/https://www.bseindia.com/xml-data/corpfiling/AttachLive/4870e007-4f3a-45b6-a775-03da7a021fb6.pdf

A very informative quarterly presentation this time. They have also strengthened the board with some good names added like Mr. Ramesh Damani (who is also on the board of DMART).

1 Like

The business model of VIP Industries is changing fast from trading to own manufacturing through its facilities in India and Bangladesh. This will provide a structural boost to margin.

1 Like

Roa and roe will also reduce due to capital required

1 Like

VIP’s Vice Chairman (also Ex-MD) seems to have shifted back to London again. In my view unstable management and late recognition of industry trends are the key reasons for VIP to slowly and steadily loosing market share to the competition. I think VIP has been reactive to market changes rather than proactive.

1. Unstable management

2. Overlapping brands, inability to protect the flagship brand from loosing mojo (old article but useful)

3. Disproportionate efforts to set-up soft luggage facility in Bangladesh to take advantage of low labour cost. By the time it was ready to produce significant quantities, market shifted towards hard luggage, which is not labour intensive.

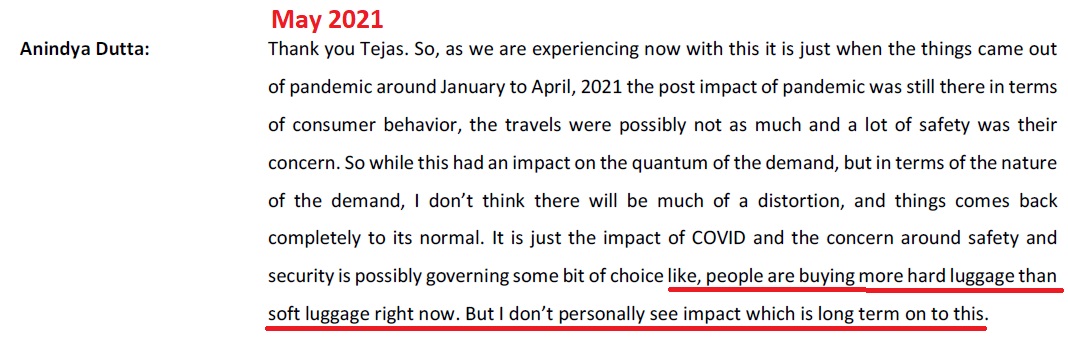

4. Late in understanding shift in trend from soft to hard luggage : International market was showing clear signs of shift, much earlier (before covid). While VIP has recognised the shift and started investing in new hard luggage capacities from FY22 end, but they were bit late. Competition had much ahead clarity that future is hard luggage.

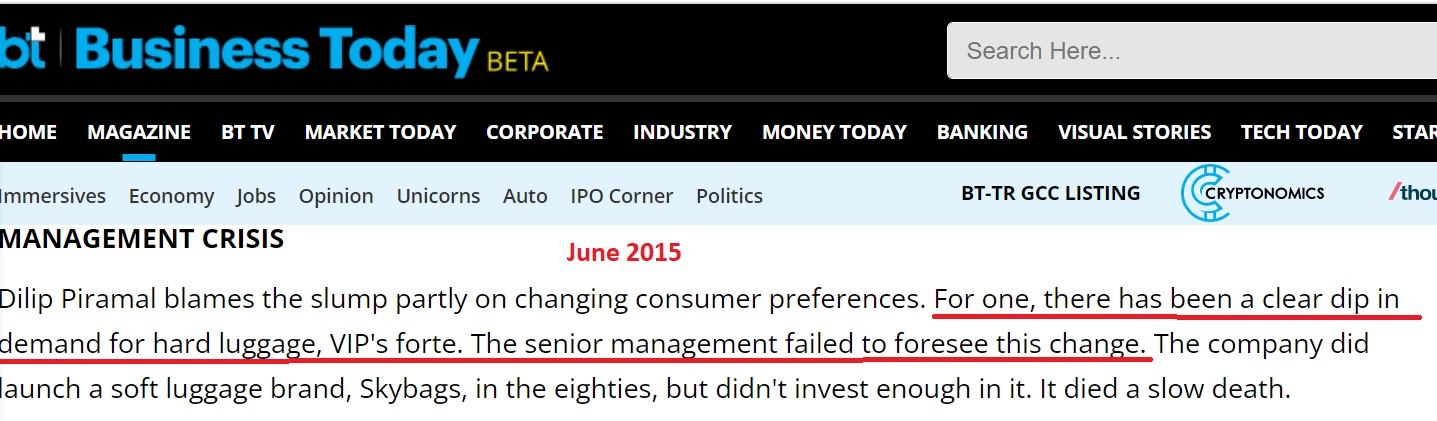

If one goes back to few years ago when industry trend shifted from hard to soft, VIP was late in understating the trend and lost market share to Samsonite.

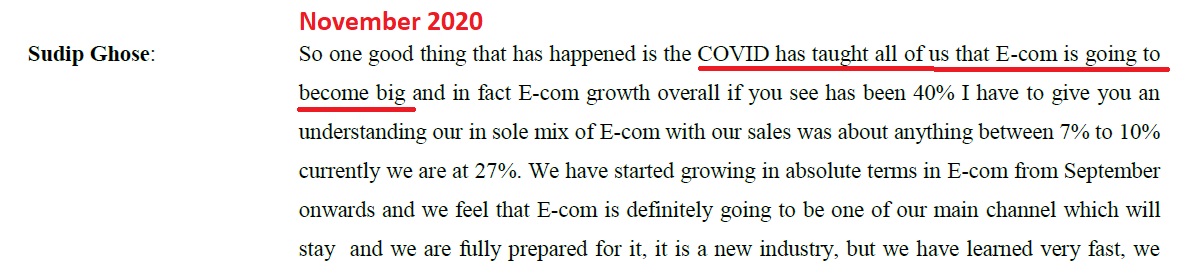

5. Late entry in e-commerce business: While competition already had significant presence pre-covid, VIP learnt only when no other option was left.

6. Late in recognizing potential of value segment : Post GST implementation and discontinuation of government incentives to luggage manufacturers in China, it was clear that unorganised players will loose ground and there is strong growth potential in value segment. Covid epidemic did accelerate the shift from unorganised the organised players; however, VIP was again late to understand this and started responding to this change only when it became too obvious.

While there is huge growth potential in luggage industry, VIP is still the leader with much higher market share compared to second player, has better financial profile than any of its competitors; unimpressive growth could be a factor of less proactive approach.

When I started reading about this industry during early FY21; threads on valuepickr forum and last few years annual reports gave me clear hint about existence of the issues. However, when I read many research reports on VIP in the last 2-3 years, I found that none of them have acknowledged or mentioned the issues.

Disclosure: Invested in VIP’s competitor and hence may be biased. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

10 Likes

2 Likes

VIP’s Bangladesh Operations – Game Changer or Exaggerated Story?

VIP has recently announced capex plan of Rs.200 crore for FY24 and a significant portion of that is planned towards manufacturing bagpacks, handbags and soft luggage in India.

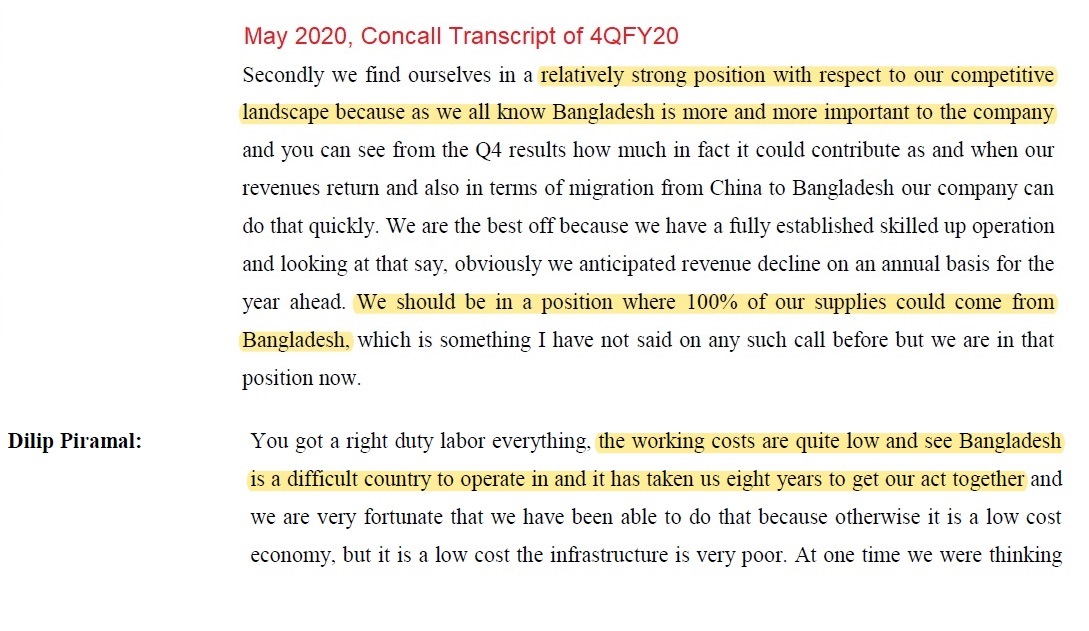

If we go back in the history, VIP had announced successful completion of manufacturing facilities in Bangladesh with eight years of efforts during FY20. As per the management, this was supposed to provide significant advantage due to low cost of production and could help in sourcing almost entire soft luggage from Bangladesh. VIP has time and again showcased its Bangladesh operations as major game changer due to supposedly lower cost of production.

By the time Bangladesh Operations were streamlined, it was quite evident that trend has changed towards Hard luggage (hard to soft ratio of 1:1 in FY20 to 2:1 in FY23), here Bangladesh has no cost advantage due to low labour intensive product. The same resulted in all industry players incurring capex for Hard luggage in India (including VIP) during FY22 to FY23. However, Bangladesh plants were still perceived advantageous to VIP for catering to soft luggage, bagpacks and bags.

The recent capex plans in India are justified by the VIP management - to supply in certain regions to balance between logistics and production cost advantages. While the capex in India might be required; Bangladesh plants which were time and again presented as major game changer for the company, do not seem to be so. To best of my understanding, Bangladesh plants could have been used interchangeably for soft luggage, bag packs and bags; had total landed cost actually been low.

In my view, VIP management could not judge the industry trend & cost matrix and ended up spending significant management bandwidth and capital in Bangladesh operations, with benefits not proportionate to the efforts.

Disclosure: Invested in VIP’s competitor and hence may be biased. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

2 Likes

Mr. Anindya Dutta, Managing Director of VIP Industries Limited, has tendered his resignation on 14th August, 2023.

CNBC’s view on the development

2 Likes

Is anyone tracking this development or how this could impact the valuation? Also, considering Investcorp exiting by selling entire stake in Safari (only other major listed peer) last month and now this news, is industry facing some headwinds which are not known to the retail investors yet? Requesting view from senior members (@GautamBafna) as this is my first post on VP. ![]()

2 Likes

It is difficult to comment on valuations as the promoter and potential acquirers may have different expectations and I cannot predict something very uncertain. Who will acquire it (may be conglomerates like Tata/Reliance or PE funds) and whether he will be able to change VIP’s fortune, is another uncertain variable. I prefer track record and certainty to the extent possible and I’m a happy shareholder of VIP’s competitor.

Planned exit by VIP’s promoter is due to succession issue and not due to industry prospects. Also, Investcorp selling small stake in Safari is a non-event as most of the PE funds have time frames and the quantity was absorbed by domestic funds. While there is significant increase in number of Safari’s shareholders holding share capital upto Rs.2 lakh, but change in percentage shares held by them is not significant.

As per the few research reports published in July or August, managements of both Safari and VIP indicated slowdown in growth at the beginning of Q2. I do not have any idea about growth rates in subsequent months. No industry is immune to short term fluctuations and luggage industry has also witnessed it in the past. However, I see long run way for growth in this industry with probably double-digit growth rate for a long period and not concerned about short term events in between.

Our investment horizons and view points might be totally different. Hence, please do your own due diligence and research accordingly.

1 Like

VIP Industries Q2FY24 Concall Summary