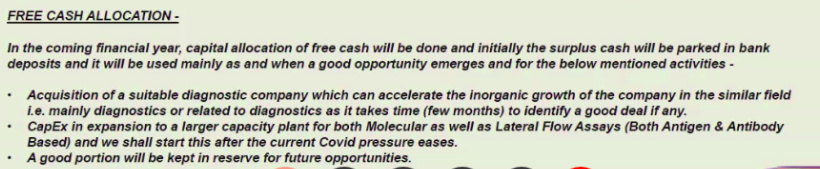

So much cash is in hand. They have not declared dividends. Is the company has a new CAPEX plan? In the presentation it is written: Business started in Middle east, Southeast Asia, USA. Negotiation is going on in Latin America.

Earnings and cash are in the books of subsidiary i.e. 3B Black Bio ltd. First they need to receive the dividend from subsidiary to be able to pay to the shareholders of parent. Alternatively they may wait till the merger of subsidiary with the parent.

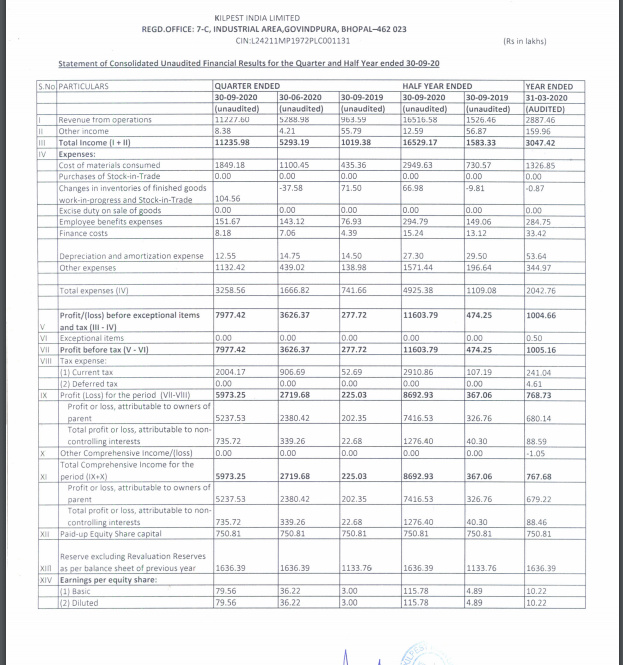

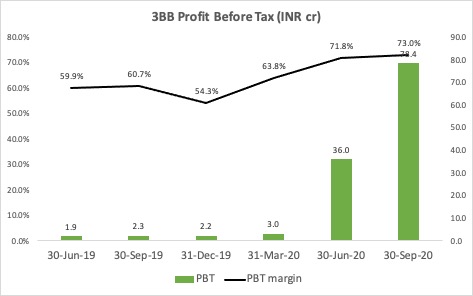

Superb results, again ahead of expectations especially on the margin front. A few things which are exciting for me:

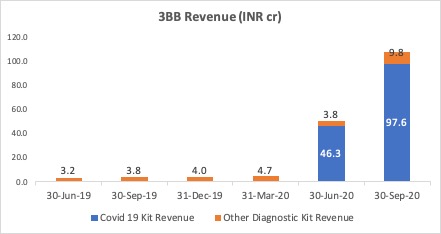

One of the key questions for us is whether 3B is indeed moving to a new growth path post Covid and how do we start to value this future growth. In other words, how do we see that Covid is not a “one-off” windfall? One significant data point is in the expansion of their customer base to 300+ from 152 in FY 2019 (+100%) and 180 as of March 2020 (+50%). More tangibly however, this quarter we can see that Non-Covid Test Kit Revenue is at its highest level ever, growing 158% YoY. I derived this number by subtracting the Covid Kit Revenue provided in the business updates from the total diagnostic segment revenue published in the results. Clearly, they are now pushing their core product portfolio to their newly acquired clients.

In the Covid business, the prices of kits have crashed from 600+ at the start of the pandemic to Rs. 172 in Oct-20 as per the company’s latest business update. While there were a few news articles talking about how reagent prices in India have fallen drastically because of oversupply, one of the obvious concerns was how the company’s margins would look in Q2 (and going forward) with kit prices falling so rapidly. From the results it seems like input costs have fallen nearly proportionally with prices and coupled with operating leverage, margins have actually expanded in Q2, while the avg price of kits sold by 3B fell from 500 in Q1 to 325 in Q2 (-35%). While some margin compression may be expected in the coming quarters (lower scale & prices), they should remain in a healthy range.

Absolutely stellar work in converting sales to cash and transforming the balance sheet. Net worth up 4x to 120 cr, 102 cr cash generated from operations, 29 crore paid in taxes for H1 (more than their total revenue in FY20 lol), 80 cr cash in the bank.

The cherry on the cake is that their legacy Agrochem division also had an excellent quarter. When it rains it pours…

Looking forward, the company seems to be on a strong footing with continuing Covid business and accelerating Non-Covid business. They have their hands tied by the govt on the huge export opportunity and hopefully that might change at some point as well. We should be vigilant about capital allocation plans and updates on the restructuring process. Listing on the NSE will give a nice fillip to volumes and attract new investors.

The words “transformative” and “inflection point” are used so carelessly sometimes that one doesn’t give them much weight, but in Kilpest’s case these last two quarters have truly been night and day in the history of this nearly 50 year old company. And yet, there is no drama or excessive marketing from the management. In fact, there is almost no change in their tone at all. Impressive

Disc. Invested and biased

Edit. Fixed incorrect non-covid revenue data based on input from @msandip