@Yogesh_s Its been a while since you discussed your exits and new entries. Would be great if you could share the same.

What is your strategy in current euphoria scenario?

My current mid-caps

Indiabulls Housing Finance - actually this can be called large cap now.

Avanti Feeds - almost a mid cap now with a 5x movement in one year.

small caps

PSP projects

Eris Lifesciences

Nitin Spinners

Eldeco Housing

My strategy is to invest in high growth companies so earnings will catch up with valuations fast and companies will recover quickly if there is a correction. I am also investing in SME stocks are these are offered at cheap valuations. I am following a diversified approach to SME stocks as this is a new area and risks are high.

Some SME stocks I have bought recently

Worth Perepherials

RM Drip & Sprinklers

Shanti Overseas India

RKEC Projects

14 Likes

Hi Yogesh,

SME investing is an interesting area to enhance learning and knowledge. It would be helpful if you can share short investment thesis on why you picked these SME companies.

3 Likes

SME platform is an exciting new avenue in Indian markets. This is where small, young and dynamic companies are traded publicly. In developed markets, small and growing companies are bought by their larger peers even before they go public so investors never get to own shares of these companies. In India, promoters are unwilling to sell their companies to larger peers and instead choose to sell only a minority stake to small and distributed investors so there are plenty of small companies that are trading publicly.

SME companies grow at a high rate and tiny in size (I think average market cap is somewhere around 50 cr) so even regular investors get the same returns as private equity investors with an added advantage of an easy exit option if things don’t work out. The big irony is that small investors are not allowed to in invest in small companies as lot size is usually 2000 to 3000 shares. This is because these are risky and SEBI assumes that small investors are not capable of handling the risk. Even then, the minimum purchase lot is around 1 to 3 lakhs so it is not totally out of reach of small investors.

Most of SME companies go public at around 2 times post issue book value and around 6 to 10 times earnings. This is much better than aggressive valuation of main board companies.However, only 1 out of 20 SME issues is worth investing so you have 95% chance of picking the wrong one. This is what makes them unattractive and keeps the overall valuation low but it also enables a careful and hardworking investor from earning huge returns.

An SME company moves to main board of the exchange once the market cap crosses 200-500 crores (this is just my observation, correct me if I am wrong here). That’s when liquidity improves. Considering that average market cap is around 50 cr, the company has to go up 4x to 10x before it will move to main board. I am sure lot of SME investors invest in SME issue with an expectation that the issue will move to main board.

Typical characteristics of SME companies that are worth investing (1 out of 20)

Pros

- Young and dynamic companies

- Fast growing companies earning high return on capital

- Typically founded by first generation entrepreneur.

- Offered at reasonable valuation relative to growth rates.

- Institutions generally are not interested as size is too small for them.

- Simple businesses, no conglomerate structure.

- IPO prospectus has detailed information about the company.

Cons

- Business model is not proven.

- Commodity business, no moat or competitive advantage.

- Growth and return ratios can drop as size increase

- poor liquidity as lot size is large.

- price can be very volatile.

- likely to drop substantially in a bear market.

- Most SME issues are bad. One has to be very careful in picking the right one.

Here are some of the issues that I have invested recently.

Worth Peripherals.

Worth is a manufacturer of corrugated boxes. It supplies packaging boxes to FMCG companies. It has a manufacturing capacity of 30,000 tons with a capacity utilization of 90%.

Pros

- Relatively new assets (plant is built in 2012) and automated manufacturing.

- Return ratios are good. Cashflow is good.

- Opportunity size is large as packaging industry is growing.

- Company has been able to pass on price increase to customers so margins are stable.

- Young and first generation entrepreneur. My interaction with management showed that management is genuine.

Cons

- Capacity is almost fully utilized. no room for further growth. Company plans on raising additional capital to fund capex once it moves to main board. this may or may not happen. It may not move to main board unless market cap rises which may not rise unless profit rises which in turn may not rise until capacity/production rises.

- Kraft paper prices can be volatile and company may not be able pass on all price changes to customers.

- IPO is for working capital and benefit of listing only and no new capacity is being created.

My only rationale in investing in this company was a good company offered at low valuations. Since growth visibility is not there, I am already considering to sell as price has already doubled. However, this is selling at fair value now.

RM Drip and Sprinkler Systems

RM Drip is a manufacturer of micro irrigation systems. Company manufacturing units are set up in 2015 and 2016 so utilization is around 25%. Sales are growing at 100% in last 2 years as new units are set up. company’s fortunes have brightened once Mr. Shyam Dash joined the company in 2015 and became director in 2016.

Pros

- Fast growing company

- New capacities with low utilization. Likely to improve over next two years

- Margins are better than competitors and growing.

Cons

- Company’s customers (farmers) depend heavily on government subsidies.

- 25% of business comes from project market where company installs MIS and files a claim with the government for reimbursement. This is a working capital intensive business as payment from govt can take 4 to 6 months.

- No competitive advantage as products are commodity. Only distribution and pricing is the differentiation.

- Competitors (EPC Industrie - Mahindra group, and Jain Irrigation) are large with strong distribution.

- Cashflow is poor. However, given the growth rate, this is OK.

RM Drip is offered at 2 times post issue book value and 28 times TTM earnings. Issue appears expensive but company is growing rapidly so earnings should catch up quickly. By my estimate, company is trading at around 13 times FY 2018 earnings.

Shanti Overseas (India) Ltd.

Shanti is a trader turned manufacturer of Soya products like soyabean meal, soyabean oil and soyabean lecithin. Shanti has been a trader and primary processor of agri commodities until 2014. Since 2015, it signed an agreement with Bushman Organic Farms (US) for supply of organic soya meal. Bushman is a supplier of organic animal feed in US. Growing preference of organic food in West is driving demand for organic animal feed. As per US law, animal has to eat organic feed to be certified as organic meat.

Company has started crushing plant of 24,000 TPA capacity in 2015 and is planning to increase it to 36,000 TPA using IPO proceeds. It is also going to set up 18,000 TPA oil refinery.

Pros

-

Agreement with Bushman and planned new capacity provides growth visibility

-

Capacity is new and utilization will improve over next two years.

-

Organic meat is growing in popularity in West.

-

India is the only country in world that exports non-GMO soyabean so Indian soya meal should command a premium in organic feed market.

-

ROE is high but likely to drop as leverage comes down.

Cons

- Company does not use any solvent for extraction which is necessary to maintain organic tag but it results in lower yields and higher costs.

- company is highly leveraged.

- Agreement with Bushman prevent company from selling organic soyameal to anyone except Bushman that is produced from mechanical expeller machines.

- Company has no experience in manufacturing. It has been a trader for over a decade.

- Industry is highly fragmented and competitive. Few organized players are significantly larger than company.

- company’s margins are significantly higher than competitors so there is a risk that margins may drop.

- Shares are trading 30% below issue price so investors are not enthusiastic about company’s prospects.

- Soyabean prices are volatile and farmers may decide not to produce soyabeans reducing plant utilization.

Shanti Overseas is a direct play on growing popularity of organic meat in US. Whether this turns out to be a trend or fad will decide fate of the company. Valuation is cheap at 7 times earnings and 1.4 times book value.

RKEC Projects

RKEC Projects is a construction company that specializes in marine infra, bridges and roads. company has made good progress in last 2 years and appears to be at an inflection point. Company is promoted by a first generation technocrat promoter.

Pros

- For a construction company, balance sheet is strong.

- Looking at list of past and present customers, company appears to be moving from an L2 contractor to an L1 contractor which should help improve margins.

- Opportunity size is large.

- No BOT portfolio. 0% captive order book.

- Current orders are worth 700 cr compared to sales of 190 cr in FY 2017. this provides revenue visibility.

- Market cap is already 200 Cr so this issue is likely to be moved to main board.

Cons

- Company’s return ratios have only improved in FY 2017. Whether these are sustainable or one-hit-wonder is yet to be proven.

- Business is working capital intensive.

- Executive compensation is high. Business is highly dependent on promoter.

RKEC was offered at low valuations however shares have quickly gone up since IPO so company is now fairly valued.

I generally take growth opportunities of SME companies with a pinch of salt as there is no assurance that company will be able to capture these opportunities. SME issues are not a macro story. It is very much individual stories that can play out (or not) irrespective of overall economic situation.

Disc: There are many SME IPO issues and I may sell any or all of these if I find something better. This is not an investment advice. Please do your own due diligence.

47 Likes

Yogesh bhai,

The thread started out trying to avoid “shock and awe” kind of experience for the investor… now its is all about it.

I guess an investor evolves. I on the other hand, am still reading and re-reading your earlier posts.

Amit.

6 Likes

Good observation. SME investing is diagonally opposite of blue chip investing. Both have their own pros and cons. I started my blue chip 10 strategy several years ago purely as an academic exercise but I am surprised by how simple yet effective it has turned out to be. However, as an active investor it is too difficult to stick to low maintenance strategy so I have only recommended this portfolio to my senior relatives while my personal portfolio includes blue chips, mid and small caps and now SME stocks as well (basically everything).

I am planning to move to a blue chip 10 portfolio but not sure if and when I will actually do that. On the other hand, SME platform enables an investor to be like a private equity investor and that’s a step towards primary market. Its exciting to fund tiny companies and watch them grow. I believe as investors we should aim at buying shares directly from issuers (primary market) than other investors (secondary market) as primary market actually creates new equity capital and helps in growth of entrepreneurship and capital market.

Disc: I am not a SEBI registered investment adviser.

6 Likes

How exactly does one invest in the BSE/NSE SME platform. I have a icici demat account. Where exactly do we see the SME ipo offerings. I asked my relationship manager and he was totally lost about the SME platform.

ICICI uses its own logic to filter which stocks are available on its trading platform. May be because of the margin and liquidity constraints. However, all brokers who are members of BSE and NSE should be able to offer all SME stocks. These trade just like regular stocks except that lot size if higher. Zerodha offers all stocks that trade on NSE and BSE.

Hi sir,

This link provides some ideas about how SME listed stocks can migrate to main platform.

Regards

3 Likes

Applying for Ice Make Refrigeration SME IPO. Apologize for posting on the last day of IPO closing. Thanks to @kaustubhkale for pointing this issue to me.

Ice Make Refrigeration is a Gujarat based manufacturer of refrigeration equipments like cold room, commercial freezer, chiller, refrigerated vehicle and ice cream hardener. Its customers include dairy, ice-cream, food processing, agriculture, pharmaceuticals, cold chains, logistics, hospital, hospitality and retail. cold room account for 60% of sales.

Company has increased capacity of cold rooms from 100,000 sq. mts to 500,000 in 2015-16 and current production is at 175,000 sq. mts. Company expects to boost production to 350,000 in FY 18-19 and further to 400,000 by FY 2020.

Company is also planning to backward integrate into manufacturing of condenser and evaporator coils which are essential components of a refrigeration equipment and currently being imported. Backward integration will be funded with proceeds from IPO. Additionally, company is planning to upgrade its current manufacturing facilities to boost productivity and quality. Company has recently acquired a similar company in Chennai and it plans to upgrade manufacturing facilities of this company using IPO proceeds.

After building new capacities in 2015-16, sales and profits have skyrocketed and expected to continue for at least another 2-3 years. Chennai acquisition will give further boost.

Company is selling 41 lakh shares at 57 rs/sh valuing the company at 88 cr post IPO. Company earned 5 Cr PAT on a sales of 88 cr so company is being valued at 18 times TTM earnings on a post-issue basis which is fair given the growth prospects.

14 Likes

Sir, can you share your views on lupin.

I am not an expert in pharma so I can’t comment on Lupin based on its portfolio of drugs or where the future sales is going to come from. My analysis is based purely on financials and valuation model. I only have a basic understanding of the industry enough to value companies using a conservative set of assumptions.

Problem with Lupin are common to Indian pharma industry. Indian pharma is going to a new normal of lower margins and higher uncertainty both of which impact valuation. I wouldn’t invest in Lupin just because it has dropped so much because market is just pricing new normal.

Indian pharma companies grabbed the low hanging fruit of simple generics and made handsome profits. Now they have to spend more on R&D to grab the complex generics opportunity. Over last 3 years, drop in net margin is largely due to higher R&D costs. After Gavis acquisition, balance sheet indicators like debt/equity ratio, receivable days, asset turnover etc are not looking great. All these have impact on valuation.

Based on all this points, a standard DCF model gives a fair value of 775. Since my understanding is limited, I generally err on the side of caution and use conservative estimates of cashflows and discount rates so an expert in the industry might value the company higher than 775. Based on this valuation, downside risk is limited. However, a stock trading at fair value has an expected return equal to discount rate used in valuation. For pharma companies, discount rate is usually lower as pharma companies are defensive in nature and produce a steady stream of profits. However, given all that is going on in the pharma industry, this assumption may not hold and that can cause valuation to drop further. In fact, this has been the case over last 2 years. At some point, valuations will bottom out and we may be near that point but upside is still limited.

15 Likes

Hi Yogesh ji ,

I wonder why you should not consider for opting of full index rather than a few hand picks I have made analysis of Nifty since 2000 I am sure that it will help the fellow VP’s and request a review from seniors

1 Like

Hello @Yogesh_s ,

Just want to know what is the blue chip portfolio for 2018. Asking this just for academic purpose. Want to learn how you selected for 2017 and 2018,

TIA

1 Like

@yourraj, I am having trouble understanding your point. Are you suggesting that a portfolio of all 50 stocks is better than a hand picked 10 stocks? That will be an index portfolio and it will perform like the Nifty 50 index. Purpose of picking 10 out of 50 is to beat the index and earn a higher return.

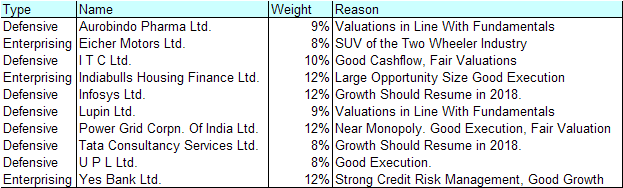

Here is the portfolio for 2018.

Notes -

Stocks removed

BPCL - Margins might drop with rising oil prices.

Coal India - Employee costs eating into dividends

HDFC - High valuations, NIM squeeze likely as new entrants are targeting HDFC customers.

Maruti - Exit purely on valuations. This may turn out to be premature but can’t hold on at this valuation.

Stocks added-

Aurobindo Pharma - Purely on valuations which are now in line with fundamentals.

Indiabulls Housing - Highest ROE in the home loan industry.

Infosys - Valuations are fair, Demand for IT services should rise driven by cloud and mobile.

UPL - Good execution, vertically integrated operations.

Overall, since consensus is growth and enterprising stocks have outperformed, I am overweight on defensives. Financials like Yes Bank and Indiabulls are well paced to ride the growth in domestic economy while pharma and IT should benefit from growth in world economy and lower rupee (if it drops, which I think it might).

26 Likes

Yogesh if you can put some light on Igarashi motors I m unable understand should invest or not because earlier I read that promoters put open offer for delisting this sector can see huge growth in coming years as electric vehicle is going to use more motor as of now regards

Why do you think igarashi will supply the primary induction motor? They currently make the simple motors used for seat, windows , etc.

Maruti is moving from a low margin product mix to high margin product and service. The upcoming models are all above 7 lakhs and we could expect something above scross at 15 lakhs in 2018-19. Nexa and Arena concept seems to be working and dealers are now interested in setting them up. If the concept of value migration works, these valuations may be dirt cheap IMHO.

3 Likes

@Yogesh_s - As always, thanks for sharing the latest 2018 portfolio. Since Lupin has been around for 2 years now, have you bought more during the current fall to bring the weightage back to 8-9% which was the case originally? This has fallen from close to 2000 odd levels, so am assuming that almost the same capital was again needed to be allocated as was done 2 years ago to keep weightage the same. The related question I had was, would this capital have been better allocated to another defensive stock, say a TCS, or a Infosys, or even a SUN?

Thanks,

Arun

1 Like

@itsnayan From what I know, IMIL motors are used in Electronic Throttle Control which are key component of a internal combustion engine but I am not sure if ETC is used in electric cars. So I cannot predict how much growth in electric cars will help IMIL. Some more due diligence is needed to ascertain growth opportunities. Otherwise, balance sheet looks good, growth is actually slowing down and at 38 times earnings there is no room for error.

@uservijay, I agree with all of your points about Maruti except valuation. Maruti is undoubtedly the best car company in India and that’s why I said exiting Martui may be premature when it is firing on all cylinders. At current valuations I think car sales have to grow at 15% CAGR for next 3-5 years to justify current valuations. I am not sure if sales will actually growth at that rate. In fact, with so many new models being introduced by not just Maruti but others as well, I think they might have pulled in future sales already. Sometimes I wonder if there is enough space on the road to drive cars. I certainly have given up driving.

About 2018 portfolio, this is a portfolio that I have recommended to few of my senior relatives who likes to call their own shots with some help. For me, this portfolio started and continues to be an academic exercise. About Lupin, yes, more capital is needed to bring the weight back to 9% since price has dropped. Allocation is based on valuation which in turn is based on fundamentals. In hindsight, yes, this capital could have been better allocated to another defensive like TCS or HLL but we can say that now with the benefit of hindsight. However, I feel pharma is down but not out and error was in my valuation not the company.

6 Likes