The pendulum has definitely swung wildly. It is really comical to see analysts falling over each other to downgrade the stock while few others could definitely claim “I told you so”. I really doubt all of these are genuine acceptance of failure. Most of these analysts have been caught off guard as the new management looks more genuine in describing the situation and it is not easy for them to come out of RK hangover. Now even the new management is not painting rosy picture. Some had vested interests in keeping the investors’ interest alive as YB has been a consistent IB client for these banks. A simple reading of UBS or independent analyst report would have saved the face. Now can we give a well deserved due to that famous well researched UBS report?

Having said that, we need to ponder how would RK react to this situation? will he remain a silent observer to the ongoing open heart surgery of the YB management philosophy or act from behind to regain relevance like Ratan Tata did with Cyrus?

As per the concall-transcript: Credit cost (includes all provisions - contingent provisions on standard assets plus provisions on NPAs) was 209 bps for full year fy19.

Credit cost Guidance for fy20 is 125 bps after Which it is expected to normalise. They expect half of the assets under watchlist to slip into NPAs (10k cr. List which is standard and already has 20% Provisioning). They want to get PCR on NPAs up from 43-44% to 60% in 12-18 months. All this will consume the 125 bps credit cost guided for fy20.

Gross NPAs are 7880 crs. To take PCR up from 43% to 60%, it would need 7880*0.17=1340 cr. provisions.

Let’s say 5000 cr. Assets under watchlist (out of 10k cr.) slip into NPAs . They already have 1000 cr. Provisions (20%). Take 60% PCR, meaning 2000 cr. more provisions.

So 1340 cr. + 2000 cr. Roughly accounts for your 125 bps credit cost (slightly more than 125 bps actually)

One can expect 800 cr. Provisions per quarter in Fy20.

Which I don’t think is that bad an outcome unless one doesn’t also trust the new CEO’s analysis on how the book will perform.

Guys a novice, please excuse me if you see info is irrelevant or wrong.

L&T housing finance also has an exposure to IL&FS SPV’s like YES BANK. However they have not shown them as NPA’s.

See blow an edit from an article.

“LTFH said in a statement that through its subsidiaries, it has around ₹1,800 crore exposure to six project special purpose vehicles (SPVs) of Infrastructure Leasing & Financial Services (IL&FS). It added that the resolution plan submitted by the government (at the instance of IL&FS board) to National Company Law Appellate Tribunal (NCLAT), specifies that these SPVs are capable of servicing loans to secured creditors and there will be priority on payments towards them.”

I don’t want to sound too optimistic or pessimistic however, showing entire exposure to IL&FS “ & Jet Airways as NPA’s did seem far fetched.

Even Ravneet Gill said they are being proactive.

Let’s see what other banks have to say about these exposure during their annual report.

As per RBI Audit for FY 18 - all was well till then. Things can not become so bad with in one year. Only two major negative developments have happened so far this year - ILFS and Jet Air. Further one billion USD will be raised via QIP - equity - which will be significant BV accretive. After all NPA deductions, current BV is a decent 116. With P/BV of 2 - 230 appears be a fair price.

I just reproduce old post. At time of post, few members didn’t understand & now I see a different view from them. I am happy that I took action based on earlier view and could save myself & hopefully few others.

We must understand that new management will do something different to ensure that regulators & investors get the confidence back. I still expect that we must closely watch the developments with result of next few quarters holding key of future.

The bank is good with expectations of being one of the best in private sector banks, but investors need to be careful in analyzing the correct entry level as per their risk appetite.

Provision is just one part of the story. They also want to cut down on corporate lending and bring it down from about 65% today to 50%. That when the market believes worst is over for corporate lenders and their stocks (Axis, ICICI, SBI) are being rerated. How should the market treat a company that is losing (or willingly conceding) market share to others in its core competence area?

Besides that, management is not expecting fee income to even reach 50% of its peak anytime soon.

Finally, they want to build retail assets which means even higher costs. A few guys sitting in a corporate office could approve a loan of 1000 crores to a builder. Disbursing 1000 Crs as loans to 1000-5000 retail customers means investment in sales team, staff and branches. So even if they are able to grow retail book, profits will be lower on that than corporate book.

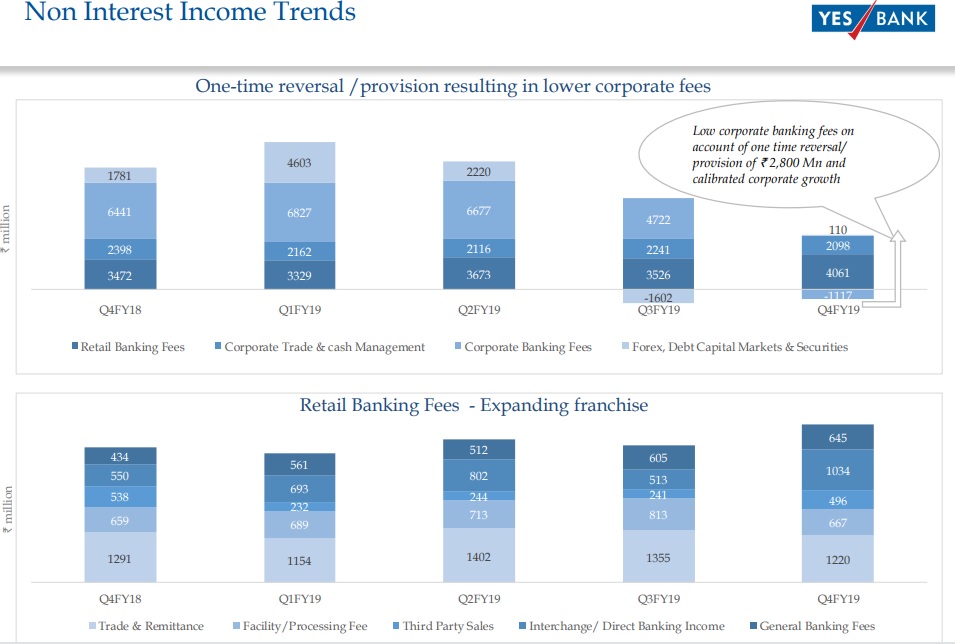

As you can see, retail banking fees grew ~20% , corporate trade and cash management was stable.

While the corporate banking fee took one-time reversal hit of 280 cr. (2800 million rupees). Referring to the concall transcript, the annual corporate fees is expected to be 1000 cr. or higher. Add to that the rest of the fee income (including retail income which is growing at a decent clip), the total non-interest income for fy20 would be 3500-4000cr (excluding any income from Forex, debt capital markets).

Imho, YB has a lot of scope and opportunity in building retail assets. It’s a massive retail liabilities brand, atleast in Delhi. Someone said about empty branches, my YB branch in Delhi is busier than adjacent ICICI and indusind branch. Even if the corporate %age comes down to 50% on account of fast retail-assets growth, 50%-corporate is a very handsome figure for a corporate bank, perhaps higher than other corporate banks.

The above article clearly says:

In what sounds like a departure from the extreme focus on retail under Kapoor, Gill said corporate lending will now become the calling card for the lender and the attempt is to only diversify the loan book.

So according to your views we should follow FIIs and not retailers ?

You know Axis and ICICI were not FIIs favorites a year ago? They have become now considering the elections , cleaned books (videocon etc) and the removal of chanda kochhar uncertainty (for ICICI).

See as a investor, it’s always easy to follow FII or MFs for margin of safety. But real investing comes from entering a firm in a phase where it’s turning around is starting (Yes Bank here for example).

FIIs will also enter Yes Bank once the overheads of NPAs etc are gone.

Thing is do you want FIIs to enter and exit before you or after you.

Disclosure : My comment is not in favor of Yes Bank but a view of an investment on it’s story and independent of who is holding and who is not. Cheers

See as a investor, it’s always easy to follow FII or MFs for margin of safety. But real investing comes from entering a firm in a phase where it’s turning around is starting

Very valid point. This is the most important thing to ponder. By the time analyst give a buy call and the FII buy up the stock. Price would already have appreciated (see how the price of ICICI and Axis move in the last 18 months, specifically after they came out with losses).

If you buy before FIIs you will make more money, with a caveat that you might have to wait longer and if you buy after FIIs then you will make money as per the company’s growth.

People who prefer to buy “after FIIs” are better off investing in HDFC bank as FIIs are already fully invested in it and 20% returns are guaranteed there.

Edit:

As OP said, this comment is not just for Yes. People can think on this lines for any sector or company that is going thru a difficult phase. Take for example, Maruti or Hero Motors. Every one is shitting on Hero right right now. Maybe this is the best time to buy the stock if you want to make above market returns.

Sometimes I feel this forums should have a counter for +ve and -ve posts for a particular company’s thread. Best time to buy the stock of that company is when the counter for -ve post becomes high and best time to sell is when the counter for +ve post becomes high.

This looks like a good idea. Like a sentiment indicator where people can vote on their view of the stock and based on it an overall sentiment is given. Whether one goes with the sentiment or goes contrarian is upto the individual investor. I guess moneycontrol has something similar. But the quality of investors is much better here. Hopefully this will also help investors to stay away from such stock like manpasand or 8k miles before the disaster.

This is not related to yes bank. But a general observation ( for medium to large sized companies). If there is no damage to stock price ( or it goes up) on a very bad result, then may be market thinks the worst is over. We have seen it in ICICI and AXIS.

Valid point, can seniors throw some light. Reading lnt fin management commentary they clearly say that as per RBI rules these are not npas …so as per RBI rules is entire yes Bank exposure to ilfs npa or they have been over cautious or lnt fin is being less proactive…is this really a management decision or rules are straightforward and to be strictly followed…thanks

Dear all… I tried to get hold of Macquire report on the double downgrade … And the UBS report dated Sep 2018 when they first started the downgrade cycle n YES. I have YES in my core portfolio and so obviously trying yo take stock of this bad news and deciden the next course ( exit/ stay/ buy more ) . Thankfully my cost is pretty much at these levels and not too bothered by the consensus and near unanimous sentiment from analyst community. Udyan Mukherjee was quite harsh on CNBC today ( I definitely respect his views) .

So I’m keen to understand these analyst reports from UBS and Macquire … and base my future actions post a thoughtful read .

Thanks Ram