This has been in my radar for awhile and the valuations were a big barrier earlier. With the current valuation, this is worth a look.

VIP as a brand has been around for a long, long time. Caprese and Carlton seem to be carving a presence and could take away market share from unorganised players and Samsonite respectively. Aristocrat as well has been doing reasonably well lately. Skybags is pretty much omnipresent these days. So as a branded play, this company is investing in branding and it seems to be paying off. The segments and branding as well is well-thought out so there is no overlap and targeting as well is on point.

Debt reduction - Consistently reduced debt from 107 Cr in FY11 to zero in FY17.

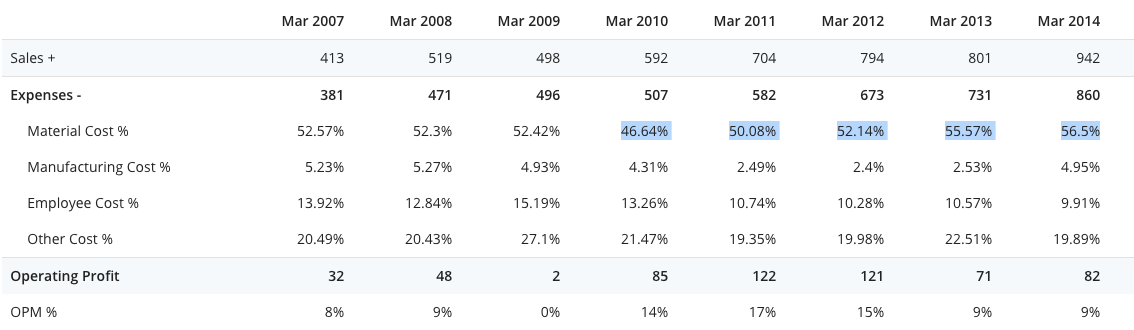

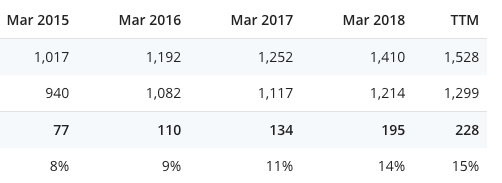

Sales growth - Topline has grown every year in the last 10

Profit growth - This however doesn’t reflect in the bottomline which has been erratic at least till FY14

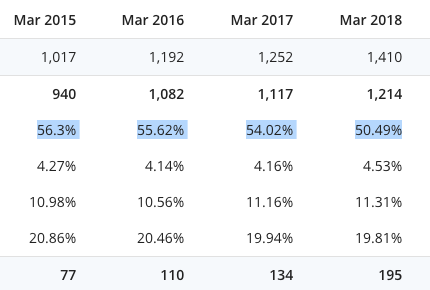

This is primarily due to the company not being able to pass on the RM cost increases to its customers. The material cost increases mirrors the drop in OPM.

However, things are different from FY15 onward. Notice the steady increase in Operating profit along with the topline and also the steady increase in OPM from 8 to the current 15%. The company was either able to pass on RM costs increases to its customers or RM costs went down during this period (Need to verify which happened).

Either way, good things seem to be happening and it reflects in the RoE too with the company improving its RoE in the last 4 years and is operating almost close to 30% at present.

Most recent quarter was particularly stellar and got a lot of attention because the topline grew almost 30% and bottomline almost 50% and OPM shot up to an all-time high of 19%. Will be interesting to see if they are able to maintain those metrics in the coming quarters.

Risks:

- Rupee depreciation could affect margins

- Customs duty increase from 10 to 15% on suitcases/bags might affect margins

- Inability to pass on RM cost increases like what happened between FY10-FY14

- The contingent liabilities of 148 Cr needs to be watched

A good brand should be able to pass on RM costs increases so all the risks shouldn’t matter if the company’s brand image is strong enough. We have to wait and see.

Valuation

With RoE close to 30% and growing between 20-30% with zero debt, 30 P/E is not unreasonable. I think they could do 200 Cr PAT for FY19 which makes current price a reasonable value.

Disc: Been buying around 400 levels which I consider fair value