Bad results. Va tech Wabag has not been able to convert profit from its operations into free cash flow in the past decade. Also the management of receivables has been pretty average. Now it is barely making a profit when its peer Ion Exchange is posting good growth yoy and wastewater industry is seeing its best days in terms of number and size of contracts given out. Wastewater treatment surely is a promising industry but not sure whether VA tech Wabag is a promising story anymore.

I feel most of the problem is due to high receivable cycle which ideally used to be around 2-3 months but have now reached to 9-10 months cycle courtesy government projects. Need to see how soon that improves. Though its quoting 40% below my avg buy price, its an avoid for now. Holding on to original quantity with patience.

Does government decision to speed up payments to its vendors changes the outlook for the company given the amount of receivables pending from Government side?

I think it may change the situation and make it more favourable. But I have some doubts on that.

Many of its receivables are from the state government side eg. APGENCO. State governments seem to be more lousy is giving dues. Only central government being committed to paying on time won’t solve all of the company’s problems.

It’s share of contracts in India are going to increase in coming years as said by management in comparison to contracts outside India. I guess most of them will be from the government and that includes both centre as well as state governments. One time payment doesn’t mean that they will get their dues in future on time. Also, dealing with governments creates many more problems than just unrecovered dues.

We do not know whether this company will receive their outstanding dues. Government deals with thousands of entities across various verticals. I don’t know which entities will get paid first and when will they get paid, even if government walks the talk(there is a chance that they might not).

If the company can receive its payments on time and on a consistent basis, then I think that this company can be a great opportunity for wealth creation. Otherwise, even their current mammoth 10000 Cr order book might not generate wealth for shareholders.

I think that the problem is that this company is a B2G(Business to Government) business. If their order book had exposure with private businesses in India as well as abroad such that it was the majority of the order book, then it may generate some good cashflows. Otherwise, they will just need more debt for their working capital and expenses( due to lack of cash and piling receivables) while simultaneously losing the cash and profits they generate to interest payments of that debt while their money is stuck in receivables.( which is likely what happened in the last decade of their operations).

Probably cause of this article.

Since I am not a subscriber, I can’t read it. If anyone has subscription to BQ, then can you please state the important points stated in this article?

Thanks

The fall has been brutal. The stock is trading at 8-9 year lows!

There has to be something bigger than an article.

Anyone’s got any idea if they’ve received the pending payments from the government as last month FM had announced that pending payments from govt’s side would be cleared soon.

Problem is this APGENCO payment is due from Andhra pradesh govt and govt is changed so this may be biggest concern for them to collect this receivables.

Add to the receivables problem, I think some MF or institution decided to sell (probably lost patience of the under performance) and because of lack of liquidity and interest in small caps, the stock has taken a tumble. Traded volume at this point of time is merely 2L shares, which is like 3.5 Crs in value and the stock is down 7-8%.

Really unfortunate to be happening to this company. Management seems okay, so seems to be opportunity but because of govt. not resolving the payment, the investors and the company are getting thumped.

read and give your insight. though i cant find any. and in anycase i know these quint are no less than punters / operators.

i have total trust on their bad intention

Thanks for sharing.

I can’t find any new insight from this article. All the information written here can easily be deduced by reading the annual reports, financial statements and credit rating reports.

Nothing concrete happened last week as no new information came out in public domain which could attribute the drastic fall in share price. If not for the article, one other thing possible here is a case of possible bad corporate governance by the promoters in which market knows before the retail investors.

Does anyone have any idea whether the management is clean or not? Or any cases of bad corporate governance in the past?

The Moneylife aticle has been an eye opener. I would highly recommend everyone to subscribe to Moneylife for their articles.

Here are some points from the article, based on my understanding:

Negative cashflow in four out of the past eight years.

High trade receivables

High trade payables

Unable to convert profits into cash

High receivable days, significant portion of receivables is non-current (greatr than 12 months)

Dues from a project in consortium with a bankrupt company

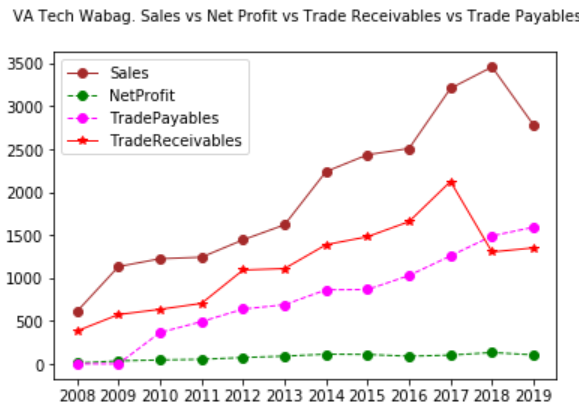

Here is a chart of the sales, profit, payables and receivables: Source: Screener.

We can see that although the sales are increasing, receivables are also growing with it. All along, the reported net profit has not grown much (it is small compated to the sales).

I haven’t read the MoneyLife article. But suffice it to say that the Receivables problem has been evident since a long time now.

While competitors like Thermax and Ion Exchange have had Cash Conversion Cycle in the 25-30 range, VA Tech Wabag has had it in the 50-60s range for several years. Put that next to their strategy of going after large government projects and you will have a recipe for disaster.

In fact, I’m surprised the company was able to do business for the past 2-3 years. The continuous increase in Debt has also helped mask the struggle of not having enough cash.

In the latest concall of Ion Exchange, I happened to ask the management “There are lots of upcoming government projects. If we tender for them, will our Margins and Receivables go for a toss?” The answer they gave was that they will never participate in a tender that does not give them control over Margins and Receivables. We have yet to see if they will live up to that. But perhaps Va Tech should take a page out of Ion’s playbook and stick only to projects that offer them ample breathing space.

The credit loss of Rs 161 cr that is directly passed through the BS, would not have created a loss if passed through P&L. The revenues and expenses would increase by an equal amount. Hence it does not matter

Rs. 1191 cr of “Dues from customers” includes the likes of APGENCO and other unbilled revenue and hence has been divided in the BS. This value would be much lower without the temporary issues

Payable days have always been high for VA tech. This does not mean that only contractors that are desperate for work will be willing to do their work. On the contrary. It means that contractors will work with them happily by pricing in their late receivables

Ratio of increase in retention money held back by customers cannot simply be judged by the ratio of increase in sales. The number of projects executed in the last two financial years have been significantly higher which would inflate the retention money temporarily

CFO has almost been flat (excl APGENCO) while cumulative PAT has been +ve. It is commendable to see that, given the nature of the business, VA has barely increased debt or equity to fend for their working capital requirement. Current debt is only because of APGENCO

Using the words that the prof used for another company, this company would drown in cash when it stops to catch a breath.

Disc: I am most definitely biased since I own this stock

I am invested from 300 levels and have begun to lose patience now. I could see that they had a receivables issue but kept hoping that APGENCO payment will work out. In the meanwhile the stock has tumbled to multi-year lows. I guess the lesson is to not invest in companies that depend on the government to make their money.

What are the odds of a recovery here? The market has so many great opportunities that I am tempted to salvage what I can frommVa Tech and deploy it in some growth ideas