Starting this thread on Zaggle Prepaid Ocean Services which had its IPO in Sep 23.

A combination of SAAS and Fintech domains. The company provides following three products:

- Propel : Suppose you won ‘Star of the year’ award at your company, You will get the reimbursement voucher on your Zaggle Propel console/card.

-Save : Suppose you had to travel as part of company work. The Zaggle card gets loaded with estimated expense for travel, stay, food etc. At the end of it you can upload your bill, your manager approves it and the loop gets closed. Hence ease of expense management for employee as well as the company.

-Zoyer: Suppose you have a vendor, You can keep transferring the sum to him on his Zaggle card, He can reimburse it subsequently.

They are also very active in Prepaid card market. That is suppose you have a fleet of trucks. You can keep loading your driver’s cards on daily or requirement basis for fuel, meal etc. Hence efficient expense management again.

I see a lot of need for a product like this. There are few competitors as well. Example

-Expensify

-Happay

-Zoho expense

SAP concur

However no listed player in India. World over there are 4-5 multinational players.

As the business model sounds it is very important to have good partnership with prominent banks.

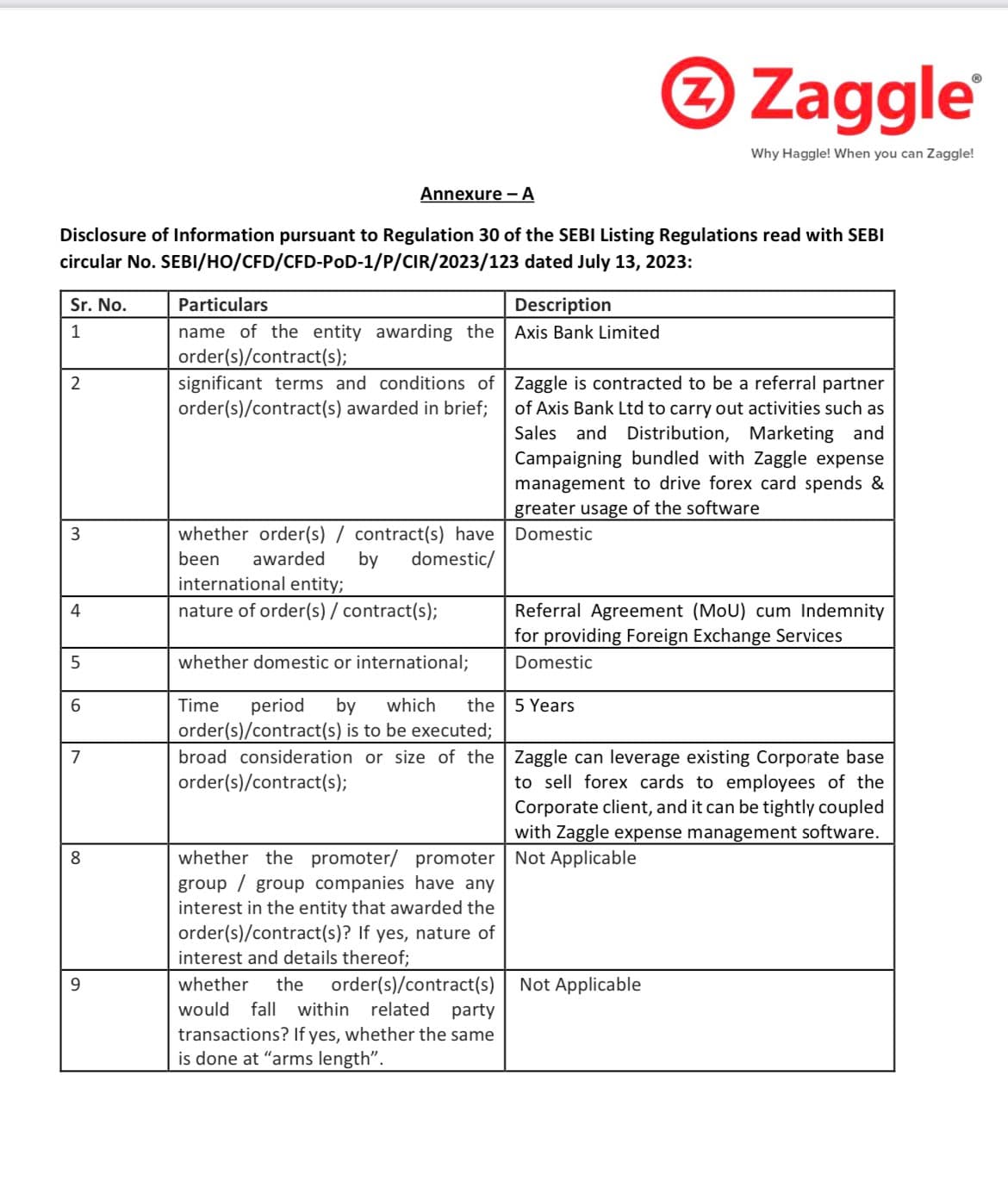

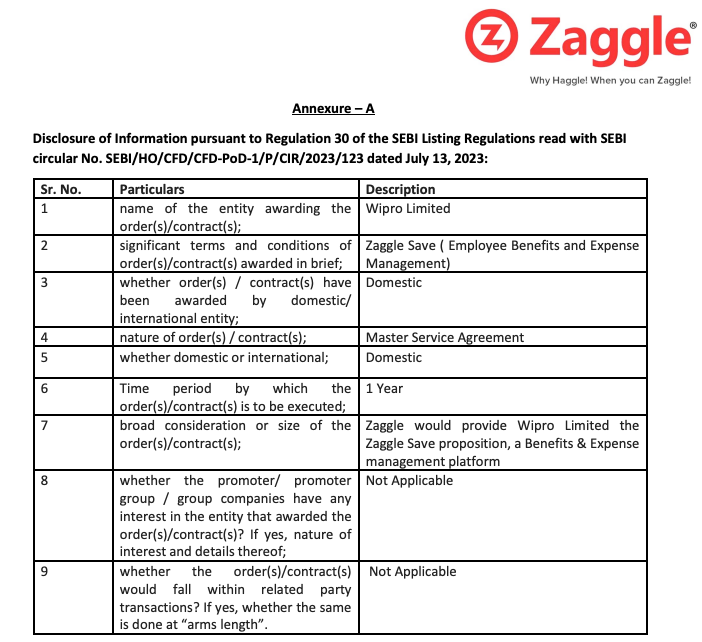

Their bank partners include Axis bank, Kotak Mahindra, Yes B ank, IndusInd to name a few.

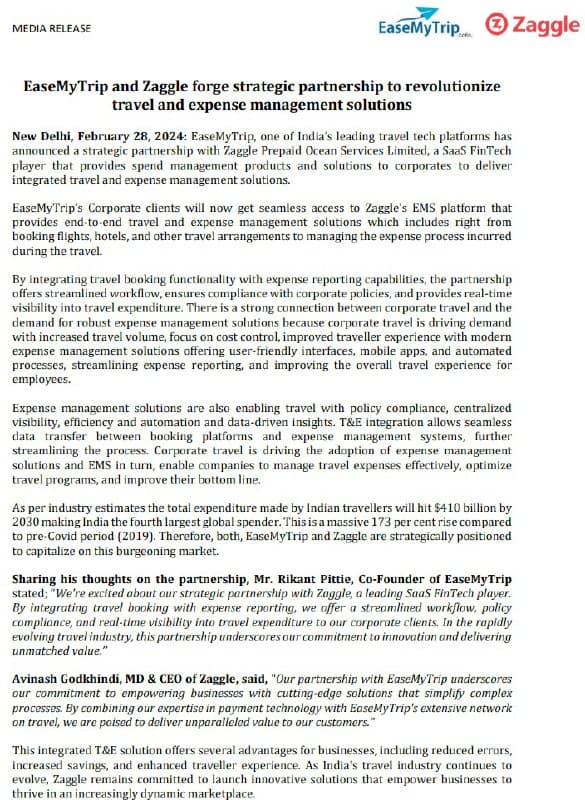

-Also have recent collaboration with VISA, Razorpay.

-Current customers include TATA Steel, Torrent Gas, Greenply, INOX, DBS, Rajiv Goenka group and many other big corporates.

Finances

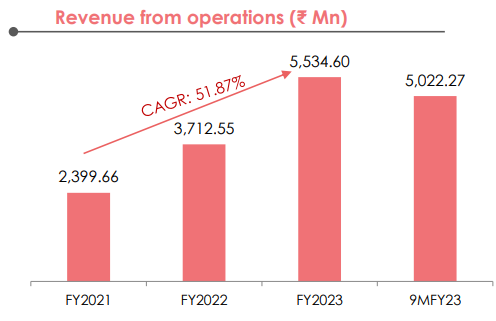

-51% CAGR revenue growth over past 3 years. Guidance of 40 - 50% growth in coming years.

-50 % CAGR EBITDA growth with margin guidance of 12 - 13 % in near future.

Cons

- Increased receivables (Inherent to business, because generally employees upload their bills in a cycle of 45-60 days)

Hence increased working capital days

-High PE (137) however as earnings increase, this will start to go down. - Company adopted IND AS accounting which has led to increased revenue from propel. As per them this is to cater for increased take rates from voucher based redemption rather than points based, could be aggresive revenue recognition.

Overall I feel the company has potential to become a multi bagger if they keep a check on receivables and working capital

-Ashish Kacholia invested in this in Q2 FY 24 then increased stake in next quarter. So there is interest from bigger investors.

Lets see what this does. It is definitely one to watch.

DISCLAIMER : Invested, Not a buy or Sell recommendation