It basically spiked to 340 which was clear over valuation due to GST taxation being on lower side than earlier taxation. Now since this is corrected, it is a moderate to low growth story (probably in the range of 10%-12% EPS growth depending how taxation is done going forward.). There are chances that, Government would continue its stringent taxation policy on cigarette business thus keeping pressure on margins and volumes.

Earlier growth rates which have been there in MOSL Wealth Creation Report of Dec 2017 may not be seen in near future unless its FMCG business grows at faster rate of about +20%.

All in all, it looks like 10%-12% EPS CAGR story and Price CAGR of close to that or above depending on your purchase price.

It is a steady Dividend yielding Large Cap suitable for some investors.

Disc: Invested from below 195 levels with long term view with moderate expectations.

As per the DRHP ice maker capacity utilisation is appr 40%. Just for info … there could be sales growth without capacity addition for some time to come.

@Yogesh_s, I truly admire your analyzing skills

Supported by analytics with numbers.

Learning is huge for me.

Thanks for being a part of this forum and educating us.

Wish you the best for 2018 and beyond.

Prasad.

Hi Yogesh. Can you please share your views on IRB Infra? What is ailing this stock? It is quoting at single digit PE. Can it be considered as a blue chip or am I missing something?

Did you follow any particular methodology for assigning the weights to individual scrips in the portfolio? Can you share on how you arrived at these weightages please.

Regards,

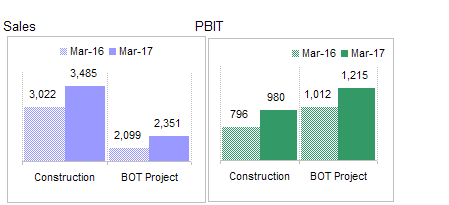

A quick look at the segment data shows that while construction brings bulk of the sales, BOT business brings bulk of the PBIT. However, BOT business has large interest costs so I think after deducting debt servicing costs (interest + principal repayment), BOT business is not contributing much to the consolidated bottom line.

Source :2017 Annual Report

Construction businesses are typically not valued like an annuity businesses because road construction is not a repeat business. however, given the scarcity of infrastructure in India, road construction business will grow for many years. BOT business while being an annuity business, is not a perpetuity business as a typical toll collection concession period is between 10 to 30 years. That means at some point, toll revenue from existing assets will drop to 0 so it cannot be valued as a perpetuity business using PE ratio.

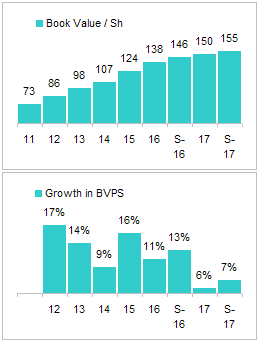

Overall, I prefer to value such businesses using book value after considering return on book value (ROE) and rate at which book value has gone up. Here are the stats:

Source: Capitaline

As you can see company has a book value of Rs 155/sh and it has grown at an average rate of about 12% over last few years. Growth rate as dropped in recent years as BOT business became larger part of the overall business. To me it looks like BOT business is weighing down on this company and that’s why they tried to monetize some of it by selling it to a trust using the new INV IT structure. However, I think it is not doing well going by the drop in price on NSE, which means company will have trouble monetizing more BOT assets.

Under the circumstances and given the low growth rate and heavy debt load, I would value the company at around 1.2 times book value or around 180 Rs/sh against current market price of 229.

No methodology for weights. Undervalued companies get higher weights and fairly valued companies get lower weights. I generally assign weights between 8% to 16%.

Just wanted to know your thoughts on Lupin after Q3 results. Would it continue to have the same weight in your blue chip portfolio or do you propose any changes.

Lupin reported disappointing numbers. The troubles for the company are not over yet and end is not in sight. However, I think these are industry wide headwinds and anyone with substantial sales in Us will face this issue. For pharma, all roads lead to US so there is no escaping from it.

Having said that, pharma is down but not out. Value proposition is still intact. Indian generics are popular all over the world for their cost and quality. any country will want to reduce cost of medicines and India hasn’t lost its competitive advantages in making low cost quality drugs.

Industry including Lupin is going to a new normal of low margin, low growth business and market is adjusting to this new normal but for last several quarters market is redefining what this new normal is going to look like. Until that happens valuations will be volatile.

Lupin, Sun made big acquisitions at the top of the cycle and now they are saddled with compliance issues and debt. These issues are limiting their ability to invest in R&D which is how future sales is going to come from. All these factors have impact on valuations.

In a DCF model, most of the value come from terminal value so one or two bad quarters does not really change the math but it does redefine what the steady state growth and level will look like which has a larger bearing on the overall valuation.

My portfolio is a low maintenance portfolio so weights are adjusted only annually.

Thanks Yogesh. What’s your thoughts on Vedanta. On a PE or DCF basis, this stock appears to be quoting very cheap. However as you have mentioned above for IRB, this stock maybe better valued on a P/B basis as the mines will have a finite life. Do you think this stock is currently undervalued?

Any idea why other cigarette companies like Godfrey Phillip got stuck in top line for years? I am bullish on this industry as I see many young people in my office smoke, drink daily. Also, I wonder why branded breweries and cigarette company top lines are not moving much when young has so much of disposable income and are spending on these stuff.

Part of your comparison is not appropriate. I am 26. Even I felt the same years back. But what we are missing out is the opportunity that external world is providing us today which doesn’t exists few years ago. I pondered upon the fact what am I doing all my school, college days only to realize that opportunity (internet, information) doesn’t exist those days. You are comparing with top b-school analysts of the past. I bet they would have done well in their generation. With whom you have to compare with is people of current generation. I make 4x of my fathers last day PSU retirement salary today. But If I compare that with my generation, I am just doing “ok”. I see many educated market retail participants (Buffet followers, value investors) and friends investing in MFs. I see markets are getting efficient day by day. Even though it appears like we are becoming absolutely rich on paper, relatively every one is on the same page. The problem to solve is, given that so much of information is available to everyone (internet), how can you generate returns way better than other participants? Otherwise, inflation eats up as every one will have same disposable income. I also feel MFs are extensively selling past data of 15-18% CAGR to new fund investors. Intuitively, I feel history will not repeat and India will follow US way (index funds returning better than MF) with markets participants getting smarter each passing day, efficient algo trades etc. Buffett is an early entrant into markets when there is no participation. RJ is one such. Today, stock markets are well known to many. If many becomes a billionaires, $1B will have no value. I kept lot of energies in markets during 2013-14 when hardly no one talked about it. Today, I became a passive investor when I see many people in my vicinity taking about balance sheets, mutual funds etc. I felt I should keep my energies in a field which is still not-priced-in despite being uncertain. For me, markets are like FD. I reserve money here. I don’t see myself getting super rich by investing in markets.

Young bro, you got me wrong. It appears that you have read so much from internet. At times, reading too much is harmful in decision making as you cannot decide what idea/theme to pick. Data is not important, information

(mining of the data, coming to conclusion, then act) is. I suffered from it.

I stay in India.

Coming to the point, I didn’t mention markets doesn’t make you feel rich. They do. But every else are on the same page investing in same markets. Hence you are no richer than them. There will be exceptions and smart investors always beat general public. But when average investor is acquiring more knowledge/education on markets, it takes extra effort to be a smart investor. I wrote it in that context. The more you dig into something, the more you like it. I have been a stock market evangelist for years. I fell in love with markets. It took me years to come to senses that Buffet and RJ days are gone. I believe most of Buffett or RJ’s wealth is because of their timing. They participated when markets are nascent. Yes, MF may still make 18% CAGR. But if that happens, then everyone (me, you, my friends, my relatives) is going to be rich which cannot be true.

According to me any field that you choose should have tailwinds and should not-be-priced-in (not many should believe or participate in it). It takes more effort today than 10 years ago to pick value stock as markets got more efficient. This effort to pick a quality stock to produce market beating returns is only going to increase either in US or India. I am not talking about bear or bull markets. I am talking in general. Of course, I park money in markets not to miss out on that 15-18% which every other average educated Joe of today in my circle is making. Its just my personal opinion. You have right to disagree. The reason to share my opinion is that I see an younger self of mine in you. The other people over here are too matured and experienced in markets to change their concentration to other fields. Its tough for them. My dad belongs to that category. He is a stock trader since 20 years.

I felt like experimenting on few businesses/field(s) which are uncertain/risky but are in naive stage. The same effort that I keep in markets could yield me better returns. I am talking in that context. I don’t want to talk without much progress to show on my side. But if I succeed I come back one day with a story to share. Give me some time.

Warren buffet has been screaming for people to compound wealth in the markets. What you are discounting is how many investors will stay the course leaving their MFs untouched for 30 years disregarding market swings etc etc. If this correction continues you will see redemption pressure overnight. Let me ask you something, Take USA and China for eg. youngsters there still dont know anything about investing and compounding. Ive met people who have studied and who work in investment banking and dont understand simple compounding. You tell an Indian that you wont make money for the first 10 years they wont be interested in holding their investments.

I cannot understand why everyone doesnt just dump money in MFs. Or for that matter in the USA index funds. Results dont show overnight, nobody does it.

Due results coming only after long periods of holding, retail investors dont put large amounts of money in MFs. They will buy insurance policies, they will buy products, cell phones. An Indian on 50k a month minus monthly expenses wont put more than 2.5k a month into MFs I guarantee you. And when the time comes to buy his house he will redeem his investments. Everyone starts, no one sticks to the plan. You are 26 today. 10 years from now I wonder how many of your friends will increase SIP or even hold their investments.

I will tell you something, in the next 10-15 years there will be huge in flow into MFs and funds. No doubt, people will know more and get more educated I agree. Everyone will invest in MFs. Not many will have the common sense to go and buy these amc companies from the open market and ride the theme. End of the day, I can virtually guarantee you that no one will take investing seriously enough to hold investments for 30 years to see results/ no one will invest big enough to see a massive return even post compounding. Nobody will dump 10-20-30-40 lakhs today and leave it for the next 30 years.

What so ever, you cannot be Warren if you start investing reading his books today. I read all his shareholder letters during 2013-14. They are superb. I was attracted to markets because of Buffett. He narrated businesses in a way that you feel it so easy to invest and make money. It pulled me towards market. The point that we miss out is, during his time, markets are not so efficient. RJ is the one from whom I learnt Buffett times are gone. When Buffett lessons are extensively available in 1990’s, RJ followed a different strategies to buy businesses. Listen/read his old interviews. He stood out. All I want to say is old lessons won’t work to produce market beating returns. Today most VPrs can say Buffett quotes even during sleep. I mean, they are priced-in heavily.

Its all your perception based on the people you meet. Only future will tell whether its true or not. I see youngsters of today are multi talented. Also, I see that you are always comparing with youngsters who doesn’t have financial education and who chill out. I am comparing with that seizable chunk who realize that there is an opportunities out there to seize because of internet. Why do you want to compare with average Joe out there? Compare with people like you, me, VPrs. Zerodha is the best example. Today, many IT people are traders. All in my office are traders. Some make money, some lose. Even though you compare with good ones, they are seizable chunk. When a seizable chunk thinks like you, acts like you, you don’t have an edge. This is happening in every field where internet bridges the gap. During older days, RJ has an edge as he stay near exchange and does trades. He gets (insider) information quickly where as people like my dad has to wait for newspaper to publish. Today, everything is instantaneous. Yes, there are guys who wants to chill out and they will be high in number (say 80%). But you are missing out comparing yourself with that seizable chunk (20%) who are making use of opportunities. I generally ignore those 80% and compare myself with 20%.

All I can say is you didn’t meet enough. May be the people you generally meet are dumb. You cannot conclude anything from it. My experience in my circle has been different.

How can you guarantee all this? I met people in my circle who invests 80% of their wealth in equity. All are below 28. There are around 6-7 people. Imagine, how many could be outside my friend circle. I mean they are seizable chunk who see opportunities like you. We are just looking at past and concluding. Opportunity is there for everyone.

Bro, I just don’t want to compare with average Joe out there and say I am doing better than him investing in markets. I always want to compare with best of participants (top 5-10%) and beat their returns. I just don’t want to be rich but filthy. It cannot happen if seizable chunk thinks and acts like you.

Hope this discussion instigates the fire in both of us to prove our points. Some are not in our hands. Only future will decide. All I vouch out for is that, the field that you should pick should be nascent. I realize that I have to prove my point with working results before making further talk. I will keep more energies in what I am doing currently. Hopefully it should work.

Guys , this thread is about Yogesh portfolio strategy for NIFTY 50 companies. Humble request, please continue the interesting discussion shifting to a more relevant thread . I am not being sarcastic or something like that, so, please do not misunderstand . It is just that every thread has a purpose and when certain things get stretched, whole purpose of that thread gets diluted for readers .Hope, I am not offensive

I second that, because every time I see a notification I expect something related to Yogesh’s portfolio, but when I visit the thread I see something else.