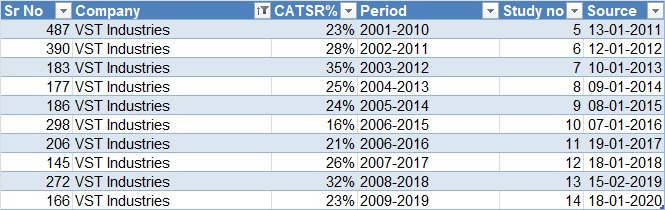

If we assume that intensity of taxes have affected recently to Ciggarette industry, at least VST industries appear to be escaped that. Find enclosed Moneylife 10 years Wealth creation study data. We find VST Industries being consistent candidate appearing with around 20% CAGR.

Except for first 4 studies of Moneylife, it appears in next 10 edition of decade wealth creation. On the thread I also shared Global trends showing Cigarette being among few cockroach surviving since Dianosour ages.

The key call one should take that future would be like past. This is big assumptions and may not be correct in very long term given the awareness and health issues. In fact, the health issue generated by Fast foods would be comparable (given the scale at which it gets consumed), if not more, then Cigarette in my opinion.

Having said, I would keep monitoring trend, sales growth, profitability and distribution. Considering the recent performance of ITC versus Godrey and VST industries, I find that small players have relatively performend better than Largest players. The reason I do not know. But if that trend continue, no competition from newer player, huge bargaining power with customer and regulatory pricing (taxes are passed on to customer). Despite volume growth decline over decade, the profitability has continue to grow. It may not be blockbuster but would be above average performer in my view. My view is right or wrong, would be known only after 10-15 years:grinning:

So please do your due dilgence before taking any investment decision

Discl: Same as in previous message

I believe VST Industries shall also get benefit of new corporate income tax 25%+surcharge. The notification is applicable to all corporate.

Refer to Note 3 in Quarterly results for period ending 31 December 2019.

Why doesn’t Mr Radhakishan Damani take over the company as he own around 29 % stake ( 25.95% through Bright Star Investments Private Ltd. & 3.26% in his personal holding)

Is VST allowed to open new factories in new geographies?

Would like to know your views on the rising taxation hurdles that VST is bound to face as the govt tries ro recover lost revenue.

As in the past, if this is transferred to the consumer, it could result in more preference to cheaper illegal alternatives . While a firm like ITC probably would not have to worry too much thanks to its diversified portfolio , wouldn’t this affect the outlook for a player like VST?

High Taxation is part of Cigarette industry. There is always a contigency and Cigarette levies increased to finance same. So I personally see limited downside from that side. This is my view and may be completely wrong.

On Diversification of ITC in other business, one need to ROCE is also lower for ITC (despite dominant position in Cigarette due to other business). I have my investment in ITC as well and hence personally do not know which company is better place between ITC and VST Industries. One has to take call after looking at his/her own risk profile.

Discl: Invested in ITC and VST Industries. Not SEBI registered advisor, not a reommendation to invest

Today VST industies announed FY20 resutls and dividend.

In my limited understanding, the performance is good considering almost 8 days being lost due to COVID in March 2020. While as compared with previous quarter, sales and profit declined, but as compared with Q4FY19, Sales grew by 14% while Net profit increased by 33%. Excise duty charged to P&L was almost tripled in Q4FY20 to Rs 58.16 Cr as compared with Rs 21 Cr in Q4FY19. Despite such jump in excise duty and increase in other expenditure, Q4FY20, the company reported excellent growth in net profit.

The dividend declared of Rs 103 for FY2020 as against EPS of Rs 196, indicated dividend payout of 52% (considering that last year company bear DDT, it is not even matching total cash outflow on account of Dividend to shareholder). Normally, company has policy to pay around 70-75% of net profit as dividend. This may be due to inferior Q1FY21 performance and expected slow down during FY21 (when recovery may be slow due to lockdown).

Overall good performance in chellanging time in my view.

Discl: among my Top 10 holdings, View may be biased, not a SEBI registered advisor, Not a recommendation.

The reduction in dividend is quite unusual… Company must be expecting a very large hike in taxes on tobacco. The payout it has given ideally would suggest a 200-220 cr PAT range for FY21.

I recently stared buying into VST. Looking at financials and recent annual reports, I am unable to figure out 2 things. Perhaps @dd1474 sir or other fellow boarders tracking VST for longer may be able to answer:

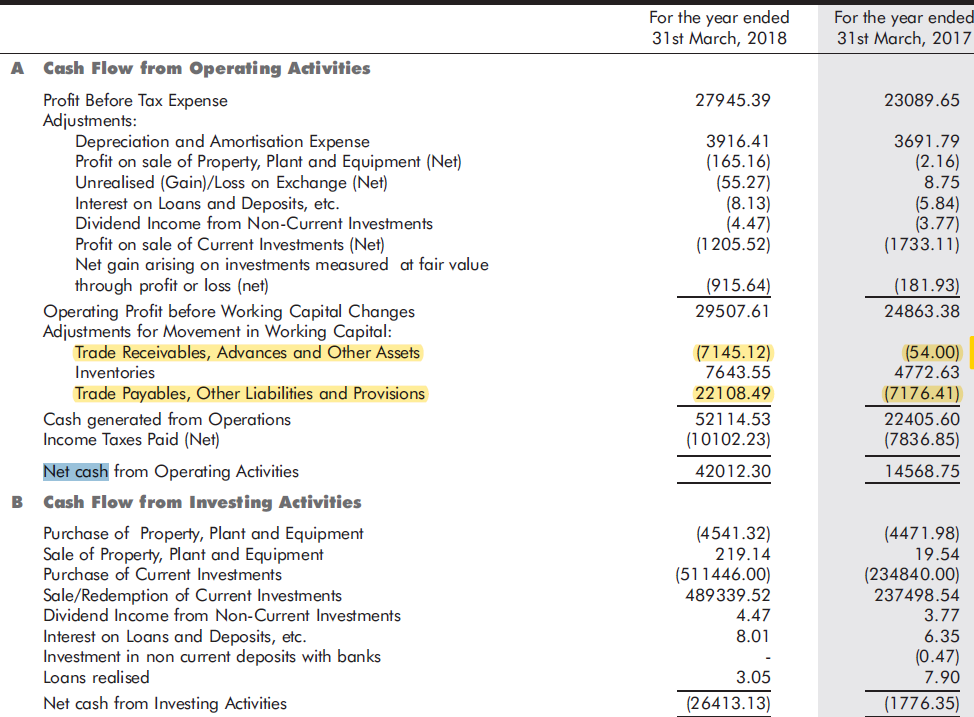

Why did CFO increase tremendously in FY18 and has sustained since (though slightly reduced vs FY18)? Aside from increase in PAT, significant increase comes from trade payables / WC changes. Is this somehow related to GST that came into effect in July 2017?

Snapshot from FY18 AR:

Despite CFO increase tremendously since FY18, excess cash is being put aggressively into buying ‘investments’ instead of ploughing back into business or returning to shareholders. Why?

On point 1, my view is every year would see some change in working capital days expansion/reduction. There would some reason to attribute to same. Hence, I do look at 5-7 years working caital days to look at trend along with ROCE and Cashflow from operations. I do not give more weightage to working capital days in a single year till the movement in range which has been observed in past.

On point 2, the company is in business of Cigarette. Cigarette industry need approval for capacity expansion from Government which is not forthcoming as the product has adverse impact on health. Hence, there limited scope for installing new capacity for the company. Rather than deploying money in other business, like ITC does with deployment in other FMCG products, along with Paper and Hotel business, the company management is more prudent to give money back by way of dividend to shareholder who can decide best use based on their requirmeent.

Hope these answer your queries.

Discl: among my top 10 investment and my view may be biased. Not Recommending investment, Not SEBI registered advisor

Dear @dd1474 sir. Thanks for your prompt reply. On point 2, fully respect management’s decisions to make now diversify like a ITC but then why is Dividend payout ratio dropping despite improving profitability and excess cash being invested in Debt MF instruments instead?

As you can can seek from the table In shared, these investments have been in 150 Cr range and divodend/CFO has fallen to 50% from high 80% range.

In my limited understanding, VST is likely to remain cigarette company and would distribute large portion of cash generated through dividend and buyback. Generally dividend payout ratio is around 65-70%. This year when board declared dividend in board meeting, COVID impact and time of uncertainty were not known to anyone. During such uncertain time, a prudent and conservative managment would try to keep liquidity in business to overcome any forthcoming crisis. Hence, I would wait for couple of more year to come to conclusion that maangment has decided to reduce dividend payout Ratio to 50% from 70%. Let us wait and watch, I see this year lower payout as onetime decision than regular policy change. I may be wrong in my understanding and only future would tell us about same.

Was not able to find a reason provided by the company anywhere. Definitely raises concern considering that he was with the company for a long time (Executive MD for 6 years and MD for 3). As the company is cash rich, it cannot possibly be a cost cutting measure. Maybe a dispute in between owners and management.

Yes, at first sight difficult to comprehend as Mr. Lahiri has been long with company and groomed for the role. His compensation was much lower than that of previous MD when he retired but he was almost 20 years older than Mr. Lahiri at that time. My best guess would be that Mr. Lahiri has either been poached by a competitor or had a fallout with the board. It’s certain whatever happened happened unexpectedly as no successor announced.

I am going through VST Annual reports and one thing that pops out is how much of MD&A is dedicated to Litigations & Tax disputes while business commentary is rather thin and not much change over last 2-3 years.

Is it ‘normal’ to have so many ongoing litigation and tax disputes for a company the size of VST? I appreciate it is in a ‘sin’ industry, but any comparisons to Godfrey, ITC or even liquor producers may help.

Is there any political issue at play here also? State of erstwhile Andhra Pradesh has been issuing adverse notices to the company and dragging them to court often. Couple of these seem to have been decided in favor of the company (e.g. land-grabbing cases in 1989 and 1991) but despite changes in governments of over last 3 decades there seem to be no end to such disputes.

Please refer to page 20 onwards of AR FY19 under following section:

“SIGNIFICANT & MATERIAL ORDERS PASSED BY THE REGULATORS OR COURTS OR TRIBUNALS” for list of ongoing cases.