Dear Santosh

Could please share the excel file ? . Thanks.

Dear Santosh

Could please share the excel file ? . Thanks.

You can download the same from above link.

Nice analysis on future potential, just curious how you are sure about downside protection for Zensar as compared to other IT companies? Thanks

Zensar is available at nominal growth of 3% in cash flow. Most of IT companies market cap factors double digit growths. Its not to say that they are not safer bet than zensar. Its just that we need to dig deeper and predict the future with more certainty.

Hi guys,

Is anybody tracking this stock?

It is a low growth it company but the valuations look decent.

Has dividend yeild of 2.2% and close to 700cr cash on books(as per screener).

If anybody is tracing this stock would request you to please throw some light and your view on it.

Sales are growing and last quarter margins were 9%. Does this look like the bottom?

It is the cheapest stock currently among IT mid/small caps interms of valuation. Fundamentally I see nothing wrong in this business except for some margin drops for a few quarters, which should not matter to an investor with even a 3year horizon. It should grow decently and margins will normalise by end 2023/2024 same as all IT stocks as TCS’s Gopinathan predicts.

Recent developments include Mr Ajay Bhutoria resigning due to personal reasons and Anant goenka taking the spot in the interim. Both moves dont give much confidence. Mr Bhutoria has had health issues for some time so I don’t see this as a rats fleeing the ship scenario though. Mr goenka seems like a left field decision which ignored all of the current executives.

Currently the company is available at just 4.5k or so mcap and all negatives including ceo leaving + margin compression look priced in. Dividend at 2.5 percent looks intriguing but in reality this will drop by a huge amount due to lower profits too. Now the unknowns are

All things considered while there looks to be an MOS forming here I’m still not fully convinced. Results are on the 23rd of January and il be keeping a careful watch then for any green shoots/updates regards management changes. Could still be a few more quarters of pain here but the valuations are very very intriguing

Disc: Not invested yet.

I think new CEO will be manish Tandon because recently he is recruited as managing director before the resignation of Ajay. And he has experience as CEO of css corp. So i think unless they offer CEO position he won’t join in the firm. I think they have to just announce publically.

Zensar has recently been facing some challenges, as reflected in their last few quarterly results. Despite being valued lower, the company has seen poor growth in terms of revenue and a decline in margins. Their expenses grew far faster than their topline. During the earnings call, the CEO appeared to struggle in answering some of the questions and was not able to provide a clear picture of the situation. This has raised concerns among investors about the future prospects of the company. It remains to be seen whether Zensar will be able to turn things around and improve its performance in the upcoming quarters.

Finally company publically announced new CEO i.e today 23rd jan 2023

zensar Q4FY23.pdf (1.2 MB)

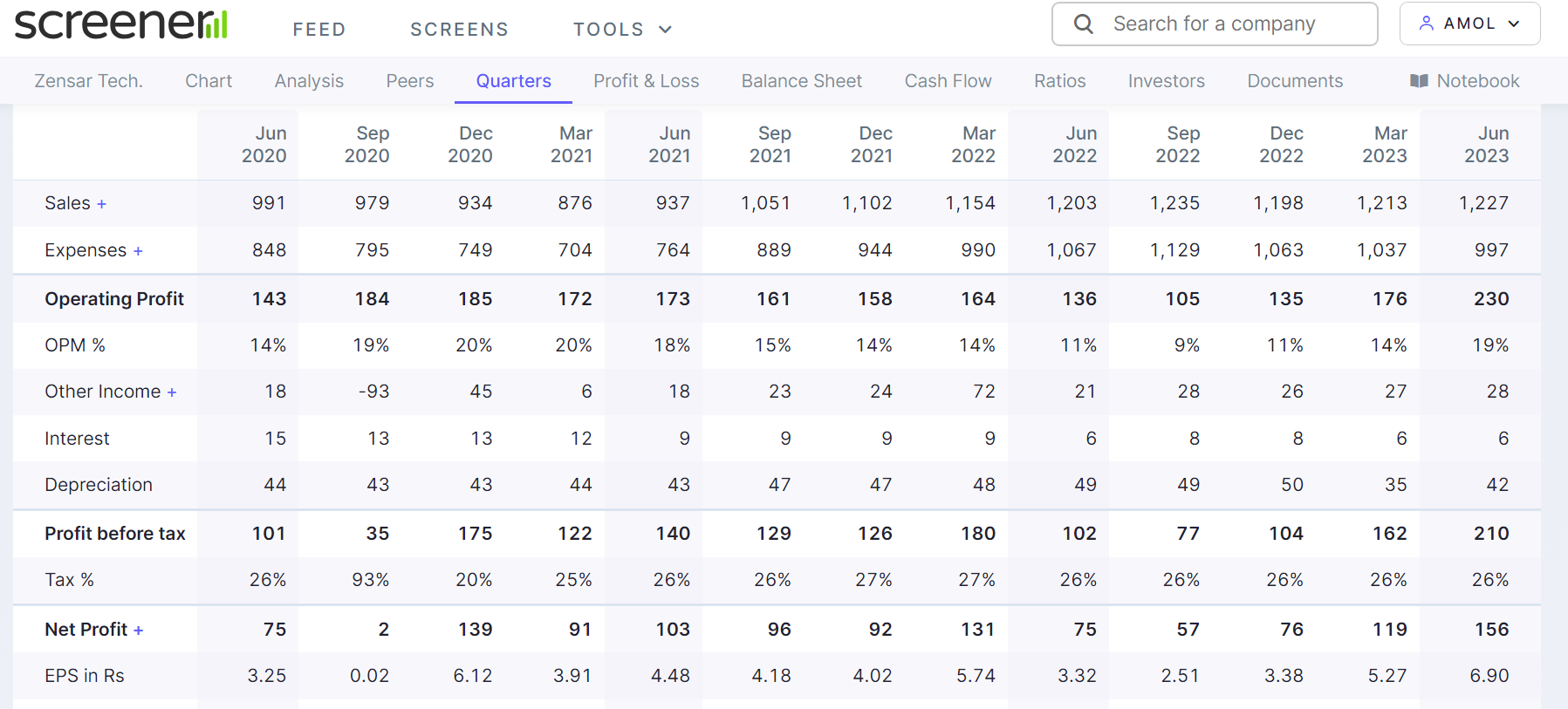

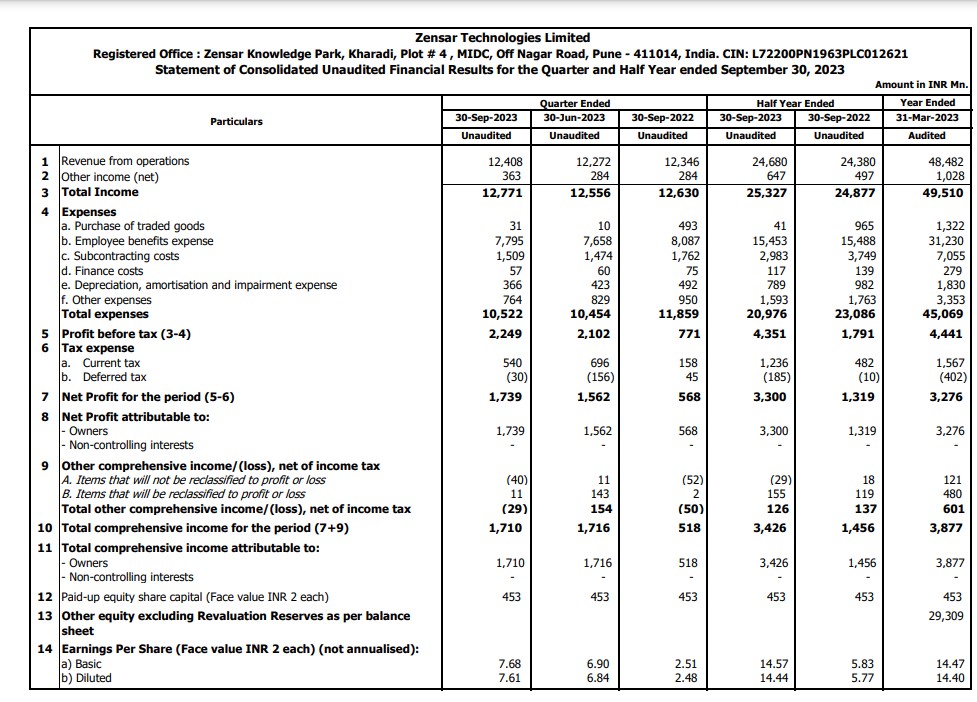

Impressive margin Expansion in the June 2023 results. Topline almost flat QoQ and YoY. PAT doubled YoY. Will be interesting to see the segment wise details and commentery on them in the next concall.

Any update on todays result

Flat topline but impressive margin expansion and stable cashflows 2 quarters in a row now. EPS has tripled YoY.

Looking forward to concall and presentation.

zensar-q3 results.pdf (807.3 KB)

Margin expansion Year on Year but no sales growth. IT cos. are struggling to add new customers, however margins are expanding, need to see why existing customers are willing to pay more, what is the reason for stickiness?

Sales growth has been muted for all the IT companies but that doesn’t mean they are not adding new clients. Almost all the IT companies have reported very healthy order book, some even their largest ever. There is always a lag between signing up a new client and execution.

Now coming to margins, they are not really expanding, they are just normalizing. The reasons margin went south, for entire indian IT industry, in 2022 and 2023 were:

1- High attrition IT- Higher salary increments paid to existing staff to retain them

2- Higher bench- IT companies hired like crazy in 2021 in anticipation of more work post-covid which never materialized due to slow down in IT spend in their key markets (US, UK, Europe)

3- Higher subcontractor deployment- due to high attrition

Now that talent market has cooled with industry wide layoffs, companies are hiring less. Attrition has gone back to historical averages which means lesser salary increments. Subcontracting has also gone down. Finally IT companies are using automation to improve their operating efficiencies.

For Zensar 18% is their highest reported EBITDA and they are still not there yet. With further revenue growth, operating leverage might even take it above 18%. Given the cheapest valuation among their peer group I find the stock quite well placed.

Disclosure- Invested in stock since 2022 (at 250 level) and could be biased.

By the way I am among very few who has continuously increased his allocation to IT stocks in 2022 and 2023 even when celebrated fund managers were giving sell calls and telling everyone to avoid the sector. Some even said CHATGPT will kill the industry.

I have worked in IT industry for close to 20 years and have seen the cycles so was confident this one will reverse too. Some of my best returns in 2023 have come from IT stocks thankfully.

Thanks Hemant for your valuable insights about the margins normalizing. It is difficult for an outsider to view the industry dynamics. I have also been invested in Zensar since 2022 ,average cost being around 280. I have also been invested in OFSS since 2021 from 3000 levels and never sold, it now comprises 5% of my Pf. I liked the stickiness of the OFSS product and once a bank onboards OFSS it may not able to leave it in the long run or the costs may be very high. As fund mamagers are now dissing HDFC/Kotak/icici… I think it would be now prudent to buy at around 10-15% fall from here.

For anyone wanting to understand Zensar at an overview level:

Very good set of numbers given the lukewarm industry environment. Sequential growth seen across all verticals. Only sour note is resignation of their CFO. Not sure if it’s just me, but I usually get concerned about resignation of CFOs on or around the results date.

Zensar Q4 2024 snippets

• In Q4FY24, the company reported revenue of $148.1M, sequential QoQ growth of 2.4% in reported

currency and 2.0% in constant currency.

• For the full year FY24, the company reported services revenue of $591.3M, yearly YoY growth of 1.0% in

reported currency and 1.3% in constant currency.

• In Q4FY24, EBITDA was at 16.5%, quarterly YoY increase of 200 bps and sequential QoQ decline of 70 bps

• In Q4FY24, PAT stood at 14.1%, a quarterly YoY increase of 430 bps and sequential QoQ increase of 70

bps

• The company reported net cash of $261.7M at the end of Q4FY24, QoQ growth of 5.4%

• US region reported a sequential QoQ services revenue growth of 4.3% in reported currency and 4.2% in

constant currency.

• Europe region reported a sequential QoQ services revenue decline of 1.2% in reported currency and 3.1%

in constant currency.

• South Africa reported a sequential QoQ services revenue decline of 2.3% in reported currency and 2.0%

in constant currency.

• Banking and Financial Services reported a sequential QoQ services revenue growth of 2.5% in reported

currency and 2.0% in constant currency.

• Manufacturing and Consumer Services reported a sequential QoQ service revenue growth of 3.0% in

reported currency and 2.3% in constant currency.

• Hitech reported a sequential QoQ services revenue growth of 0.8% in reported currency and 0.7% in

constant currency.

• Healthcare and Life Sciences reported a sequential QoQ services revenue growth of 3.6% in reported

currency and 3.5% in constant currency.