unfortunately it seems like that this report is only accessible by top equity fund managers etc.This is a 154 page report with the detailed analysis of all the market variables of this industry and in depth analysis of all the players involved in the game, could be a goldmine of knowledge. Thanks for bringing it up, trying to check if anybody I am aware of has access to it or not, though seems highly unlikely.

While trying to get a hang on the current status of lead ban in PVC pipe manufacturing, i happened to find this notification. This, to me, sounds like a final notification that’s been given to the PVC pipe manufacturers!

Whats interesting (if i have interpreted it right) in the notification issued by MoEF (Ministry of Environment, Forests and Climate Change) is the clarity associated with their guidelines; Clarity on timelines of implementation, clarity on the phased manner in which product categories have to comply with these regulations.

-

The said draft rules shall be taken into consideration by the Central Government after the expiry of a period of sixty days from the date on which copies of the Gazette containing this notification are made available to the public

-

Any person or organisation desirous of making any suggestion or objection in respect of the proposed draft rules may forward the same in writing by mail for consideration of the Central Government within this period

Broadly there are 3 categories of PVC pipe manufacturers, as listed by the regulator:

-

Category A: Use of PVC pipes and fittings for potable water supply

-

Category B: Use of PVC Pipes and Fittings in Agriculture and in Suction and Delivery Lines of Agricultural Pumps and Rain Water Systems

-

Category C: Use of PVC Pipes and Fittings for Drainage and Sewerage System

The manufacturers of products, in each of these categories, have been given a specific time period within which time they need to comply with the notification. While manufacturers in Category A need to ban the usage of lead within an year from the date of teh rules being published, those in Category C have been given a time period of 4 years.

Based on my limited understanding, a majority of PVC pipe applications fall under Category A, which would mean that a large part of the PVC pipe manufacturers would be compelled to use other stabilisers (Tin or Zinc) to fall in line with the rules.

Vikas Ecotech could be one of the major beneficiaries, if the implementation is done in accordance with the rules as they only manufacturers of the globally- acclaimed tin based additive, Organotin. Its important to note that they also possess capabilities to manufacture Zinc based additives, enabling them to capitalise on on any opportunities that may open up with this ban.

padi, lets not carry away with narrative of they are the only manufacturers, monopoly etc remarks. They are not. I saw a lot of such narrative recently, so thought i will do some research. I am sharing what i found. This might help few investors.

First, lets collect some data which will help us with reasoning.

- Is VEL only company manufacturing organotin?

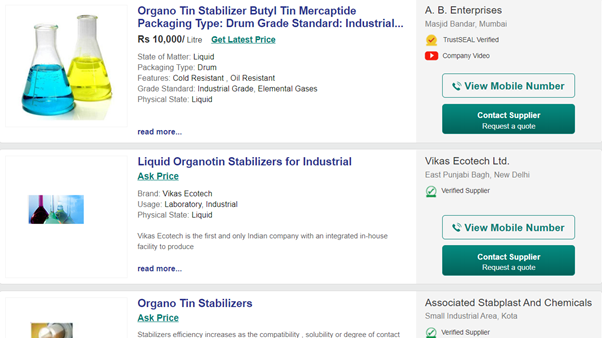

I did a quick search on indiamart for organotin and found apart from VEL, there are other selling this compound.

How others are selling then, if VEL is the only one manufacturing and selling as their brand?

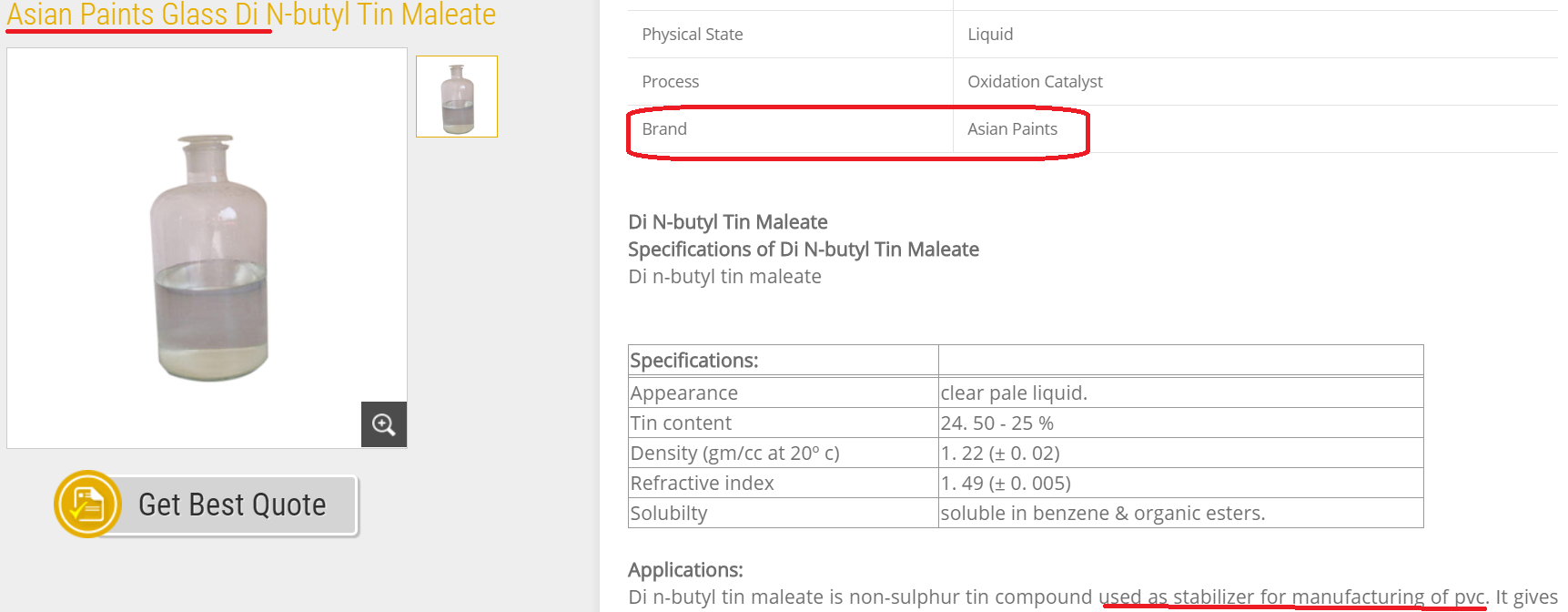

Well, if you look at A.B Enterprices, they sell from Brand Asian Paint as below!!

Clearly, VEL is not the only one manufacturing and selling it. As claimed by VEL in their add, they are the FIRST to manufacture in India, not the only ones as below -

Now, lets see if there is any truth in saying if they have any advantage after BAN of existing legacy stabilizers.

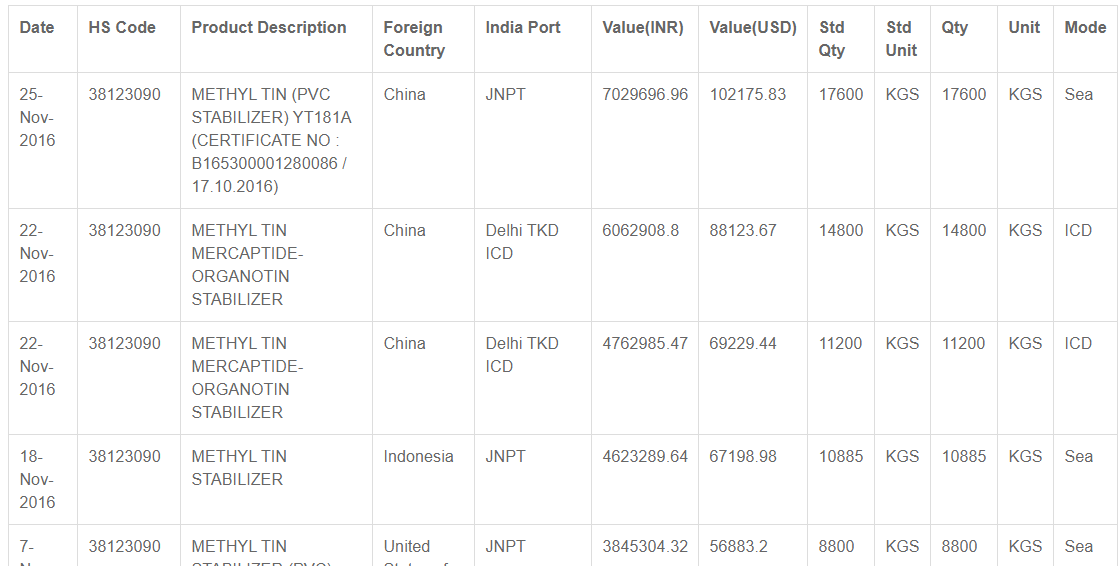

Some import data of organotin during 2016. This is old data, but gives some hint nevertheless.

As you can see, this compound comes from China, US and even Indonesia into India! I assume the same for 2019 as well as nothing changed during this time.

Lets check the biggest manufacturers of this worldwide -

They are

- China

- US - Galata Chemicals

- Indonesia - around 25%

So, if the BAN by India is implemented, I do not see any reason business will shift to VEL. Companies here just import more from these countries as they are doing now than buy from VEL! After all, they are currently importing for a reason than buying from VEL.

As we are at it, lets also check the effect of Trump’s tariff on Chemicals from China. As per below report, organotin is placed under 10% tariff which is NOT significant and one of the biggest manufacturer of Organotin in US, Galata chemicals, is facing loss because of this. Read below.

Also, because of this 10% tariff, China will have more supply and will sell it cheaply to India, which is an attractive market.

So, in a nutshell, VEL has to beat China,US and Indonesia in price to take advantage of the ban which i am pretty sure this company can’t do. This can be very well seen by their trade receivable(2 times of their TOTAL REVENUE of Q2 which is 84).

This company simply doesnt have pricing power. I don’t see any benefit if this company ties up with Yuan to sell in US market. There is already enough supply. Unless India completely bans import of this chemical, nothing is going to happen to this company. Even if India does that, there are other biggies to capture the market.

7 Likes

Appreciate the divergent views you are bringing to the forum. Thanks.

I shall let you know what i have learnt about this subject, so far, and let someone with better knowledge on the subject/company take it further.

I would like to rephrase what i meant: (1) VEL is the only manufacturer in India, who manufactures Organotin MTM from the basic RM (Tin) stage. (2) There are a few (like Shital Inds etc) who also manufacture Organotin MTM in India, but they do it from the n-1 stage i.e. they import the intermediate from China and then do value add and sell (3) Organotin MTM consumption (to the best of my knowledge) in India was close to 6000 MT anyways, and was being fed thru imports from China as well. So not that it was a under served market

Organotin is a stabiliser manufactured using Tin metal as the RM. Organotin is manufactured in 3 diff forms, MTM (Methyl Tin Mercaptide), BTM (Butyl Tin Mercaptide) and OTM (Octyl Tin Mercaptide); of which MTM is more preferred and used, over the other compounds, globally on account of its strength and properties.

Besides, should India go ahead and ban lead stabilisers completely (as is what it looks like), the demand can technically shift to alternative (non carcinogenic) metals like Zinc also. Calcium Zinc is also widely used in European countries which have banned Lead. VEL also has the technology and capacity to manufacture CaZn (Calcium Zinc) stabilisers (thats what i think i had read sometime last). That said, Tin stabilisers have much better strength and properties even over Zinc, the only drawback being its more pricier over Zinc and hence the immediate demand could shift towards Zinc.

I have not made any claim of VEL being the ONLY beneficiary. If you read what i have written, i have said it ‘could’ be one of the major beneficiaries. (‘could’, grammatically, is used to indicate possibility and does NOT indicate confirmation of anything) ![]() Also, as i have mentioned earlier, Organotin is not new to India and was being imported even earlier. As to why most of the local demand was satiated via imports needs to be looked deeper into, to get a balanced view?

Also, as i have mentioned earlier, Organotin is not new to India and was being imported even earlier. As to why most of the local demand was satiated via imports needs to be looked deeper into, to get a balanced view?

How and what impact will the raise in tariffs eventually have is open to interpretation, isnt it? That said, i go by the recent distribution agreement signed by VEL with Yuntinic Resources to decipher what this could mean for Chinese and Indian companies. Yuntinic is a 100% sub of Yunan Tin, the largest tin manufacturer in the world, has agreement with VEL to manufacture Organotin MTM in India and supply to Yuntinic clients’ in the US. Why would they choose to do so? Besides, from what i also get to understand, stabilisers sold in the US need a certification of NO RM purchase from China. VEL procures tin metal from Indonesia and 2EHTG from Germany and hence has the certificate.

Imports from China (including import duties of 7.5%) works out to $7.7/kg to an end consumer in India. On the other hand, VEL sells at $8.2/kg to an end consumer and $7.5/kg to traders. Yuntinic’s tie up also enables VEL to reduce production cost thru process improvement and more efficient purchase pricing of the RM, possibly making it more competitive going forward.

Needless to mention, this DEFINITELY is an issue, precisely coz of which the stock doesn’t find a favor amongst investors today. The ‘Lead ban benefitting VEL’ narrative getting super prolonged (more than 2 years as i recollect), corporate governance issues, receivable issues not getting sorted etc are overhangs, undoubtedly. May be thats why the stock is trading where it is, who knows?

I apologise for my lengthy reply, was trying to clarify several points you had made in your note. I am NOT recommending any buy or sell

Disclosure: Have very small tracking positions in the stock and have been keeping a track on this name for the last 3 years now.

1 Like

Has anyone been tracking Vikas Multicorp? the company which was spun off from Vikas Ecotech, and listed separately. Ive been trying to understand the company better and would appreciate some help.

After listing at ~Rs. 5 last May, the stock collapsed to ~Rs.1 in April 1st week this year. In my opinion, this capitulation is a result of holders wanting to exit at whatever cost possible. From that low, the stock has gained to Rs.2.30 in about a months time. What’s interesting to note is that this price gain comes on the back of much lesser volumes (consolidation of shareholding in the fall?) and a slew of recent announcements made by the company last weekend (attached herewith):

Vikas Multicorp - Board meet announcements

What caught my attention from these announcements were:

-

Acquisition of a leading EPR company, with MNC clients, which is synergistic to VMLs existing business

-

Company intending to make Rs.25 crs of investment into profitable speciality businesses

-

Consolidation of capital ie increase FV from Rs. 1 to Rs. 5

While the increase in FII holding limits, also announced, is immaterial (given the market cap of the stock), the above developments look interesting. Backed by my observation of consolidation of shareholding (as explained above, weak hands getting out), do these announcements mean anything significant to any of you going forward?

I would appreciate some views on this please. Thanks.

Greetings to everyone. This being my first post here, was a passive reader until now.

Writing my views here. The stock Vikas Ecotech has been under continuous UC’s &LC’s since March 2020. The company has been posting losses lately after the Demerger. I found a few anomalies in the AR (Annual Report) 2017-18 & 2018-19.

-

Change of course mid-way. Dahej plant was announced in 2016, to produce 2-EHTG, a key raw material in the manufacturing of Organotins – a lead free and non-toxic PVC heat stabilizer. In the AR 2017-18, it shows an entry in the Capital commitment for purchasing the property for 1,15 Cr at Dahej, Gujrat. In the AR 2018-19, it shows [Industrial Property at Dahej –II, Industrial Estate, Dist. Bharuch Gujarat owned by Company. The Property has been disposed off on 29.05.2018 of Rs. 4,26,50,827 INR and entire proceeds kept by Bank as Colleteral vide FDR No. ‘00073021044520 Dt. 29.05.2018 of Rs. 65,00,000.00 & ‘00073021044490 Dt. 29.05.2018 of Rs. 3,61,50,827.00 with Oriental Bank of Commerce.] No further details are available.

Another property to be purchased at New Rohtak Road, Delhi mentioned in AR 2017-18 at a contract price of 16.80 Cr, with 13.42 cr payment already made. Same property at New Rohtak Road, Delhi mentioned in AR 2018-19 for the price of 18.25 Cr with 17.94 Cr payment made. What I know of, if a contract price is set, the seller has to honour the agreement. This cannot be changed midway & can be challenged in the court. Both of these are mentioned under Point 36. Capital Commitment in the Annual Reports. How these costs are mentioned in the latest Annual Report remains to be seen. -

Though, this may not be anything or maybe something. The Donation amount decreased substantially from 79.23 Lacs in 2017-18 (Demerged) to 7.36 Lacs (Demerged) in 2018-19. The amount of donation was exceptionally high before the Demerger. Noteworthy, the company is not debtfree & pays rent for its premises. One of the recipient of the Rent is the wife of the Director.

Disc: Invested since 2016, reduced the Investments after perceived promoter integrity issues.

1 Like

VEL business update uploaded on the exchange today. This is what they are essentially saying.

- VEL’s Organotin exports of Organotin PVC stabilizers to the USA (worlds largest Organotin maiket) continues unabated.

- VEL has tied-up with one of the largest speciality chemical Organotin stabilizer distributors in the USA, having a well-established country wide distribution network.

- The US company has continued ptacing its orders as per their earlier agreement for 2020, and is eyeing a long-term association. Globally, Organotin is a $ 1bn market on an annual basis.

- Domestic demand trajectory looks strong, post NGT ban on lead.

- VEL recently got an order from HIL Limited (a CK Birla Group Co.), resuming business post covid-19 lockdown.

- VEL expects a sharp jump in domestic demand, post lockdown. Stock inventory depletion during the lockdown implies replenishment of stocks in the supply chain.

Disclosure: have maintained small tracking positions for over 3 years now.

VEL - Business Update.pdf (431.3 KB)

VML announces entry into ‘Food protection and Personal Hygiene’ segment of FMCG Industry, by signing a definite agreement for acquisition of a portfolio of trademarks, comprising of popular and well established national brands like:

- ‘Homefoil’ and ‘Chapati Wrap’ (aluminium foils and sheets in food protection segment)

- ‘Cleanwrap’ (cling films in food protection segment) &

- ‘Mistique’ (tissue products in personal hygiene segment).

VML is initiating the process to identify and acquire an existing plant for manufacturing these items and has laid out plans to invest ~Rs. 100 Crores over 2 years.

In the interim, alternate arrangements are being made to produce these products through 3rd party contract manufacturing.

Market share of acquired portfolio:

- Aluminium Foil market size (domestic) is ~200,000 MTPA (~Rs. 7000 crs), in which VMLs acquired brands have market share of about ~6%.

- Tissue paper market (domestic) is ~Rs. 5,000 crs, of which the branded tissues market is ~Rs. 2000 crs.

- VMLs acquired brand (Mistique) has ~10% market share in the branded tissues category.

VML claims these brands to have a presence at more than 10 Lac retail counters across the country, besides being sold to prestigious domestic institutional customers like: Most large 5 Star hotels, prominent hospitals, prominent airlines, Canteen Stores Department (CsD), Railways and Airport Authority of India to name a few. Internationally, they claim to have a well-established presence in UK, Europe and ME.

PR attached herewith.

Disclosure: have maintained small tracking positions, courtesy owning VEL (from which it was spun off and listed separately) for over 3 years now.

VML - Brand aquisition.pdf (842.6 KB)

I had invested around 40 during the period 2018, (PS : was a novice to stock market) all went good till when the company planned to declare bonus.

The company had a split into 2 sectors : Vikas Ecotech & Vikas Multicorp the price being paid to shareholders were about 2-3 rupees in both sectors…

This was a lesson learnt for me

I invested in this company around 18-20 price … it went to 40+ during the bull run in 2018. My mistake was not to book profit during that time. I sold all my holdings this yr for around 50% loss.

I had high hopes for the company. Learned my lesson to ignore the news flow and decide based on company performance.

I invested in this company in 2017 or 2018 for around 13 rs and I sold for 150% profit later…the reason I sold, this company was only talking and no actions, extremely high receivables, fire in factory, announcement on LATAM contract but no news after that for long time, demerger announcement as if any achieved something already, like this few more points, worst WC…so sold…

Lot of lessons learnt through this stock

Vikas Ecotech has come out with RE (Rights Entitlement). I already own 50K Qty of Vikas Ecotech and now my Demat is showing a 65K Qty for RE. I am not sure what to do with RE (65K) appearing in my demat.

-

Should I sell the RE and pocket whatever money comes to me? (This company is a dicey one, promoters keep coming up with one gimmick or the other. The only reason I am holding the 50K qty is to sell when my price comes and get out).

-

Should I be paying extra money to turn RE into normal trading share when the window ends around 29/June?

Looking for some feedback.

Thanks

It appears that management does not have any intention to recover the bad debts . On the contrary it may be their plan to give funds to known people and draw money from them in own names. Fearing this may be the gameplan i have sold the right issue on the exchange . Also sold the original shares thereby booking a loss.

Results seems excellent. Any input from any boarders here:

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=784063c5-feed-4551-8754-fb27c3970c35

Is anyone still following this company?

To me it does look a complete turnaround story and stock about to get further re-rated considering all the news and updates flowing in. Be it orders received from OEM’s like Olectra Greentech, Debt Reduction, Expansion Work In Progress, Promoters Buying from Open Market, and now the update as per the attachment which shows orders received from OEM’s like Zara & Clarks.

Disl. Invested heavily from bottom levels.

I have been following it and also trying to add from lower levels. But I don’t trust them very much. They keep throwing such media releases from last 1 year be it debt reductions, new business, order wins etc. etc. Really need to see next 4-6 qrts performance to be convinced.

Thanks

1 Like

Comany seems to be committed to be debt-free by 2023.

55% debt reduction completed till date though is on the base of further increasing the share capital.

1 Like

Nowadays(September-2023) there are news about FII buying into Vikas Ecotech through QIP…but the news articles have limitation…it only talks upto 52 week rather than the whole picture from history.

To me these news articles seem to be just a recycled PR show/ Advertisements, Since the managements doesnt evoke trust.

Disc - Not invested.

1 Like