Sharing what I learned while analyzing 360 One WAM ltd. for the SOIC league by @Worldlywiseinvestors.

Summary:

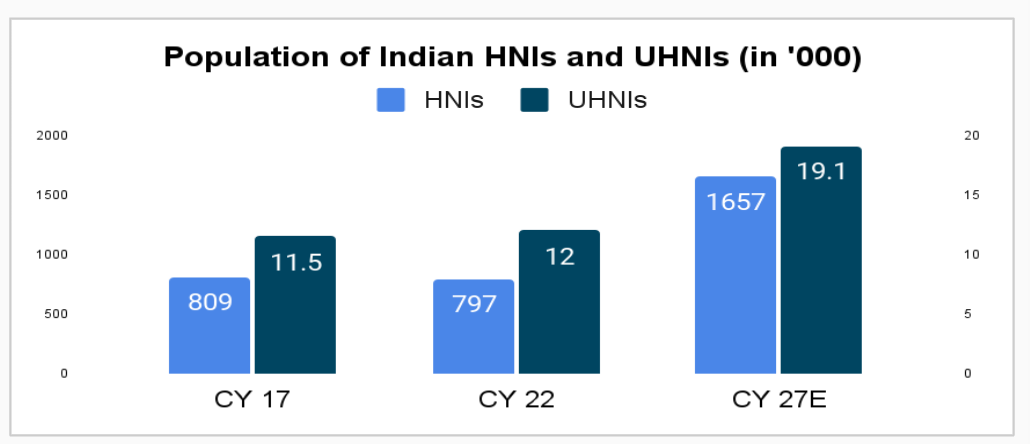

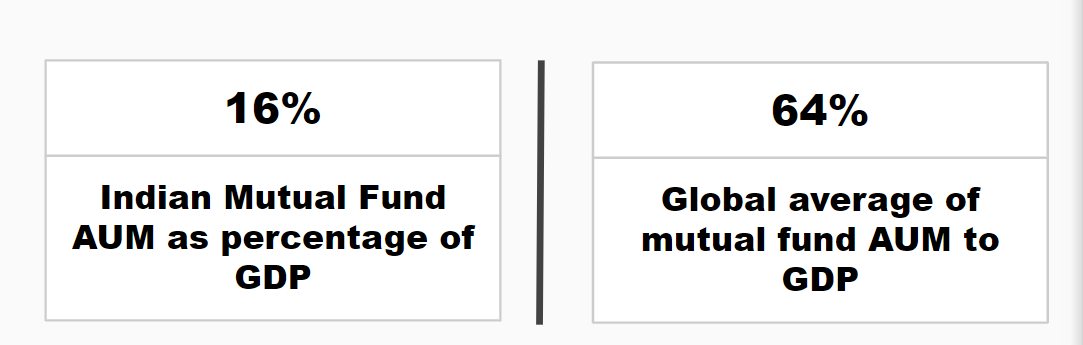

Number of HNIs and UHNIs in India are growing at double digit CAGR. Indian wealth management industry is still under penetrated. Wealth management companies with excellent track record of performance as well as integrity may be well positioned to grow rapidly.

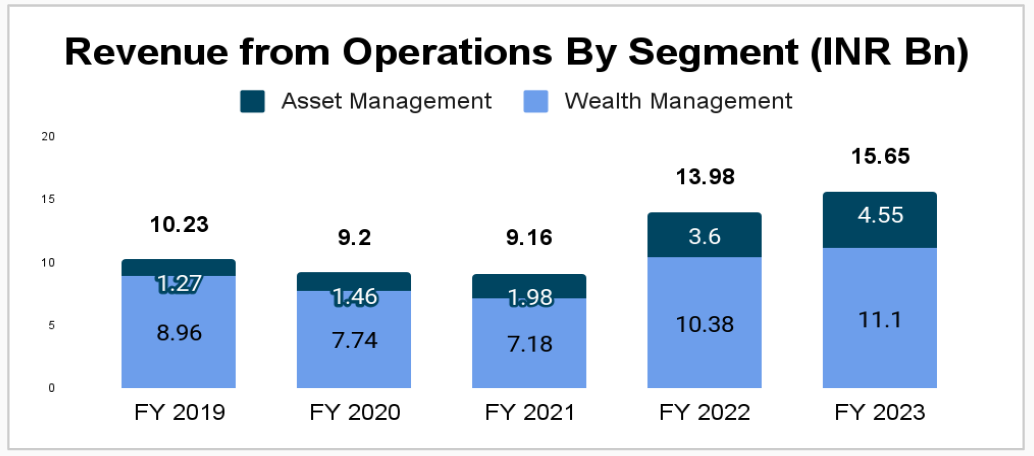

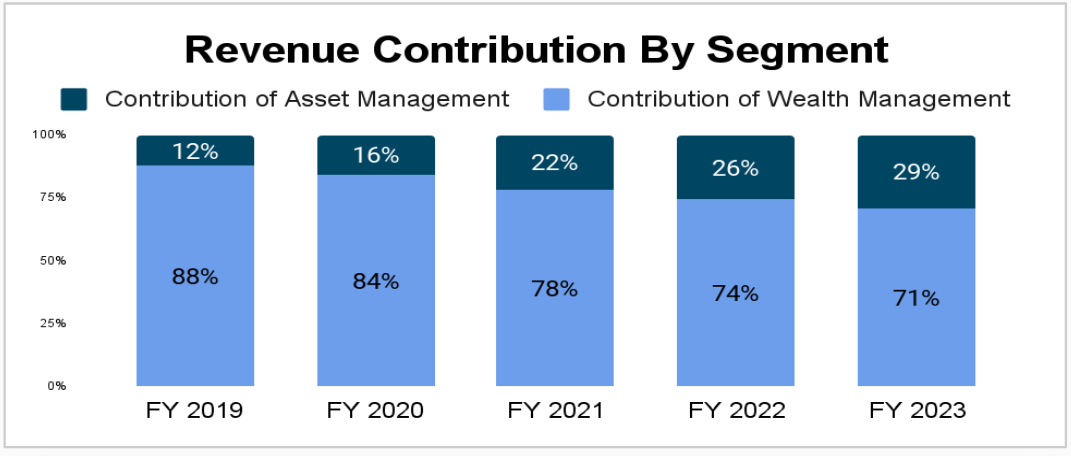

360 One WAM is an established business that is exclusively catering to HNIs and UHNIs since 15 years. Operating leverage is playing out nicely as the operating profit margin has expanded from 39% in FY 20 to 54% in FY 23.

In my opinion, the business is on growth trajectory along with the entire asset management sector in India.

History:

Founded in 2008, the business was part of the IIFL group. Currently one of the largest non bank private wealth management firms in India

Founder, Mr. Karan Bhagat, holds an MBA from IIM, Bangalore

Rebranded from IIFL Wealth Management to 360 One Wealth and Asset Management in November 2022

Current market cap is about 18500 crores (INR 185 Bn)

History of inorganic growth

2011: Acquired Pune based “Finest Wealth Managers”

2013: Acquired an asset management company and a PE firm

2016: Acquired an NBFC

2018: Acquired Chennai based “Wealth Advisors India” and Bangalore based “Altiore Advisors”

2020: Acquired “L&T Capital Markets” from L&T Finance Holdings

Services Offered

Wealth management: Customized solutions to targeted towards HNIs and UHNIs. Services include distributors, advisors, PMS manufacturer, brokers, AIF management, MF manager

Asset management: Less customized solutions focused towards maximizing portfolio value. Solutions include AIF, PMS and Mutual funds. Early movers in AIF space

Estate planning: Facilitate passing of generational wealth. Largest trusteeship service in India. 650 HNI\UHNI families are clients

Lending: An NBFC that lends to wealth management clients to serve their short term needs (working capital, acquisition, etc.). Loan book of ~5000 crores (INR 50 Bn). Typically the loan book is 1.5% to 2% of the AUM

Disclosure: This is not a recommendation. Please conduct independent due diligence. I have tracking position.

Antithesis pointers divided across two categories:

Internal:

Resignation of KMPs in last 2 years: Since FY 21, two company secretaries and compliance officers (one person with both duties) have resigned. Since FY 21, one CFO has resigned

Attrition among relationship managers: After changing business model in 2019, the business has seen attrition among RMs. It is a significant risk as the RMs form rapport and develop trust with client and have ability to take the client away with them. Company stopped publishing RM data since 2022

Currently trading at Peak Margins + Peak Revenue: The business currently has highest margins and highest PAT ever (and hence highest share price). Any impact to growth rate of the business may impact valuation

Promoter has pledged shares

External:

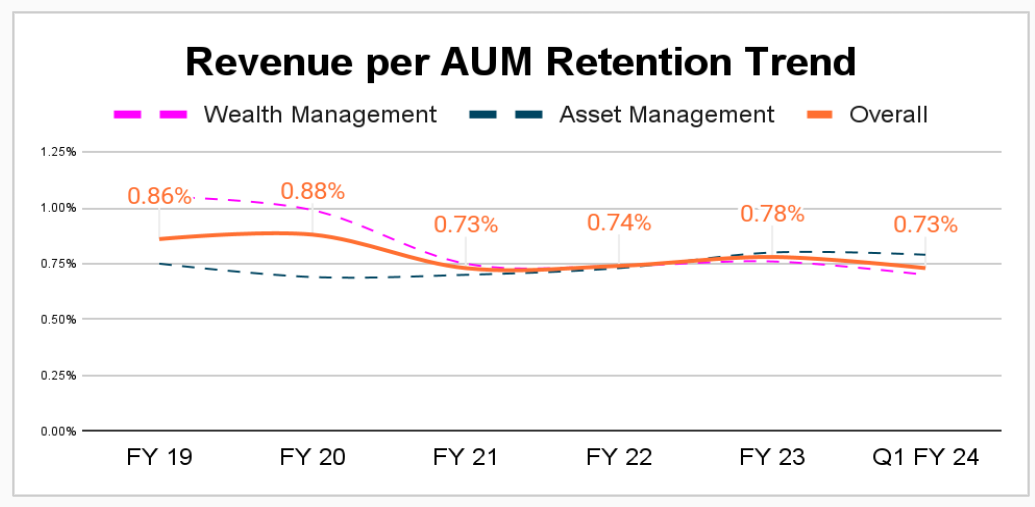

Regulation: The business is dependent on regulation around TER. Despite AUM growth, current revenue yield of ~0.75% may come down

Exposure to market movements: During down cycles of the market, new inflows get affected and MTM losses affect results

DIY Culture and Rise of independent advisors

Impact of not having a bank as a natural sales channel remains to be seen

Increasing competition by purely technology platforms (Robo advisors): highly are cost competitive

Reputation and people: Wealth\Asset management business is sensitive to reputation. Ability to retain advisors who have built relationships with clients is important to retain the clients

Data privacy and security are risks since any lapse may harm reputation and invite regulatory censure

The overall wealth and asset management industry is growing at a fast clip

Increasing acceptance of wealth\asset managers is Indian society is a positive

New product launch: In recent concall, management hinted that they have soft launched a product targeted at people with net worth of 5 Crore to 25 crore. Considering currently they target people with net worth > 25 crore, this may be a new mini segment. They also stated that number of customers per RM will go up for this category. Hence could be higher margin segment

Lesser incremental capital needed: When a new business raises an NFO, clients expect the fund managers to put up own capital into the fund (skin in the game). However, as the business gains credibility, they don’t need to put up same amount of capital in an NFO or fund raise. During a recent ~1000 crore AUM raising, the company invested only 5 crore of own capital

The management has a stated policy of distributing at least 75% of the PAT as dividend. They have been walking the talk thus far. Current dividend yield is about 3.5%

In recent years, management has simplified holding structure by reducing number of subsidiaries

Overall revenue per AUM (Yield): Tracking revenue per AUM a few quarters after launch of the new product would be important.

Excessive growth in loan book: Important to monitor any NPAs in the loan book

Addition of of new relationship managers and their attrition: Steady growth would show management’s confidence in winning future business while retaining talent

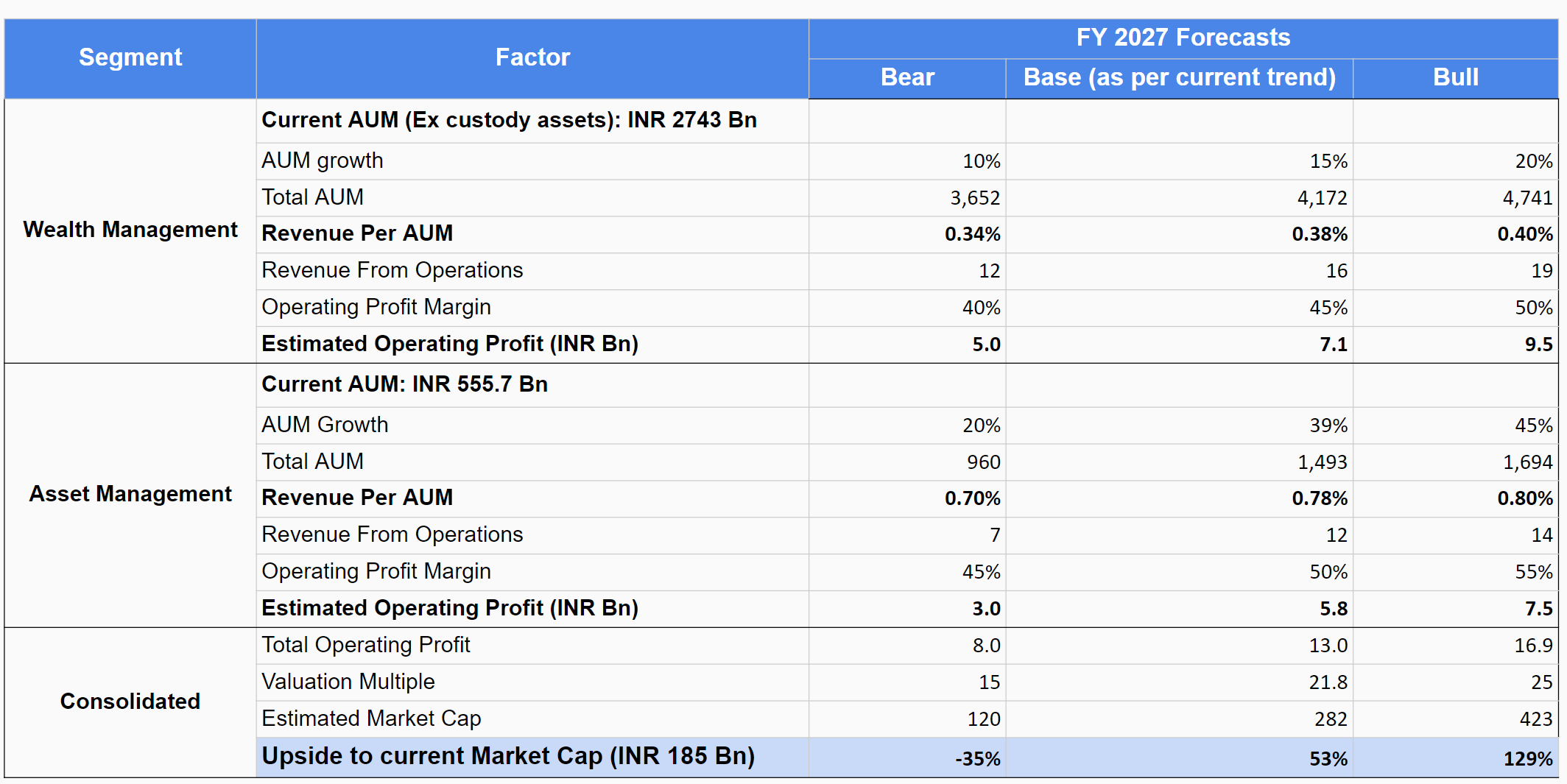

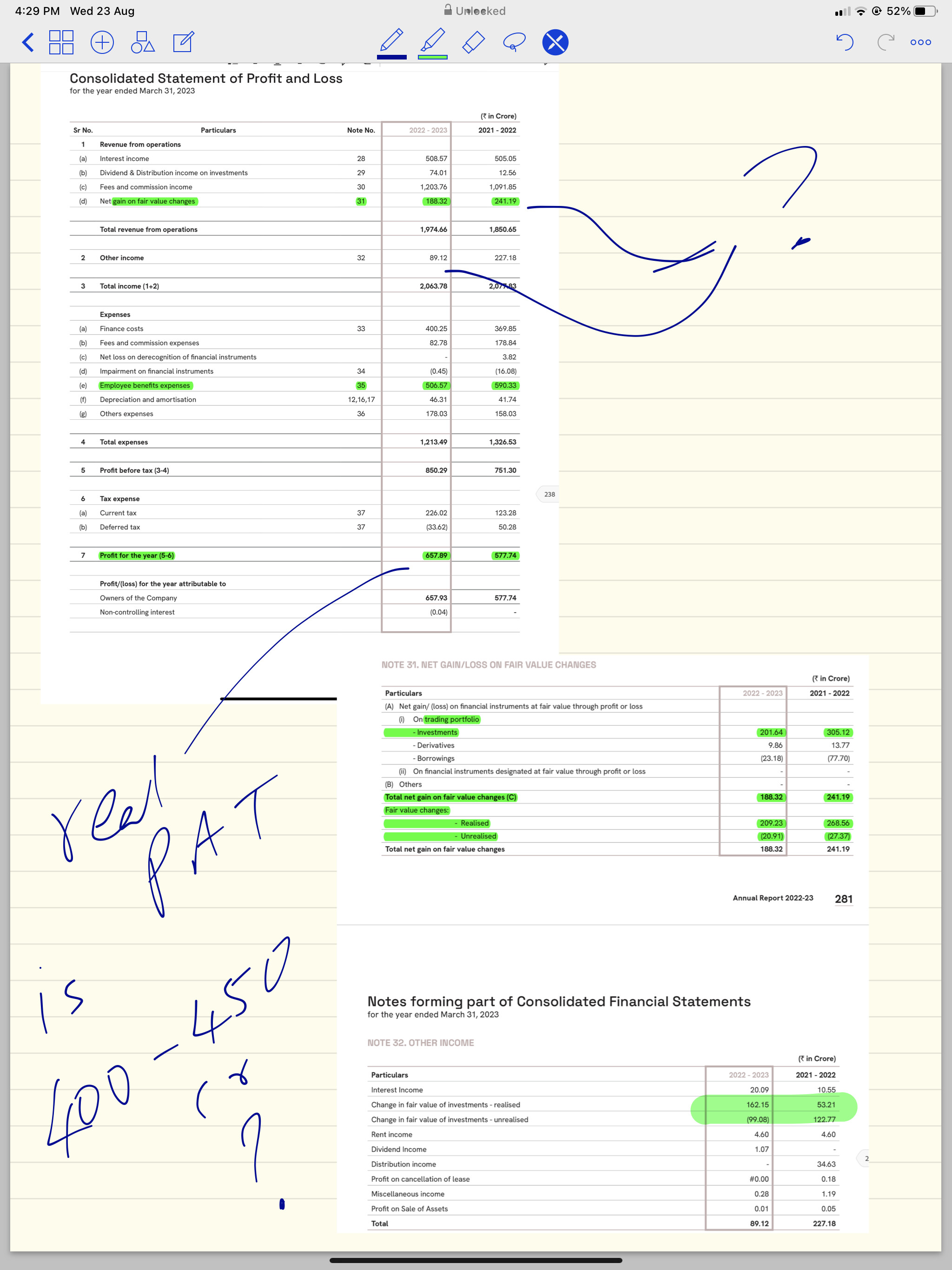

Due to variability of other income, I think the company should be looked at on operating margin basis. Hence, the valuation multiple calculated represents “price to operating margin”.

In addition, we seem to have 3600 cr of long term investments ( equity, AIFs, debt securities) funded by equity and by 4000 odd cr of MLDs ( total debt closer to 6400 cr; and a 5000 odd cr LAS book).

@mahesh_s can you enlighten more about asset and wealth management in terms of what they do, how they manage funds, where do they put money in. Etc etc.

How is this differentiated when it comes to edelweiss/nuvama?

Hi, yes you are correct. However, in my opinion, due to the nature of the business, it will always have income through gain on investments when they sell something at profit.

“Other Income” also consists of some amount of net gain/loss on investments. During valuation, one might want to exlcude these two or allow some wiggle room.

Asset management:

Offer mutual funds, portfolio management service (PMS) and alternative investment funds (AIF).

PMS typically is about managing client’s money via equity investments. Investment in private equity, real estate, precious metals, etc. is called “Alternative” investment. They offer AIFs also where they manage client’s money via investments in categories mentioned above. They are one of the leaders in AIFs in India.

Here, ability to customize as per individual needs is quite less. For instance, mutual fund may not accept a request to limit exposure to carbon emitting industry because one individual client prefers it that way.

Wealth Management

Most services from asset management segment but customized to one particular individual’s needs. Folks who have large corpus (above 25 crores) may opt for this service and define the the type of investment, horizon, risk, tax implications, etc. as per their needs (usually described in Investment Policy Statement).

Apart from this, the segment includes preferntial brokerage, advisory, family planning and lending services under Wealth Management segment.

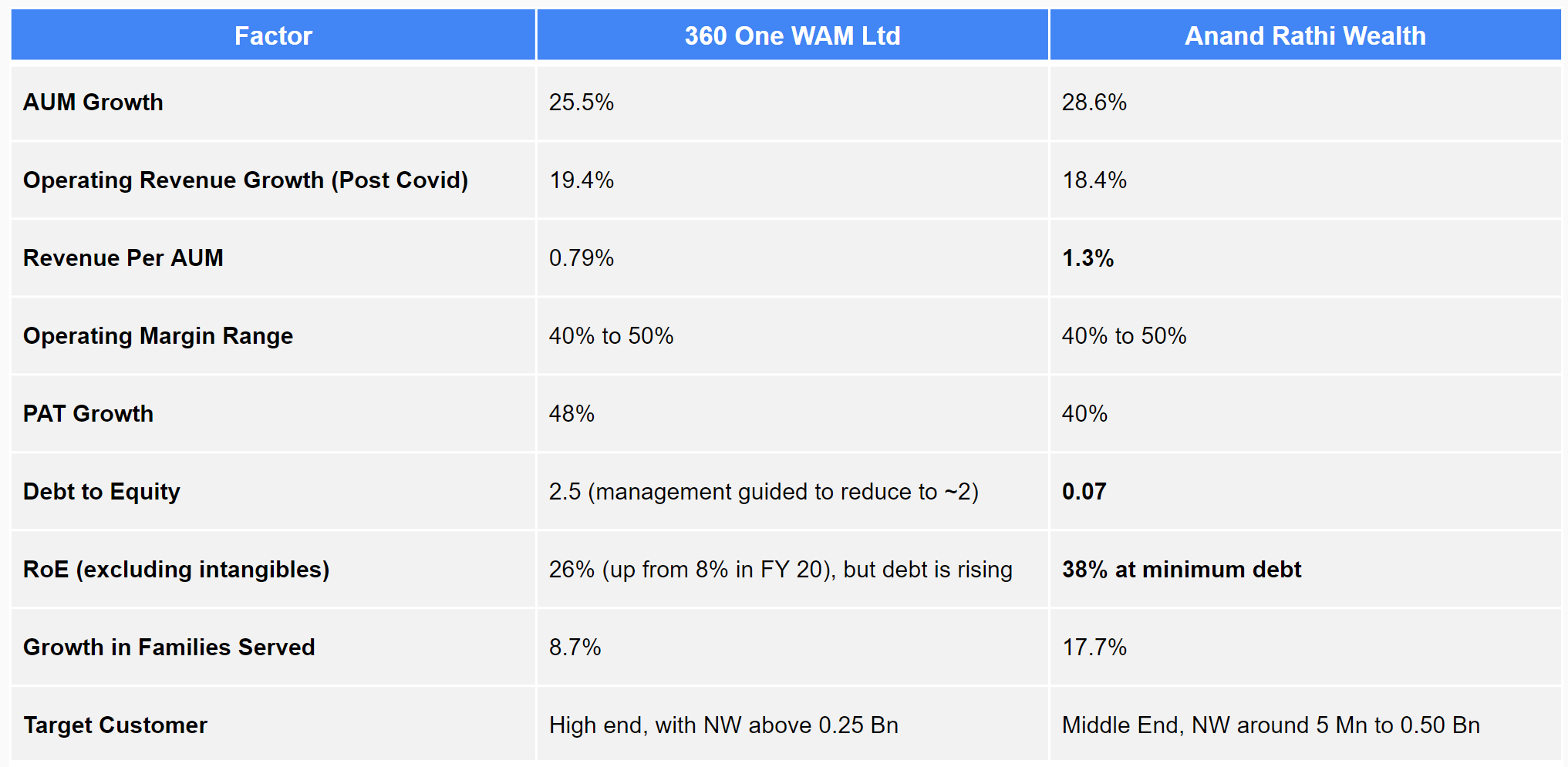

I havent studied Nuvama yet but it is in the pipeline (along with Anand Rathi Wealth).

Hope it helps

Excellent presentation on Wealth Management industry by Mr. Yashodhan Nerurkar from PPFAS. Here is the link.

Few key insights:

For a wealth management business, cost to acquire a customer is probably one of the highest expenses after employee cost

To cater to lower end of customers by spending minimum cost, global and Indian wealth management companies are investing in technology. Hence technology spend is probably going to be higher for a few years.

(Note to self: Think what may happen when technology spends are complete. When can it happen?)

Advantage to Bank Wealth Managers:

A client who has bank account with a bank, the data is available readily

Getting a meeting with client and pitching for wealth management business is not very hard

Lending against AUM is easier for a bank since they have the know-how in lending and recovering

Advantage to Boutique Wealth Managers:

The RM (relationship manager) develops trust with a client

If a particular RM leaves due to attrition, the client may not feel comfortable with new RM immediately

Few (not all) boutique wealth management firms are co-owned by the RMs. Hence attrition could be low and a long-lasting relationship with client may be forged.

very informative input I must say. I am new in reading this sector, so pardon me if my question is basic. but will u please help me understand the retention ratio these companies share. what is it exactly ?