Bombshell by the new CEO : Entire top mgmt to be replaced with new hires.

2 Likes

1 Like

Its in Airoli for 4000 seats.

We are working on few projects linked to it.

3 Likes

Surprise 1500cr Loss

This shows the book’s earlier were fudged and revealed less than actual. No wonder RK wanted to continue forever.

New CEO wants to start with a clean slate. We can only “expect and wish” that these results have fully factored the earlier sins and nothing is left over to account for in future. If next quarter also they do the same thing then it will be too bad. But it is certainly possible.

1 Like

Dats what happened with SBI as well as rite. Every new comer wanna build on low base so dat it looks gigantic when next quarter results come out. We need to hear out d Mgmt commentary

1 Like

Nothing wrong in results, loss has been reported due to full provisioning for IL&FS account of 2650 cr and additional Provisioning for Jet airways for 550 cr, even Indusind has to account 2700 cr this quarter due to IL&FS. Bank has very aggressive expansion plans. Will go long way, considerable part of my portfolio.

7 Likes

This sort of provisioning is usually only the beginning, going by what has happened in the past - look at PSU banks in the last 3-4 years, Axis/ICICI in the last 2-3 years - this is where Yes Bank caught everyone’s attention (including RBIs), since they didn’t appear to be affected like Axis/ICICI. What’s known to everyone comes out first, the rest later.

Why is IndusInd a benchmark for anything? These sort of comparisons in a race-to-the-bottom scenario mean nothing. I saw lot of comparisons of RBL Bank to Yes Bank during their IPO and post that as well but now no one would dare make that comparison (they should, at least to themselves). They (IndusInd) appear to be in similar situation as Yes Bank but strangely trading at a much higher P/B multiple (4x). Both Yes Bank and IndusInd appear to have provisions in a single quarter or single account that is roughly equivalent to 25% of their PAT in the last 5 years. If that is how quickly book profits can vanish - it reminds me of Taleb’s Turkey problem where the Turkey thought the butcher was its friend as he fed it everyday - until Thanksgiving.

24 Likes

Thanks for sharing. For me the highlights in this is in the last question:

“this year, we grew around 17%, 18%. But what we want to do is, we want to go and stabilize at, let’s say, 20% to 24%. We don’t want to chase a 40%, 50% growth strategy that has been there in the past. We just want a much more calibrated growth model. And quite clearly as a bank, our aim is to be generally consistent long-term-sustainable ROE (I think this should be RoA) in the vicinity of 1.5%. So obviously, that’s a long distance away at this point in time… we want to stabilize at a growth rate of 20% to 24% and ROE which is in the high-teens.”

It seems like Yes is going through a complete reset. They want share of corporate loans to go down to 50% from current 65-68%. They want to build retail and SME to the other 50% and they are hoping their fee income comes to around 50% of its peak. This all sounds disastrous to me. In fact they are looking like a PSU bank on their corporate side with much worse CASA, fewer retail assets and dwindling fee income.

The market was already expecting this and that’s why we have seen it correct from 400 to below 250. Now if we give a benefit of doubt to management and say they will be able to achieve what they plan in next 15-18 months then still it does not deserve to trade above 2 times P/B. If you factor in the risks, it should trade even lower may be. Most probably it will trade in a range for next 2 years.

Disc: invested around 220.

Analyst presentation post results

7 Likes

Just wondering what will be the reaction of Mr market on Tuesday…given the analyst meet call…Gill has said it’s not about kitchen sinking… good to buy at 200 and hold onto for a year or 2

1 Like

Video link is not working.

I personally believe this will be the best interest of all shareholders to have a open book… I believe the new CEO is trying to play a open book game and take the company into new territory…

This action will not be liked by short term investors looking for quick profit and they will surely sell in huge chunk and drag the price to surely below may be even to 52 week low…

3 Likes

Nothing hidden as far as Yes bank is concerned, market was more apprahensive due to Rana Kapur pledged shares, it was a clear sign of low corporate governance as he was MD. He gave loan to R Navel in favour of same, Reliance Capital gave him loan of 3000 cr on his personal holdings. NPA divergance till March 2018 is zero and certified by RBI. Ravneet Gill has cleaned the slate completely now, perception has been changed, large investments will attract yes bank now as FII’s know very well that this is one of best bank with digital banking edge. I doubt any further downfall. DHFL and Zee loans are part of stress book however it is less likely to turn NPA due to good quality assets and colleterel value. Growth will slowdown however ROA will increase due to credit cost drop hence P/E and P/B will rise due to improved corporate governance.

4 Likes

We can’t say that. When IDFC split away IDFC Bank as a separate entity, they also declared huge NPA and claimed it as a one time hit and that post those NPA declarations, their book was pristine. They kept declaring fresh slippages for many quarters after that and stock price is down from 80 to 50 odd more than 3 years later.

Divergence is zero not NPAs.

Yes bank is one of those shares where retail holding has increased the most in last 1 year. FIIs are buying ICICI and Axis for now. YES is out of favour with them for now.

2 Likes

There is no comparison between IDFC Bank and yes bank, start studying asset book quality. IDFC bank without CapF had largoe legacy Infra loan book which was inherited from IDFC, infra loan book is worst quality loan book for a bank. Secondly Its clearly mentioned NPA divergence is zero not NPA, are you looking for a zero NPA bank, better stop investing in financial stocks and rest in peace. ICICI and axis were at worst state than Yes Bank last year and still expensive. Market like what and hate what has no relation with value of stock, its our Job to foresee and hope for a valuation correction in future which is process of large wealth creation.

2 Likes

ICICI and Axis have much better retail franchise compared to Yes bank and they are much more hungry and persistent about the growth of their retail book.

When the whole industry is so Gung Ho about the retail credit, yes bank doesn’t seem to bother about it. Market leader HDFC Bank has 30% share in the active credit cards and they are still hungry for growth in the number of credit cards on the other hand Yes bank doesn’t bother to share single statement in their investor presentation on their credit card franchise. I’ve account with Yes bank and whenever I visit their branches are almost always empty. I don’t understand how will they grow given the impending crisis in their corporate book.

Let’s see how bank will come out of this mess under the leadership of Mr. Gill.

Thanks

4 Likes

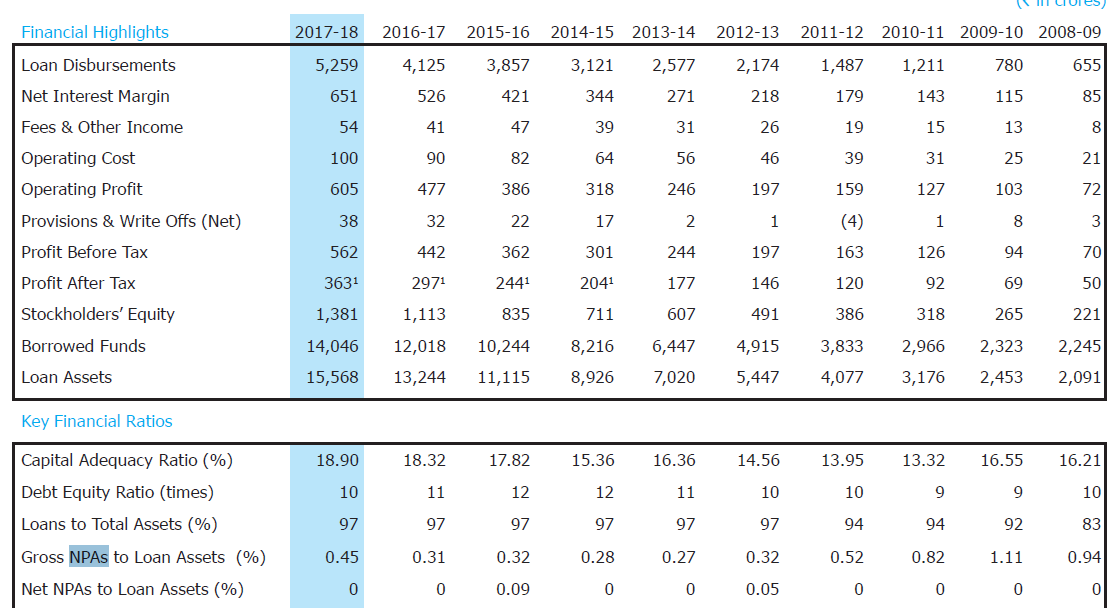

Surprisingly, it is possible to be a zero npa company even if you are in the lending business. Check out Gruh Finance. Over the last 10 years, it has been a NIL npa company with the exception of FY2015-16 at 0.09% and FY12-13 at 0.05% (screenshot attached of last 10 years - last line).

If a loan has gone bad, please provide 100%. Whatever & whenever you recover, you can write that back. SIMPLE ![]() .

.

4 Likes

I will say it again. Divergence is zero not NPAs.

IDBI reported NPAs of 30% plus. Suppose they come out and claim their NPAs are only 3 % and rest is divergence. Then a few quarters and RBI action later, they come back and say our NPAs are 30% actually but now our divergence is zero. Will that make IDBI a great bank? That is what Yes was doing all this while.

Again. How do you know that? This is what experts are saying.

https://twitter.com/kothariabhishek/status/1122710411499851777

I also want to know what is the book value for a bank leveraged more than 10 times and possibly having GNPA of 8%? That takes you to near bankrupt category.

4 Likes