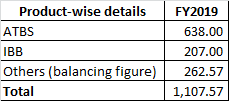

In the Annual Report for FY19, company said it was “aiming for doubling of revenues over the next 3 years”. At that time, the revenue break-up was broadly as follows:

But now, Ms. Vinati says the doubling will be in 3 to 4 years. Taking a liberal view, let us see if the company can add another Rs.1,100 crores by FY23 at least:

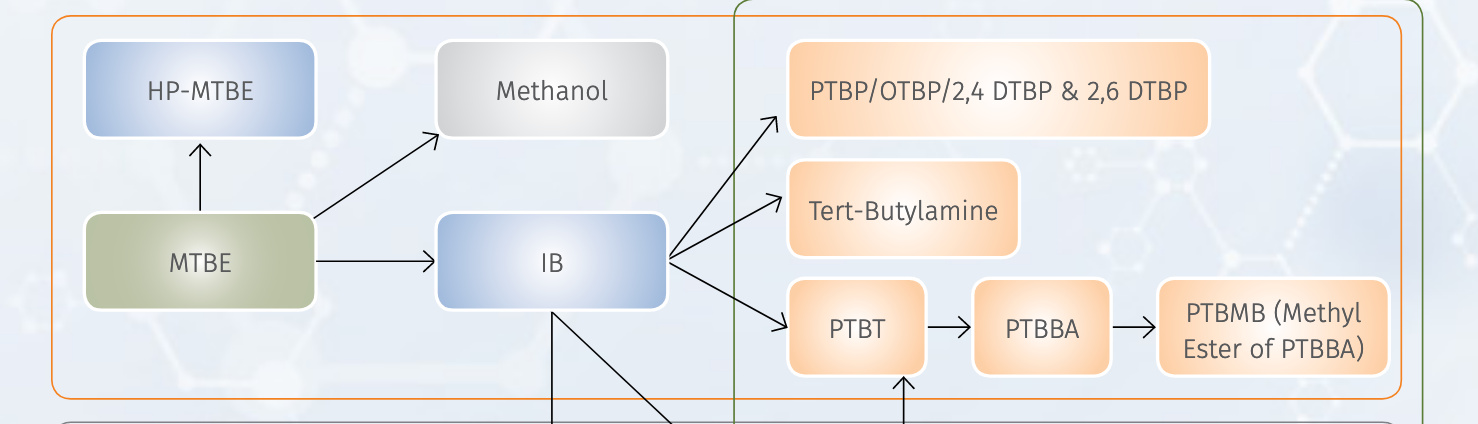

Butylphenols

As per management’s guidance, Butlyphenols will add Rs.400-450 crores of revenues per year at full capacity. Let us assume an optimistic Rs.450 crores from this in FY23.

ATBS

Last year, ATBS brought in Rs.638 crore. These prices were at peak, brought about by temporary demand supply mismatch. The mismatch is now gone and prices are coming down. It is difficult to say how much prices will correct, but as per one report ATBS prices were Rs.150 per kg in FY17 and Rs.258 per kg in FY19. Assuming prices correct back to the same level by FY23 (40% decline is not unusual in commodity markets) and the company manages to sell its entire capacity of 40,000 MTPA (50% increase from current level), still the total revenues from ATBS will increase only marginally. When the management says ATBS will grow at 10-15% per year, I assume it is the volumes and not the revenues. Even granting a liberal 5 % p.a. growth in revenues per year from the peak pricing of FY19, ATBS will add at most around Rs.140 crore to the revenues in FY23.

IBB

IBB earned Rs.207 crores in FY19 and management says it will grow at 10-15% per year. Once again taking an optimistic assumption of 15%, IBB will add another Rs.150 crore of revenues in FY23.

In other words, even after taking optimistic scenarios of Butylphenols, ATBS & IBB and giving the company 4 years instead of 3 to double revenues, we get incremental revenues of Rs.740 crores in FY23. That still leaves a hole of another Rs.300 crores to be filled up from other products – which collectively gave just Rs.262 crores in FY19.

This doesn’t seem possible unless the company has another new big scorer up its sleeve. That may be the case, since one would normally not expect the management to make such a forecast without having something specific in mind. However, I cannot say that is the case here, since the management has several times in the past said one thing and changed the goalposts later.

What is certain is that near term outlook is bleak, with ATBS prices correcting and Butylphenol capacities delayed.

(Disc: Invested, booked partial profits recently)