Sure, I will try that. Thanks!

Even though the list is on hold, do you guys think it is a threat for VIP industries?

But the management has said that Central Police Canteen contributes very less to their revenues.

They do produce locally, also source from Bangladesh.

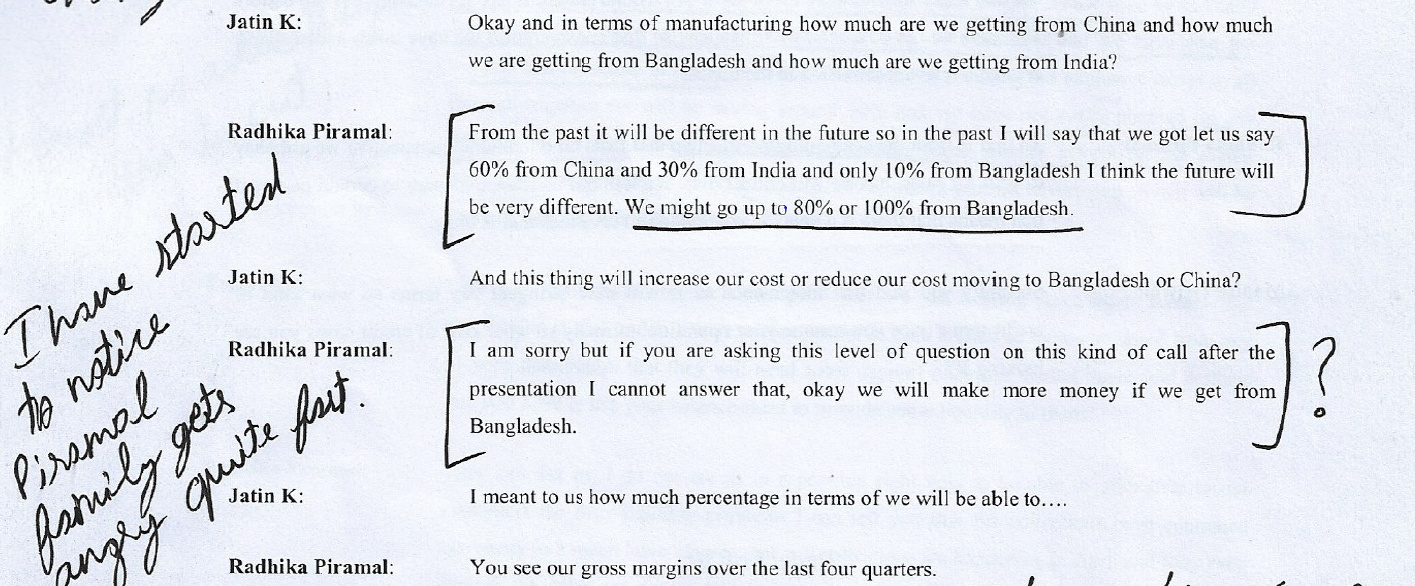

But they import 90% of their raw materials from China. Read their Q4 con call page 10 conversation with Varun Goenka.

I have also uploaded a snapshot below.

VIP shifted their production to Bangladesh but RM source from China . The reason for shifting from China to Bangla is much lesser labour cost…

Dis . invested

Here are some points on VIP Industries which I came across…

Positive

- Management of company has said that they can survive this pandemic even if there is zero revenue for next 6-8 months.

- Gross margin increased from 48% (Q4 FY19) to 58% (Q4 FY20). This was mainly due to shifting their production from China to Bangladesh partially. As the plant in Bangladesh is wholly owned by them.

- Till now their manufacturing was 60% China, 30% India, and 10% Bangladesh. But now company plans to make it 80-100% from Bangladesh. And for reaching 100% manufacturing from Bangladesh there is no further capex requirement .

- They also mentioned that they also have to depend on China sometimes for some special/innovative products.

- On importing from Bangladesh company does not required to pay import duties whereas they have to pay 20% import duty on Chinese products. This is a huge competitive advantage .

- Further to mitigate risk of dependence on Bangladesh company has manufacturing unit in India. Also they have a office in Hong Kong which can continue buying from China anytime.

- Company has received waiver of rent for 60% of their stores , which is quite a good sign.

- Demand for hard luggage is on rise and it is good for company as there is no competition from unorganized sector in this segment.

- Due to COVID there is rise in general trade. This is beneficial for VIP Industries as their market share is higher their compared to modern trade. But we need to remember this is temporary.

- The fluctuation in Rupee is not going to affect VIP Industries for at least 7-8 months as they do not anticipate new orders from China and are well stocked.

Not So Positive

- Company has increased their borrowing limit from Rs 100 cr to 220cr. But till now they have utilized on 100cr.

- Due to COVID company’s June quarter which is generally their strongest quarter got affected .

- Marriage Season got destroyed which used to increase demand for luggage. This season contributes 30% to sales.

- School Season got destroyed as everything went online. This season contributes 20-30% to sales.

- But it seems that these season would just be postponed and not cancelled as if marriages were planned it wont be cancelled instead just postpone and schools are expected to open by September as per government.

- VIP Industries is planning to close around 50 to 100 stores out of their 250 stores.

- Company still haven’t received their claim on the goods which lost at Ghaziabad warehouse due to fire. Company has also made a provision for it of around 8 cr.

General

- Company has taken 30% reduction in cost which also includes their decision to not advertise this year as to cut cost.

- Central Police Canteen(CPC) had released a list of products which were not Indian and decided to not to sell them in their canteens. VIP Industries products were also mentioned in that list. But immediately that list was taken back and government had put a stay on that list. Even though CPC contributes very less towards their revenue, I think VIP Industries being labelled as Non-Indian product at such times when a movement of boycotting Non-Indian is trending can affect its brand value.

- While reading more about the company I realised that Ms. Nisaba Godrej & Mr. Ramesh Damani are non-executive, independent directors in company. It is quite amazing to have such people on board!

- This pandemic has given opportunity to the company for focusing on e-commerce and increasing their market share in this channel.

- We can also expect the move of demand from unorganized to organised players, temporarily.

Thoughts

It took eight years for the company to set up its plant in Bangladesh. As country is quite behind infrastructural it becomes very difficult to set up a plant which would be as per their standard of products.

I think this creates a Moat for the company which will keep widening as they further try to expand it.

The time and efforts put by company has started to pay off and it would be different for any other competitor to set up a plant like this in near future.

This Bangladesh plant is full owned by them which means that it is unlikely that VIP Industries would face a supply chain disruption.

This is also a huge competitive advantage! As other peers would be relying on their suppliers for shipment and plan according to their rules.

Another Moat which I found was their Float money.

VIP Industries has Float of around 360 cr : Trade Payable of around 292cr, other Current liabilities of 40 cr, & some provisions and differed tax.

This shows that approx. 30% of their Operating Assets is supported by their Float money .

Disclaimer: I am not a SEBI registered adviser. All the information provided by me are for educational/informational purposes only.

8 Likes

Although the plant has been put up in Bangladesh, the raw material would still be coming from China which can be a negative, should china increases duty on exports for Indian companies or puts up some restrictions.

Yes, that is absolutely true. May be this importing from China was one of the reasons why it was included into the Non-Swadeshi list released by Police Canteen.

I think it’s quite unrealistic because the plant in Bangladesh they follow what is the tax rate in the respective country basis not each industry.

Dis invested

Disclosure: Not Invested.

2 Likes

I was on the call and heard it too. Chairman was dismissive as soon as he heard an individual investor is asking the question. To be fair, the question was referring to some item in the annual report which Chairman felt that it should have been asked at the AGM which happened yesterday. So he was not in mood to answer questions about FY 20 and was more focused on Q1 performance. Also the invite clearly called for “Conference Call for analyst/institutional investors” . So I think he got annoyed that an individual investor was allowed to join the call in the first place.

I have attended one Tata Steel call where I was respectfully told by call center employee that call is for “analyst/institutional investors” only and I had to disconnect. Once I attended a conference call where I was told that individual investors are not allowed to ask questions.

3 Likes

I would also like to mention that I noticed this similar behavior in their previous con-calls also, if you read their calls caring you will understand that the management gets annoyed very quickly.

Here is a screenshot of the statement which I found during my analysis:

9 Likes

I feel that the analyst should have read the presentation, if you just keep on asking this basic question again & again , you are bound to get annoyed. The fault is of the analyst.

1 Like

Yes, it can be but this is not the first time you notice this and when you are at a high post like being a CEO your image plays a vital role in company’s brand image.

3 Likes

My views on VIP Industries. I think the risk reward seems favorable at this price with a recovery expected in travel and tourism. Moreover, no matter what people think of this business, their 10 year sales/PAT growth and an average ROCE of 20-25% suggests the business has a moat and the industry has entry barriers. Let me elaborate below.

Luggage Industry size globally and in India

The size of the global luggage industry (including unorganized) is US$180bn1 and has been growing at about 5% CAGR over the last 15 years. This definition includes sub-categories such as handbags, luggage, bagpacks etc. Global per household spend on luggage is around US$80.

For comparison, the size of the Indian luggage and bagpacks market is about US$3bn and has been growing at 12% CAGR over the last two decades. Approximately 60% of the market is still unorganized versus 75% in 2005. Indian per household spend on luggage is around US$10 (1/8th of global).

The key drivers of the luggage industry globally have been rising business and leisure travel, luggage and bags being treated as lifestyle products and proliferation of different usages – sports, business, education, trekking, fashion etc.

In India, all the above is applicable but in a more accentuated way given the rising incomes, aspirations and mobility. Additionally, weddings and gifting are additional drivers for luggage consumption in India. The overall TAM in India can compound at 10% over the next 10 years with steady share gains for the organized players like VIP.

Industry structure globally and in India

Globally, organized luggage industry is consolidated with top 2/3 players taking a large share of the market. Several of the large global brands are very old. For example, Samsonite, the global leader is a 100+ years old. Other large players like LVMH and Delsey are also 50+ years old. India is no different, with VIP and Safari (#1 and number #3) players being around for the last 40+ years. The second largest player in India is Samsonite which has also been in India for the last 20 years. Luggage as a category has few examples of new entrants which have scaled up meaningfully. This is despite e-commerce and modern format retailing becoming large channels over time.

Incumbents have been able to retain their market shares over time by converting the luggage from an utility product to lifestyle product with strong brand identities. Branded luggage is better quality and comes with warranty unlike unbranded. Incumbents also have distribution advantages due to wide reach, ability to share higher channel margins and monopolizing the limited shelf space in a store.

Luggage companies globally and in India have remained highly profitable. Global leader Samsonite makes gross margins of 55% while the Indian trio of VIP, Samsonite and Safari make gross margins between 45-50%. Moreover, gross margins have moved up over the last five years in tandem for all players. Samsonite and VIP make post tax ROCEs of 25-40% while Safari which operates completely at the mass segment of the market also clocks 12-13% post tax ROCEs (improving directionally).

VIP – key competitive advantages

Brand strength : VIP is India’s leading luggage brand with a 40% organized market share in luggage. Given the large unorganized market, VIP’s share in the overall luggage market in India is ~15% offering a large growth runway as increasingly consumers turn to branded luggage.

VIP has brands across segments from mass (<Rs5k), economy (Rs5k-7k) to premium (Rs7k+) although their brands are the most dominant in the economy segment. All the brands are either number 1 or 2 players in each of the three segments. VIP is a dominant leader in the economy segment with 60%+ share (per mgmt.) while Samsonite leads the premium segment and Safari leads the economy segment.

Like most other leading consumer franchises (PIDI &Asian 4%), VIP spends 5-6% on advertising and promotions which translates into annual spends of Rs100-120cr on brand building which is 30% higher than Samsonite and ~3x Safari. The absolute size of these ad spends also acts as a barrier for a new player to build strong brand in the category. The company has demonstrated the ability to launch and scale up new brands – Skybags and Caprese which were introduced after 2010 contribute to 40-45% of sales for VIP today.

Distribution advantages: The brand pull becomes very important for a voluminous category like luggage as distributors and retailers are only willing to stock what sells. VIP’s broad channel mix is as follows: CSD (20%), EBOs (20%), Modern trade (30%), Traditional channel (25%) and e-commerce (5%). Except e-commerce which does not have a space restriction, all other channels naturally stock brands with strong consumer pull.

This is also evident as Safari, the weakest brand among the top 3, has to offer 40% channel margins versus 25% for VIP. Strong brands such as VIP and Samsonite also find it to easier to attract franchises (50% EBOs are franchise owned and operated) while Safari has found that difficult. VIP had 500 EBOs (2.5x Samsonite) until pre-COVID. All players have decided to rationalize the EBO count due to COVID until demand comes back.

Rising e-commerce penetration globally has not led to any new brands or private label taking meaningful share from the incumbents. Instead, e-commerce is turning out to be a new channel for the brands. For example, Samsonite Global gets ~15% of its sales from e-commerce.

Competitive advantages corroborated by long term financial performance:

VIP’s financial performance is comparable to that of very high-quality consumer discretionary franchises in India in terms of earnings growth, return metrics and FCF generation (given consistent dividend payouts).

Revenue drivers

Medium term revenue drivers for VIP would be share gains from the unorganized sector, reducing luggage replacement cycle (from 10 years to 5 years), rising per capita consumption and premiumization of the portfolio. India’s per capita luggage expenditure is small fraction of global averages suggesting a long runway for growth (India at $1.5 versus Europe at $11 and US at $24). Source: Ambit report, Statista.com

In terms of product mix, luggage is 75% of revenues today while faster growing categories such as backpacks and handbags are 25%. The latter two have been growing faster given lower organized sector penetration, lower price points and lower replacement cycles. These should grow at 25-30% and will contribute 35-40% of sales over the next 4-5 years.

Skybags, VIP’s main backpack brand launched in 2011 is already India’s number 1 brand by value. Caprese (women handbags) was a late entrant but has gained share and crossed Rs1.3bn in sales already. Handbags is fragmented market today as it started the consumerization journey much later.

Near term , the recovery in revenues would depend on the lifting up of lockdowns and a revival in business and leisure travel. Historically, trends in aviation traffic have been a good proxy for luggage industry growth rates. The is correlation between the two but not necessarily complete causation.

In a post COVID world, while business travel may be impacted for some time due to travel cuts, leisure travel may bounce back fast. Leisure travel is not dependent on-air travel only but also on train and road trips. Besides, wedding and gifting also remain strong demand drivers for luggage. Growth in backpacks (20%) of sales should revive once schools and colleges re-open. Handbags (8-10%) of sales should also come back once lock downs are lifted and people start get back to socialize.

Margin drivers

All the three large players traditionally have used India as a manufacturing base for hard luggage (VIP has 6 manufacturing facilities in India). Hard luggage manufacture is less labor intensive as the main case is plastic extruded. Soft luggage manufacturing is more labour intensive and there has always been a strong vendor base for this in China. Which is why all the Indian players (including unorganized) started importing soft luggage from China.

China imports are dollar linked and thus sharp INR depreciation can hurt gross margins. China being a sourcing hub for everyone globally meant that the vendors there have strong bargaining power even versus large players like VIP. There are duties on Chinese on imports too.

Starting 2014, VIP made a strategic move to reduce dependence on China for and start sourcing from Bangladesh and started setting up their own factories. Soft luggage manufacture is highly labor intensive (includes luggage, bagpacks and handbags) and thus more comparable to textile manufacturing which has moved from India to Bangladesh due to lower labor costs. Share of China sourcing has come down to 40% and will drop below 20% over the next two years. Competitors Safari and Samsonite still import most of their soft luggage from China and thus Bangladesh manufacturing will be a near term competitive advantage for VIP.

Higher share of Bangladesh imports should drive higher gross margins due to a) lower costs versus China and b) VIP captures the 20% manufacturing margin as well as opposed to paying it to the sub-contractor. FY20 saw a sharp 380bp gross margin improvement as share of Bangladesh in sourcing doubled from 15% to 30%. Expect more tailwinds ahead from this shift.

Even otherwise, the category has decent pricing power and gross margins for all the three players have moved up over the last three years. This has been partly due to premiumization and benign commodity costs.

Key risk factors

Threat from e-commerce and Amazon basics

E-commerce has not changed the pecking order for luggage brands globally as well as in India. In India, there were similar concerns when modern format came off age but there as well the existing brands continue to dominate. Big Bazaar had tried private label but failed despite cheaper pricing. When ordering luggage on-line, customers are more comfortable ordering brands they are familiar with than new brands. Luggage and backpacks also have a service element as most come with a 3-5-year warranty. Smaller players may be able to push their products online but do not have the offline service network. Xiaomi entered the luggage category couple of years back through the e-commerce route but has had limited impact.

Checks suggest that Amazon basics has not had any meaningful impact on the incumbents. Product pricing is on the lower side with lower warranty period suggesting mass segment positioning. Indian consumers seek value and look at lifecycle costs and thus prefer brands over private labels. E-commerce is about 10% of sales for the industry and the branded players are using it yet another way to reach customers.

Competition from Safari

There has been a concern that Safari is taking market share from VIP. Safari’s sales have grown 7x since Sudhir Jatia (former VIP MD) took over the company. VIP has certainly ceded some market share to Safari especially at the mass end where Safari operates. However, given Safari’s mass positioning, very high discounting, high dealer margins and higher credit days, bulk of its share gains have come likely come from the unorganized sector.

Channel checks suggest limited impact to VIP’s mainstream brands – VIP and Skybags as they have much superior positioning and operate in the higher priced segments. Safari has also been very aggressive in the CSD channel due to Jatia’s strong relationships there which he took along when he left VIP. Institutional and CSD segments would contribute 40-45% of sales for Safari versus about 25% for VIP.

Unlike VIP or Samsonite which have multiple brands for different segments, Safari has just one partially established brand right now which presents a scalability challenge for them beyond a point. I don’t see a major risk to VIP until Safari does a successful launch in its core economy segment. Finally, despite Safari’s high growth, industry remains a three player one. VIP’s last five-year sales CAGR is 10%, ahead of Samsonite’s 7% but lower than Safari’s 25%. VIP has maintained its gross profit pool share over the last five years.

18 Likes

VIP management change Anindya Dutta joined as new MD in place of Sudip Ghose from 1st Feb 2021.

From update PDF:

Anindya brings more than 20 years of leadership experience in the FMCG industry across business verticals and categories. Prior to joining VIP Industries, he was the Managing Director of Havmor Ice Creams Pvt Ltd (a Lotte Group company). Being the first MD after its acquisition by the Korean conglomerate, he was not only instrumental in scaling up the business to a national brand but also brought about an organizational transformation towards a professional and streamlined business operations poised for fast paced profitable growth.

Prior to Havmor, he was with Britannia Industries for almost 18 years, in roles of increasing impact in Sales & Distribution, Category & Brand lifecycle management, Channel development, Supply chain operations and leading P&Ls like Britannia’s Dairy, Breads and International Business SBUs.

In leading VIP Industries, Anindya will be responsible for managing all the business verticals and its operations. He will work alongside Dilip Piramal and Radhika Piramal to drive strategic business growth and efficiencies. The Company expects to reinforce its leadership in the industry by expanding its consumer franchise and strengthening the consumer trust it enjoys.

5 Likes

Thanks for your detailed Analysis. When we look into Share holding Pattern, it seems like FIIs are more interested with Safari than VIP IND. But Safari is gaining the market share by compromising their margin. So, I think its better to be with leader in current situation.

1 Like

Vip industries

Key conference call takeaways

i) On the sourcing front, Bangladesh continues to gain higher significance for the company. It has shifted majority of products sourced from China to sourcing from its Bangladesh facility,

ii) the company has shut around 100 EBOs in FY21 and is expected to mostly continue with remaining EBOs,

iii) VIP has again initiated talks with landlords for rent waiver for the lockdown duration during Q1FY22. The talks have been conducive with positive response from landlords,

iv) the management indicated that it was well prepared to meet any pent up demand while its own manufacturing capabilities will provide it sufficient headroom as and when demand picks up,

v) VIP’s revenue share from e-commerce has gone up to 17% in FY21. Catering to e-commerce, the company has been able to cover gaps in its product portfolio,

vi) VIP has lost market share in FY21 and regaining market share is its main agenda as and when the demand situation normalises,

vii) on the geographical demand trend, the management indicated that tier II, III cities have recovered faster than metros and major cities.

10 Likes

Good performance by VIP in the Q2 with revenue reaching to 80% of pre-covid level along with decent EBITDA margin despite raw material cost headwinds and supply chain disruptions

Demand is more in hard luggage segment (47% of sales for VIP now) and VIP has already reached to 100% capacity utilization. They need to undertake capex across the plants to cater to this market shift.

VIP had invested in Bangladesh plant for soft luggage to take advantage of low labour cost. In-house manufacturing has cost advantage (to be achieved through planned capex) but geographical cost advantage vis-a-vis competition will be a monitorable now.

Stronger & premium brand range and distribution network would continue to work in VIP’s favour in terms of better market share and profitability.

Investor PPT

02e29dee-deae-4ae4-986e-63d9328c3620.pdf (1.9 MB)

1 Like