We still need to be very cautious as VEL is in a tight spot for corporate governance and ethics standards.

updating this thread!

-

Company informed about going for backward integration, setting up of 2-EHTG plant, which would basically produce a key raw material required in the production of organotin, currently they import it from China. They will use 80% of the produce from this plant for in-house activities, rest will be sold in open markets. 30-35 crores will be the cost to set it up on a bot basis. Estimated timeline is 1 Year. So basically another dent in the capex.

-

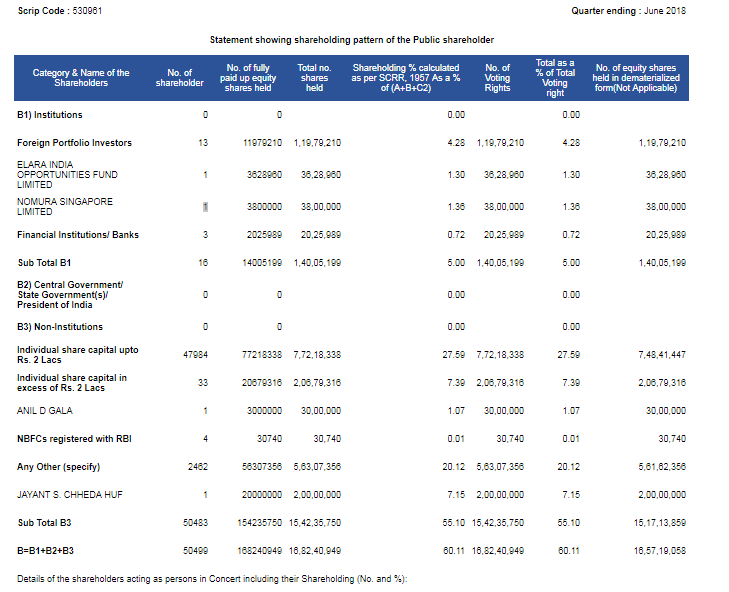

Company released their latest shareholding pattern

I can see few FPI’s making entry into the stock which were not there earlier like Nomura. Promoters also seemed to have done some buying but it’s almost negligible anyway. -

Company has announced that they will be releasing the results of qtr ending June on 19th July.

Can anyone update on the cause of DRI raid ?

Also do we have a fix on the manufacturing assets and value additions from these assets.

The company had very large receivables indicating that it was fudging turnover by either transferring products to its distributors on credit with title recovery or was fudging the turnover .

I am unable to analyse the cash flow. Could someone knowledgeable please analyse the same to see the divergence with sales

It is important that any investor in this company analyses these and other parameters

i spoke to one of the players of PVC stabilizers in India( unlisted). did not receive good reviews about the company and the industry. 95 % of the market in India is of lead stabilizers . This will slowly get phased out , and open up an opportunity for Ca/Zn stabilizers. He said that tin stabilizers has no scope or future. Tin is also a heavy metal just like lead , and the move from lead to tin is highly unlikely. Most of the world - europe , japan , australia ,etc. are moving from lead to Ca/Zn. There are no significant advantages of Tin over lead. We have tin prevalent greatly in North America , that too because lead never entered those markets. I spoke to another unlisted player who feels even America will make the move from tin to Ca/Zn. Also note that moving from lead to Ca/Zn is not very easy as lot of investments have to be made in technology. The stabilizer industry may hence see a lot of consolidation in the future.

Coming to Vikas Ecotech , i am warned to be careful about the promoter .Also to note that the promoter has earlier been a stock broker and a market player. He says the AR will mention XXX crores of sales and talk about selling a lot of tin stabilizers, but not give you the exact amount of tin stabilizer sold , or the revenue from that division.

i also made an observation that the statutory auditors have the same address as the registered office address of the company. Promters hve sold more than 6 percent of their holdings in the last year.

Scuttlebutt method has helped me here big time, to stay away from such companies.

Disc- Not invested

12 Likes

Thanks Shikhar for the informative post and scuttlebutt . Strengthens lot of the arguments some of members have made on this company in this thread based on data available in financials and annual reports . One of the suppliers n shareholders on which lot of hope was made was prince pipes and seems they are also coming with an IPO. I think considering this related history, evaluating prince pipe would also require an extra bit of caution.

3 Likes

Nice observations. I did not know this as a ex share holder of this company. Looks like i had to do put more effort in research!

I had obtained this number in from company last Oct. They also said they are ready to share this info in their conf call.

VEL - Data.xlsx (40.7 KB)

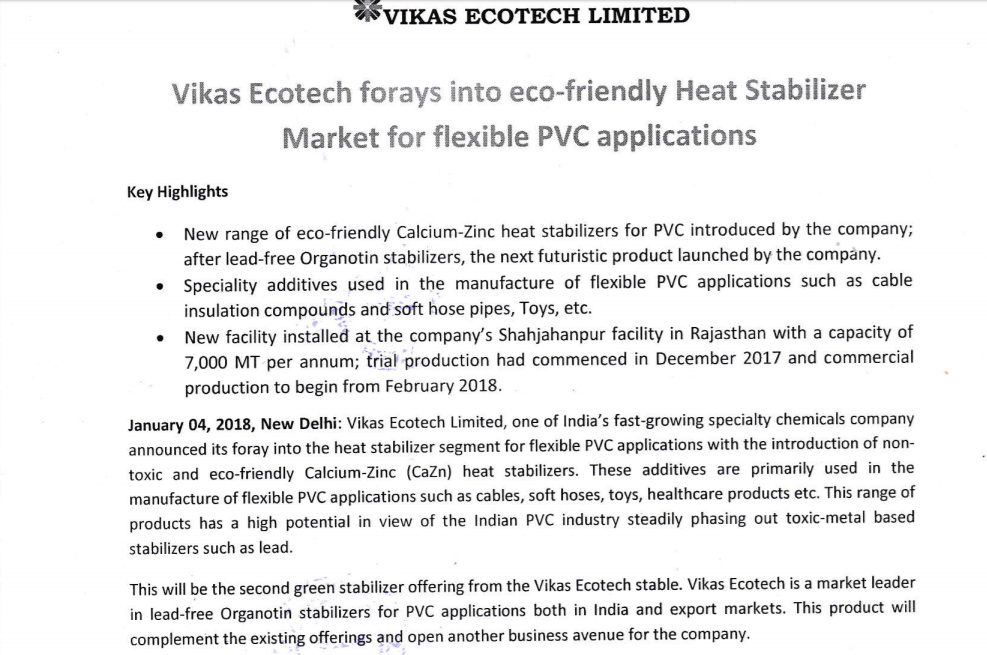

They have announced Ca/Zn based product in Jan 18.

But i doubt this has FDA approved as with their other tin product. But overall, i agree with you that the promoter is not well intention-ed and there are too many red flags with regard to this company. I was fortunate to exit with very minimal loss.

Disc: No holding now and only tracking this company to learn.

2 Likes

I’d like you to pls verify whatever you hear from A B C D with actual facts before putting forward that to a wider audience, otherwise this forum would too become like mmb board. Half of things you claimed were wrong coz you did not verify them. however, things like auditors having the same address is completely true. I’d request you to first verify the information and then post it. Quantity and segmented revenue figures are all present, the number itself being fake is something different altogether but your source lost credibility as soon as they mentioned something which was not true and could have been easily verified. Otherwise this would become a gossip mongering forum, hence pls verify things before you post.

2 Likes

Ya maybe the company not giving sales break up was wrong …but i was not able to find a source where they give this break up…except that everything was correct…perhaps u should read the post again instead of just writing nonsense…i have mentioned clearly that these were the insights received by someone from the same industry. Also u seem to be having some other reasons for such a bitter reaction. Perhaps if u could start with disclosing your position in the stock that could help.

Disc -not invested

i did not have a bitter reaction. i just said that we should also verify things before posting. for example, you mentioned about tin stabilizers being a complete waste, coz somebody told you so… it’d have been better if you had given some stats of the consumption of tin stabilizers currently to check and verify claims. My point is simple, many people said many things but they presented some sort of proofs for it and numbers… not like a gossip mongering thing, coz for that, mmb board is always there. So tin stabilizers are a complete waste as i understand, so are they not being used currently? if they are, why are they being used if they are similar to lead based stabilizer and also cost more than that? that would be an immediate question that would come to anybody’s mind right. I ain’t talking about indian market, but globally.

disc : was invested, made exits, got to book profits as i was invested from lower prices, still holding positions for tracking purpose, may purchase again in future depending upon the situation and circumstances

2 Likes

it appears we have limited qualitative or quantitative research so far.it is however clear that the Promoter appears to have serious credibilty issues. Opaque data seems to also be an issue.

Nomura only bought 35 lacs what about the rest???

1 Like

June 2018 Nomura held 38 lac shares

Sep 2018 Nomura held 30.56 lac shares

1 Like

Don’t know, this is all the information I have.

Got that data from trendlyne…yesterday after your post

Vikas Ecotech’s promoter sells over 1cr share; eyes inorganic ‘vikas’

Vikas Garg has sold 1,13,79,144 equity shares at a price of Rs14.01 per share, amounting to Rs.15.94cr on November 16, 2018, to raise funds for an upcoming inorganic growth opportunity.

The funds raised will be utilized by the company in the form of a zero-interest, unsecured loan.

As per the company’s filing with the exchanges, VEL is currently exploring a strategic inorganic growth opportunity for the production of 2-EHTG as well as other asset purchases.

Not as straightforward as it appears. I somehow,cannot take this on face value, but cannot put my finger on it.

Disclosure - Invested .

1 Like

The company seems to have huge trade receivables in excess of 180 days of sale. this has been the pattern for a long time.

this usually raises of concern of bad debt as if credit to sales channel is so high there exists likelihood of bad debt. it is not possible for me to access the qualty of debt information and if the Auditor does not expose such concerns this could be a further time bomb waiting to take down the company.

lending by Garg as interest free loan maybe a way to transfer fund through credit to people of interest.this would balance the balance sheet and in future he can withdraw the money

the management do not create trust

1 Like

Me too sold my holding because of management. Management is talking but not doing anything. I also noticed that company talks of too many product innovation but none is going to add meaning full addition to their topline and bottomline. Recent non disclosure of raid by an govt agency added ghee in fire.

Disc: sold my holdings way back

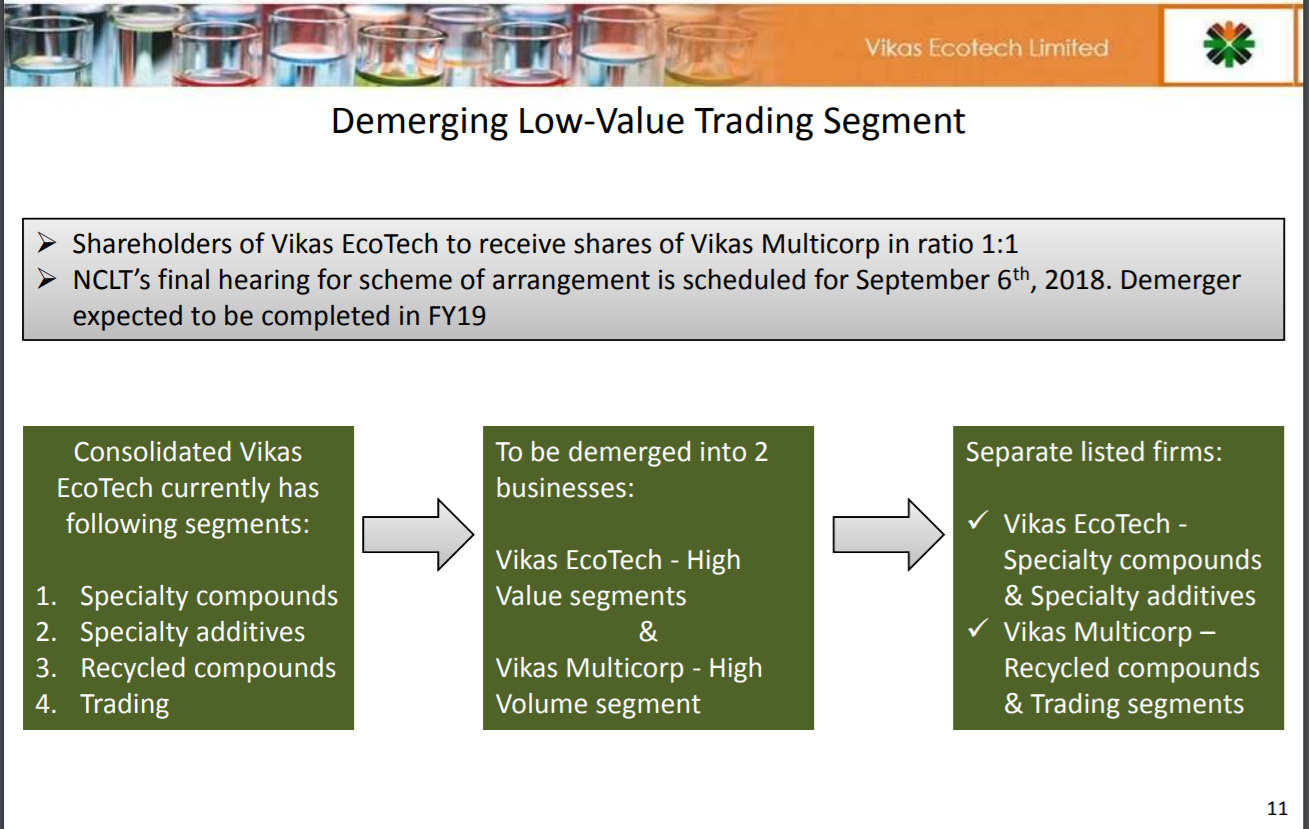

Update on Vikas Ecotech

Update on what has happened in the company so far:

De-merger of High Value and high volume business – High volume business of recycled compounds and the trading business have been shifted to a separate entity named Vikas Multicorp Ltd and will be listed soon. Vikas Ecotech Ltd retains the speciality compounds, speciality additives and the Organotin business which are high margin businesses.

Environment protection led ban in China on Chemical manufacturing companies led raw material disruption – 2-EHTG a key raw material for the production of Organotin has been banned in China due the government’s “Blue Skies” policy. This has led to an acute shortage globally and disruption in Organotin manufacturing for VEL. VEL however is looking at the following options to resolve this matter:

- Temporarily 2-EHTG is being imported from a German company

- Partner with the same German company to get the technical know-how for manufacturing 2-EHTG to India for royalty. They will do CAPEX to backwardly integrate Organotin manufacturing and also increase its current capacity for Organotin

OR

Partner with the same German company to get the technical know-how for manufacturing 2-EHTG to India for royalty. They will acquire a Delhi based company having production facilities ready in Daman.

Promoter sells stake:

16th November, 2018: Promoter sold 10% of his current stake (reduced stake from 40% to 36%) for 15Cr. A large chunk of that sale was bought by Nomura Singapore Fund. Rationale for the sale was given as money raised through the sale to be given to VEL as a zero-interest loan for its expansion purposes. On asked why dint the promoter rather pledge those shares, he said that the timeline for the acquisition/capex was too short to go through a bank. (Stake sale happened on 16th Nov 2018, and no further announcement with regards to the use of those funds has come). They showed their intent to buy stake again in the future if funds available.

6th December, 2018: Promoter sells yet another 3% stake in Open markets citing similar reason as mentioned above.

The promoter selling 7% stake, in-spite of the reason given, seems quite perplexing.