Hi Yogesh, regarding Eris, I agree that it has a long runway ahead. This is a market leader with strong margins and is positively placed as it is a 100% domestic story. However, main issue I felt with the offer was pricing. Can you please share your views on that? I see that it traded below offer price after listing, so some ground can surely be cleared at the lower price, but still how you found value there would be interesting & educative to know. Thanks!

Disc: tracking, no investment till date

Eris Lifesciences is pricey. No doubt about it. 500 would have been a right price. Seller was an accomplished private equity fund so they knew how to price the issue. This is not a value play. This is purely a growth story.

I like the genesis of the company. It is founded by a salesman and not a doctor. He worked for MNC pharma so knows nuts and bolts of the industry. Domestic pharma is all about selling a commodity molecule at high prices using your sales machine. Their field force productivity is second best in India (Sun Pharma is number one).

I see a lot of runway ahead. India is going to be a diabetic capital of the world as we are the largest producer of sugar in the world. Vegetarian diets are getting loaded with fats like butter, cheese and oil so that will (unfortunately) lead to an epidemic of heart disease.

Eris focuses on cardiovascular and anti-diabetic segments of the market which are actually niche but fastest growing segments of IPM. Eris with its still small share of the market has a long way to go. So a company gaining market share in a market that itself is expected to grow at a high rate for several years is a compelling growth story.

Being a sales focused supply chain company, they use analytics to see what’s selling and where’s the niche and sell that unlike other companies that make things first and then go looking for customers. With the new plant, they are now capturing some value in the manufacturing part of the supply chain as well.

they are not export oriented company so no USFDA issue. I am also hoping that domestic price controls will be mostly limited to acute segment and will not impact chronic lifestyle diseases.

Pharma companies tend to produce stable earnings so they should be discounted at a lower rate producing higher valuation. From an investment perspective, as long as we get 25-30% EPS growth over the next 3-5 years, stock will not be re-rated down a lot from current levels.

GST related de-stocking could be an immediate risk for Q1 risk but the long term story is good.

Yogesh, thank you so much for this post. I am curious how you assess the view on economy/market. How do you take a contrarian view? Is it based on GDP numbers/interest rates or expert opinions (which sometimes confuses more). Thanks again for sharing this approach.

Have to admit your amazing clarity of thought and linking of dots to connect the pieces of the puzzle left me pretty speechless.

I know there is a like button to appreciate a post of another person but this really warranted a comment of appreciation. Great work sir!

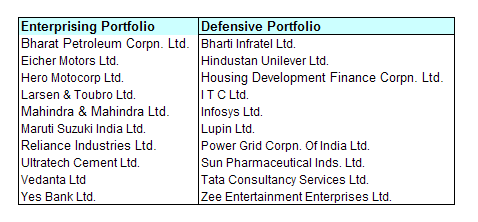

Central concept in the book Intelligent Investor by Benjamin Graham is that of Enterprising vs Defensive Investor. I took that concept and classified Nifty 50 companies as either Enterprising or Defensive and built 2 virtual portfolios. Enterprising Portfolio comprises 10 companies classified as Enterprising and Defensive Portfolio comprises 10 companies classified as Defensive. Enterprising companies are companies that produce volatile earnings while defensive companies are ones that produce steady stream of earnings.

Here are the current portfolios

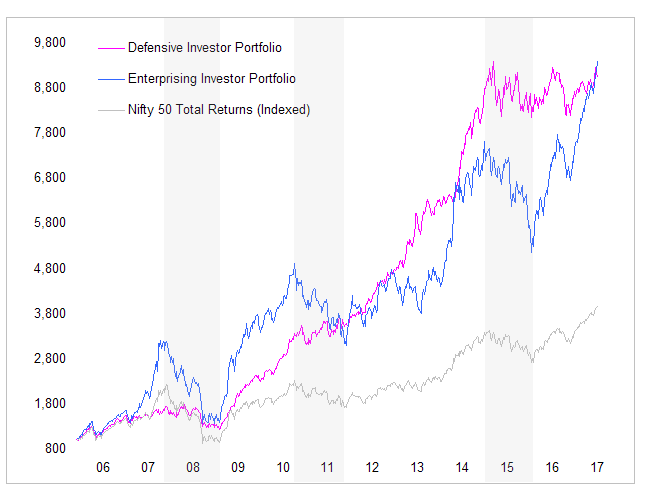

These portfolios are revised every year but not many changes are done. I monitor price performance of these virtual portfolios. Chart below shows performance of these portfolios over last 10 years.

Source: BSE

Note: Shaded areas are bear markets.

This chart shows that defensive portfolio (as expected) is much less volatile than enterprising portfolio. This portfolio outperforms in bear markets while enterprising portfolio outperforms in bull markets. Both portfolios performs about the same over long periods of time and outperforms Nifty 50. Most of volatility in Nifty 50 can be attributed to enterprising stocks while most of the stability can be attributed to defensive stocks.

My low maintenance portfolio consists of 10 stocks chosen from these 20 stocks. When consensus is growth, enterprising stocks outperform. When consensus is slowdown, defensives outperform. When enterprising stocks outperform, I overweight defensives and when defensives outperform I overweight enterprising when I rebalance my portfolio for next year. That’s my contrarian logic. I don’t always get it right but that’s the goal. Also these are all good companies. A mistake isn’t going to cost you a lot.

Thank you, Yogesh, this clearly spell out your thought process. As an investor, we really have to keep eyes on pricing control issue, as you already mention. regards.

I have gone through your thought process and find it very rewarding in the market parlance. I had just two questions.

1: How do you segregate defensives and enterprising companies. Its ok to understand from the face but can you explain if you use some quantifiable method to segregate amongst the companies.

2: How do you determine individual company weightages and also portfolio weightage for these two portfolios. Is there some quantifiable parameter that you follow.

Any idea what % of their sales come from sweetener? I think it’s low. They derive most of their sales from margarine. Artificial sweetener is a niche even in West where there is a lot of awareness of lifestyle diseases so I am skeptical of the opportunity size in this category.

You can use CAPM beta as a quantitative measure of volatility. Defensive stocks have low beta while enterprising stocks have high beta.

Another measure will be to look at volatility of earnings growth. You can use standard deviation of earnings growth. Standard deviation will be high foe enterprising.

Another way is to use coefficient of variation (average / standard deviation) of earnings growth to account for compounding effect of earnings. This measure will be high for defensive and low for enterprising.

Weightages are generally proportional to company’s weight in the index but adjusted for valuation. Undervalued companies get a higher weight.

Thanks a lot for this informative chart as well as all the insights you provide in the forum.

I had one query regarding the chart:

Is it a fair comparison to select few of the current Nifty50 companies and compare their performance against Nifty50 index? Note that many of them would not have been in Nifty50 in the last few years. Now that they are in Nifty50, it implies that they have outperformed the market as well as their peers. We might get a better idea of the performance of such a portfolio construction (against Nifty50) if we included the companies in Nifty50 in past years (and regularly updated them as suggested by you). In summary, I felt that the chart is biased, probably having hind-sight bias.

There is no hindsight bias in these portfolios as these were constructed several years ago and updated regularly to include only the companies in Nifty 50 at that point in time.

Enterprising and diversified portfolios presented in earlier post are CURRENT versions of these portfolios. Over the years, companies were added and removed from these portfolios based on what’s included in or excluded from Nifty 50. E.g. Eicher was added only last year only AFTER it was added to Nifty 50. So historical performance of Enterprising portfolio does not include historical performance of Eicher. Eicher’s performance is counted only AFTER it was included in the Nifty 50.

A quick question…if I want to start my portfolio today…can I start with 10 stocks with 50percent defensives and 50 percent enterprising…share your thoughts on how to allocate specific percentage to a stock.

Basically I want to start a portfolio today and rebalance year on year during March 2018 ,2019, and so on

That’s a good starting point. Allocation depends on relative valuation so tough to answer in a short para. I normally keep it between 8% to 12%. financials usually get a higher weight as they have higher weight in the index.

Hi Yogesh,

You did mention that you have select midcap and small cap also to your portfolio.

Can you also let us know the basis of selection of these stocks.

I like your strategy for large cap but at the moment I have a portfolio with lot of midcap and small cap and would like to balance it by considering your strategy for midcap and small cap.